Why the USMCA Matters for North America’s Economic Future

The USMCA is the operating system for North American production, investment, talent, and digital commerce. Canada, Mexico, and the United States should renew the agreement and explore ways to update it to preserve certainty, deepen regional supply chains and innovation capabilities, and strengthen the continent’s ability to compete with China.

KEY TAKEAWAYS

Key Takeaways

Contents

Background: The Importance of a North American Economic Bloc. 4

Why CUSMA Matters for Canada. 12

Why T-MEC Matters for Mexico. 17

Why THE USMCA Matters for the United States 22

Introduction

The 2026 review of the United States-Mexico-Canada Agreement (called the USMCA in the United States, CUSMA [Canada-United States-Mexico Agreement] in Canada, and T-MEC [Tratado entre México, Estados Unidos y Canadá] in Mexico) represents a test of whether North America can preserve the production scale, technological capacity, and investment certainty needed to compete in a global economy increasingly shaped by Chinese mercantilism, industrial policy, and supply-chain fragmentation. The USMCA began as a modernization of the North American Free Trade Agreement (NAFTA), but it now functions as the institutional foundation for a North American production system spanning more than 500 million citizens, nearly one-third of global gross domestic product (GDP), and almost $2 trillion in annual trade.

The central question for policymakers is whether Canada, Mexico, and the United States can use regional integration to strengthen productivity, innovation, and economic security. Canada brings energy, critical minerals, advanced manufacturing, and defense-industrial depth. Mexico provides manufacturing scale, engineering talent, logistics capacity, and a platform for nearshoring production away from China. The United States anchors the region with market size, capital, technology leadership, and advanced industries. Together, these assets give North America a scale advantage none of the three countries can achieve alone. The USMCA contributes to anchoring a “factory North America” that can effectively compete with China.

Uncertainty over renewal, tariffs, rules of origin, or bilateral side deals risks delaying investment at the very moment North America has an opportunity to capture supply chains leaving China and other distant production hubs.

Viewed from all three national perspectives, the USMCA’s greatest value is predictability. Firms invest, hire, build supplier networks, and reorganize production only when trade rules are stable. Uncertainty over renewal, tariffs, rules of origin, or bilateral side deals risks delaying investment at the very moment North America has an opportunity to capture supply chains leaving China and other distant production hubs.

The agreement also matters because North American trade is highly strategic, as key industries depend on the cross-border movement of inputs, workers, data, and capital. These flows are the source of regional scale. A vehicle assembled in one country may incorporate parts, engineering, software, and materials from the other two countries. Likewise, digital trade rules allow companies to serve customers across borders, protect source code, and avoid costly data-localization mandates. Weakening the USMCA would therefore reduce competitiveness across the continent, raise costs for producers and consumers, and create openings for China and other competitors. It would also undermine the region’s ability to translate allied production into economic power.

This report explains why renewal matters from Canadian, Mexican, and U.S. perspectives, then identifies the policy choices negotiators should prioritize to preserve North America’s competitiveness while updating the agreement for the next decade. It reflects the shared view of the authors at the Macdonald-Laurier Institute’s Center for North American Prosperity and Security (CNAPS) in Canada, the Information Technology and Innovation Foundation (ITIF) in the United States, and Fundación IDEA in Mexico that CUSMA/T-MEC/USMCA should be renewed and modernized rather than allowed to drift into uncertainty. Each country has distinct priorities and political constraints, yet all three benefit from a rules-based framework that supports investment, supply-chain integration, digital commerce, and strategic production. The task for policymakers is to preserve tariff-free regional trade where it strengthens competitiveness, address legitimate irritants, and update the agreement for the next decade of geopolitical and technological competition across North America.

Background: The Importance of a North American Economic Bloc

The USMCA covers one of the largest economic regions in the world, representing more than 500 million people and accounting for almost 30 percent of global GDP.[1] Since the trade agreement was enacted in 2020 to replace NAFTA, goods and services trade within the region has increased by 37 percent, reaching an estimated $1.93 trillion in 2024.[2] The USMCA provides the foundation of North American coproduction in industries such as agriculture, automotives, and medical devices, and its continuity is central to the United States’ techno-economic power. Beyond facilitating trade and cross-border investments, the agreement also expands access to markets, talent, and resources, extending each country’s economic capacity well beyond what any of the three nations could achieve independently. A breakdown of the USMCA would weaken the global competitiveness of American—and North American—goods, creating openings for adversaries such as China to expand their already significant share of global markets, especially in advanced-technology industries.

Since the trade agreement was enacted in 2020 to replace NAFTA, goods and services trade within the region has increased by 37 percent, reaching an estimated $1.93 trillion in 2024.

The USMCA as a Counterweight to China

One of the greatest achievements of the USMCA, and its predecessor NAFTA, has been the localization and continental integration of markets and supply chains. By granting tariff-free access to American, Canadian, and Mexican inputs that meet rules-of-origin thresholds, the USMCA creates a structural incentive for North American firms to replace international imports with regionally produced alternatives.[3] Specifically, preferential market access within the USMCA weakens the attractiveness of Chinese inputs that would otherwise undercut domestic alternatives on cost. This encourages nearshoring and helps weaken China’s manufacturing capacity. Without the USMCA, the tariff and market access incentives that make nearshoring and regional sourcing competitive would disappear, leaving firms little reason to choose North American suppliers over cheaper Chinese alternatives.

Although the USMCA enables companies to gain preferential access to the U.S. market without investing directly in the United States, for instance through production in lower-cost Mexico, regional production represents a significantly more favorable outcome than offshoring to China does. Increased Chinese production not only raises strategic concerns about bolstering an adversary’s manufacturing capacity, but also yields minimal economic returns. Because roughly 40 percent of the inputs to Mexican finished goods originate in the United States, every dollar spent on Mexican imports returns approximately 40 cents to the U.S. economy. In contrast, every dollar spent on Chinese imports returns just four cents.[4] In this context, the United States has a compelling interest in regionalizing production, regardless of whether it occurs on American soil or in another USMCA country.

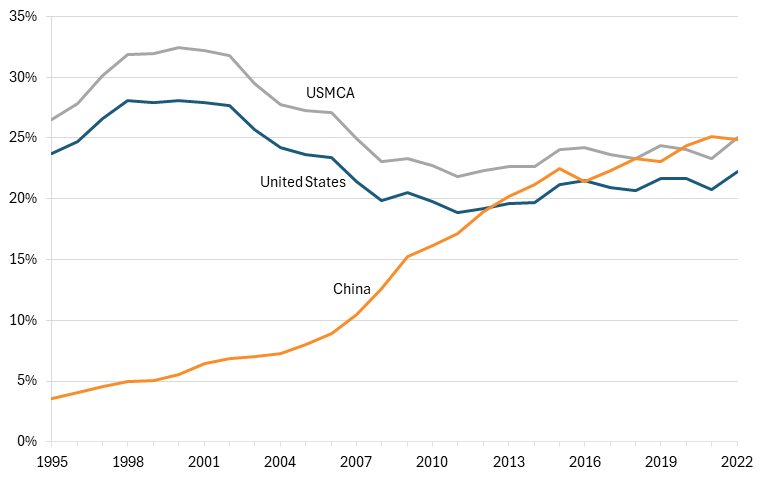

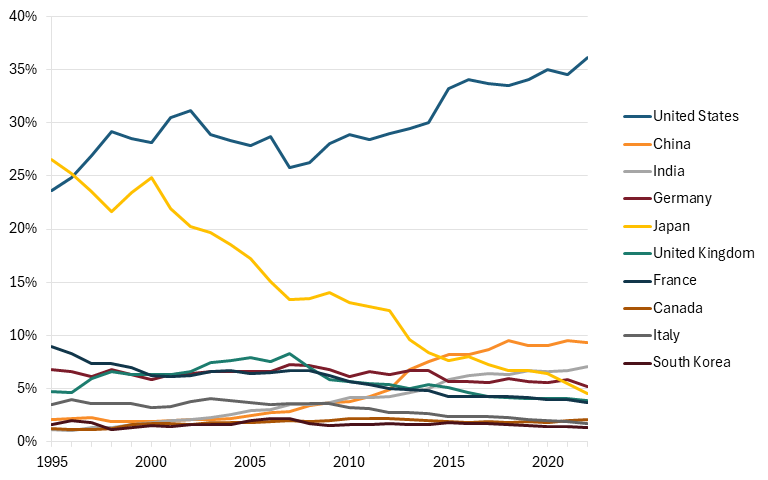

North American companies depend on the USMCA’s mobility and efficiency gains to compete globally, particularly against Chinese companies that benefit from state-sponsored mercantilist protections. Absent access to Mexico’s lower-cost production environment and science, technology, engineering, and mathematics (STEM) talent pool, or Canada’s abundant natural resources and strengths in quantum technologies and aerospace, many American companies would struggle to stay competitive.[5] As ITIF has shown, China already outperforms the United States and its neighbors across several strategic sectors—and without an integrated North American production system, the gap would be even wider.[6] Figure 1 shows that, on its own, the United States’ share of global output across 10 strategic sectors (pharmaceuticals; electrical equipment; machinery and equipment; motor vehicle equipment; other transport equipment; computer, electronic, and optical products; information technology (IT) and information services; chemicals; basic metals; and fabricated metals) is 3.1 percent lower than China’s. However, with the USMCA, the gap with China is reduced to only 0.3 percentage points.

Figure 1: Select regions’ shares of global output in strategic sectors,1995–2022[7]

The USMCA for Regional Competitiveness: Case Studies

Tariff reductions and eliminations on USMCA-qualifying goods have encouraged North American firms to capitalize on the complementary economic advantages of each member country, resulting in deeply integrated production networks across industries and increased intra-industry trade. This enables companies in the region to maintain efficient manufacturing processes, lowering domestic consumer prices while remaining competitive in global markets.[8] North American firms rely on the mobility and access provided by the USMCA, and uncertainty surrounding the trade agreement risks discouraging investment and weakening regional competitiveness.

The Automotive Industry

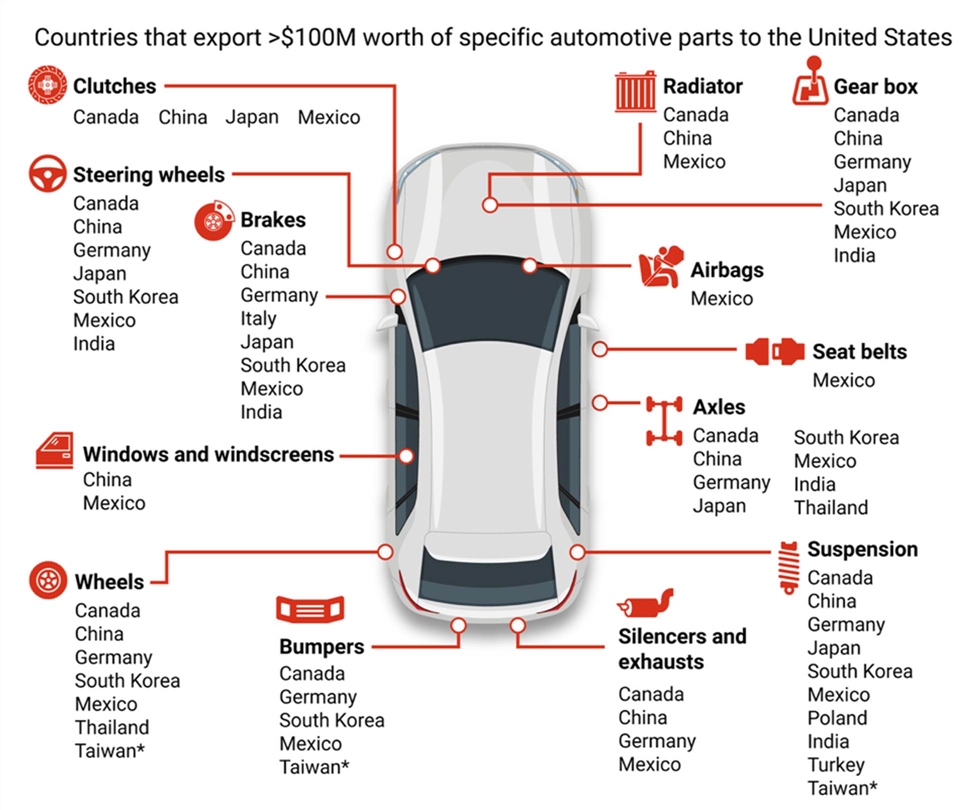

Automobile manufacturing is one of the most important industries in North America, with total auto trade accounting for the largest share of USMCA trade at 22 percent.[9] North America is the third-largest producer of motor vehicles in the world after China and the EU, and the industry employs roughly 3.3 million people across the region.[10] The USMCA and NAFTA free trade provisions have encouraged firms in the industry to organize production according to each country’s comparative advantage, with U.S. auto companies sourcing inputs from across the USMCA and beyond. (See figure 2). Within the region, some auto components cross borders up to eight times before reaching final assembly.[11] Absent the USMCA, tariffs accumulated at each border crossing would render automotive production in the United States economically unviable, particularly as competition from low-cost Chinese producers drives down global prices.

Figure 2: From where the United States sources auto parts imports[12]

Semiconductor Production

While semiconductor production is highly globalized, the success of the North American semiconductor industry depends heavily on regional market access and talent mobility enabled by the USMCA. Several U.S. semiconductor companies have design and research and development (R&D) facilities in Canada and back-end facilities in Mexico, with subcomponents routinely crossing USMCA borders before being integrated into final goods such as automobiles and consumer electronics.[13] The agreement also plays a crucial role in strengthening the cost competitiveness of North American investments and facilitating the export of U.S. semiconductors not only to Canada and Mexico but also to markets throughout the Americas.[14] Reliable cooperation with Mexico and Canada on skills development, trade, and assembly, testing, and packaging (ATP) capacity are essential to reducing reliance on Asia for semiconductor manufacturing.[15]

Foreign Investment

Beyond trade, the USMCA underpins one of the world’s largest cross-border investment relationships, providing a predictable, rules-based environment for investing across North America. In 2022, U.S. direct investment in Canada and Mexico totaled $569 billion, while investment from those two countries into the United States reached roughly $623 billion.[16] Data from the United Nations Conference on Trade and Development suggests that, since the implementation of the USMCA, foreign direct investment (FDI) in North America has increased by 16 percent.[17] While the United States remains the world’s top FDI destination, Canada has climbed from 10th to 6th place globally since 2019.[18] Mexico has similarly benefited from the agreement and its implications for nearshoring, with new FDI into the country increasing one year into the USMCA and total FDI growing 10 percent year-on-year in 2025.[19] The United States is Mexico’s main source of foreign investment, representing 45 percent of total FDI since 2017 and an estimated 3.4 percent of Mexico’s GDP in 2024.[20] However, recent turbulence in U.S. trade and tariff policy has dampened investment flows across the region, and rising anxiety ahead of the agreement’s review risks further intensifying this trend.[21]

Since the implementation of the USMCA, FDI in North America has increased by 16 percent.

Jobs and the North American Workforce

The USMCA offers significant benefits for job creation, with workers across North America relying on the agreement and the trade it enables for their livelihoods. While estimates of the number of jobs supported by the USMCA vary widely, a study by the Wilson Center suggests that USMCA-enabled trade led to a 32 percent increase in job creation between 2020 and 2022, supporting nearly 17 million jobs across the region.[22] Another study by the U.S. Business Roundtable finds that more than 13 million American jobs depend on trade with Canada and Mexico.[23] Overall, trade with Mexico and Canada is responsible for roughly one-third of all U.S. export-supported jobs.[24] While this represents a small portion of total U.S. jobs, at less than 2 percent, manufacturing is an overrepresented industry in export-supported jobs, accounting for approximately one-quarter of USMCA-supported U.S. jobs.[25] A potential failure to renew the agreement might put up to 13 million American jobs at risk, disproportionately impacting manufacturing workers—an outcome at odds with the current administration’s stated goals.

The USMCA also plays an important role in expanding the available talent pool beyond what any single member country could develop on its own, thereby creating a North American workforce. This is an area of growing importance for the United States as competition with China intensifies in strategic sectors and for highly skilled workers, and as a growing number of scientists leave the United States to work in China.[26] The USMCA provides American companies with broader access to valuable talent across Mexico and Canada, particularly in STEM fields where domestic supply increasingly falls short.[27] Canada and Mexico not only produce a higher proportion of annual STEM graduates than the United States does, with STEM majors accounting for 26 percent of total graduates in Canada and only 20 percent in the United States, but they also enjoy a higher proportion of graduates with backgrounds in engineering, manufacturing, or construction.[28] Mexican universities graduate more than twice the share of students in engineering, manufacturing, and construction as do their American counterparts. (See figure 3).[29] When it comes to R&D personnel, the United States led China by roughly 100,000 enrolled Ph.D. students in 2023.[30] Through the USMCA, Mexico and Canada added approximately 123,000 more doctoral students—widening North America’s collective edge over China in the pipeline of future R&D talent. (See figure 4.) Easy access to this workforce is critical for the continued competitiveness and innovation capacity of American, Canadian, and Mexican companies.

A potential failure to renew the agreement might put up to 13 million American jobs at risk, disproportionately impacting manufacturing workers.

Figure 3: Share of engineering, manufacturing, and construction graduates from tertiary education by country (2013–2023)[31]

Note: Missing values for select years estimated via linear interpolation.

Figure 4: Number of students enrolled in doctorate programs by country (2023)[32]

Negotiation Pathways

It remains unclear how the trade partnership between the three countries will evolve. Under Article 34.7 of the USMCA, Canada, Mexico, and the United States were required to decide by July 1, 2026, whether to extend the agreement, with or without revisions, or to let it lapse in 2036.[33] Three possible pathways were agreed to in advance:

▪ All parties agree to extend: If all parties agree to extend, the agreement would be in place for another 16 years, until 2042. In 2032, there would be another review to determine whether to extend for an additional 16 years.

▪ At least one country does not agree to extend: If the parties do not agree to extend the agreement, the agreement would remain in effect but be subject to annual reviews for the next 10 years. At any point, these reviews could result in a renewed deal, but if they do not, the USMCA would sunset on July 1, 2036.

▪ At least one country withdraws: Parties to the USMCA would have the right to withdraw from the agreement at any point with at least six months’ notice.

Indeed, the U.S. government chose the path of no extension. On July 1, 2026, the Office of the U.S. Trade Representative (USTR) issued a statement noting that “the United States did not agree to renew the USMCA in its current form.”[34] This means that the U.S. government has opted, instead of renewals, for annual reviews of the trade agreement. Under this scheme, the USMCA remains in effect until 2036. In practice, this means that the three countries will continue the renegotiation path.

In recent trade negotiations, the Trump administration has favored bilateral agreements over multilateral deals. So far, Washington has conducted only bilateral informal talks regarding the extension, and Canadian leadership has indicated that bilateral agreements will accompany the USMCA.[35] Bilateral agreements are possible in all three extension scenarios.

▪ Parallel bilateral agreements: Vienna Convention Articles 30 and 41 state that countries may have bilateral agreements outside a preceding multilateral agreement as long as the provisions of the bilateral agreement do not impinge on their responsibilities to other parties as outlined in the prior multilateral agreement or change the treaty’s purpose or agreement.[36] This means that, with the USMCA still in force, with or without extension, Mexico, Canada, and the United States could make bilateral agreements on issues not covered in the USMCA, such as critical minerals, defense procurement, and the governance of artificial intelligence (AI) or on issues that don’t impact the third country.

▪ Bilateral agreements that supplant or supersede the USMCA: However, many of the substantive issues on which the countries disagree are discussed in the current USMCA text, meaning that all three would need to agree to remove the existing provisions from the text to allow for bilateral agreements to prevail, or the countries would need to withdraw from the agreement altogether.

How Might Key Issues Be Resolved in Renegotiations?

Both Canada and Mexico have signaled their interest in renewing the USMCA with minimal adjustment.[37] The United States, on the other hand, has sent mixed signals, with President Trump telling reporters that the United States is “not looking to renew” the USMCA, while Canadian prime minister Mark Carney reported that American negotiators would like to avoid the kind of substantive changes that would send the agreement to Congress for approval.[38]

Congress has authority under Article I, Section 8 of the U.S. Constitution to “regulate commerce with foreign nations,” but until 2021, it delegated some of its decision-making authority over trade agreements to the executive branch through Trade Promotion Authority. The authority has since expired, raising questions about whether adjustments to the deal’s architecture would require greater congressional involvement.[39]

The most significant points of contention over the status quo involve automotive rules of origin, steel and aluminum tariffs, agriculture, and the relationships Mexico and Canada have with China.

Automotive rules of origin that require certain percentages of North American content are the most likely point of substantial departure from the existing architecture. The original USMCA negotiations raised the automotive rules of origin from the 62.5 percent required under NAFTA to 75 percent. American negotiators have proposed even higher content requirements and, in an effort to reshore American manufacturing, have floated new thresholds for content specifically from the United States.[40]

The most pressing agricultural negotiation concerns Canadian dairy import quotas, established in the original 2020 agreement to allow American farmers to import their cheaper dairy products into Canada without harming the Canadian dairy industry. Americans complain that Canada almost never meets this quota and want better access to the Canadian market.[41]

Steel and aluminum tariffs have also been a sticking point, though they operate largely outside of the USMCA. The United States has imposed 50 percent Section 232 tariffs on steel and aluminum, which cut Mexican steel exports by 37 percent.[42]

Finally, the United States has taken issue with Canada’s and Mexico’s relationships with China, including Canada’s strategic partnership with China and concerns about transshipment through Mexico.[43] The USMCA already includes a nonmarket economy clause, which allows any party to terminate the agreement if another party enters into a free trade agreement with a nonmarket economy.[44]

The USMCA could be modified using several instruments that would require varying levels of negotiating intensity.

The first is to write additional side letters, which can add new provisions to the agreement or clarify existing provisions without rewriting the USMCA text. There are currently 12 side letters attached to the USMCA, on topics ranging from Section 232 tariffs to the protection of natural water resources.[45] For agreements involving digital trade and critical minerals, which are absent or only partially covered in the USMCA text, we may see the United States, Mexico, and Canada negotiate parallel side letters. Side letters may also be used to add strictly bilateral commitments or clarifications to the USMCA, which we may see for issues such as Canadian dairy quotas. An even softer mechanism would be a memo of understanding that does not become part of the formal agreement but could outline changed expectations for trade operations.

Side letters can be useful tools, but they should not be treated as a substitute for formal amendments when the parties seek to change core obligations, such as rules of origin, dispute-settlement procedures, or market-access commitments. Bilateral side letters are most appropriate when they address issues not covered by the agreement or when they do not alter the third party’s rights or obligations.

The most difficult instrument to implement would be a protocol of amendment, which directly changes the text of the existing agreement. If one of the countries pursues an amendment protocol, these more significant changes might require congressional review. Changes to procedures, such as the Rapid Response Mechanism for labor disputes or the dispute resolution process, would likely require an amendment protocol.

Negotiators might also amend the agreement’s annexes, which outline additional rights and obligations for specific sectors such as cosmetics, pharmaceuticals, and information and communication technology.[46] Amendment to these annexes would likely require congressional input, but addressing their implementation and regulatory compatibility can be done with a lighter touch. In their meetings on June 15–17, 2026, negotiators from the United States and Mexico agreed to create a committee to review the sectoral annexes.[47]

Many believe the most likely path forward is to adjust the agreement using instruments that do not require changes to the agreement’s text.[48] Given the support for the agreement among the Republican majority in Congress and the existing tensions between the president and congress over U.S. legislation, a battle over formal amendments to the USMCA could be quite lengthy and contentious.

As discussed earlier, however, it is not completely out of the realm of possibility that the USMCA could be renegotiated altogether. As with the transition from NAFTA to the USMCA, a new agreement might keep many of the existing chapters but exact compromises from Canada or Mexico on agriculture, tariffs, and rules of origin.[49] Negotiators would have until 2036 to iron out such an agreement before the USMCA sunsets, but lengthy negotiations would create a highly unstable business environment that would discourage investment and production.

Even more unlikely, but not impossible, would be the expansion of the USMCA to include current CAFTA countries.[50] Most analysts and industry insiders believe that the USMCA has been quite successful, and an “enlisted and expanded” Western Hemisphere might be one that draws Central American and Caribbean neighbors into a fully integrated trading system.[51]

A failure to extend would not immediately terminate the agreement, but annual reviews would create a rolling uncertainty tax on North American investment. That would be especially damaging for autos, semiconductors, critical minerals, logistics, advanced manufacturing, and digital services—sectors wherein firms make multi-year capital commitments.

Why CUSMA Matters for Canada

While many observers initially viewed CUSMA as a modest update to NAFTA rather than a transformational trade agreement, its greatest contribution has been preserving the integrated North American economy amid growing protectionism and geopolitical competition.

Historical Context

Canada stands among the world’s most trade-dependent economies, with the United States serving as its largest export market and it serving as America’s largest customer.

Canada and the United States have a long history of integrated trade. The lesson of World War II for the growing American superpower was that having a trusted, stable secondary source of the inputs needed by the defense industrial base was crucial to achieving a successful wartime footing. Starting in 1940, Canada and the United States began working together to support one another’s war efforts. In 1956, Canada and the United States signed the Defense Production Sharing Agreement (DPSA), which, among other things, allowed Canadian companies to be treated as American when competing for defense contracts. Canada and the United States have entered into many defense production agreements in the years since, but the DPSA was the first major step in recognizing mutual reliance and the strength of diversity in supply chains stemming from geographically proximate allied production.[52]

The post-World War II era also saw America begin to rely on Canada for quick access to many of the things the economy urgently needed to accommodate a booming population and hot economic growth, and likewise, Canada’s post-war baby boom prosperity inspired new imports from the growing American production powerhouse.

As both countries grew, the 1965 Auto-Pact ensured Canada would gain a foothold in the U.S. car manufacturing industry in exchange for preferential market access for some American vehicles. The Auto-Pact had many evolutions before it was eventually replaced entirely, but this initial policy agreement has left a lasting legacy: Canada remains the largest foreign market for American vehicles.[53]

NAFTA allowed Canadians to experience lower prices and faster shipping on a variety of American and Mexican goods. This directly improved the quality of life in Canada in small but important ways, such as increasing year-round access to a variety of fresh fruits and vegetables. It further generated economic investment in Canada, provided Canadian businesses with the opportunity to compete fairly with American and Mexican counterparts, and led to a modern trade-rules framework that allowed for greater market certainty.

NAFTA was not perfect, however, and the USMCA agreement, which replaced NAFTA, sought to address trade irritants, such as increasing American rules-of-origin requirements, addressing perceived protectionist policies and subsidies for business in Canada and Mexico, as well as creating fewer loopholes for wage discrepancies across the three continents.

Throughout this history of trade, Canada and the United States grew ever closer. Supply chains organically formed due to geographical proximity.

Canada has benefited immensely from the USMCA and the increased integration of the North American market that preceded it. One in five (or approximately four million) Canadian jobs are dependent on Canada’s exports, and 70 percent of Canadian exports are bound for the United States.[54]

Direct access through the agreement provides trade certainty, encourages investment, reinforces North American supply chains, includes trade rules for a digital era, and establishes a stable framework for future economic cooperation.

The Current State of Canada-U.S. Relations

In November 2024, President-elect Trump threatened to slap Canada and Mexico with a 25 percent across-the-board tariff and a 10 percent tariff on energy and critical minerals. The president went on to fluctuate and change the different tariff amounts and the covered and exempt goods for the first year of his presidency, almost on a whim.

At first, the Canadian response was a charm offensive, led by then-Prime Minister Justin Trudeau, who flew to Mar-a-Lago to have dinner with President Trump. Unfortunately, the president is reported to have made a joke that if Canada suffered economic ruin because of tariffs, they could become the 51st state.[55] The idea of Canada joining the United States soon became a theme in presidential rhetoric about Canada.

The annexation rhetoric from the White House, combined with prevarication about taking over Greenland for Arctic security, led Canadians to feel fear of another country. Worse was the perception of betrayal by an otherwise stalwart ally upon which much of the Canadian economy depends. By June 2025, 59 percent of Canadians considered the United States a “threat.”[56]

While the election of Mark Carney in May 2025 and the global tariffing of countries beyond Canada have calmed the situation, president Trump has continued, on occasion, to say publicly that he still wants to exit CUSMA. There is also no relief in sight for the 232 sectoral tariffs on Canadian exports, despite CUSMA.

Canada is now entering a once-unthinkable scenario, as privileged access to the American economy and seamless integration of its supply chains with the United States are viewed by some as a major liability. The stable trade and mutual prosperity that flowed north and south, taken for granted for decades, are now being reconsidered on both sides of the border. The future of tariff-free North American trade is increasingly uncertain.

CUSMA Provides Trade and Investment Certainty

Perhaps the greatest benefit of CUSMA has been the certainty it has provided to businesses and investors through stable, reliable access to the U.S and Mexican markets. Capital follows certainty, and the attractiveness of the North American market for external investment, including in the United States, has been primarily due to investors’ ability to count on the continent’s predictable investment rules.

Indeed, during the 2017–2020 renegotiation of NAFTA, uncertainty regarding the future of North American trade policy caused many firms to postpone investment decisions until the terms of a successor agreement became clear. A Brookings article notes that “the private sector paused investment until the outcome was clearer, and risk could be estimated,” underscoring the economic value of predictable trade rules.[57]

We have already seen in Canada what the uncertainty from the CUSMA review and the Section 232 tariffs have wrought on the Canadian economy. Since threatening tariffs in November of 2024 as President-elect Donald Trump initiated a campaign that upset the predictable nature of rules-based trade. Since then, Canada’s economic growth has slowed in all regions except Alberta and Saskatchewan, whose main exports to the United States, energy and critical minerals, are fully exempt from American tariffs (and likely to remain so).

CUSMA has provided blanket protection against the shocks of earlier iterations of across-the-board tariffs, such as the International Emergency Economic Powers Act (IEEPA) tariffs and the Section 301 tariffs (as of this writing). However, provinces with a larger share of goods production subject to Section 232 tariffs have fared worse than have their less-exposed counterparts. Ontario and Quebec, both home to steel, aluminum, and auto industries, have been hit hardest by the tariffs.[58]

By June 2026, Canada had entered a technical recession, felt more acutely in the provinces most exposed to tariffs. However, the preservation of the CUSMA exemption on most goods, combined with the higher tariffs faced by other countries globally, has still given Canada a competitive advantage in cost and access to the American market.

Until the USMCA review is completed, many businesses are concerned that the uncertainty will continue to make planning difficult. The Canadian government is under significant pressure from businesses to strike a deal with U.S. president Trump to lock in certainty on the USMCA.

The Canadian government has held that it would be more harmful to Canada in the long term to make a bad deal quickly than to take time to negotiate a better one. The Section 232 sectoral tariffs on Canadian products, imposed despite CUSMA, have already seriously harmed Canadian businesses, and the Canadian federal government has moved to provide financial support to hard-hit industries to weather the storm. Despite this, businesses are feeling pressure. Quebec’s representative to the United States called for the federal government to end the uncertainty and make a deal with the Trump administration.[59] In response to the 232 sectoral tariffs, Canada retaliated with a 25 percent reciprocal tariff on American-made steel, aluminum, and non-CUSMA-compliant American-made autos.[60]

Businesses cannot plan expenditures, expansions, investments, or hiring without having certainty about how tariffs will potentially impact markets in the future. The degree to which Canada agrees on a good or bad deal may well rest on how long Canadian businesses can weather this uncertainty storm brought on by the presidential tariff decisions.

The Specter of the End of the USMCA Demonstrates Its Strength

The current low state of Canada-U.S. relations has led many Canadians to question Canada’s economic integration and dependence on the United States, a relationship that previously proved profitable for Canada. Some have questioned why Canada should continue with the agreement when the United States has moved to impose tariffs on Canada anyway.

A canceled CUSMA would subject Canada’s highly exposed and integrated economy to an across-the-board tariff imposed by the United States, as other countries now face. In exchange for certainty, other economies have opted to enter into tariff agreements. Canada, however, is deeply exposed to the American economy and cannot afford to make a bad deal—or any deal—that would impose across-the-board tariffs.

By looking at how detrimental the 232 sectoral tariffs have been to Canadian businesses, one can project the problems that would be faced by increased prices in the United States and what that might mean for Canadian businesses.

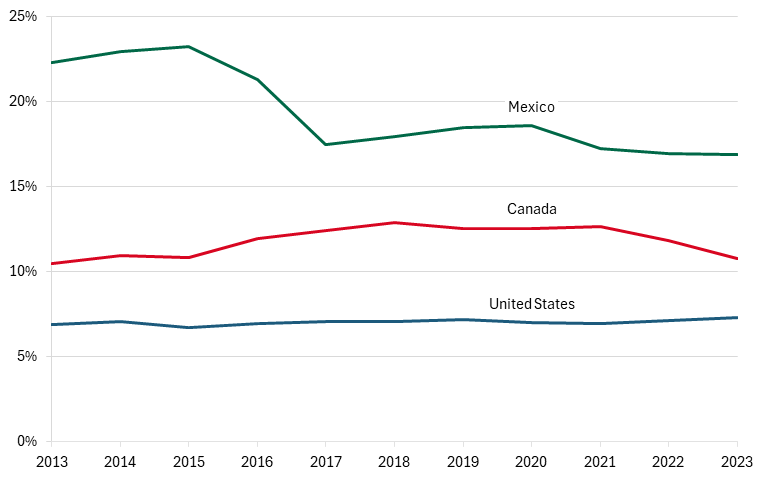

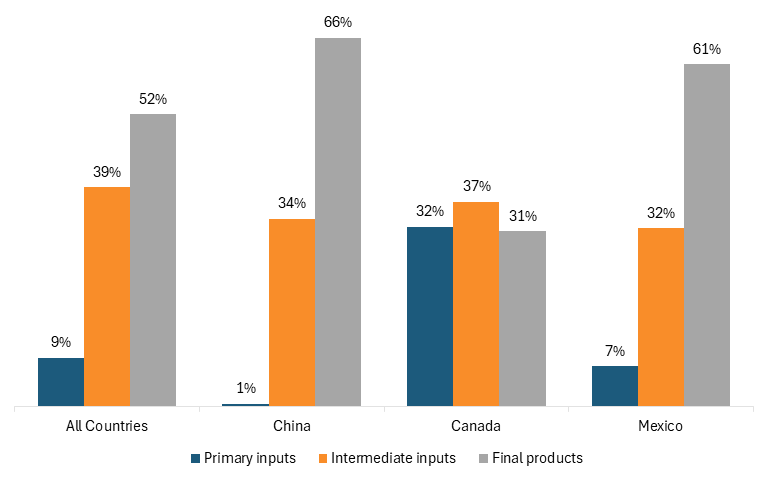

But further, increased tariffs on Canada would equally hurt economic growth in the United States. As CNAPS points out, more than two-thirds of the goods the United States imports from Canada are primary inputs (32 percent) or intermediate inputs (36 percent).[61] Only 31 percent of what the United States imports from Canada is finished goods. This means that most American tariffs on Canadian goods will increase the costs borne by American producers and manufacturers that rely on Canadian primary and secondary inputs.

Figure 5: Composition of goods imports into the United States by country

Most of these inputs are not easily replaced or sourced in the United States. For example, Canadian heavy-sour crude is required in many American refineries to offset American light-sweet crude in the chemical refining process. America is not a significant source of certain critical minerals or rare earth elements, which must be imported.

Further, exiting CUSMA would result in a period of trade chaos while a lengthy bilateral agreement is negotiated between Canada and Mexico and, more crucially, between Canada and the United States. While Canada and Mexico may agree on free trade, Canada has very little exposure to Mexican exports. Access to trade with the United States, on the other hand, is existential to the Canadian economy.

CUSMA Strengthens North American Supply Chains and Attracts Investment to Canada

A major benefit is that CUSMA reinforces North American production networks and supply chains. Modern North American manufacturing depends upon integrated supply chains that cross borders multiple times before a finished product reaches consumers. Canadian automotive, aerospace, energy, agricultural, and advanced manufacturing sectors all rely heavily on this continental production model in which primary and secondary manufacturing inputs cross the border several times before becoming part of a finished product.

The USMCA’s updated rules of origin encourage companies to source more components from North America rather than overseas suppliers. While these provisions increase compliance requirements, it has the correlated effect of incentivizing manufacturing firms to locate new investment within Canada, the United States, and Mexico.

The ability to source inputs across three geographically proximate countries, with standardized trade rules and an economically robust base capable of purchasing finished products, is a strong pull factor for onshoring FDI.

The Macdonald-Laurier Institute and CNAPS argue that North America should increasingly view economic integration through the lens of economic security. Their “Grand Bargain” proposal contends that resilient continental supply chains for energy, critical minerals, semiconductors, and advanced manufacturing improve both economic competitiveness and national security.[62]

Modern Trade Rules for a Digital Economy

Modern businesses run on data. Every time a laptop is turned on, a credit card is swiped, or a bank transaction occurs, data exchanges hands. A tariff on digital services, something once too incalculable to consider, is now something that, with the advent of AI, could be implemented by countries in the name of digital sovereignty. A threat to tariff digital exchange would be a significant blow to Canada (and the United States), which has been a great incubator of modern digital services companies.

The agreement includes one of the world’s most comprehensive digital trade chapters, protecting cross-border data flows, limiting unnecessary data-localization requirements, recognizing electronic signatures, and facilitating digital commerce.

These provisions particularly benefit Canadian services industries, technology companies, and small businesses that increasingly rely upon digital platforms to reach North American customers.

The agreement also improves transparency, customs procedures, and regulatory cooperation, reducing administrative burdens for small and medium-sized enterprises that historically have faced disproportionately high compliance costs.

Nonetheless, these rules do need to be updated. In 2025, Canada repealed its recently enacted Digital Services Tax, over which it faced a trade tribunal challenge from the USTR. The challenge largely centered on discrimination against American companies rather than on any specific digital exemptions in the agreement, demonstrating that CUSMA, although imperfect, does have first-principles provisions that have been useful in securing the digital economy.[63]

CUSMA Protects Canada

Perhaps the strongest argument for CUSMA is not what it changes but what it prevents.

International trade has become increasingly shaped by tariffs, industrial policy, export controls, and geopolitical competition. Canada remains particularly vulnerable to American tariff decisions because nearly three-quarters of its exports are destined for the United States.

CUSMA does not eliminate trade disputes, but it does provide institutional mechanisms—including consultation procedures and dispute settlement—that help resolve disagreements before they evolve into prolonged trade wars.

CUSMA’s dispute settlement mechanism reduces the potential for lengthy trade conflicts. By pre-agreeing on a set of rules to govern their trade, the three countries have provided a strong framework that outlines acceptable and unacceptable activities. The predictability and negotiation of the trading rules between countries result in fewer legal disputes and, therefore, more trade access for selling products in one another’s economies.

While Canada remains particularly vulnerable to American tariff decisions, CUSMA has offered a blanket of protection for the vast majority of its goods destined for the United States. Further, diversifying trading partners is not an “either-or” strategy but rather an “either-and” strategy, recognizing that the two economies will always be intertwined and will, to some degree, rise and fall with one another’s success.

As North America approaches future reviews of the agreement, policymakers should prioritize strengthening continental competitiveness, energy security, digital commerce, and strategic supply chains rather than reopening settled market-access negotiations. In this respect, CUSMA should be understood not merely as a trade agreement but as the economic foundation of North American prosperity and security.

Why T-MEC Matters for Mexico

For Mexico, the 2026 review and reauthorization of T-MEC is not a routine trade-policy exercise. It is a strategic decision that will shape the country’s export model, industrial transformation, geopolitical positioning, and long-term competitiveness within North America. Since the agreement entered into force in 2020, Mexico has consolidated its position as the United States’ top trading partner and one of the principal beneficiaries of global supply-chain realignment. The agreement now underpins Mexico’s role as a manufacturing, logistics, and investment platform for the North American market.

The U.S.-China trade war, geopolitical fragmentation, industrial policy competition, and the acceleration of nearshoring have transformed North America from a traditional free-trade region into a strategic economic bloc. Mexico is now central to this transition.

The importance of reauthorization has grown because the global context has fundamentally changed since T-MEC negotiations concluded in 2019. The U.S.-China trade war, geopolitical fragmentation, industrial policy competition, and the acceleration of nearshoring have transformed North America from a traditional free-trade region into a strategic economic bloc. Mexico is now central to this transition. Reauthorization, therefore, matters not only because it preserves tariff-free access, but also because it determines whether North America can continue to function as an integrated production platform capable of competing with China and other emerging industrial powers.

In this context, T-MEC increasingly functions not only as a trade agreement but also as the institutional architecture supporting North American economic security. As geopolitical fragmentation accelerates and supply-chain vulnerabilities become more visible, the agreement provides a framework for the region to reduce dependence on external suppliers in strategically sensitive industries, including semiconductors, electronics, medical devices, automotive components, and critical manufacturing inputs.[64]

At the same time, uncertainty surrounding the review process already risks discouraging investment and slowing the relocation of supply chains into Mexico. For Mexico, timely reauthorization is critical because investment decisions in sectors such as automotive, semiconductors, logistics, energy, and advanced manufacturing are being made now, not after 2026.

T-MEC as the Foundation of Mexico’s Export Economy

Mexico’s economic model is deeply tied to North American integration. Total Mexican trade has exceeded $1 trillion in recent years, while exports reached approximately $600 billion in 2023.[65] The United States absorbs roughly 80 percent of Mexican exports, making preferential access to the U.S. market indispensable to Mexico’s macroeconomic stability and industrial growth.[66]

At the same time, Mexico has consistently remained one of the United States’ two largest trading partners. In 2024, Mexico was the largest source of U.S. imports and the second-largest destination for U.S. exports, underscoring how North American production systems depend on reciprocal trade flows rather than on unilateral export dependence. U.S. exports to Mexico include machinery, electrical equipment, vehicles, plastics, energy products, and more than $30 billion in agricultural goods, while Mexico’s exports to the United States are concentrated in vehicles, electronics, machinery, medical devices, and agricultural products.[67]

T-MEC preserves the tariff-free treatment of originating goods and provides the legal certainty necessary for integrated manufacturing across the region.[68] These rules are especially important for Mexico because its competitive advantage depends not only on lower production costs but also on the ability to participate seamlessly in cross-border production networks.

The automotive industry illustrates this integration clearly. Automotive components can cross the Mexico-U.S. border seven or eight times before a vehicle is completed.[69] Without T-MEC protections and customs coordination, these repeated border crossings would become economically inefficient and undermine the competitiveness of North American production as a whole.

North American manufacturing integration is significantly deeper than traditional trade relationships with external competitors. As noted, estimates indicate that every dollar of U.S. imports from Mexico contains approximately 40 cents of U.S. content, compared with only 4 cents in imports from China.[70] This reflects the existence of highly integrated regional production systems in sectors such as automotive manufacturing, electronics, aerospace, and medical devices where production is distributed across all three North American economies rather than concentrated in a single export platform.

Mexico’s competitive position increasingly depends on industrial ecosystems that combine manufacturing scale with technical specialization. In northern industrial corridors such as Tijuana, firms operate within dense supplier networks and benefit from growing pools of engineering and technical talent tied to aerospace, medical-device, and electronics clusters. Tijuana alone hosts more than 600 suppliers within a 50-mile radius and produces approximately 8,000 engineering graduates annually, supporting advanced industrial operations rather than purely low-cost assembly activities.[71]

Since NAFTA and later T-MEC, Mexico has evolved from a low-cost assembly platform into a strategic manufacturing hub. Mexico is currently the world’s third-largest automotive exporter, 4th-largest exporter of medical devices, and 10th-largest exporter of electronics.[72] The country also increased its economic complexity ranking from 30th globally in 1995 to 21st in 2022, reflecting its growing capacity in advanced manufacturing and industrial production.[73]

The review process matters because it will determine whether Mexico can continue consolidating this transition toward higher-value manufacturing.

Nearshoring, Investment, and Competition With China

One of the most important developments since the U.S.-China trade war began has been Mexico’s emergence as a nearshoring destination. Mexico overtook China as the largest source of U.S. imports in 2023, reflecting a broader shift in global supply chains away from Asia and toward North America.[74] Mexico’s share of total U.S. imports has increased from over 7 percent in 1994 to 16 percent in 2026.[75]

The reconfiguration of North American supply chains is no longer a future scenario but an ongoing structural shift. Between 2017 and 2023, U.S. imports from China declined significantly while imports from Mexico expanded rapidly, reflecting accelerated diversification away from Asian manufacturing platforms.[76]

This shift validates many of the expectations advanced by Mexican policymakers and economists after the escalation of U.S.-China trade tensions. However, the scale and speed of nearshoring have exceeded most early forecasts. Mexico has become a preferred destination not only because of its geography and labor costs, but also because T-MEC provides preferential market access, legal protections, and regional rules-of-origin incentives that encourage firms to locate production within North America rather than in China.

FDI trends reinforce this transformation. Mexico received approximately $36.9 billion in FDI in 2024, 2.3 percent higher than the previous year.[77] The United States accounted for 45 percent of total inflows.[78] More importantly, 54 percent of FDI was directed toward manufacturing industries, especially transportation equipment, electronics, chemicals, and metals.[79]

These trends demonstrate that reauthorization is directly tied to capital allocation decisions. Investors are relocating production to Mexico because they expect continued preferential access to the U.S. market. Any uncertainty regarding the future of T-MEC could delay or redirect investment toward alternative geographies.

The economic gains associated with supply-chain relocation remain substantial. According to estimates cited by the New York Times, if North America were to manufacture just 10 percent of the imports it currently receives from China, Mexico’s GDP would grow by approximately 1.2 percent, the United States’ GDP by 0.8 percent, and Canada’s by 0.2 percent.[80] These estimates illustrate the scale of the economic opportunity associated with regionalizing supply chains within North America rather than relying on Asian production platforms. This creates a narrow but significant strategic window for North America to consolidate regional industrial capacity before competing jurisdictions capture future investment flows.

Mexico benefits from U.S. efforts to diversify away from Chinese manufacturing, but it also faces increasing pressure from Washington on transshipment, Chinese investment in Mexico, and regional content enforcement.

However, competition with China has also introduced new tensions into Mexico’s trade strategy. Mexico benefits from U.S. efforts to diversify away from Chinese manufacturing, but it also faces increasing pressure from Washington on transshipment, Chinese investment in Mexico, and regional content enforcement. As a result, Mexico increasingly finds itself balancing two competing objectives: maintaining economic openness while aligning more closely with U.S. regional-security priorities.

Despite ongoing diversification efforts, North America remains highly dependent on Chinese inputs across several strategic sectors, including electronics, pharmaceuticals, automotive components, and advanced manufacturing supply chains.[81] This dependence increases the region’s exposure to geopolitical disruptions, trade restrictions, and industrial bottlenecks, reinforcing the importance of strengthening regional production networks under T-MEC.

Labor, Industrial Policy, and Political Sustainability

Another major shift since the renegotiation of NAFTA has been the growing importance of labor standards and industrial policy. Unlike earlier trade agreements, T-MEC incorporates enforceable labor provisions and the Rapid Response Labor Mechanism, which allows expedited review of labor-rights violations in specific facilities.[82]

For Mexico, these provisions initially generated concern about sovereignty and external pressure. However, labor reforms have also helped make North American integration more politically sustainable by reducing criticism that Mexico’s competitiveness relies primarily on low wages and weak labor protections.

Mexico has implemented major labor reforms, including new labor courts, collective bargaining rules, and union legitimization processes.[83] While implementation remains uneven, the agreement has strengthened Mexico’s labor institutions and reduced political pressure in the United States for protectionist responses against Mexican manufacturing.

T-MEC labor provisions have also coincided with a gradual shift toward higher-value-added manufacturing activities requiring more specialized labor. Regions linked to automotive, electronics, and advanced manufacturing supply chains have experienced growth in technical employment and higher-wage industrial operations, particularly in sectors affected by regional-content and labor-value requirements. Manufacturing hubs in northern Mexico, including Monterrey and Saltillo, have benefited from the expansion of automotive and advanced industrial production linked to T-MEC regional-content and labor-value requirements, reinforcing the region’s role in higher-value North American manufacturing supply chains.[84]

At the same time, Mexico’s domestic economic strategy has evolved toward a more active industrial-policy framework. The current administration’s “Plan México” explicitly prioritizes nearshoring, import substitution, local-content development, and strategic sectors such as semiconductors, electromobility, aerospace, pharmaceuticals, and energy.[85] The government aims to create 1.5 million jobs in strategic industries and increase domestic industrial capacity through targeted incentives and infrastructure investment.[86]

Mexico’s transition toward higher-value-added manufacturing has also accelerated growth in advanced industrial clusters linked to semiconductors, aerospace, electronics, and medical devices. Regions such as Guadalajara have benefited from cross-border technology initiatives and semiconductor-related investment, while medical device and aerospace firms increasingly leverage T-MEC’s rules of origin and intellectual property protections to integrate production within North America rather than Asia.[87]

At the same time, the transition toward knowledge-intensive industries has increased demand for specialized labor and technical expertise. Employers in advanced manufacturing sectors continue to report shortages of highly skilled workers, reflecting the rapid evolution of Mexico’s industrial base toward more sophisticated production activities.[88]

Why Timely Reauthorization Is Critical for Mexico

The strongest argument for timely reauthorization is that uncertainty itself carries economic costs. T-MEC’s review mechanism creates periodic political risk that can affect long-term investment decisions even before formal negotiations begin. Because manufacturing and infrastructure projects operate on multi-year timelines, firms require confidence that North American integration will remain stable well beyond 2026.

This issue is particularly important for sectors such as semiconductors, automotive manufacturing, logistics infrastructure, and clean energy, where investment decisions involve long amortization periods and highly integrated supply chains.

Uncertainty surrounding the review process has already begun affecting business expectations in export-oriented manufacturing sectors. Companies linked to automotive production, auto parts, metalworking, and integrated industrial supply chains have expressed concern about future rules-of-origin requirements, tariff risks, and potential modifications to regional content rules. Business groups in Puebla have reported delays in plant expansions, new production lines, supplier contracts, and other capital investment decisions while firms await greater clarity regarding the future direction of T-MEC implementation.[89]

In some cases, firms have delayed or reconsidered investment decisions while awaiting greater clarity regarding the future direction of North American trade policy. Private equity investors and industrial developers linked to nearshoring activity in Mexico have acknowledged that tariff uncertainty and concerns about the future implementation of T-MEC are slowing the pace of some transactions, industrial expansions, and manufacturing investments. Companies participating in logistics, industrial real estate, electronics manufacturing, and cross-border supply chains continue to view Mexico as strategically attractive, but several investors have indicated that uncertainty surrounding future trade rules is affecting the timing and structure of investment decisions.[90]

Mexico also faces a narrow strategic window. The country is benefiting from geopolitical fragmentation and the reorganization of global production networks, but this opportunity is not guaranteed to remain open indefinitely. Other countries—including India, Vietnam, and members of the European Union—are also competing aggressively for supply chain relocation and advanced manufacturing investment.

From Mexico’s perspective, T-MEC is no longer simply a trade agreement. It is the institutional foundation of North American competitiveness and the central platform through which Mexico seeks to move from export dependence toward higher-value industrial development.

Industrial relocation decisions are highly path dependent. Delays in reinforcing North American integration could therefore generate long-term consequences. Firms that establish manufacturing ecosystems and supplier networks in alternative regions may not relocate production again for decades, particularly in capital-intensive sectors such as semiconductors, automotive manufacturing, and electronics assembly.

Timely reauthorization matters because it signals continuity, predictability, and regional commitment at a moment when firms are determining the geographic location of the next generation of industrial investment.

Ultimately, from Mexico’s perspective, T-MEC is no longer simply a trade agreement. It is the institutional foundation of North American competitiveness and the central platform through which Mexico seeks to move from export dependence toward higher-value industrial development.

Why THE USMCA Matters for the United States

The United States’ core interest in the USMCA renewal is to preserve and expand the North American scale that U.S. firms need to compete in strategic industries. The agreement strengthens U.S. competitiveness not only by keeping regional trade largely tariff-free, but also by enabling firms to source inputs, talent, data, and production capabilities across Canada and Mexico. This matters because U.S. economic power increasingly depends on advanced industries that operate through cross-border supply chains, including IT, semiconductors, automobiles, medical devices, aerospace, and advanced manufacturing. Weakening the USMCA would raise costs for U.S. producers, reduce regional market scale, and make it easier for China and other competitors to gain ground in sectors central to national power.

For the United States, the agreement’s value is especially clear in two areas: digital trade and national power industries. The USMCA’s digital rules protect the open data flows, software, and cross-border services that underpin U.S. technology leadership. Meanwhile, North American trade in strategic goods helps U.S. firms combine domestic innovation with regional production depth. Renewal should therefore preserve the agreement’s core market-access benefits while updating its rules for an era of technological competition.

The United States is a world leader in IT and information services. Its companies in this sector are among the world’s largest, with R&D investments that outcompete those of entire countries such as Germany and Japan.[91] The U.S. IT and information services sector—the largest advanced industry in the United States—accounts for over 36 percent of the global market share in this industry, and without this activity, the United States would have failed to measurably increase its market share in advanced industries over the past decade.[92] (See figure 6.)

Figure 6: Top 10 producers’ shares of global output in IT and information services, 1995–2022[93]

USMCA Helps the United States Maintain Its Leadership in Digital Products and Services

Market-oriented digital rules, such as the ones outlined in the USMCA, safeguard America’s position at the forefront of the global digital economy. U.S. technology companies depend on open cross-border data flows, bans on data-localization mandates, protections for source code, and strong cybersecurity standards to scale internationally. These rules enable digital services companies to aggregate data, refine services, and stay globally competitive.[94]

The USMCA’s digital trade chapter—chapter 19—is one of the agreement’s most important contributions to maintaining U.S. competitiveness. As its predecessor, NAFTA, entered into force in 1994, it did not include key elements to ensure seamless, frictionless cross-border transactions in the digital economy. The USMCA closed that gap by establishing a high-standard, enforceable digital trade framework for the region—and, in the process, becoming a standard for digital trade agreements worldwide.[95]

Chapter 19 established binding commitments on nontaxation of cross-border electronic transmissions, non-discriminatory treatment of digital products, electronic signatures, online consumer protection, privacy frameworks, anti-spam rules, open Internet principles, cross-border data flows, and a ban on forced data localization.[96] It also added high-profile rules on source code protections, cybersecurity cooperation, open government data, and protections for interactive computer services. Table 1 outlines the provisions in chapter 19, their relevance to economic development, and whether the USMCA treats them as binding rules or voluntary commitments. The USMCA’s digital trade rules exclude all government procurement policies from its provisions. (ITIF has previously noted that this carve-out makes it easier for policymakers to include data localization requirements and weakens protections for source code, among other irritants.)[97]

Table 1. USMCA digital trade chapter’s provisions[98]

|

Article |

Provision/Commitment |

Economic relevance |

Binding? |

|

19.3 |

Moratorium on customs duties. Prohibit duties on digital products sent electronically |

Keeps software, media, and other digital products duty-free |

Yes—hard obligation |

|

19.4 |

Non-discrimination on digital products. Bar discrimination against partner-country products |

Supports a regional market for software and digital content |

Yes—hard obligation, with exclusions |

|

19.5 |

E-transactions. Requires a legal framework for online transactions |

Gives certainty to electronic contracts and online transactions |

Mixed: hard framework; soft regulatory guidance |

|

19.6 |

E-signatures. Protects legal validity and choice of authentication tools |

Enables cross-border contracting and digital compliance |

Mixed: hard validity rule; soft interoperability. |

|

19.7 |

Online consumer protection. Requires laws against online fraud |

Builds trust in e-commerce and digital marketplaces |

Mixed: hard legal baseline; soft cooperation |

|

19.8 |

Privacy protections. Requires a personal data protection framework and transparency |

Protects users while supporting compatible privacy regimes |

Mixed: hard framework; soft interoperability |

|

19.9 |

Paperless trade. Encourages electronic trade documents |

Cuts trade paperwork, delays, and customs transaction costs |

Nonbinding |

|

19.10 |

Open Internet. Recognizes user access to online services and apps |

Sets an open-Internet baseline without imposing net-neutrality rules |

Nonbinding |

|

19.11 |

Free flow of data. Prohibits restrictions on business-related cross-border data transfers |

Protects cloud, software, logistics, finance, and digital trade |

Yes—hard obligation, with public-policy exception |

|

19.12 |

Ban on data localization. Bars local server mandates as a market condition |

Prevents forced local infrastructure and protects cloud efficiency |

Yes—hard obligation |

|

19.13 |

Anti-spam. Requires measures against unsolicited commercial emails |

Improves trust and reduces spam-related costs in digital commerce |

Mixed: hard email rules; soft, wider cooperation |

|

19.14 |

Cooperation. Encourages exchanges on digital trade and regulation practices |

Helps the parties update policy as technology changes |

Nonbinding |

|

19.15 |

Cybersecurity. Encourages risk-based cooperation and incident response |

Promotes cooperation without prescriptive cyberrules |

Nonbinding |

|

19.16 |

Source code protection. Bars forced transfer of source code or algorithms |

Protects software, algorithms, and embedded digital technology |

Yes—hard obligation, with enforcement carve-outs |

|

19.17 |

Interactive services. Limits liability for third-party online content |

Reduces platform risk while preserving IP and criminal enforcement |

Yes—hard obligation, with major exceptions |

|

19.18 |

Open government data. Encourages open, reusable public data |

Supports transparency and accountability |

Nonbinding |

The value of these provisions lies in their ability to prevent digital fragmentation. For example, a data localization mandate functions as a de facto tax on digital trade by forcing firms to duplicate infrastructure, store data inefficiently, weaken cybersecurity, and operate separate national systems. Mandating disclosure of source code or algorithms threatens trade secrets and undermines incentives to innovate. Discriminatory treatment of digital products can tilt markets toward domestic champions and against foreign competitors. By prohibiting such practices, the USMCA establishes a default rule that North America’s digital market remains open, interoperable, and innovation friendly.

Relative to other agreements in force at the time, the USMCA was substantially more open than other digital economy-related provisions were. For example, the European Union-Japan Economic Partnership Agreement’s (EPA’s) e-commerce section (chapter 8, section F), which entered into force in February 2019, included source-code protection, e-signatures, privacy, and spam disciplines but only a commitment to revisit whether to include “free flow of data” rules within three years, not a binding right to move data across borders nor a localization ban.[99] Another example is the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), a free trade agreement among countries in the Indo-Pacific region, including Canada and Mexico, which entered into force in 2018 and includes strict digital rules in its e-commerce chapter.[100] CTPP’s digital rules are also considered a “template” for digital trade provisions; however, compared with CPTPP, the USMCA’s chapter 19 strengthened the data-flow rule, made the data-localization prohibition more stringent, expanded source-code protection to algorithms expressed in source code, and added a first-of-its-kind trade-rule analog to intermediary-liability protection.[101]

The USMCA digital trade chapter matters globally because it establishes a distinct model for the global digital economy—neither the Chinese model of cybersovereignty nor the European model of precautionary regulation.[102] China’s model centers on cybersovereignty, with extensive state control over data, platforms, content, and network architecture. China exports this model through digital rules embedded in trade agreements; for example, the Regional Comprehensive Economic Partnership (RCEP), an agreement among China, Southeast Asian countries, and other major Indo-Pacific countries, makes cross-border rules compatible with the People’s Republic of China (PRC) digital laws (e.g., Cybersecurity, Data Security, and Personal Information Protection Laws), and permits data localization rules under “essential security interests” reasons.[103]

For the United States, the digital trade chapter’s value is largest in sectors wherein data movement is integral to production or service delivery. That includes cloud computing, enterprise software, professional and technical services, finance, logistics, entertainment, digital advertising, and advanced manufacturing systems. Because U.S. firms are disproportionately strong in IP-intensive and data-intensive activities, legal protection for cross-border data transfers and against arbitrary localization works like an export-enabling rule. It protects the ability to serve North American customers from integrated regional or global networks rather than requiring redundant local infrastructure in every market. That lowers fixed costs and strengthens economies of scale.

Taken together, the digital trade chapter is one of many strong reasons for the United States to preserve and update the USMCA. Its provisions protect the operating conditions that enable U.S. firms to lead in the global digital economy. By keeping data flowing across borders, limiting forced localization, protecting source code and algorithms, and preventing discrimination against digital products, the USMCA helps North America remain an integrated digital market rather than three fragmented regulatory jurisdictions. A potential next phase of the USMCA should therefore reinforce these rules, close gaps such as the government-procurement carve-out, and ensure that North America remains the world’s leading pro-innovation digital trade bloc.

USMCA Strengthens U.S. National Power Industries

The USMCA’s central value for the United States is that it strengthens the competitiveness of U.S. strategic industries by preserving tariff-free access to lower-cost critical inputs while enabling U.S. firms to achieve greater scale across the Canadian and Mexican markets. While the digital trade chapter provides an important framework for the digital economy, the agreement’s broader importance lies in facilitating cross-border production and trade across the full range of industries critical to U.S. competitiveness.

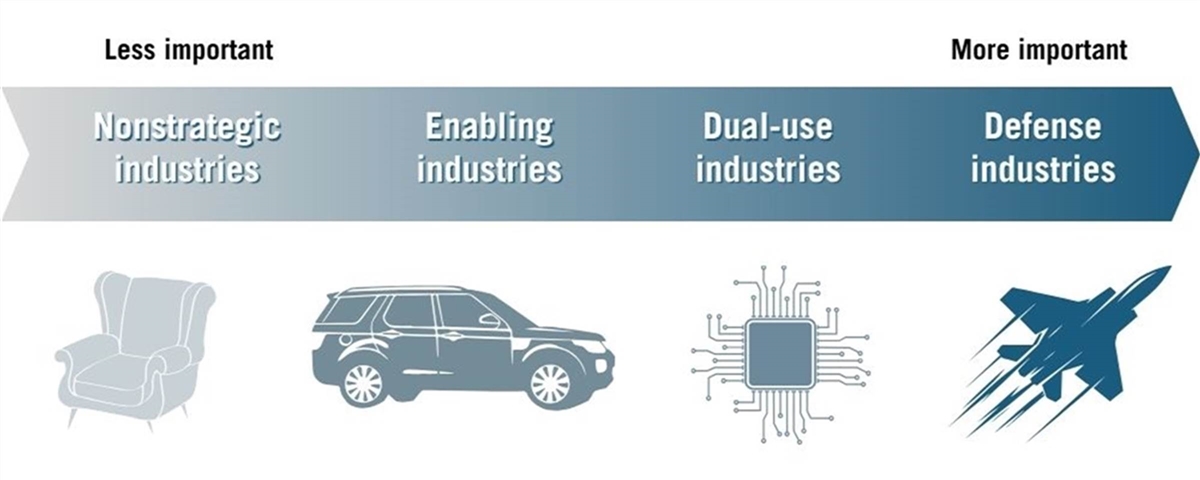

A useful way to assess the USMCA’s strategic value is to examine cross-border trade in goods primarily produced by industries that contribute to U.S. national power. National power is a country’s ability to deter other states from acting against its core interests and to shape the choices of other nations. The conventional view holds that only the defense industry matters for national power. But in the globally integrated economy of the 21st century, that view is far too narrow. National power increasingly depends on strength in industries that not only support the development and production of weapons systems, but also provide economic and technological leverage over adversaries while reducing their leverage over the United States. These industries span a broad spectrum, from purely defense-related production to dual-use technologies with both military and commercial applications to enabling industries that sustain the broader industrial commons. They include semiconductors, aerospace, biopharmaceuticals, telecommunications equipment, advanced chemicals, precision machinery, robotics, AI systems, and many other advanced sectors.[104]

As such, ITIF has developed a classification of U.S. industries for their relevance to national power. This can be viewed as a continuum between defense industries on one side and nonstrategic industries on the other, with strategic dual-use industries and strategic enabling industries in the middle. (See figure 7.)

Figure 7: Industrial power scale

The USMCA disproportionately supports trade in goods tied to advanced production, industrial capacity, technological leverage, and defense-relevant supply chains. For the United States, this means that regional integration is one of the mechanisms by which domestic firms achieve economies of scale, reduce input costs, and compete globally.

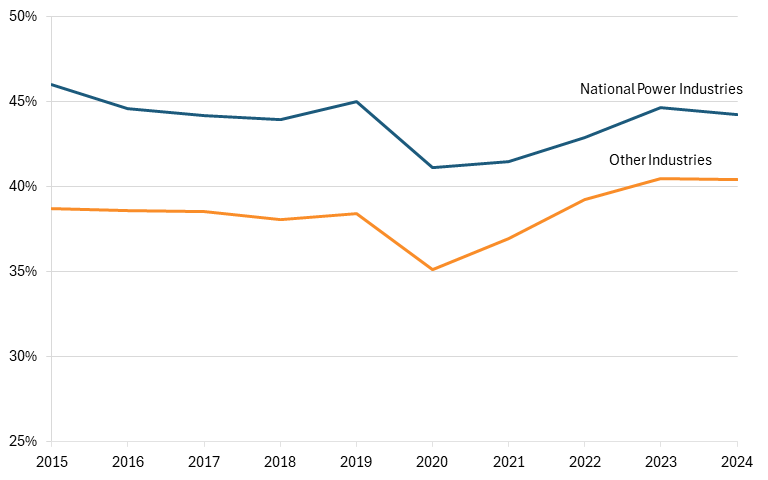

Although these “national power industries” provide a sectoral categorization of the economy, they can be translated into product-level categories for purposes of trade analysis. As such, figure 8 shows that the USMCA (and NAFTA before 2020) contributed to U.S. trade being more intensive in national power industry goods than in nonnational power goods. For the 2015–2024 decennial, national power industry goods accounted for 44 percent of total trade with Canada and Mexico, while cross-border commerce in nonnational power industry goods accounted for 38 percent. This difference is consistent across the five years of NAFTA before its modernization (2015–2019) and the first five years of the USMCA (2020–2024).

Figure 8: Aggregate U.S. trade in goods with Canada and Mexico relative to total trade in goods[105]

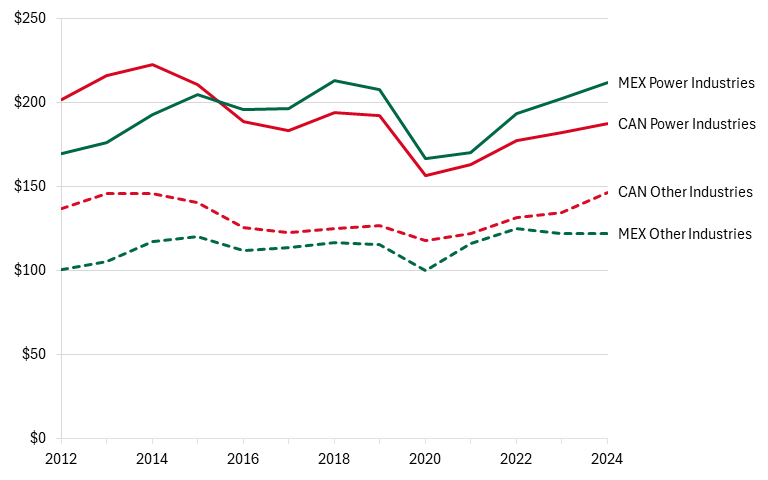

USMCA trade is concentrated in sectors central to U.S. competitiveness and security. U.S. exports to both USMCA partners are consistently led by national power industry goods, underscoring the agreement’s role in sustaining North American production in strategic sectors. (See figure 9.) Exports of these goods to Canada remained near or above $180 billion for most of 2012–2024, fell sharply in 2020, and then recovered to nearly $190 billion by 2024. Exports of national power goods to Mexico show a stronger upward trajectory, rising from roughly $170 billion in 2012 to more than $210 billion in 2024, after a pandemic-era decline. Nonnational power exports are smaller and flatter for both partners.

Figure 9: U.S. exports to its USMCA partners (in billions at 2024 values)[106]

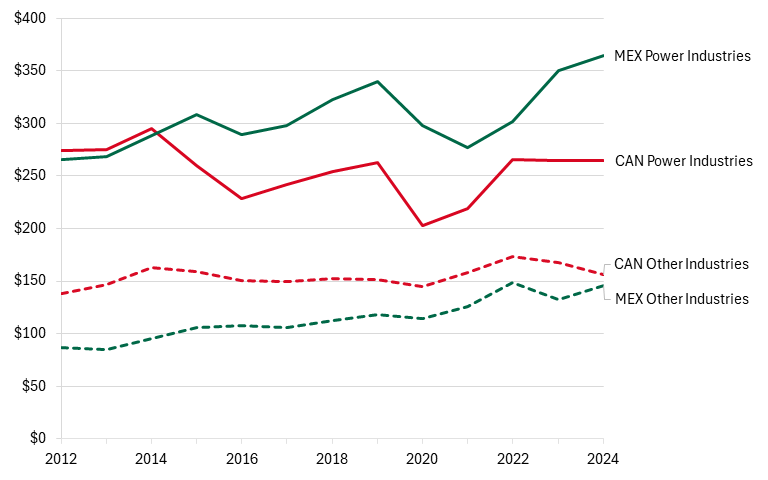

Likewise, figure 10 shows U.S. imports from Canada and Mexico are also heavily concentrated in national power industry goods. Mexico stands out: U.S. imports of these goods rose from about $265 billion in 2012 to roughly $365 billion in 2024, with especially strong growth after 2021. Canadian imports are lower and more stable. Nonnational power imports remain smaller for both partners, reinforcing the overall strategic character of North American trade.

Figure 10: U.S. imports to its USMCA partners (in billions at 2024 values)[107]

Conclusion

The 2026 review of the USMCA should be treated as a strategic opportunity. For Canada, Mexico, and the United States, the agreement is now the core institutional framework for North American production and economic security. It preserves tariff-free trade for qualifying goods, supports integrated supply chains, and gives firms the predictability they need to invest across borders. Allowing the agreement to drift into uncertainty would weaken all three economies at precisely the moment when global competition is intensifying.

The case for renewal is strongest when the USMCA is understood as a platform for shared competitiveness. Canada contributes energy, critical minerals, advanced manufacturing, and defense-industrial capacity. Mexico provides manufacturing scale, logistics networks, engineering talent, and a vital nearshoring platform. The United States anchors the region through market size, technological leadership, capital, and advanced industries. Together, these complementary strengths allow North America to compete more effectively than any one country could alone.

A successful review would send a clear signal that North America remains open to investment, committed to rules-based integration, and capable of acting as a coherent economic bloc. Policymakers should renew and modernize the USMCA to strengthen continental competitiveness, reduce dependence on China, support high-value jobs, and secure the region’s long-term prosperity.

Acknowledgments

This report is the product of collaborative effort on the part of the authors. They cowrote the opening sections, and they individually contributed the later sections providing perspectives on why the agreement alternately known as CUSMA, T-MEC, and the USMCA is important for Canada, Mexico, and the United States, respectively.

The authors also would like to thank Stephen Ezell, Mary Marsh, and Esther Serger for their contributions to this work.

About the Authors

Rodrigo Balbontin is an associate director covering trade, IP, and digital technology governance at ITIF. He has extensive experience in policy design and research on science, technology, and innovation governance in the Americas and the Asia-Pacific regions. He earned a master’s degree in science and technology policy from the University of Sussex and a bachelor’s degree in economics from the University of Chile.

Carolina Agurto is the executive director of Fundación IDEA, one of the first and main think tanks on public policy in Mexico. Throughout her career, Ms. Agurto has collaborated with organizations such as DOL, the U.S. Department of State, the World Bank, the Inter-American Development Bank, the OECD, the OAS, and the United Nations on projects related to economic development, trade, regulatory policy, competition, intellectual property, and governance. She has direct experience in international trade policy, having participated in negotiations of the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) and the Pacific Alliance. Carolina holds a bachelor’s degree in Economics and an MPP from The University of Chicago, where she was a Fulbright Scholar, a grant recipient of the JJ/World Bank, and a Dean’s Scholar.