The Hamilton Index, 2026: China’s Dominance in Advanced Industries Is Growing

China now produces nearly one-quarter of global output in the 10 advanced industries that make up ITIF’s Hamilton Index, outpacing all other nations. America and the West must recognize that China’s gains are coming at the expense of their techno-economic and national power.

KEY TAKEAWAYS

Key Takeaways

Contents

Introduction

Advanced industries sit at the core of modern economic growth. They drive productivity gains across the broader economy, support high-wage employment, and generate export revenues that underpin strong currencies and favorable terms of trade. And because these sectors are deeply embedded in global supply chains and characterized by scale, nations that secure leadership in advanced industries tend to lock in durable advantages. Winning in innovation alone in these industries is not enough; without domestic or allied production capacity, countries forfeit much of the economic value of discovery, lose critical knowledge, and weaken the ecosystems that translate research into commercial and strategic power. These industries are what the Information Technology and Innovation Foundation (ITIF) calls “national power industries.”[1]

China’s rapid ascent into advanced industry production has fundamentally altered the global landscape. It has not become more specialized in these advanced sectors over the past decade (because the rest of its economy has also grown), but its absolute output and share of global production in these advanced industries has grown steadily. Indeed, China has moved from a peripheral manufacturer to a central player and, in some sectors, a global leader in advanced industries. This shift poses a direct challenge to the United States and the broader Western alliance bloc. As advanced industries increasingly underpin defense supply chains, digital infrastructure, and economic growth, China’s gains are often coming at the expense of U.S. and allied capacity. The result is a more fragile industrial base, making the United States increasingly vulnerable to the coercive pressures from China.

Methodology

To assess U.S. and other nations’ performance, ITIF has examined changes in global shares of value-added output in 10 advanced industry sectors aggregated into the Hamilton Index of Advanced-Technology Performance: information technology (IT) and information services; computers, electronics, and optical products; chemicals (not including pharmaceuticals); machinery and equipment; basic metals; motor vehicles; fabricated metals; pharmaceuticals; electrical equipment; and other transportation equipment. This report serves as the second update of the Hamilton Index, following the first edition published in 2022 and the second published in 2023.[2] To conduct this analysis, ITIF uses value-added data from the Organization for Economic Cooperation and Development’s (OECD’s) trade in value added dataset, which covers the period from 1995 to 2022.[3] ITIF’s analysis focuses on 39 countries included in that dataset. Because of problems with how Ireland’s output is reported, it is not included in the analysis or in EU-wide aggregate data.[4]

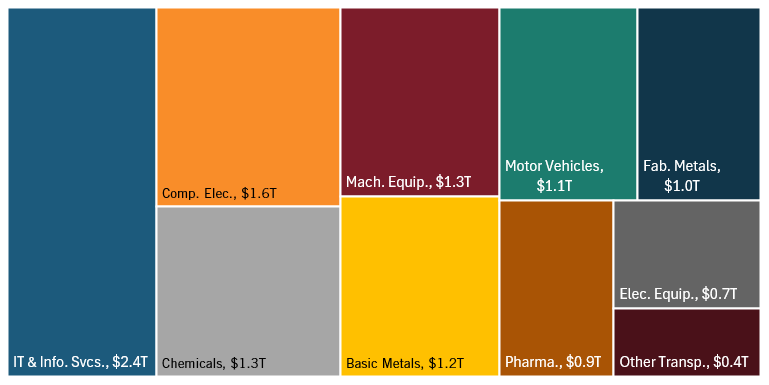

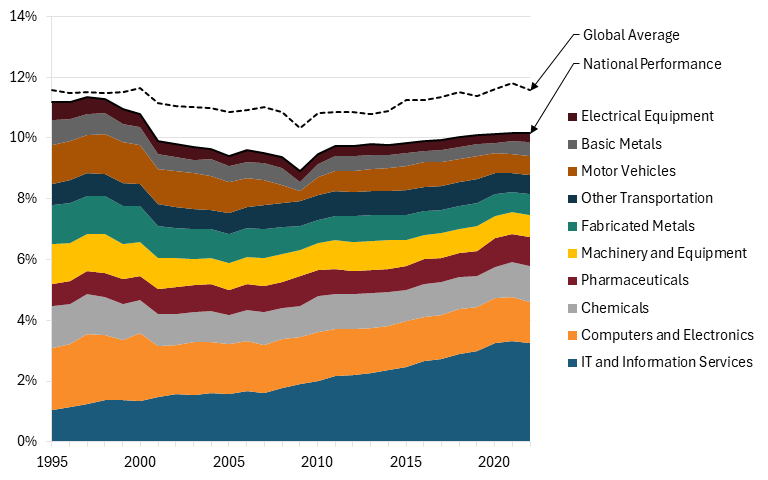

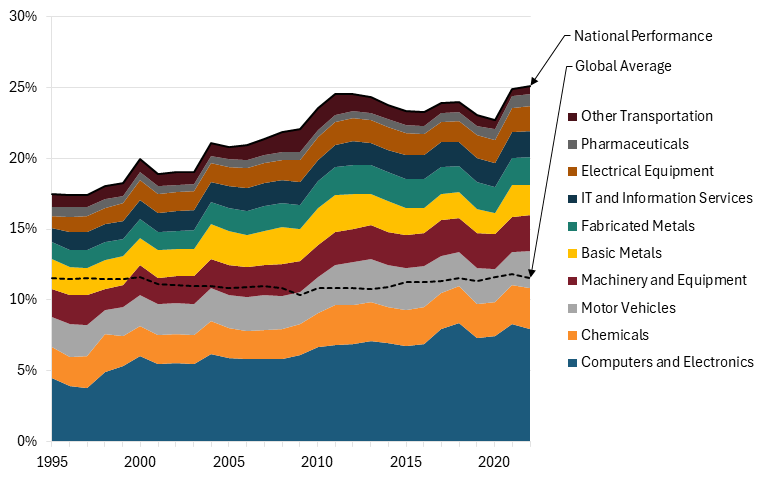

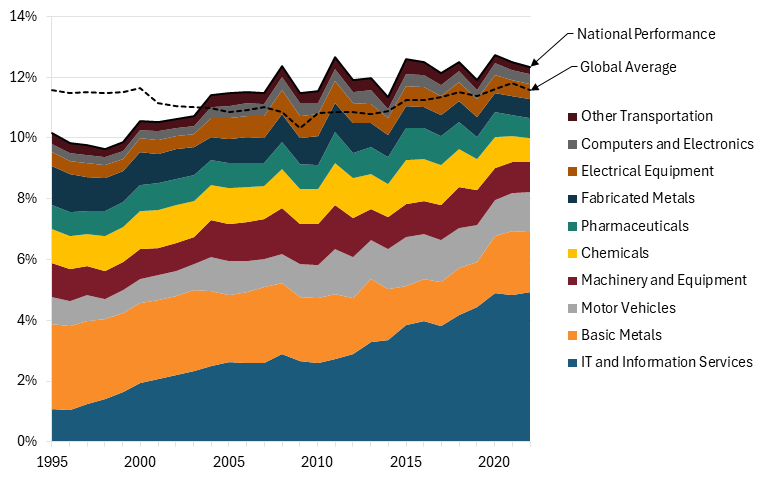

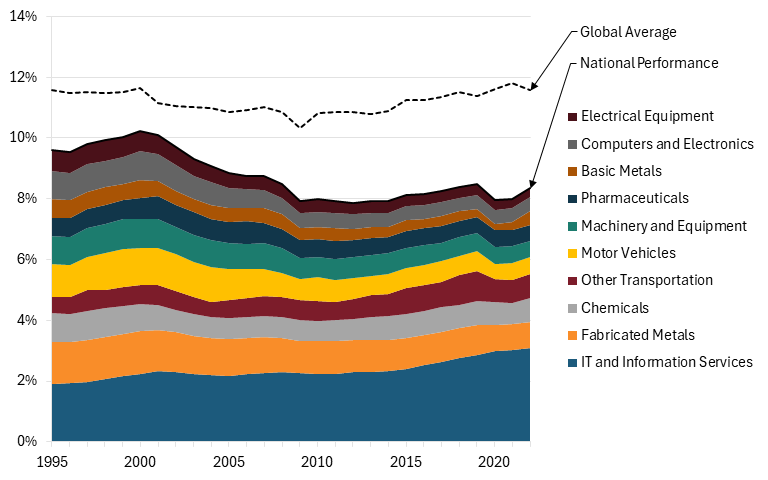

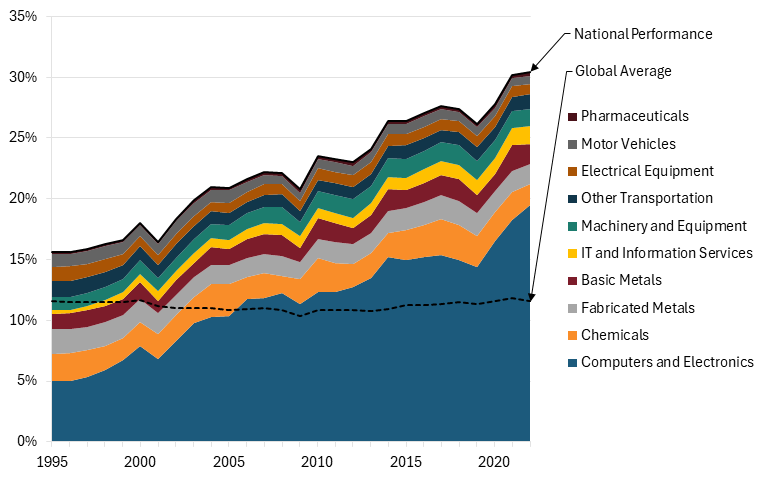

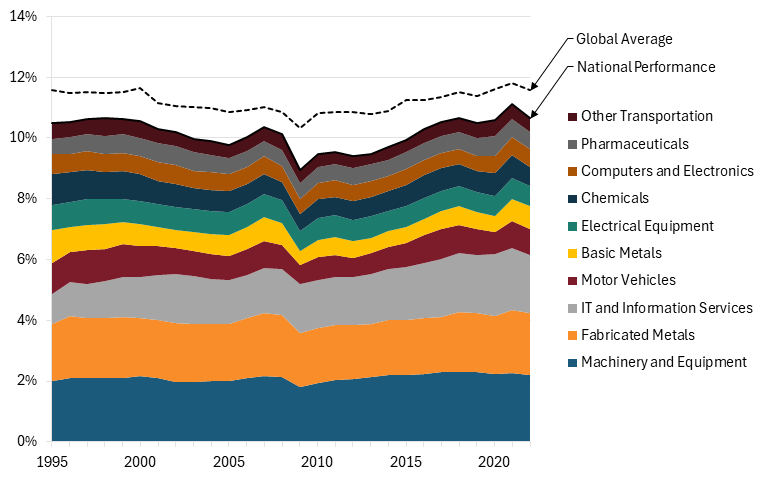

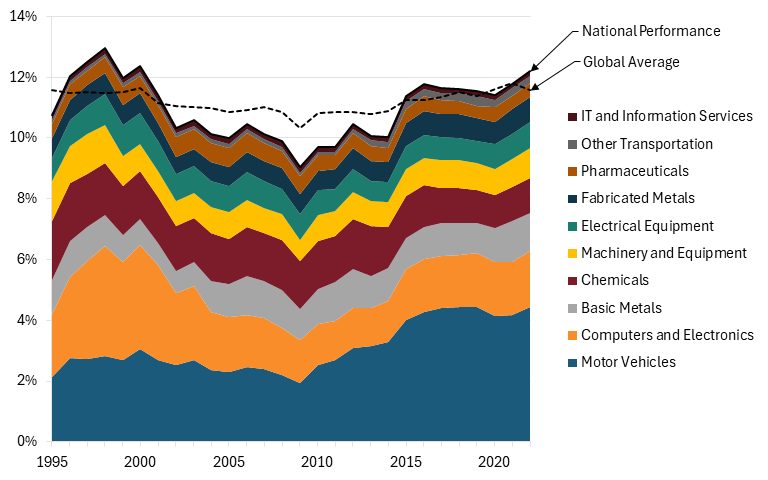

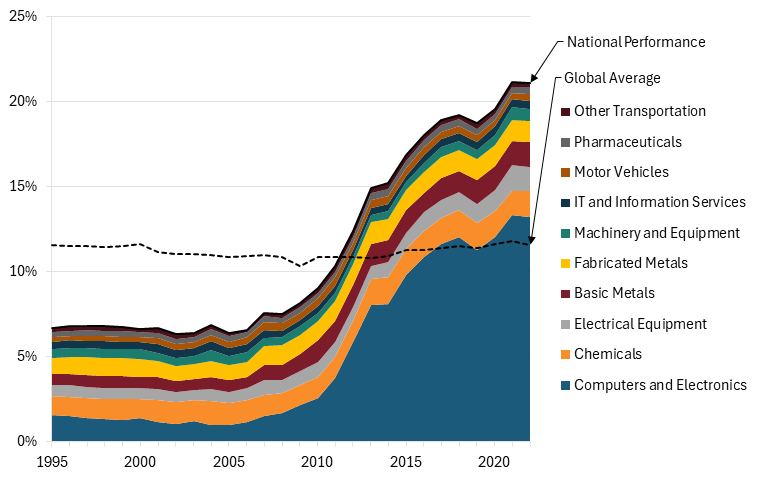

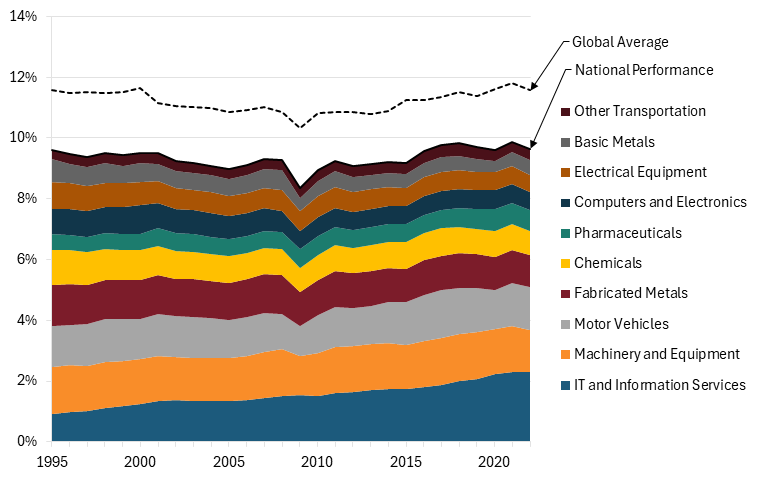

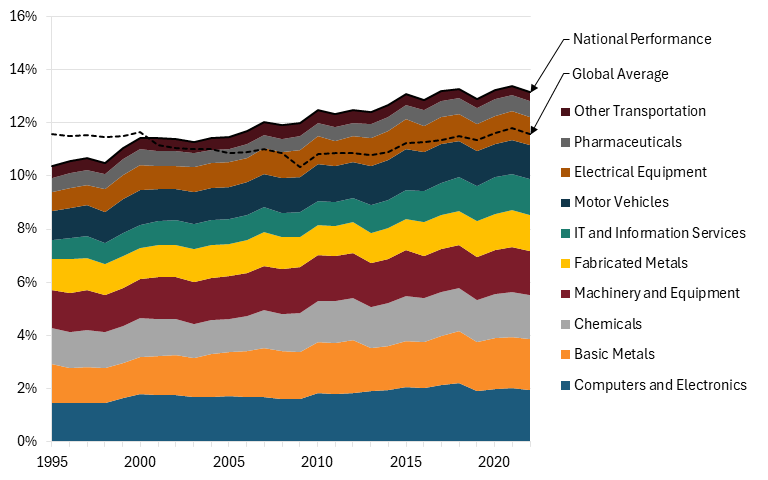

The 10 industries included in the Hamilton Index together accounted for nearly $12 trillion in global production in 2022 (figure 1). The information technology (IT) and information services industry (which includes software, Internet services, and data processing) is the largest of the 10, accounting for 20 percent of global advanced industry output.

Figure 1: Global output from industries included in the Hamilton Index, 2022 ($11.9 trillion, total)

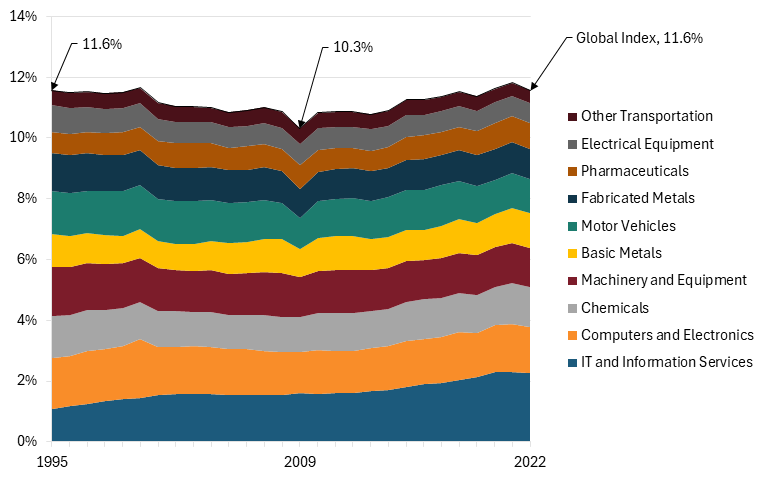

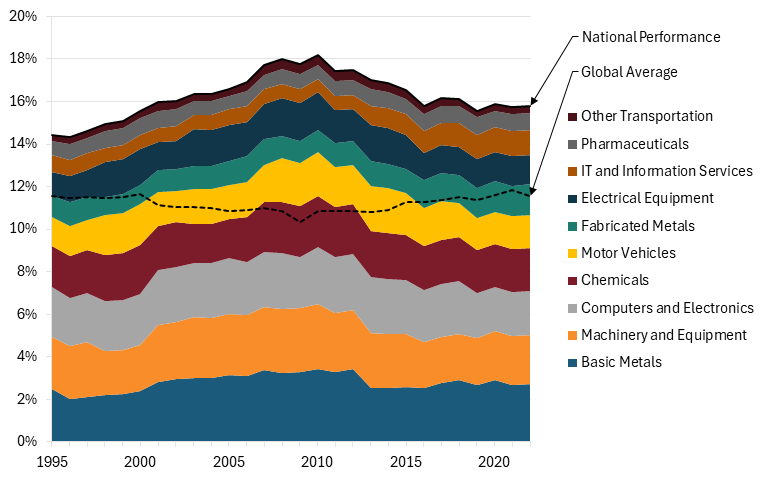

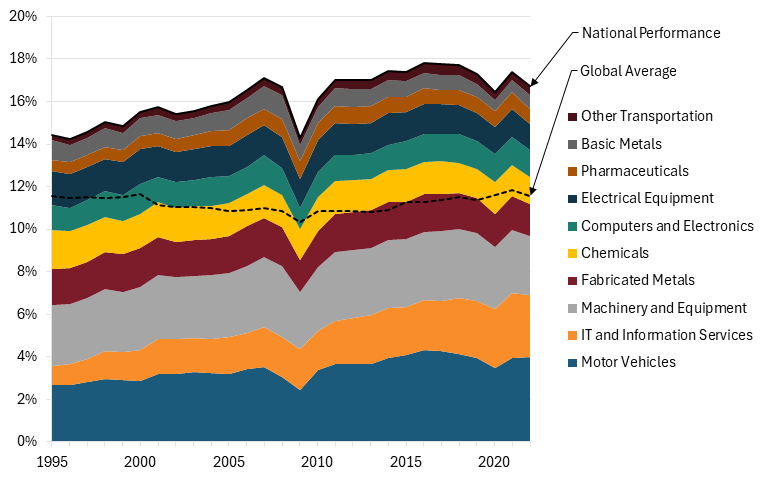

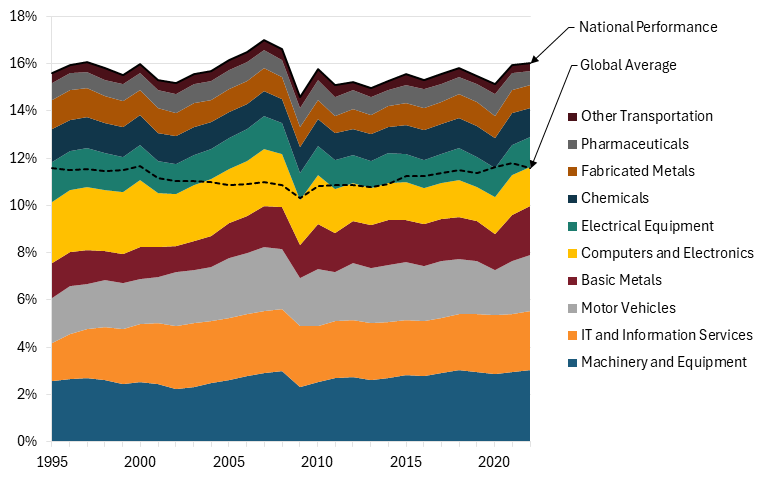

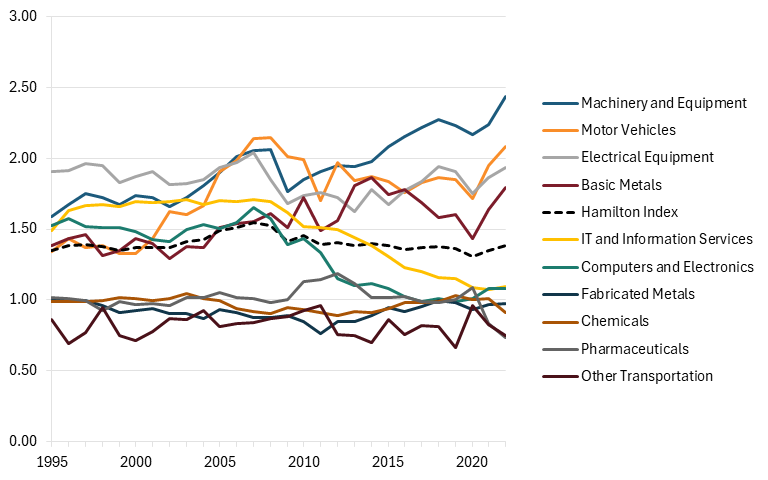

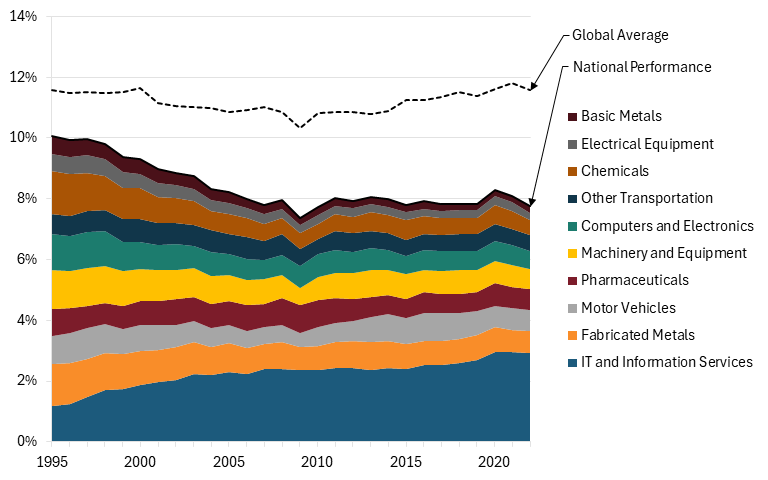

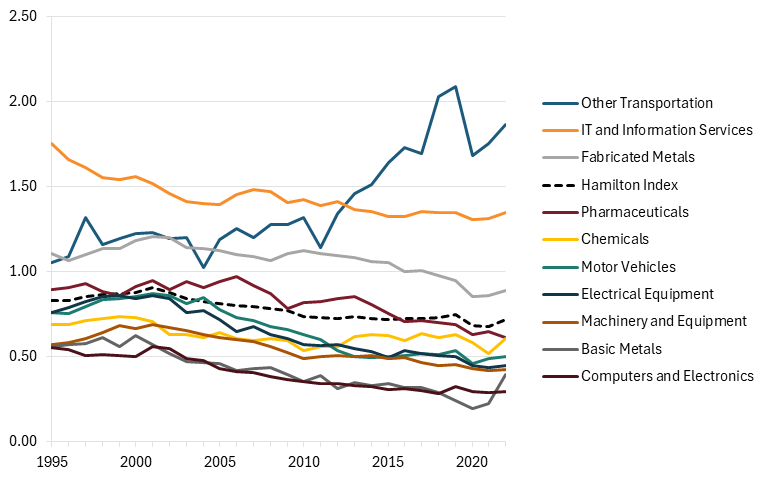

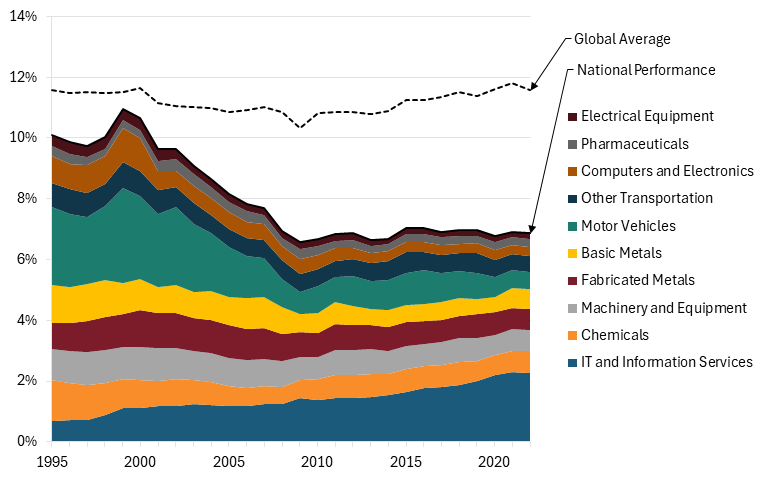

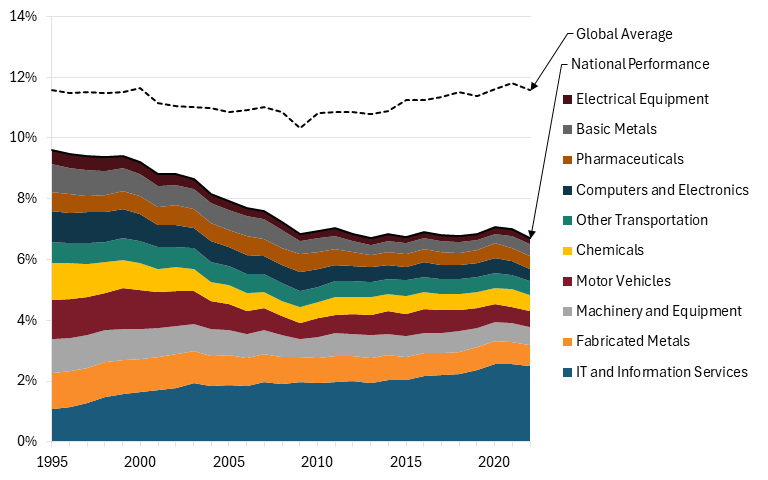

The aggregate production of the 10 industries equaled 11.6 percent of the global economy in 2022, the same as in 1995, rebounding from a nadir of 10.3 percent in 2008, when advanced industry production declined more than the overall gross domestic product (GDP). (See figure 2.) However, the output of each individual industry has changed, with IT and information services’ share of the global economy growing 45 percent since 2002. The fact that the overall share of advanced industry output in the global economy has not changed underscores the zero-sum competition between nations.

Nations are, or at least should be, competing for a greater share of this fixed pie, as China has shown itself to be. The United States, the world’s dominant techno-economic power for over 125 years, has allowed itself to stand on the sidelines of this global competition as China and the rest of the world capture growing slices of market share, and is now at risk of losing this race—and a loss would be catastrophic, turning the United States into a deindustrialized economy with weak economic growth and innovation capabilities. Time is short. The first half of this decade was one in which China proved its prowess in dominating advanced industries, moving from simply a copier to an innovator. The second half of this decade will be the time for the United States to demonstrate its willingness and ability to turn around U.S. advanced industry fortunes because, once China gains sufficient global market share, allied and U.S. production risks being permanently weakened.

This report is one of a series published by ITIF addressing the Chinese national techno-economic power industry challenge and will demonstrate the decline in U.S. advanced industry production over the past 27 years and China’s rise as a global leader. Future reports in this series will lay out in great detail the specific policy actions needed to better combat Chinese dominance.

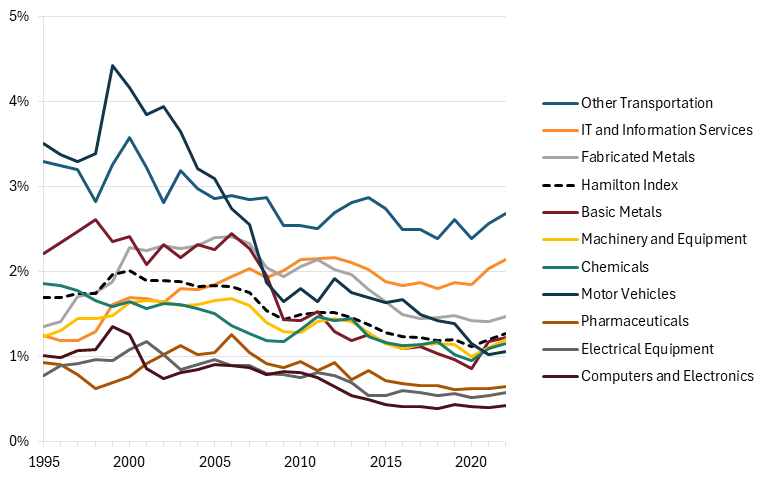

Figure 2: Hamilton industry shares of the global economy, 1995–2022

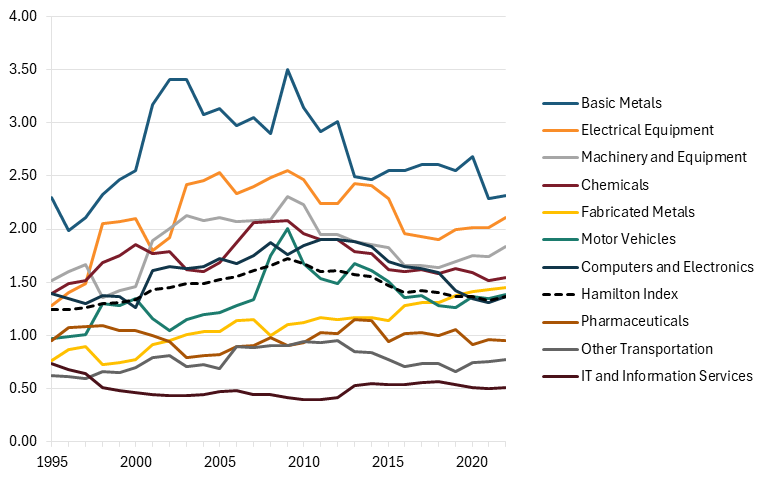

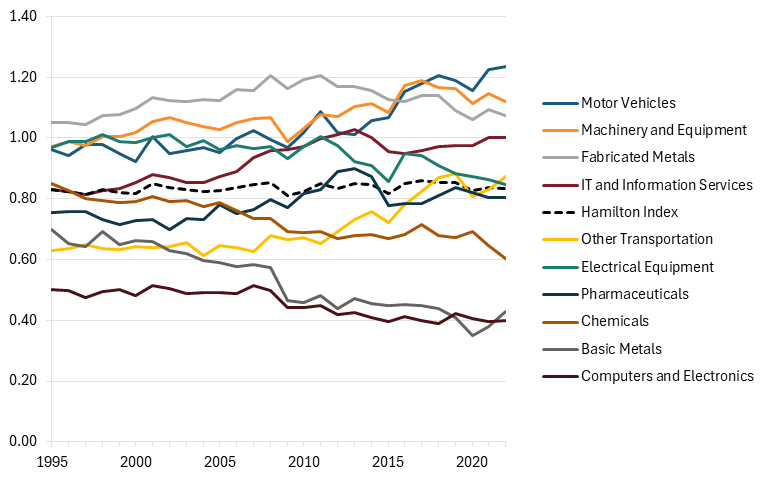

Of course, global market shares of advanced industries cannot serve as the only metric of national competitiveness because nations have different-sized economies. To assess nations’ relative performance in strategically important industries, ITIF uses an analytical statistic known as a “location quotient” (LQ), which measures any region’s level of industrial specialization relative to a larger geographic unit—in this case, a nation relative to the rest of the world.

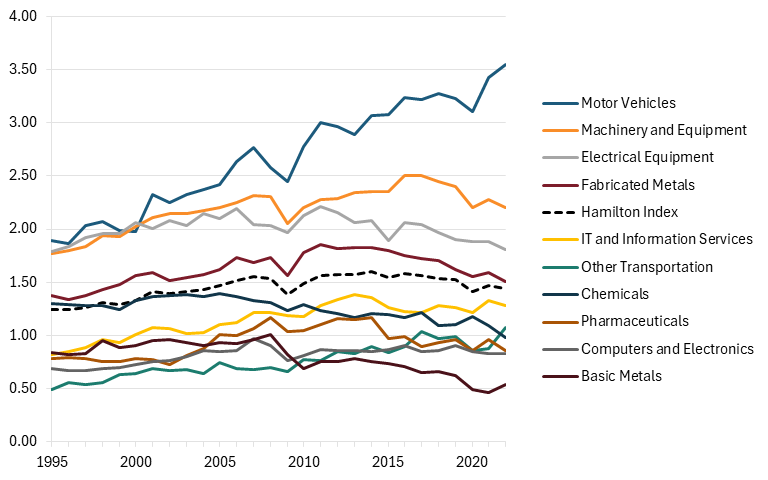

The LQ is calculated as an industry’s share of a country’s economy divided by the global industry’s share of the global economy, or as a country’s share of global output in an industry divided by the country’s overall share of the global economy. Either way, an LQ greater than 1 means the country’s share of global output in an industry is greater than the global average, and an LQ less than 1 means a country’s share is less than the global average. For example, the U.S. motor vehicle industry’s output in 2022 was 13.79 percent of global motor vehicle production, while the U.S. economy overall accounted for 25.39 percent of global GDP. Thus, the U.S. LQ in the motor vehicles industry was 13.79 percent divided by 25.39 percent, or 0.54, meaning the United States significantly underperformed in the industry. Its output was just 54 percent of the level we would expect based on the size of the U.S. economy.

Because LQ measures the importance of an industry relative to the size of a country’s economy, a country’s LQ can decline even if its industries are expanding rapidly, provided the rest of the economy is growing even faster.

The Hamilton Index, 2026: Data Visualization Tools

This report is accompanied by three data visualization tools for the Hamilton Index dataset:

§ “The Hamilton Index, 2026: Industry Visualizations”

Overall Findings

Specialization Rankings

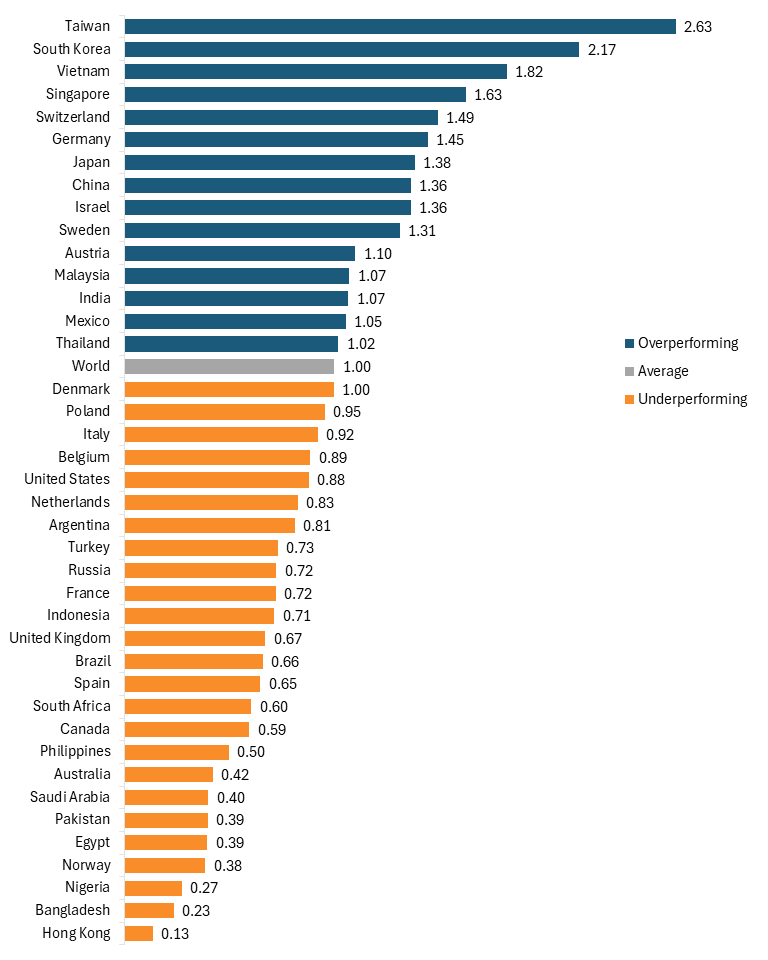

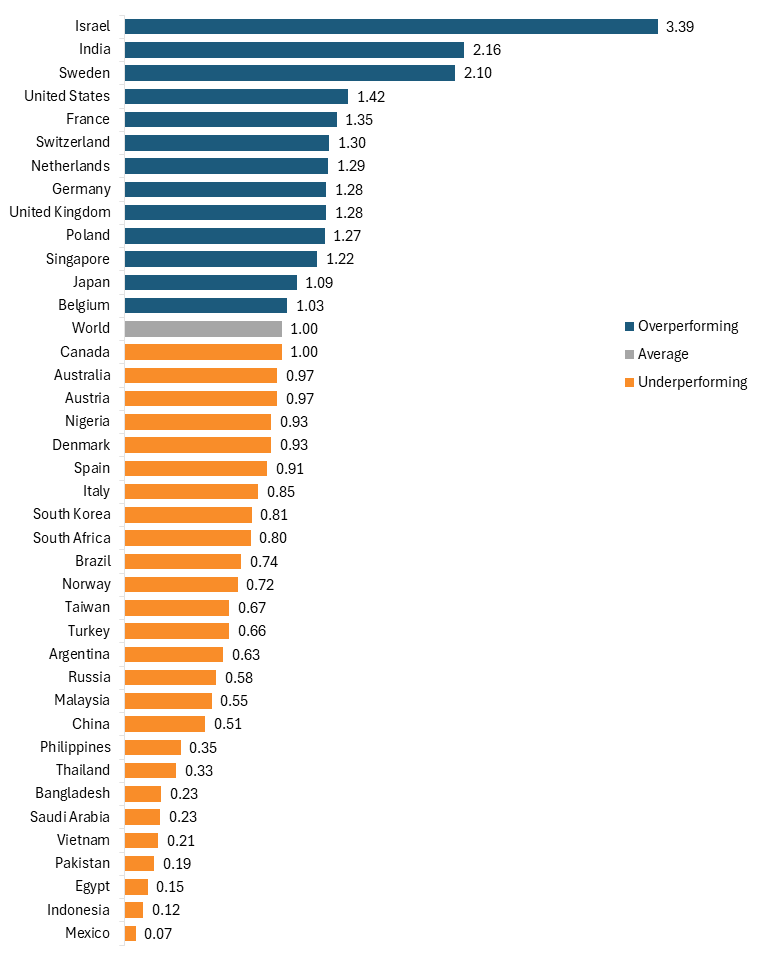

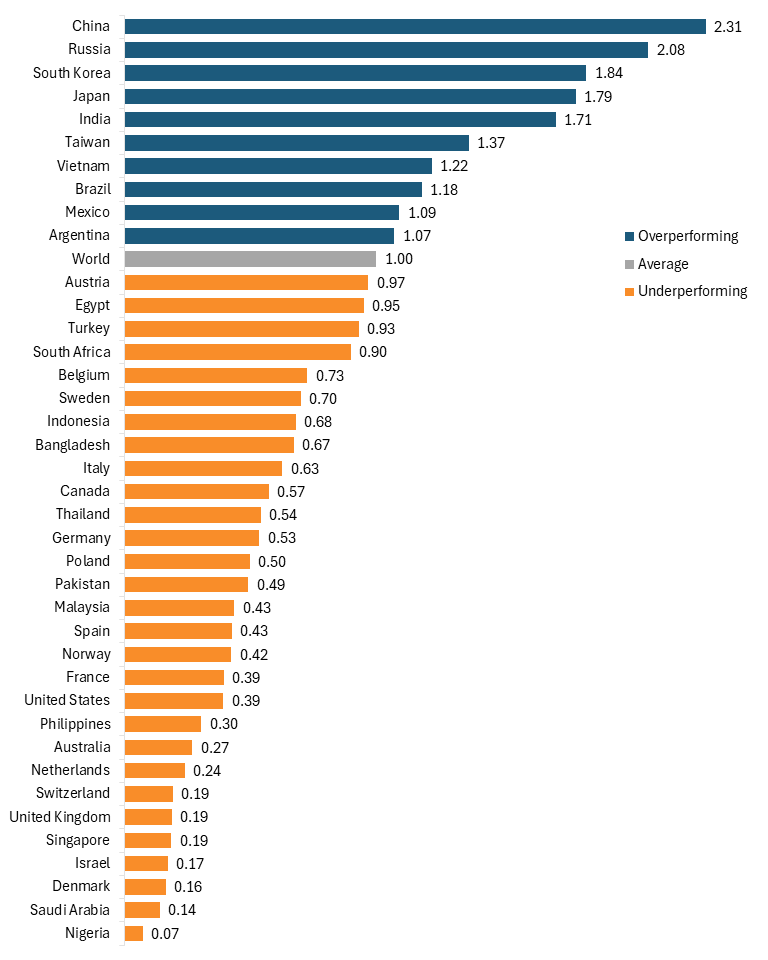

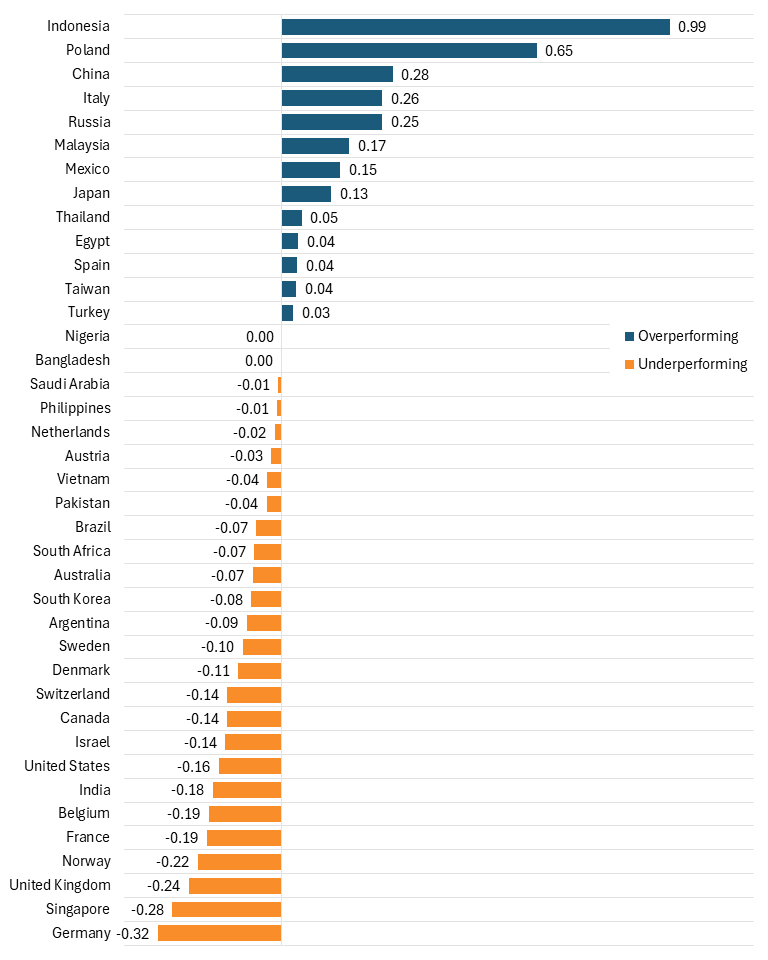

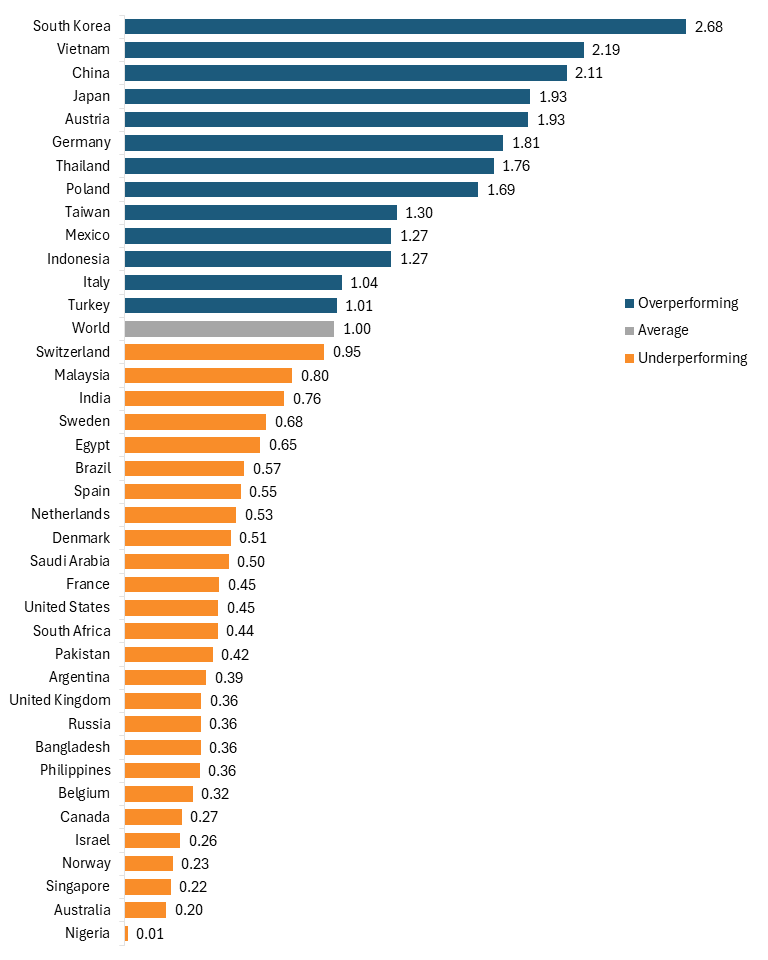

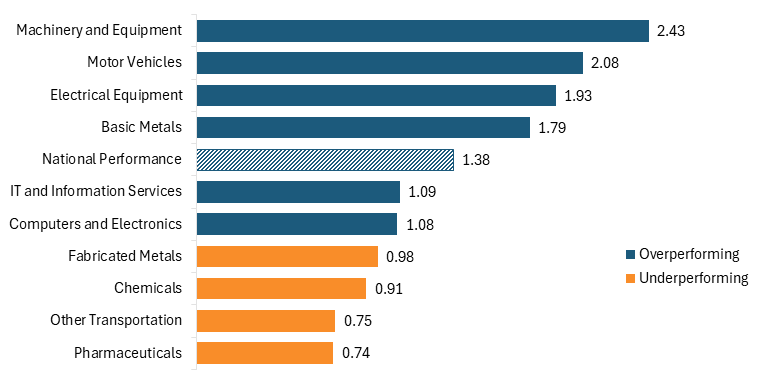

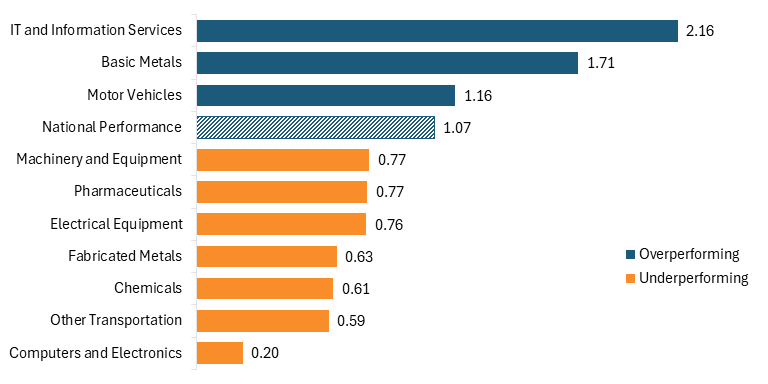

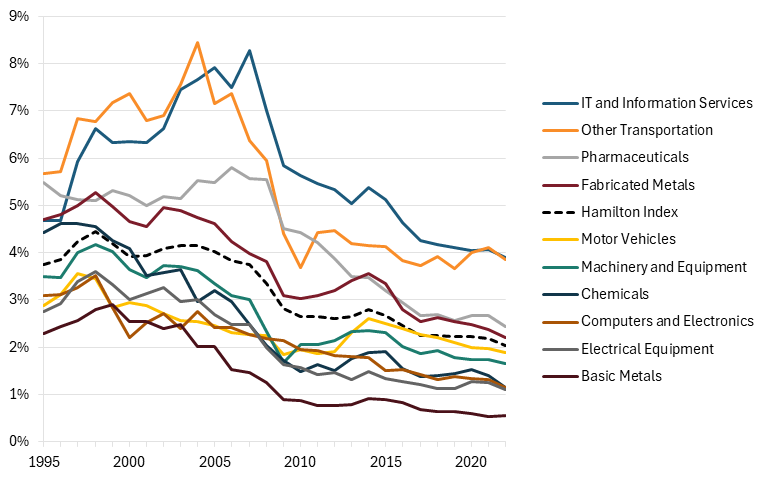

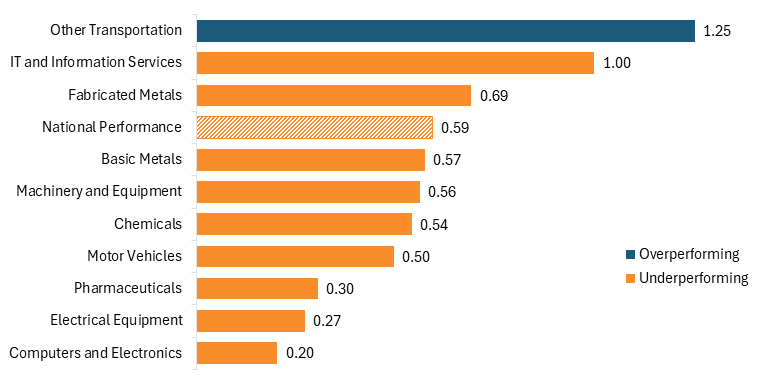

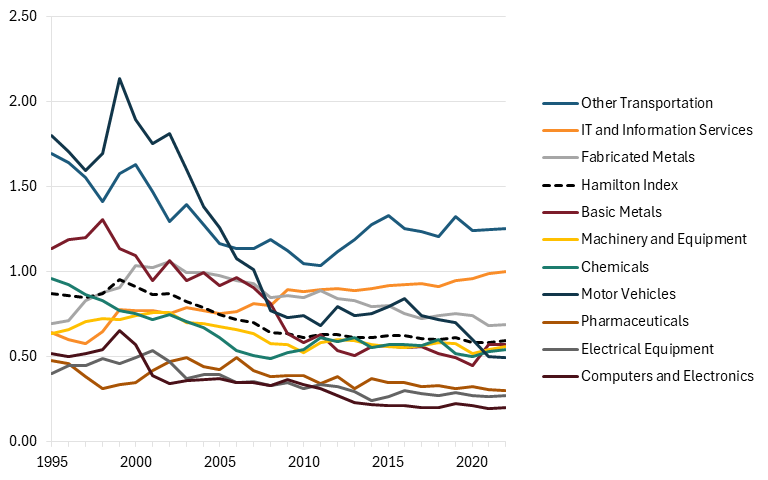

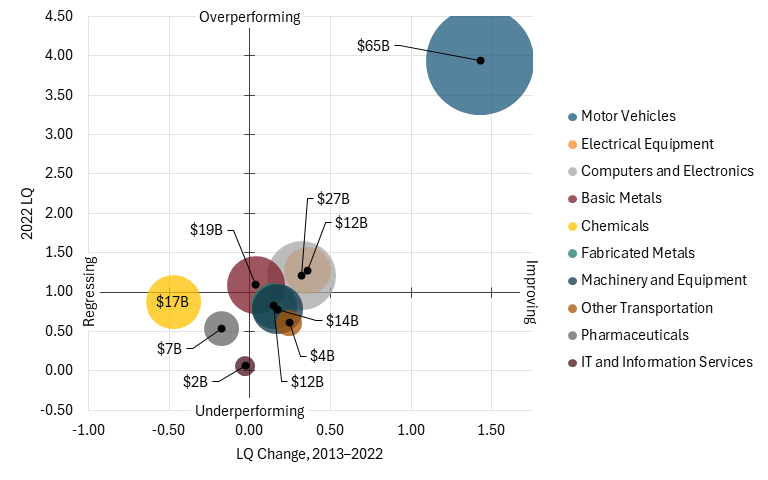

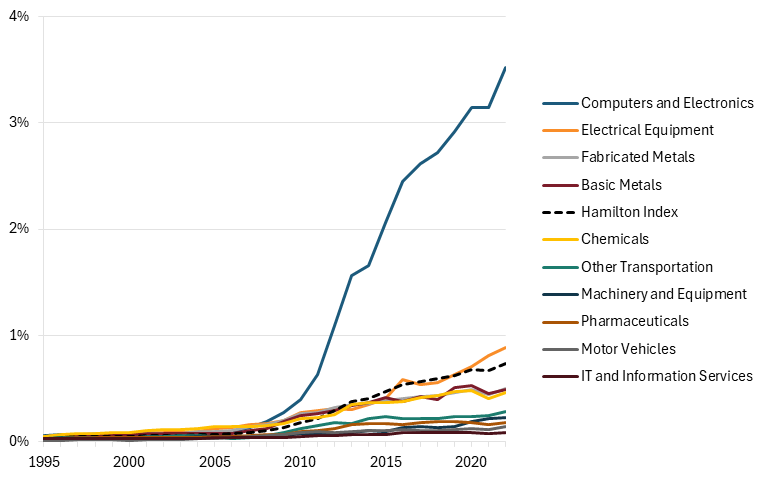

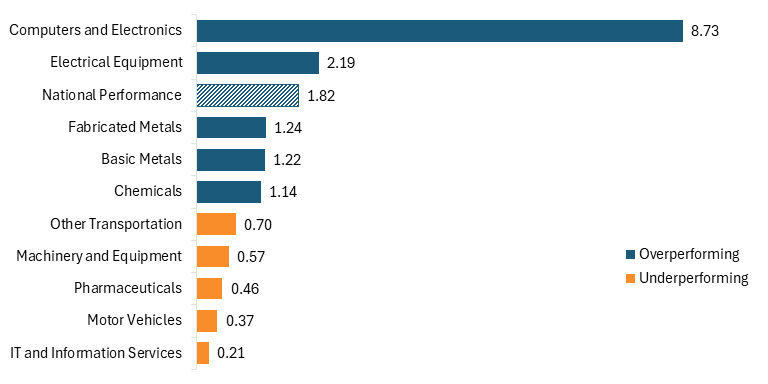

Fifteen countries overperformed in their composite Hamilton Index LQ in 2022, led by Taiwan with an LQ of 2.63 (the large majority of which was driven by the country’s semiconductor industry, which is included under the computer and electronics industry). (See figure 3.) South Korea, Singapore, and Japan, all technologically advanced East Asian nations, ranked second, fourth, and seventh, respectively. These three nations have intensively focused on advanced industry development over the past several decades—a strategy that has been reflected in their LQs and global market shares in industries such as computers and electronics. European nations, including Switzerland, Germany, Sweden, and Austria, rank 5th, 6th, 10th, and 11th, respectively, leading in engineering and chemical-intensive industries.

While most developing nations underperformed with LQs significantly below 1, Vietnam stands out as an outlier, ranking third overall with an LQ of 1.82. This marks a rapid rise in relative performance, driven primarily by its growth in the computers and electronics industry. Other developing nations that overperformed include Malaysia, India, Mexico, and Thailand.

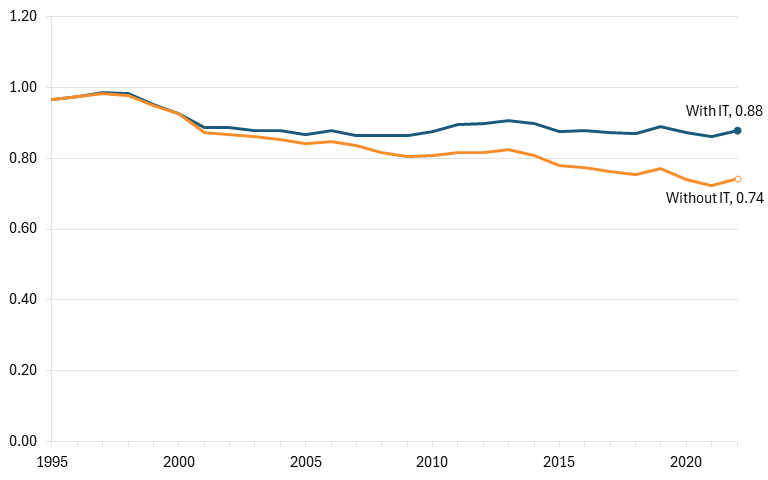

The United States’ LQ was 0.88, meaning that as a share of GDP, U.S. Hamilton industries’ value added was lower than the global average. For the United States to achieve an LQ of 1, advanced industry output would have needed to be $370 billion greater in 2022, a 14 percent increase. This would be equivalent to more than doubling the output of the computer and electronics industry in the United States last year.

Some will argue that it’s acceptable or even normal for the U.S. LQ to be this low because it is a large economy and one in which the share of GDP that is globally traded is below average. But LQ is not a measure related to trade; it’s a measure related to production. Moreover, there was a small but positive correlation between national GDP and LQ in 2022 (0.05), suggesting that the U.S. score should not be below average and, if anything, should be above average. The reality is America’s low LQ reflects failure, not success.

The United States’ LQ was 0.88. For the United States to achieve an LQ of 1.00, advanced industry output would have needed to be $370 billion greater in 2022, equivalent to more than doubling the output of the computer and electronics industry last year.

China, which ranked eighth, has perhaps focused more than any other country on cultivating advanced industries, becoming a top performer in several Hamilton industries, including basic metals, machinery and equipment, and electrical equipment. Yet, over the past decade, China experienced the largest decline in overall LQ among countries in the sample, falling by 21 percentage points. (See figure 4.) Importantly, this decline does not reflect a weakening of China’s advanced industry production. China’s output in these industries grew by 7.3 percent annually over the previous decade—faster than the United States, OECD, or the global average. Instead, it reflects China’s extraordinary economic growth, with GDP growing nearly 9 percent annually over the same period, meaning the rest of the economy expanded even faster than advanced industries did. As a result, advanced industries make up a slightly smaller share of China’s economy even as China continues to capture growing global market share and remains a dominant force in these sectors. China also continues to overperform in the Hamilton Index, with its LQ being 36 percent higher than the world average.

Figure 3: Relative national performance in the composite Hamilton Index (2022 LQ)

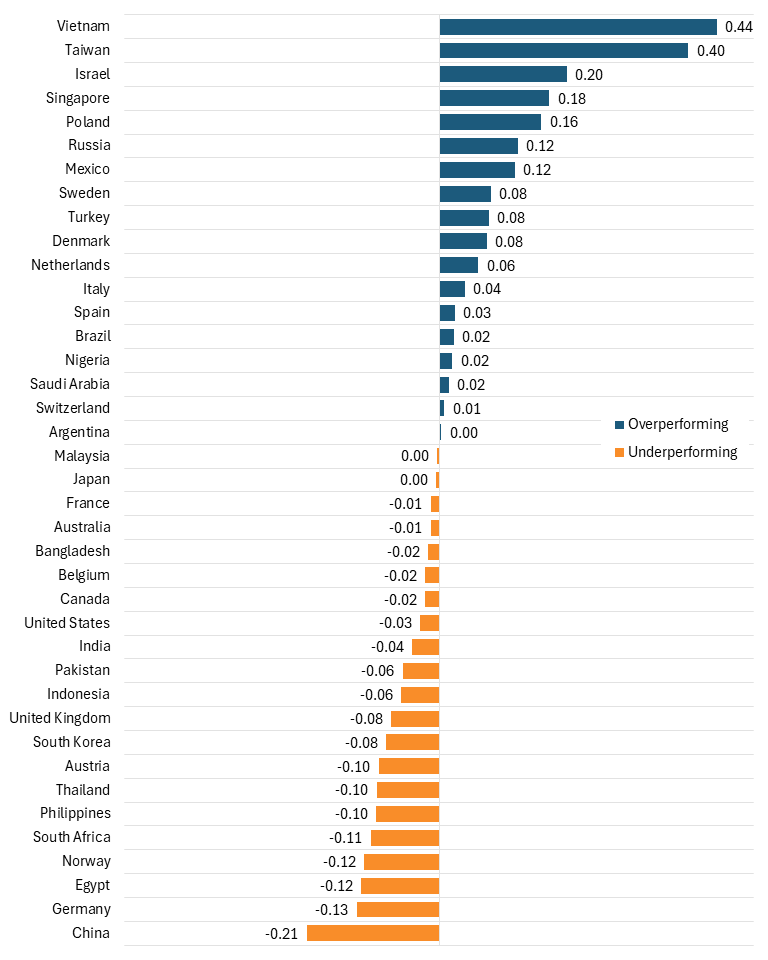

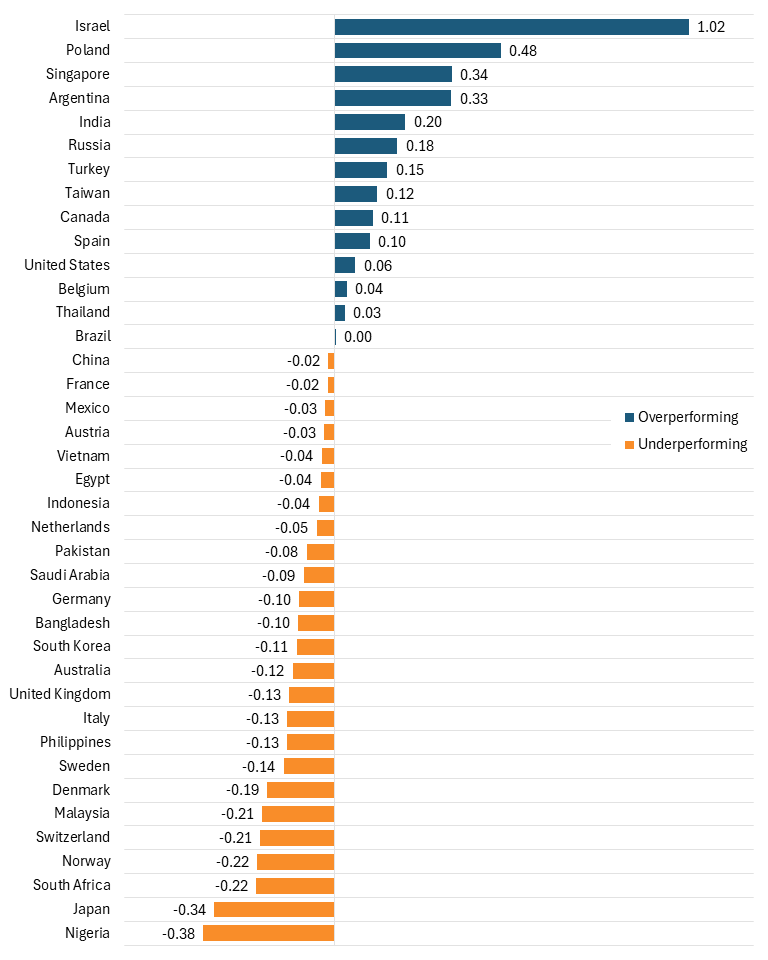

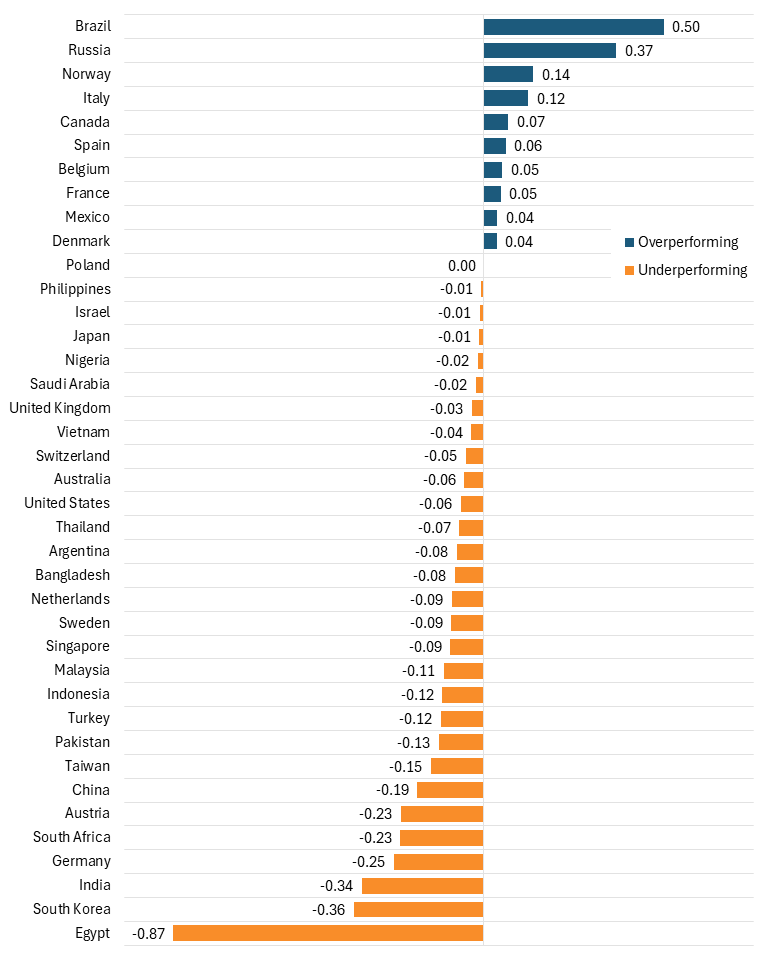

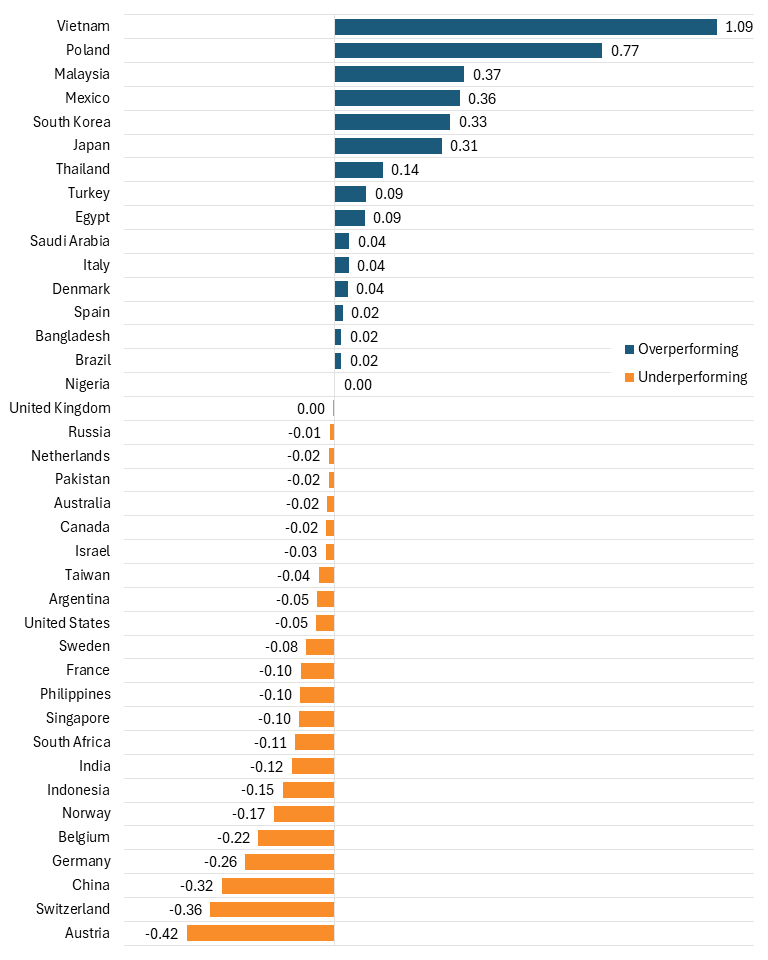

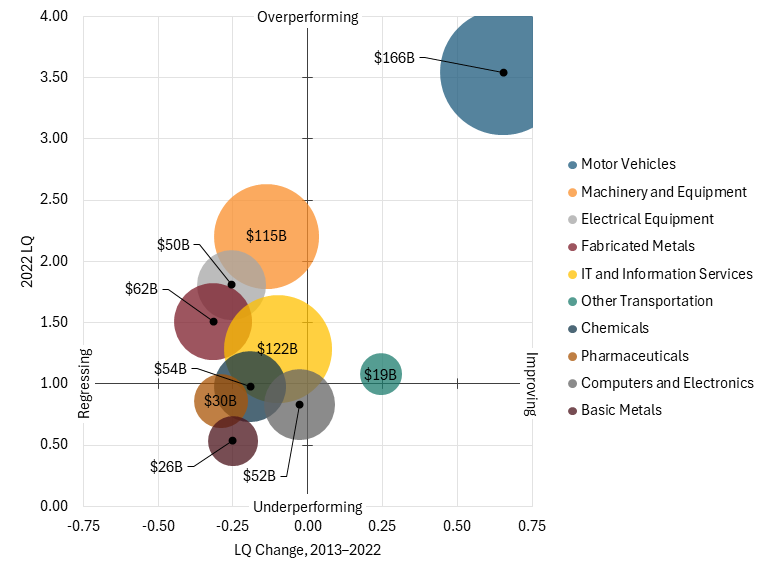

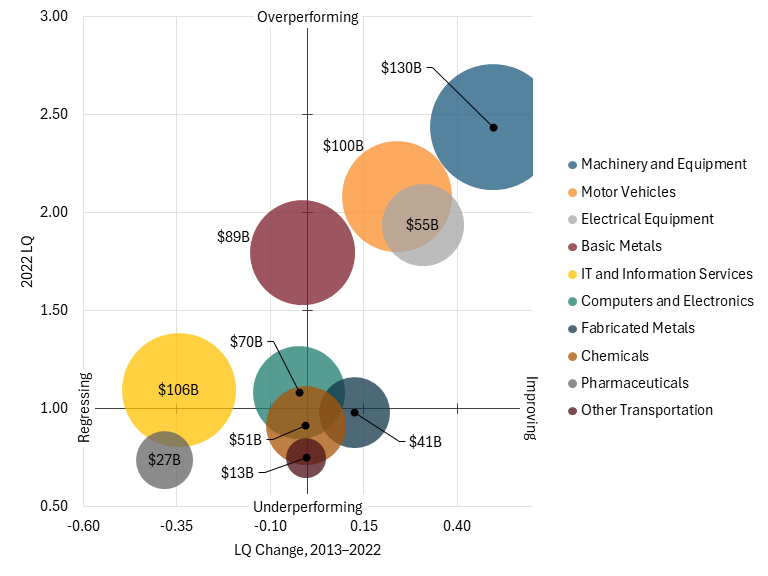

Vietnam saw the largest increase in LQ, rising by 44 percentage points, followed by Taiwan and Israel. Several developing nations saw a moderate rise in LQ, including Poland, Mexico, and Turkey, while the United States, Canada, and Japan were among the nations that experienced moderate declines.

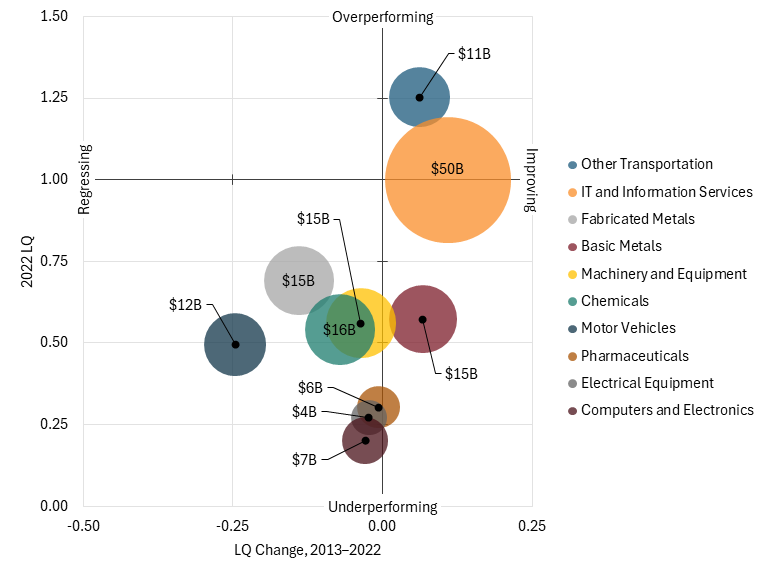

Figure 4: Change in relative national performance in the composite Hamilton Index (LQ difference, 2013–2022)

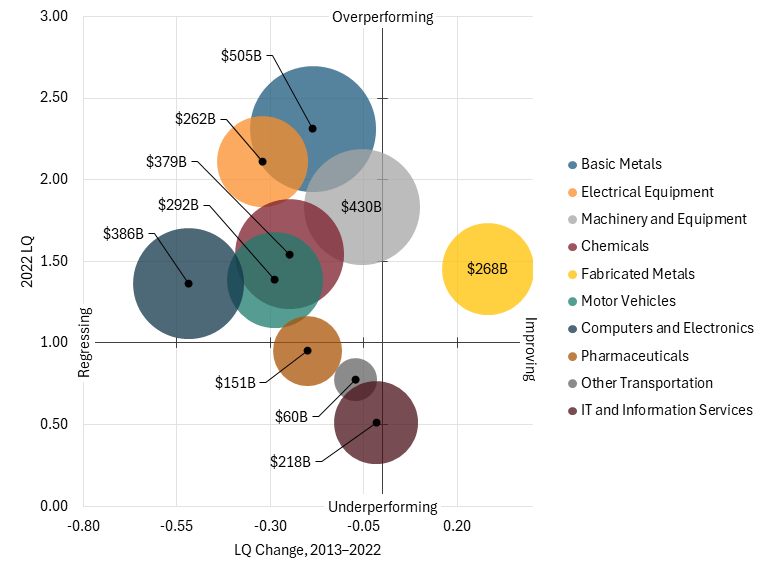

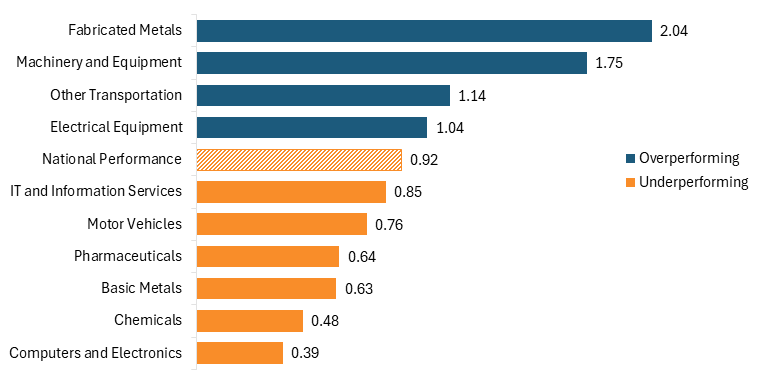

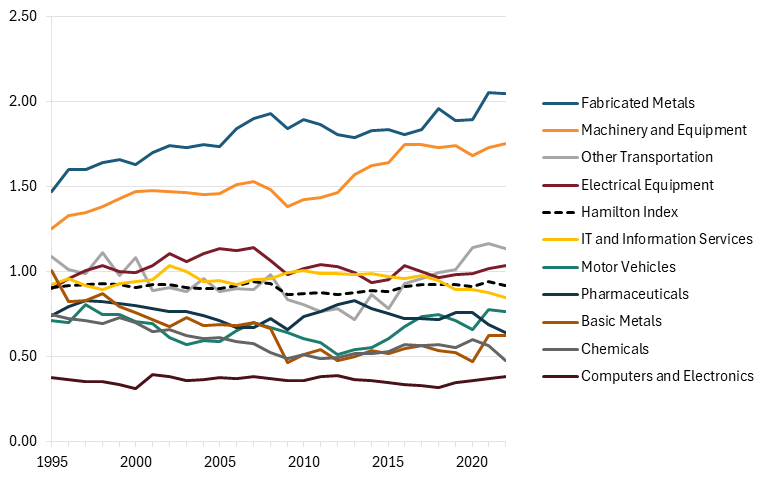

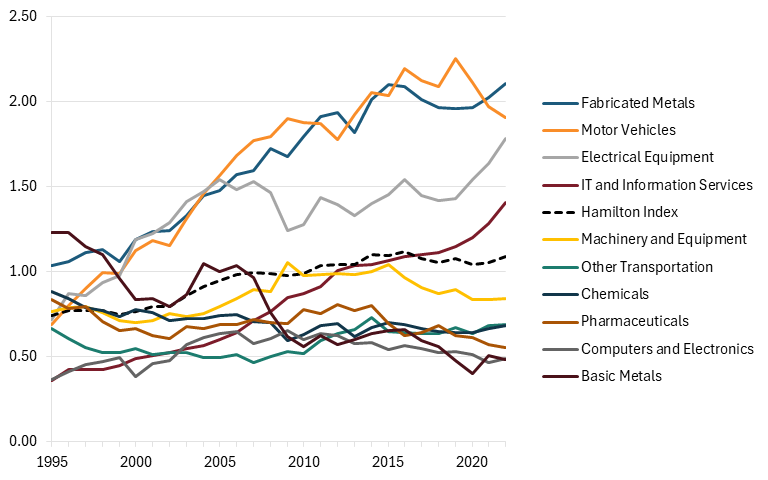

For many countries that overperform on the LQ measure, that strong performance is driven by one or two dominant industries. For example, nearly two-thirds of Taiwan’s and Vietnam’s advanced industry output is from the computer and electronics industry. Countries such as these dominate specific niches but have limited influence over the broader advanced industry ecosystem. By contrast, countries with capabilities spread across multiple advanced industries can exert influence over several supply chains, shaping multiple segments of global trade.

Figure 5 shows the specializations of the largest advanced industry producers using a normalized Herfindahl-Hirschman Index ranging from 0 to 1, wherein 0 indicates an equal distribution of output across all 10 Hamilton industries, while a 1 indicates complete concentration in a single industry (a detailed explanation can be found in appendix D). An index score of 0 to 0.06 indicates that output is broadly distributed across industries, a score of 0.06 to 0.17 indicates moderate specialization, and a score above 0.17 indicates strong specialization.

Unsurprisingly, Taiwan is the most specialized among the top producers, with the majority of its advanced industry output concentrated in a single industry. India, the United Kingdom, France, Canada, the United States, and South Korea all exhibit moderate specialization, with about one-third of advanced industry output originating from their largest sector. China’s relatively low specialization score highlights the broad distribution of its advanced industry production across the full range of Hamilton industries. Even China’s largest advanced industry by output, basic metals, accounts for only 17 percent of its advanced industry output, significantly less than other peer countries’.

China’s dominance differs structurally from that of the United States, and its breadth of capability across industries poses a more systemic challenge. Rather than leading in a narrow set of industries, China is simultaneously building strength across a number of critical sectors. This broad-based industrial capacity enables China to shape multiple supply chains, creating dense industrial ecosystems that reinforce its long-term technological and manufacturing leadership.

Figure 5: Specialization Index Rankings, 2022

And just like countries, some industries are more concentrated than others. For example, South Korea, the country most specialized in chemical manufacturing, has an LQ of 2.16, the lowest among the leading countries, while Taiwan leads in the computer and electronics industry with an LQ of 12.88, the highest among the leading countries. In many industries, a high LQ is reflective of the size of a nation’s economy, with smaller economies, such as those of Taiwan, Israel, Mexico, and Indonesia, more likely to have a single industry that dominates each country’s economy. But in other cases, it is because industries such as machinery, chemicals, and electrical equipment are much broader and have wider arrays of subindustries.

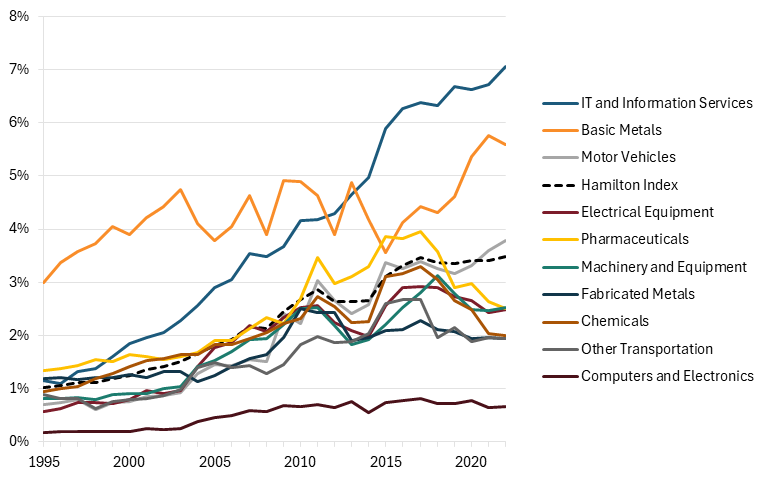

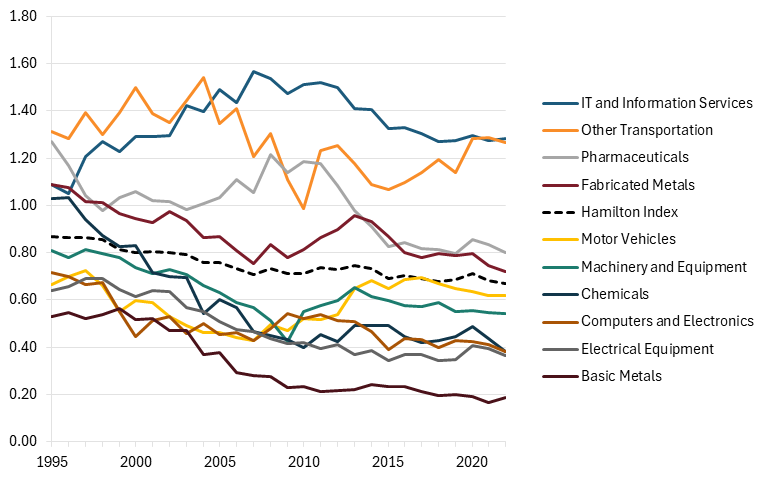

Without IT and information services, the United States has failed to measurably increase its market share in advanced industries over the past decade. The same cannot be said for China.

In terms of absolute production, China is far and away the leader in almost every industry, capturing the largest share of the global market in 7 of 10 advanced industries and holding nearly 25 percent of global market share across Hamilton Industries.

Table 1: Hamilton Index leaders by industry, 2022

|

Industry |

Global Output (Billions) |

Leading Producer |

Leader’s Share |

Relative Leader |

Leader’s LQ |

|

IT and Information Services |

$2,333 |

USA |

36.1% |

Israel |

3.39 |

|

Computers and Electronics |

$1,551 |

China |

24.9% |

Taiwan |

12.88 |

|

Chemicals |

$1,347 |

China |

28.2% |

South Korea |

2.16 |

|

Machinery and Equipment |

$1,287 |

China |

33.4% |

Japan |

2.43 |

|

Basic Metals |

$1,197 |

China |

42.1% |

China |

2.31 |

|

Motor Vehicles |

$1,155 |

China |

25.3% |

Mexico |

3.94 |

|

Fabricated Metals |

$1,013 |

China |

26.7% |

Indonesia |

3.16 |

|

Pharmaceuticals |

$872 |

USA |

28.5% |

Switzerland |

5.62 |

|

Electrical Equipment |

$680 |

China |

38.5% |

South Korea |

2.68 |

|

Other Transportation |

$423 |

USA |

38.5% |

Taiwan |

2.87 |

|

Composite Hamilton Index |

$11,858 |

China |

24.9% |

Taiwan |

2.63 |

Top 10 Producers

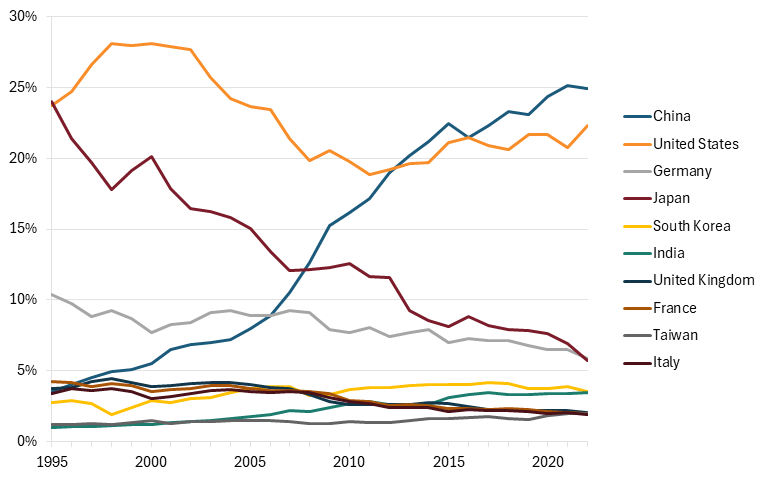

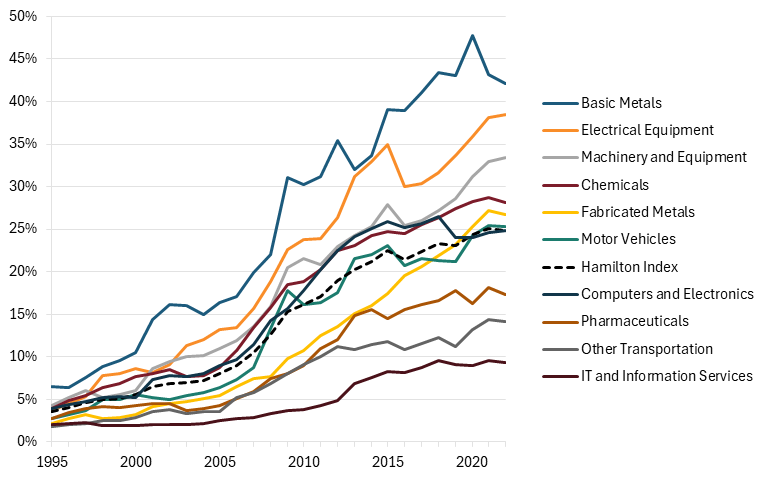

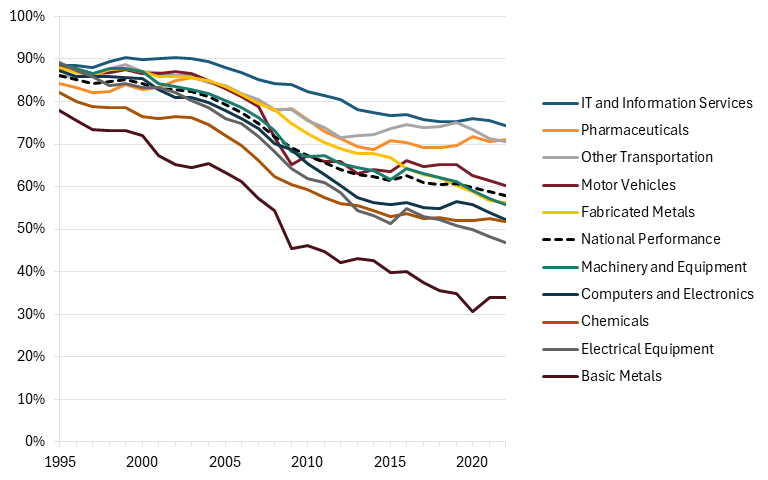

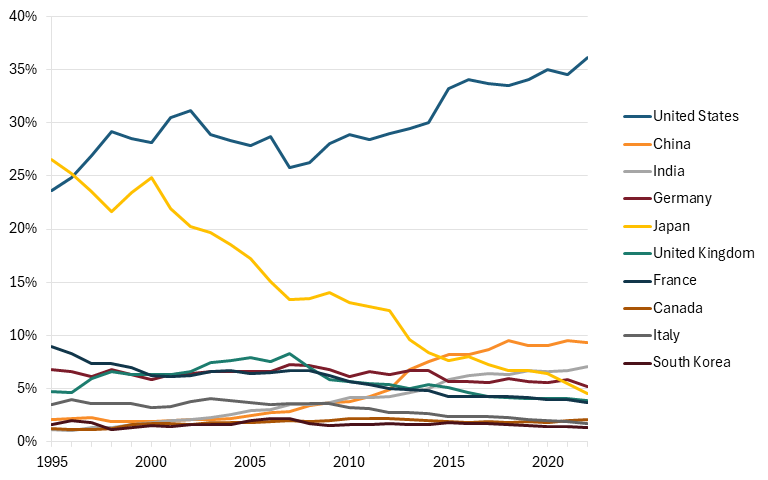

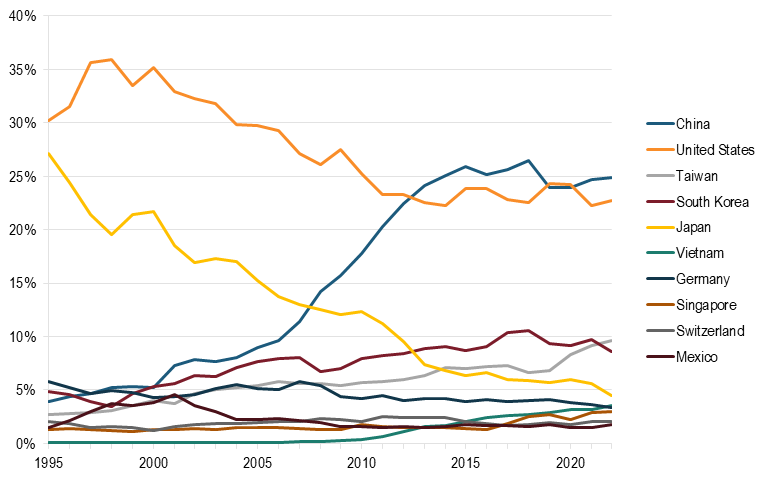

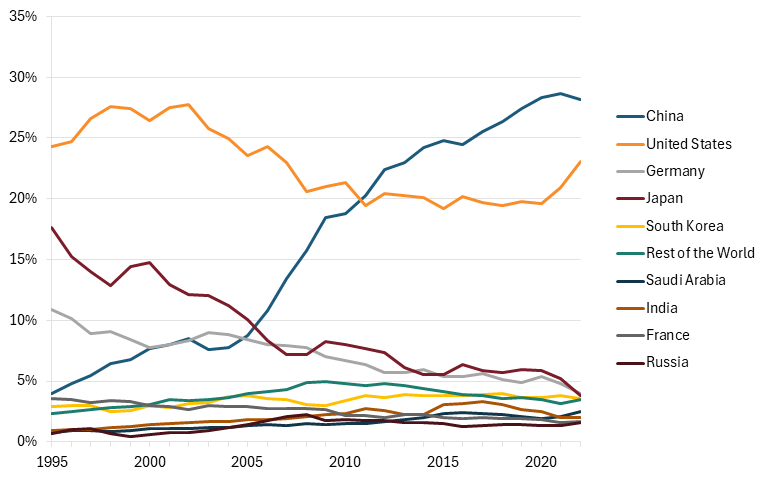

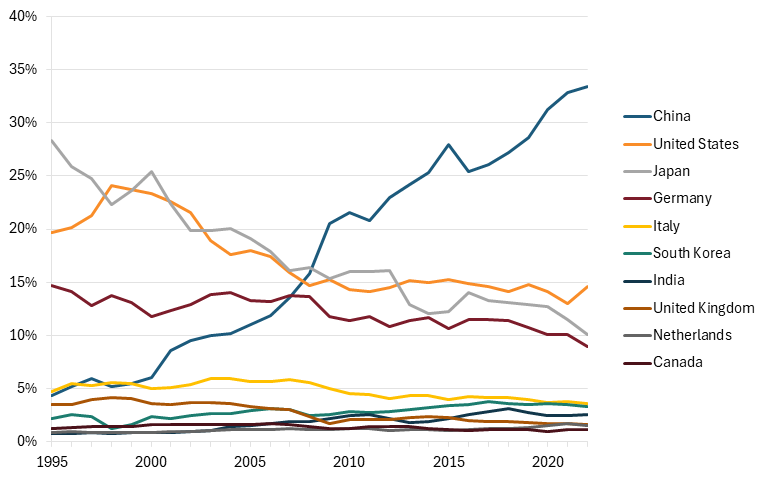

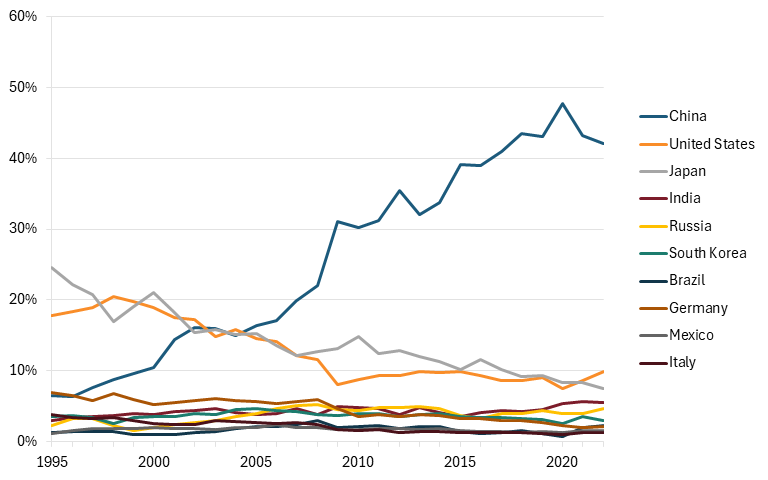

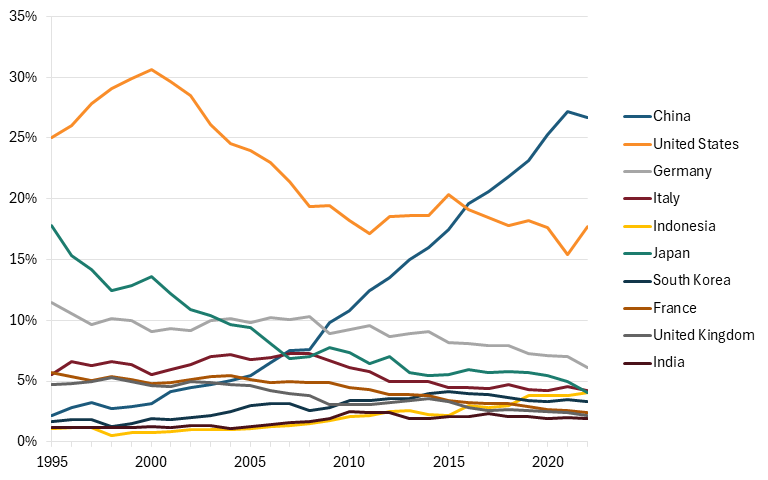

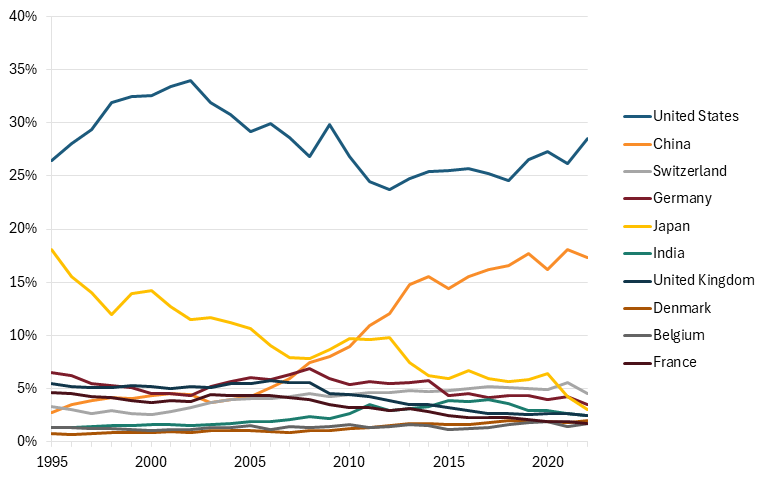

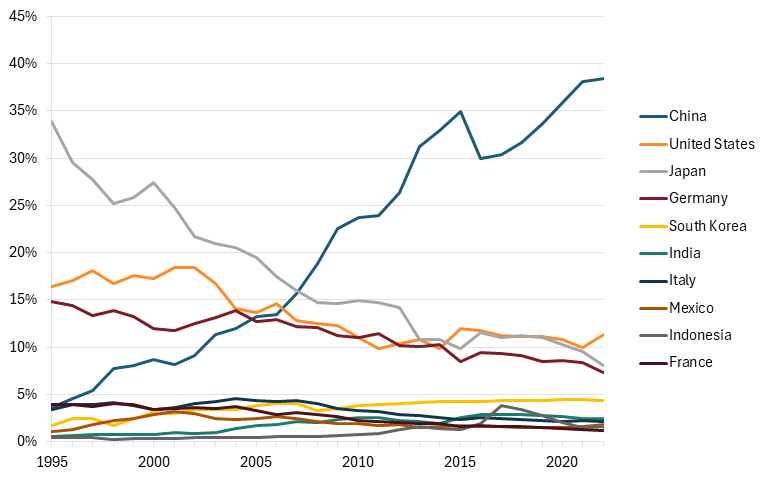

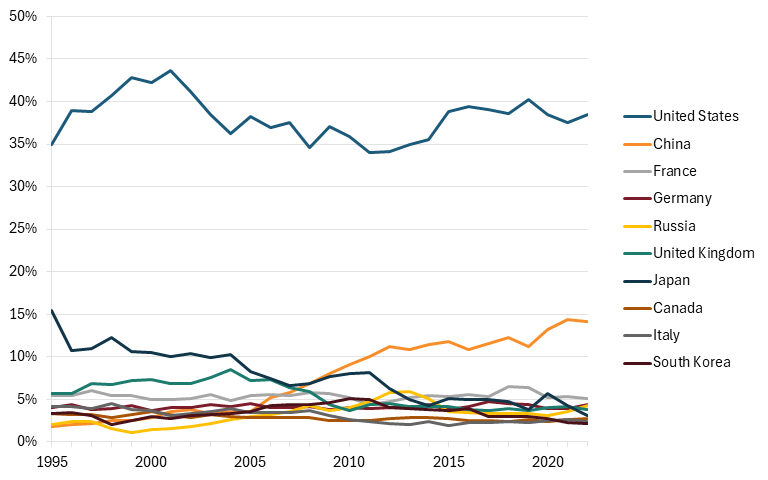

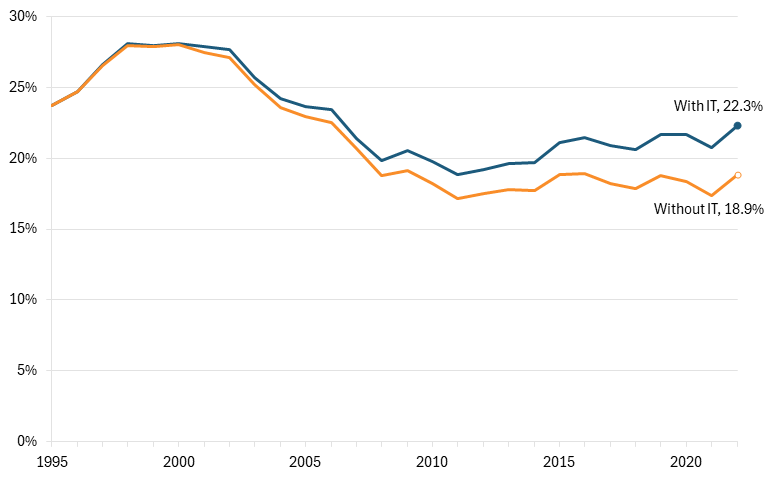

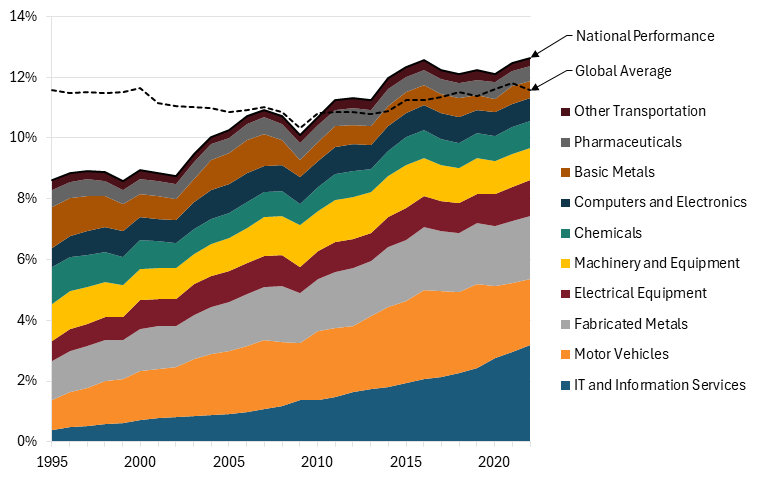

From 1996 to 2012, the United States was the leader in advanced industry output, holding the largest slice of global market share in these 10 industries. However, China’s accession to the World Trade Organization (WTO) in 2001 opened the floodgates to Chinese dominance. Since 2012, China has taken the lead from the United States, currently holding 24.9 percent of global market share, while the United States has fallen to 22.3 percent. Advanced industries being the zero-sum game that they are, the rise of China has been coupled with the decline of several other once-dominant countries. Japan, which led the world in advanced industry market share in 1995, regressed to fourth by 2022, a decline of more than 18 percentage points. Germany, while not declining as much as Japan, also fell by about 5 percentage points. The United Kingdom, France, and Italy have also seen their shares of the global market fall over the past 27 years.

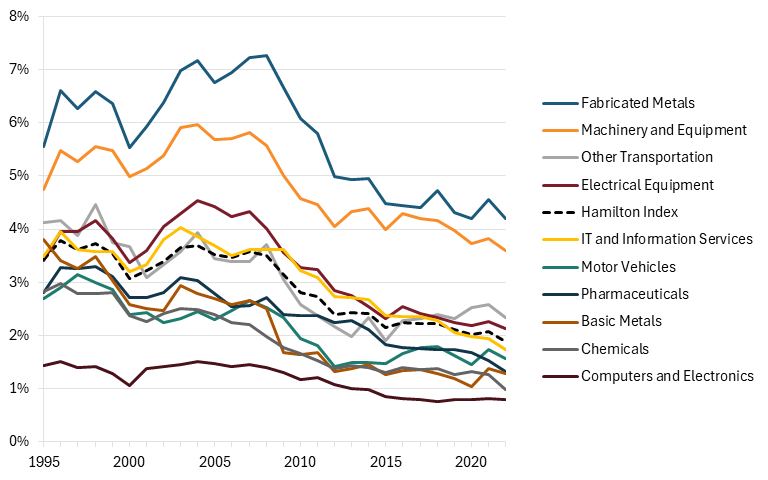

Figure 6: Top 10 producers’ historical shares of global output in Hamilton industries, 1995–2022

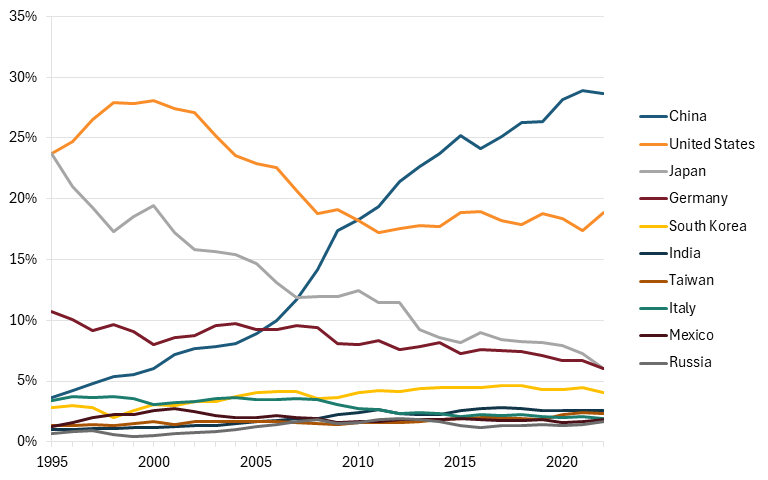

China’s dominance is even more evident when the IT and information services industry is removed from the equation. IT and information services is the largest advanced industry in the United States by a large margin (it made up 32 percent of U.S. advanced industry output in 2022), but it is one of the smallest in China, making up just 7 percent of its output.

When excluding IT, China became the world’s largest producer of advanced industries in 2010, surpassing the United States, and its share has continued to grow rapidly. By 2022, it held nearly 29 percent of the global market share. The United States, on the other hand, has seen its share of these nine industries fall rapidly and then stagnate. Between 2000 and 2011, U.S. market share declined from a high of 28.1 percent to a low of 17.2 percent, and in the years since, it has hovered between 17 and 19 percent. (See figure 7.) Without IT and information services, the United States has failed to measurably increase its market share in advanced industries over the past decade. The same cannot be said for China.

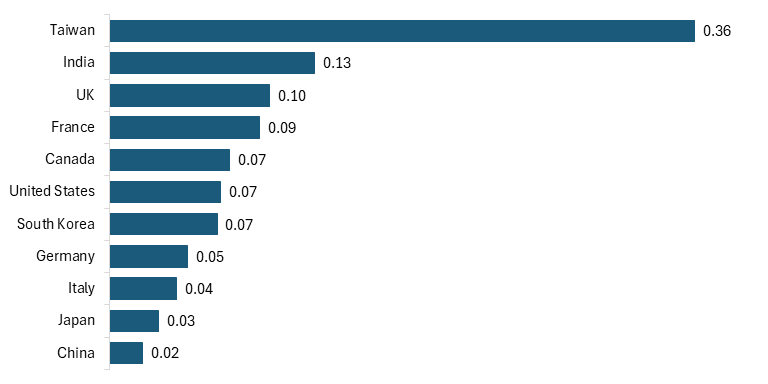

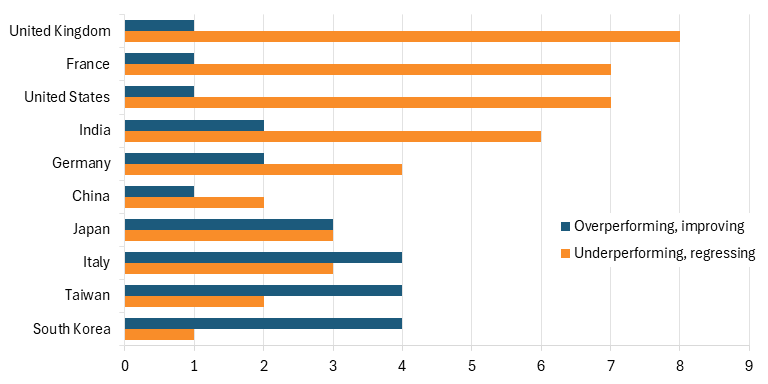

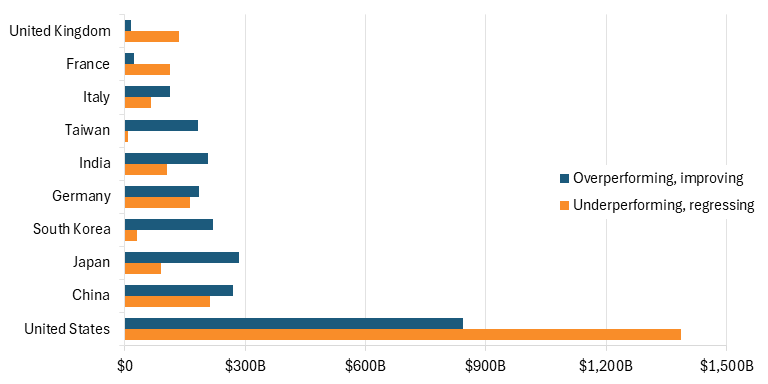

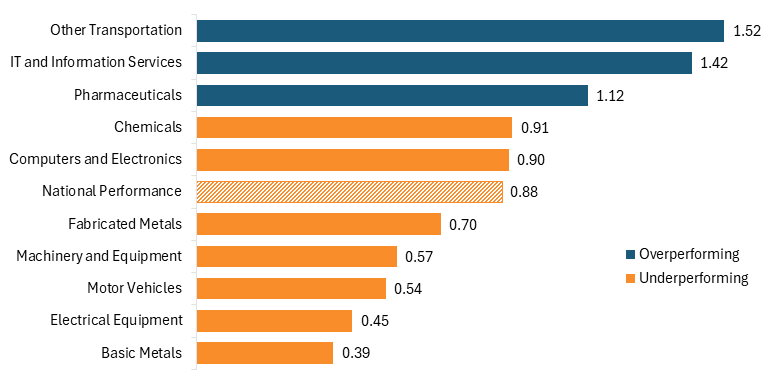

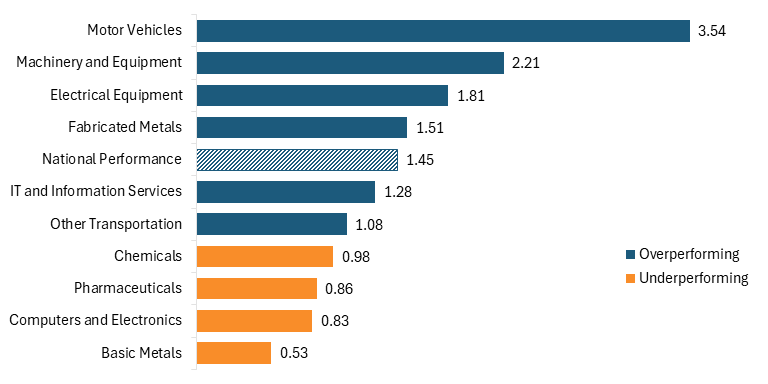

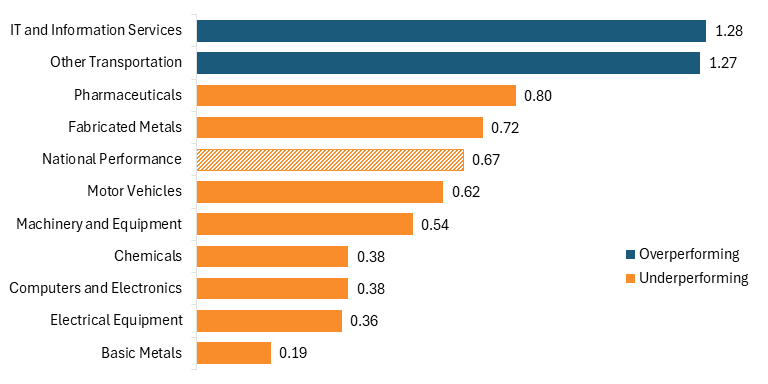

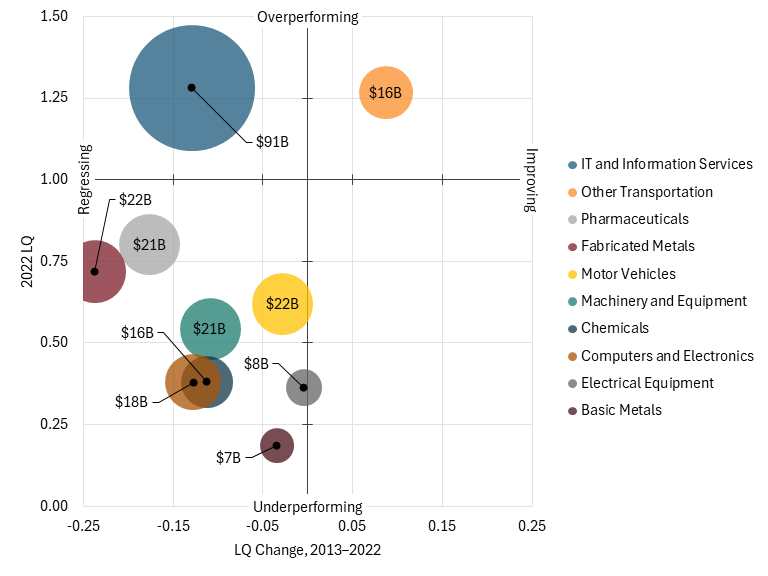

Later in this report, each country is assessed on its LQ in each industry based on whether it is overperforming or underperforming and whether it has improved or regressed since 2013. Both measures taken together are important because having industries that are overperforming but also regressing is not a sign of a strong advanced economy, but rather of a weakening one, while industries that are underperforming but also improving exemplify a developing economy. Figure 8 shows the two extremes, the number of industries that are both overperforming and improving, which will be referred to as strong and growing industries, and underperforming and regressing, which are weak and declining, for the top 10 performers in this Hamilton Index. The countries are organized by the number of industries that are strong and growing relative to those that are weak and declining. South Korea leads the top producers with four strong and growing industries and only one, IT and information services, that is weak and declining. Italy and Taiwan also have four strong and growing industries, but have two and three weak and declining sectors, respectively. These three countries are also the only 3 in the top 10 to have more strong and growing industries than weak, declining ones.

The United States and China have the same number of industries that are strong and growing: just one. However, where they differ is the number of weak industries they have. China has just two industries that fit this classification, whereas the United States has seven. The United Kingdom performs the worst with eight industries that are weak and declining and only one that is strong and growing.

Figure 7: Top 10 producers’ historical shares of global output in Hamilton industries minus IT, 1995–2022

Figure 8: Numbers of comparatively strong and weak industries in the top 10 producer nations

Looking at the value added of these industries, the one industry in which the United States overperformed and improved was the IT and information services industry, with an output of over $800 billion. (See figure 9.) However, the value of industries in which the United States underperformed and regressed was much higher, at $1.4 trillion. Aside from the United States, weak and regressing industries outvalued strong and improving industries only in France and the United Kingdom.

Figure 9: Value-added output by comparatively strong and weak industries in the top 10 producer nations

The China Juggernaut

If there is one takeaway from the past 27 years of advanced industry analysis it is that China is not a normal competitor. Its output across all advanced industries has grown at rates unmatched by any other nation, making it the leader in almost every industry.

China’s share of global advanced industry output has increased by over 21 percentage points, from 3.5 percent in 1995 to nearly 25 percent in 2022. In every advanced industry, China’s output has increased by at least 1,750 percent, with the average increase over 2,200 percent. Compare that with the United States, where output, on average, increased by just 200 percent.

As previously discussed, advanced industry output as a share of GDP has been stable over the 27-year period analyzed in this report, meaning that when one country gained market share, other countries lost it. China’s market share in every advanced industry has grown threefold or more over the past 27 years, leaving it with more than a quarter of global market share in several industries, including fabricated and basic metals, chemicals, machinery, and electrical equipment. (See figure 10.)

Figure 10: China’s global market shares in Hamilton industries, 1995–2022

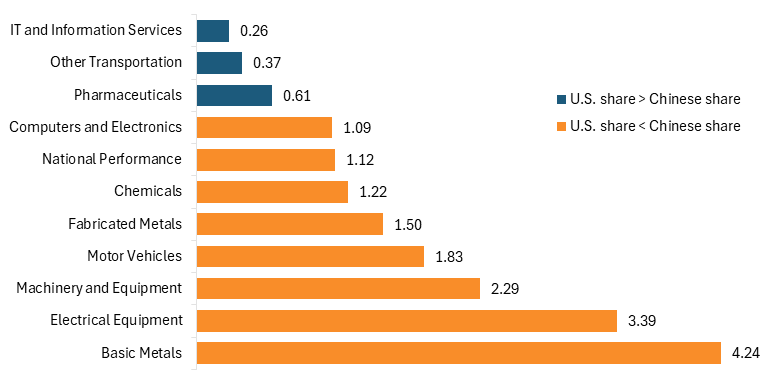

China leads the world in 7 out of the 10 Hamilton industries and therefore leads the United States. Excluding IT and information services, other transportation, and pharmaceuticals, China holds a greater share of the global market than the United States does. Figure 11 shows the ratio of China’s global market share in 2022 to the United States’ share, meaning that industries with a value greater than one are industries in which China holds a larger share of the global market. Though the United States is close to China’s market share in some industries, such as computers and electronics and chemicals, in other industries, such as basic metals, China has a clear and definitive lead.

Figure 11: Ratio of Chinese to U.S. global market share in Hamilton industries, 2022

In the years immediately after its accession to the WTO and up to 2011, China’s advanced industries underwent their most rapid growth in history, with output in these sectors increasing by up to 34 percent annually in some years and by 18 percent on average. Since then, China’s growth has cooled moderately, but it is still one of the fastest-growing advanced industry economies in the world. Overarching industrial strategies, such as the Made in China 2025 Plan, and sector-specific industrial policies have led advanced industries in China to continue growing at unprecedented speed. For example, China’s fabricated metals industry output increased by over 9 percent annually between 2018 and 2022, while output for the rest of the world grew by just 2 percent.

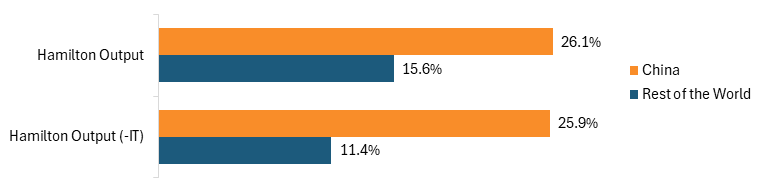

Overall, China’s output in Hamilton industries has increased by over 26 percent since 2018, while the rest of the world’s output has grown by only 15.6 percent. When removing IT and information services, an industry in which the United States and OECD perform strongly, the picture is even grimmer. China’s output increased by 25.9 percent; the rest of the world’s output increased by only 11.4 percent.

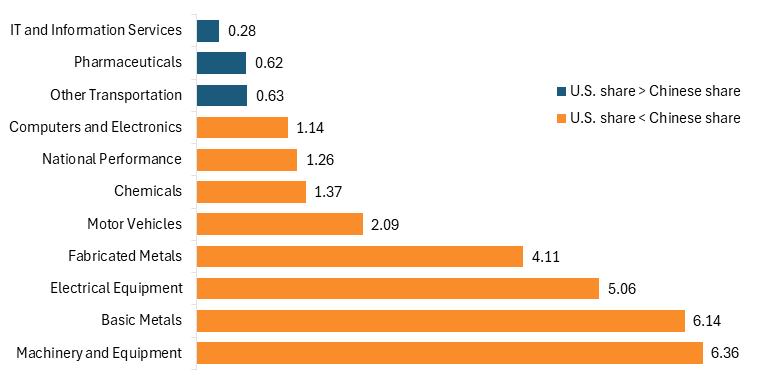

Looking more closely, China’s output has increased faster than the United States’ in seven Hamilton industries. Figure 12 shows the change in China’s output in advanced industries divided by the change in U.S. output. Industries with a value of 1 or more are industries in which China’s output has grown faster than the United States’. In all but IT and information services, other transportation, and pharmaceuticals, China’s output has grown at a greater rate than the United States’, with industries such as basic metals and machinery and equipment growing six times more than that of the United States.

Figure 12: Change in China’s output as a share of the change in U.S. output in Hamilton industries, 2013–2022

To appreciate the enormity of the gap between the United States and China, consider that, in order to match the advanced-industry share of China’s economy, the United States would have needed to increase its output by nearly $1.5 trillion in 2022, a 56 percent increase. An increase of this kind would have required almost doubling output in IT and information services, quadrupling output in computers and electronics, or increasing pharmaceutical output by a factor of six.

Figure 13: Nominal change in output from 2018 to 2022, China vs. the rest of the world

The Fall of the OECD

China’s rise as the leader in advanced industries meant that OECD nations that were once leaders were now followers, and the OECD as a whole no longer had the economic power it once did. Between 1995 and 2022, OECD nations’ market share in advanced industries fell from 86 percent to 58 percent, a 28 percentage-point decline. Put another way, in 1995, more than 8 out of every 10 dollars of value added in advanced industries originated in the OECD; now that figure is down to less than 6. China’s gains in global market share across all Hamilton industries were strongly correlated with the OECD’s losses, with a correlation coefficient of -0.94.

The OECD’s market share declined in every Hamilton industry, but these losses were not distributed evenly. The largest declines for the OECD came in basic metals, where the bloc’s market share fell by 44 percentage points, and in electrical equipment, which declined by 42 percentage points. However, the losses in the basic metals industry appear to have mitigated over the past two years, as the OECD has begun to regain market share (4 percentage points) since 2020. Although not a large jump, the gain represents the first time since 1995 that the OECD’s market share in basic metals has increased for two years in a row. In fact, basic metals is the only industry in which the OECD has increased its market share since 2020. Perhaps unsurprisingly, China ceded market share in this industry between 2020 and 2022. Notably, China still leads the world, controlling 42 percent of the basic metals market.

Figure 14: OECD’s global market share in Hamilton Industries, 1995–2022

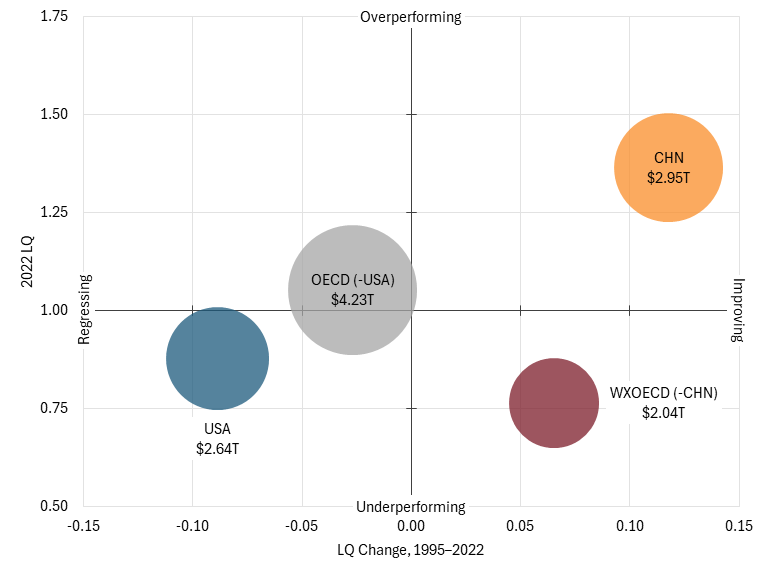

It would be one thing if China’s performance in advanced industries were proportional to the size of its own economy, but over the period from 1995 to 2022, that was not the case. China made a concerted effort to overperform in these industries, recognizing their importance from a geopolitical and economic standpoint, perhaps before many other leading countries. And these efforts largely succeeded. In 2022, China’s value-added output was 36 percentage points more than the global average, while the OECD’s was 2 percentage points less than the global average.

The United States and OECD vs. China and the Rest of the World

The growth of China, while coupled with the decline of the West, has also occurred alongside another geopolitical trend: the rise of the Global South and the developing world. Through programs such as the Belt and Road Initiative, China has leveraged large-scale infrastructure investment worldwide to entrench trade dependencies, reinforce strategic partnerships, and cultivate export markets. Not every non-OECD country takes part in the Belt and Road Initiative; however, the initiative is just an example of how China has used its economic and political power to strengthen the economies of historically economically weaker countries.

In 1995, more than 8 out of every 10 dollars of value added in advanced industries originated in OECD; now that figure is down to less than 6.

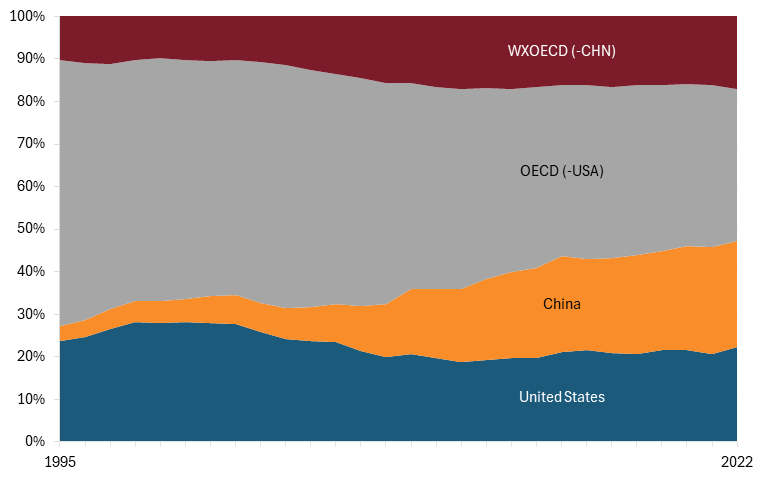

The global market share of non-OECD countries increased by 28.2 percentage points between 1995 and 2022, but most of that increase was driven by China’s growth. Excluding China from the calculation, non-OECD countries still experienced a sizeable increase in market share, rising by 6.9 percentage points. (See figure 15. The bloc of non-OECD countries without China is shown as WXOECD (-CHN).)

Most of the industries that non-OECD economies, excluding China, excelled in include traditional heavy manufacturing industries, such as basic and fabricated metals and electrical equipment. These industries saw their market shares increase between 7 and 8.5 percentage points. However, the industry in which the bloc experienced the greatest increase was computers and electronics, where its global market share rose by 14 percentage points, driven by Vietnam’s growth as a hotspot for electronics manufacturing.

Figure 15: Global market shares of Hamilton industries for the United States, OECD, China, and non-OECD countries, 1995–2022

The push for China-Plus-One or China-Plus-Many strategies, wherein companies diversify manufacturing by opening operations in other countries with favorable labor costs, may mean that non-OECD countries could see a greater increase in market share in the near future.

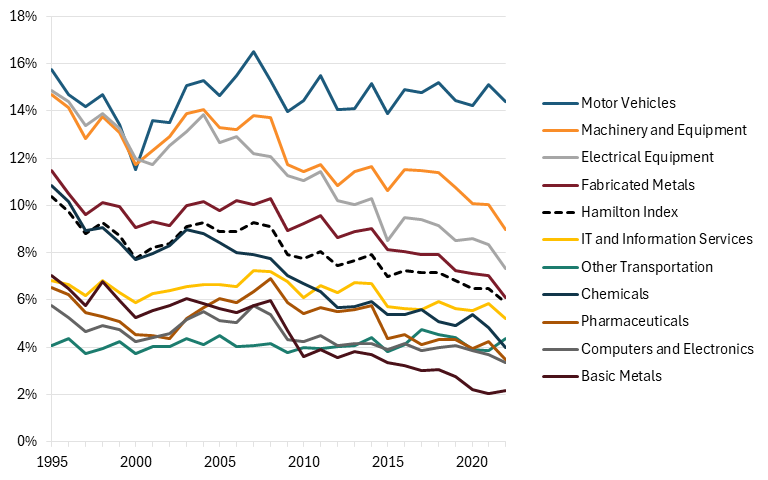

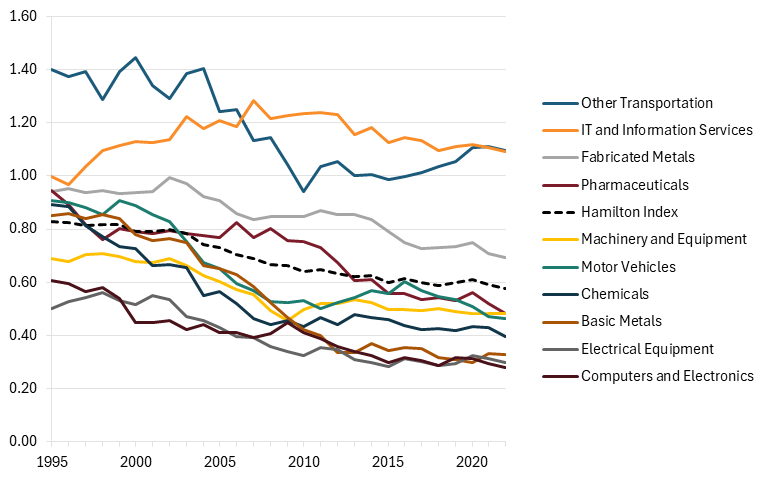

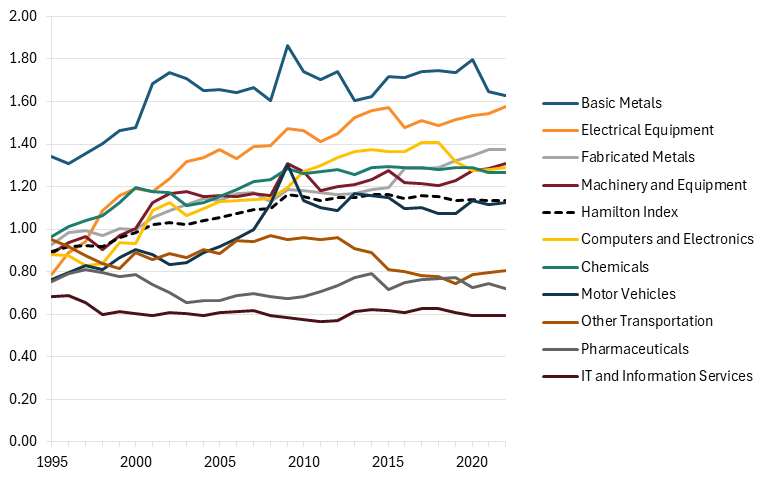

In terms of LQ, both China and non-OECD countries have seen their LQs improve since 1995, though non-OECD nations still underperformed relative to the world average as of 2022 (figure 16). Between 1995 and 2022, non-OECD nations, excluding China, saw their LQ increase by 7 points, while China’s increased by 12 points. In comparison, OECD and the United States declined in relative performance, with their LQs falling by 9 and 3 points, respectively, further demonstrating the shift from Western world dominance to closer parity in advanced industry production between developed and developing nations.

Figure 16: Net performance in Hamilton industries since 1995 (scaled to 2022 output)

China’s growth as a leader in advanced manufacturing and its ability to capture large swaths of market share over the past 27 years have meant that many developing nations have not been able to become strong advanced manufacturing hubs when they otherwise may have. However, the tensions around China have driven companies toward China-Plus-One or China-Plus-Many strategies, in which they diversify manufacturing by opening operations in other countries with lower labor costs. These strategies may mean that non-OECD countries will see a greater increase in market share in the near future.

Industry Profiles

Data Visualizations for Each Advanced Industry

Use the data visualization tool to browse the complete dataset for all 10 advanced industries and the composite index: “The Hamilton Index, 2026: Data Visualization for Industries.”

IT and Information Services

IT and information services includes several IT services subindustries, such as software development (including artificial intelligence (AI)), cloud computing, Internet services, and data processing and hosting. It is strategically important due to its high wages and international trade volume and is recognized as a key driver of innovation, as seen in the AI industry in recent years.

The industry has grown substantially over the past 27 years, with output rising 592 percent in nominal U.S. dollars from 1995 to 2022, making it the largest advanced industry in the world since 2003. The industry also grew by more than two times global GDP over the same period: 229 percent. Unlike most other advanced industries, the IT and information services industry is concentrated in the OECD, accounting for 74 percent of global market share. However, the OECD’s dominance in this industry has declined slightly, falling from a peak of 90 percent in 2003.

The United States leads as the top individual nation, holding 35 percent of global market share in the industry, up from 24 percent in 1995. U.S. dominance in IT and information services has been driven by the emergence and growth of key technology companies, including Amazon, Google, Meta, and, more recently, leading AI firms such as OpenAI and Anthropic. (See figure 17.) Considering the United States’ continued dominance in AI through 2026, it is likely the United States will maintain its leadership in the industry for the next several years. The next highest-ranking nations are China (9.3 percent), India (7 percent), and Germany (5.2 percent). The EU, not including Ireland, has seen its share fall by 6 percentage points since 1995 as its reliance on U.S. and Chinese information systems has grown.

The OECD’s dominance in the IT services industry has declined slightly, falling from a peak of 90 percent in 2003 to 74 percent in 2022. The market share of non-OECD countries increased to 38.4 percent in 2022.

Countries that saw the greatest growth in their global market share of the IT industry over the 27-year period include the United States, which increased its lead by 12.5 percentage points, China (7.3 percentage points), and India (5.9 percentage points). Non-OECD countries collectively saw their global market share increase by more than 13 percentage points, to 38.4 percent, as of 2022. Conversely, Japan, which led the world in this industry through 1996, experienced a 22 percentage-point decline, the largest among any nation. The United Kingdom also saw its share fall by over 5 percentage points.

Figure 17: Top 10 producers’ historical shares of global output in IT and information services, 1995–2022

Looking at relative performance, Israel leads the world with an LQ of 3.39, driven by high investment and technology crossover from its well-funded military and defense industry. Other strong relative performers include India (LQ of 2.16), Sweden (2.10), the United States (1.42), France (1.35), Switzerland (1.30), the Netherlands (1.29), and Germany (1.28). Several European nations make up the top 10, with others, including Belgium, Austria, Denmark, and Spain, performing well, with LQs of 0.9 or higher. Collectively, the EU boasts an LQ of 1.23, not far behind the United States, which it targets with nontariff attacks such as substantial fines on U.S. tech firms. The EU has recently reignited rhetoric pushing for “digital sovereignty”—a costly mission that is sure to damage European firms and consumer connectivity more than improve European technology production.

China has an LQ of 0.51, the lowest of all its advanced industries, putting it on par with other developing and low-income nations, including Argentina, Russia, and Malaysia. Despite its high global market share, China’s output in this industry is relatively low relative to the size of its economy. It is likely that, as China continues to invest more in AI development and pushes toward digital and technological sovereignty, China’s LQ in this industry will increase. It has already begun elevating national champions such as start-up DeepSeek and Alibaba, both of which have developed high-level AI tools. Lagging nations include Pakistan, Egypt, Indonesia, and Mexico, which have LQs of 0.2 or lower. (See figure 18.)

As well as having the highest LQ, Israel has experienced the greatest growth in LQ over the past decade, increasing by 102 percentage points from 2013 to 2022. Other highly improved nations include Poland (48 points increase), Singapore (34 points), Argentina (33 points), and India (20 points). The U.S. LQ increased by 6 points over this period, rising slowly but steadily each year, while China’s LQ declined by 2 points. Nigeria experienced the greatest decline in its LQ, with a fall of 38 points, just slightly more than the next-greatest decline, Japan. This coincides with the substantial decline in Japan’s global market share over the same period.

Figure 18: Relative performance in IT and information services (2022 LQ)

Figure 19: Net change in relative performance in IT and related services (LQ difference, 2013–2022)

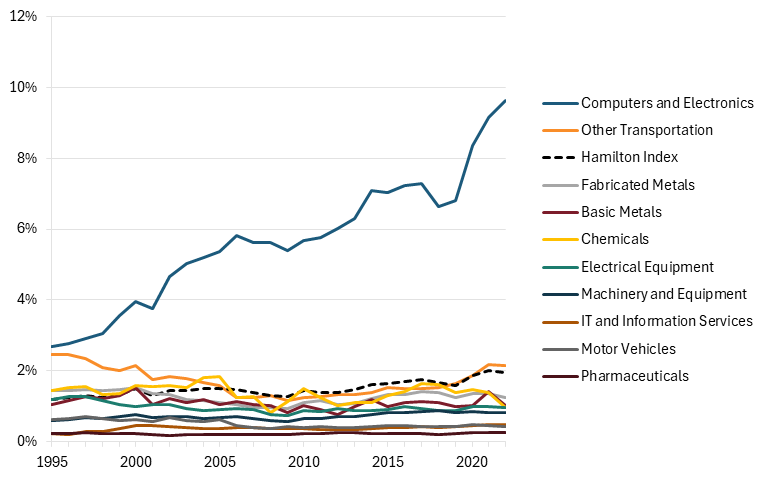

Computers, Electronics, and Optical Products

The computers, electronics, and optical products industry includes the production of displays, electronic hardware, and semiconductors. As such, it’s a fiercely contested industry today.

This industry has nearly tripled in output since 1995, growing by 198 percent globally, making it worth over $1.5 trillion. However, this has still been less than the growth of global GDP, which has grown 229 percent. This industry is highly concentrated in South and Southeast Asia, where industry leaders such as Huawei, Taiwan Semiconductor Manufacturing Corporation (TSMC), Samsung, and LG are located, all of which dominate their respective markets. However, China stands out as the clear leader among these countries. Controlling nearly 25 percent of the global market share, China has become the global leader in electronics manufacturing through concerted national development plans designed to empower national leaders, such as Huawei and SMIC, the leading Chinese semiconductor manufacturer. In its “Made in China 2025” Plan, China has provided these firms with substantial subsidies and explicitly pushed for technological sovereignty, encouraging Chinese firms to purchase only domestically produced hardware and capital, thereby further driving China’s dominance.

China’s rise has been coupled with the United States’ fall. The United States has gone from the global leader to second place, declining from 30 percent of global market share to 22.7 percent. Behind the United States are Taiwan (9.6 percent), South Korea (8.9 percent), Japan (4.5 percent), Vietnam (4.5 percent), and Germany (3.5 percent). The EU has also lost significant market share, most of which can be attributed to the EU-17—the original members of the EU that joined before 2004. The EU held 7.8 percent of global market share in 2022, a fall from 15.3 percent in 1995.

Controlling nearly 25 percent of the global market share, China has become the global leader in electronics manufacturing through concerted national development plans.

China’s global market share has increased by nearly 21 percentage points since 1995, the most of any country in the Hamilton Index and three times more than the next closest country. Other countries that have experienced high levels of growth include Taiwan (6.9 percentage points), Korea (3.7 percentage points), Vietnam (3.5 percentage points), and Singapore (1.7 percentage points). Non-OECD countries collectively have seen their global market share increase by 34.9 percentage points, while the OECD has declined by the same amount, leaving OECD nations to hold 52.3 percent of global market share. Like IT services, Japan has experienced a sizeable fall from grace, with its global market share falling by 22.7 percentage points.

Figure 20: Top 10 producers’ historical shares of global output in computers and electronics, 1995–2022

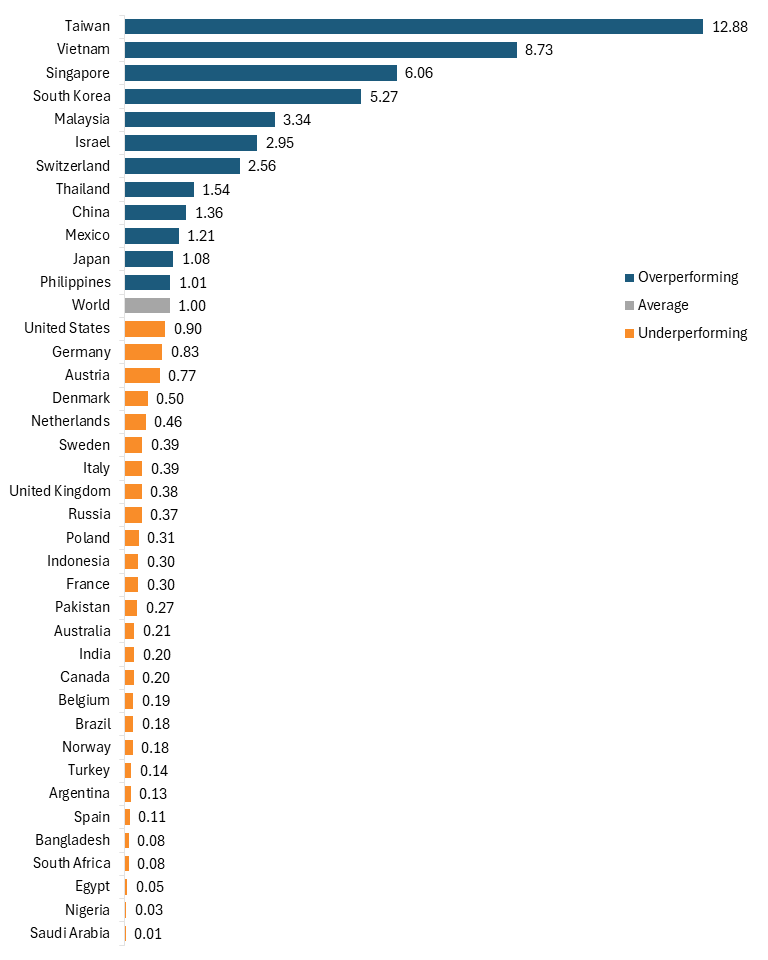

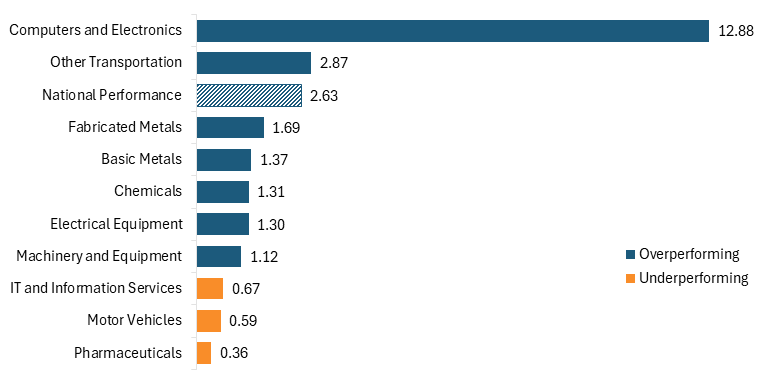

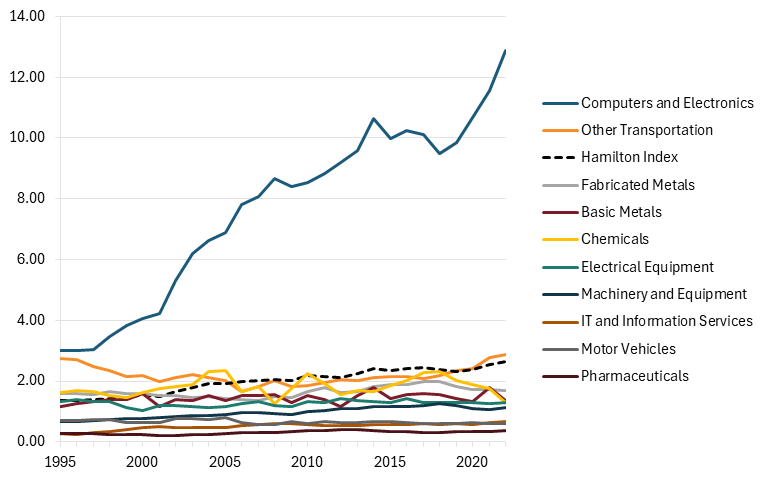

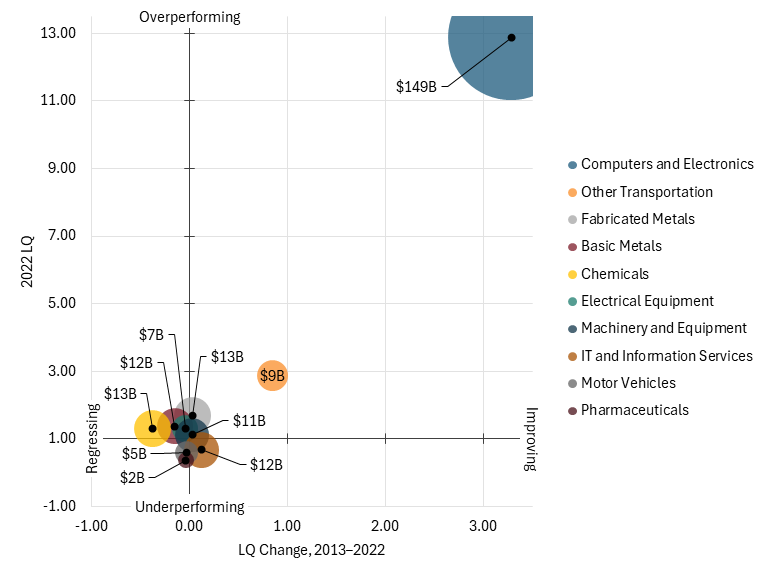

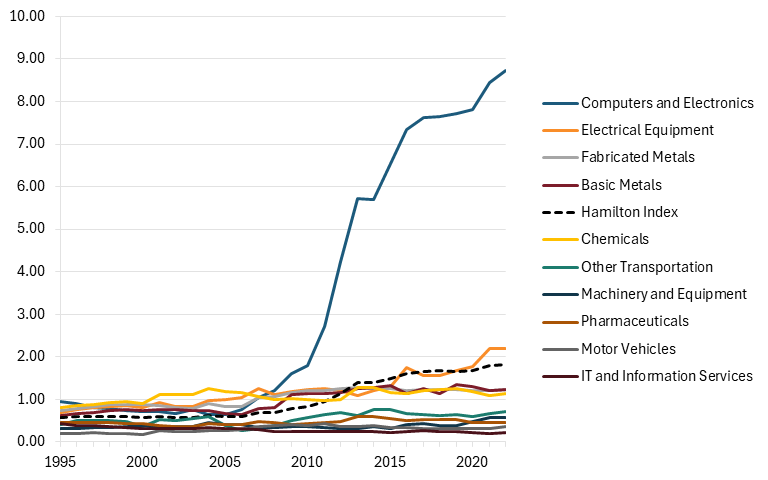

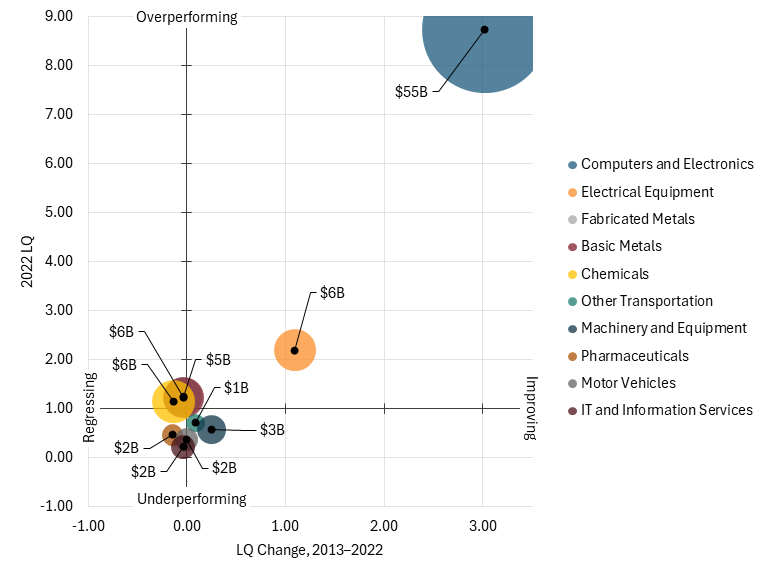

Taiwan is the leader in relative performance in computer and electronic manufacturing with an LQ of 12.88, meaning its production in this industry is nearly 12 times larger than expected based on the size of its economy. Taiwan is the world’s largest manufacturer of advanced logic chips, led by TSMC.[5] Other countries with leading LQs include Vietnam (8.73), Singapore (6.06), South Korea (5.27), Malaysia (3.34), and Israel (2.95). In contrast, the United States is underperforming in this industry with an LQ of 0.90, along with several European nations, including Germany (0.83), Austria (0.77), Denmark (0.50), and the Netherlands (0.46).

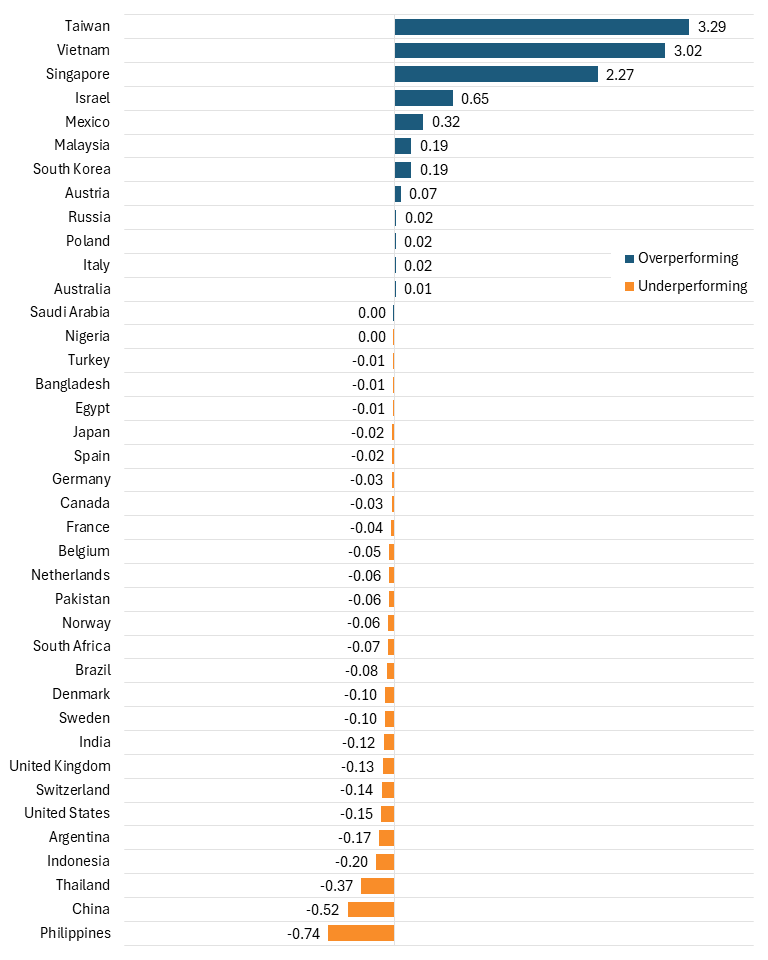

Taiwan underwent the most dramatic increase over the past decade. Its LQ in this industry increased by 329 percentage points, a dramatic increase reflective of its transformation into one of the largest electronics exporters in the world.[6] Vietnam also grew significantly over this period (302 percentage points), followed by Singapore (227 points), and Israel (65 points). Both the United States and China LQ fell over this period by 15 and 52 points, respectively.

Geopolitically, the Belt and Road Initiative overperforms in this industry with an LQ of 1.29, a decrease of 8 percentage points since 2013. At the same time, the OECD and the EU have both seen a decline in relative performance in this industry over the same time period, with OECD and the EU declining by 3 percentage points each, giving them LQs of 0.88 and 0.48, respectively, in 2022.

Figure 21: Relative performance in computers and electronics (2022 LQ)

Figure 22: Net change in relative performance in computers and electronics (LQ difference, 2013–2022)

Chemicals

The chemicals industry includes both specialty chemicals and commodity chemicals, though it does not include any products made by the pharmaceutical industry. This sector produces critical inputs to national power industries such as electronics and defense industries.

Globally, this industry has grown by 211 percent in nominal U.S. dollars since 1995, but at a slower pace than global GDP, which has grown by 229 percent. The industry’s value-added output in 2022 reached $1.3 trillion. This industry is highly concentrated between the United States and China, with the two countries collectively making up over half the global market. China leads the world with 28 percent of global market share, followed by the United States, which holds 23 percent. However, it was once the United States that led this industry by a large margin, holding 24 percent of global market share while China held just 4 percent. OECD, which once controlled 82 percent of the global market in 1995, held 52 percent as of 2022.

Outside the two leaders, this industry is widely dispersed across other nations, with Germany, the third-largest chemical manufacturer, holding 4 percent of the global market, followed by Japan (3.8 percent) and South Korea (3.5 percent). Japan lost the largest slice of global market share over the 27-year period, losing 13.8 percentage points. The EU and the Quad, which includes Australia, Japan, India, and the United States, both declined by about 14 percentage points, sizable losses largely driven by declines in the United States, Japan, and Germany. Saudi Arabia, India, and Russia all increased their global market share by about 1 percentage point.

Figure 23: Top 10 producers’ historical shares of global output in chemicals, 1995–2022

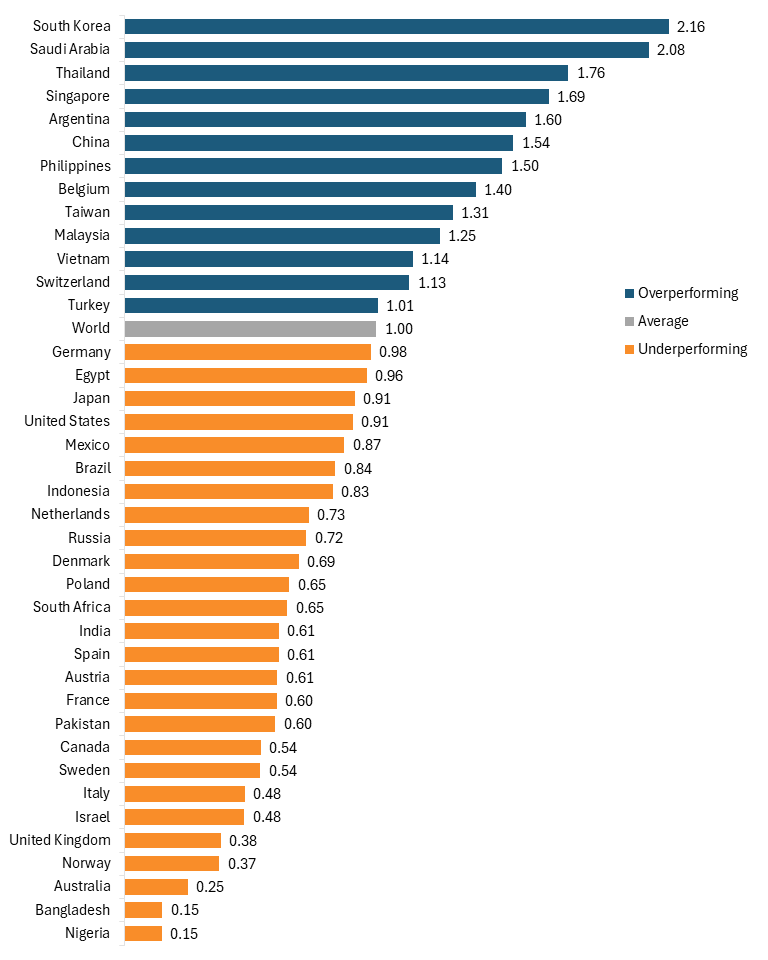

The picture is quite different when it comes to industrial specialization. In 2022, the nation with the highest LQ was South Korea, at 2.16. Other high-ranking countries were Saudi Arabia (2.08), Thailand (1.76), Singapore (1.69), Argentina (1.60), and China (1.54). While it still overperforms, China’s LQ has fallen over the past decade from a high of 1.79 in 2013. Similarly, the United States, which underperforms in the chemical industry with an LQ of 0.91, has also seen its LQ decline since 2008, albeit more moderately, falling from 0.94 in 2013.

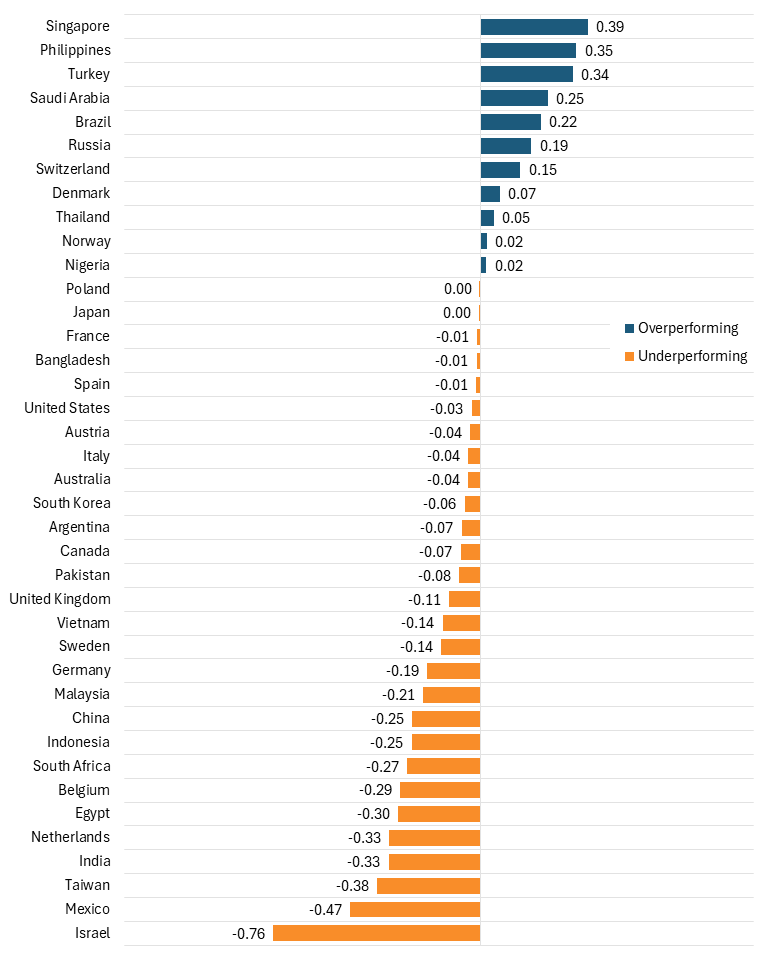

Looking at the change in relative performance, Singapore saw the largest increase in LQ over the period from 2013 to 2022, rising by 39 percentage points. The Philippines (35 percentage points), Turkey (34 percentage points), Saudi Arabia (25 percentage points), and Brazil (22 percentage points) also experienced significant increases in LQ. By contrast, Israel (76 points), Mexico (47 points), Taiwan (38 points), and India (33 points) all experienced a substantial decline in LQ over the 10-year period.

Geopolitically, both the Belt and Road Initiative and the collective non-OECD nations overperformed in chemical production. On the other hand, the OECD moderately underperforms, with an LQ of 0.87, a marked decline from 1995, when its LQ reached 1. Similarly, the EU has an LQ of 0.73, down from 0.99 in 1995.

Figure 24: Relative performance in chemicals (2022 LQ)

Figure 25: Net change in relative performance in chemicals (LQ difference, 2013–2022)

Machinery and Equipment

The machinery and equipment industry comprises machine tools and mechanical systems, including agricultural machines, engines, turbines, and industrial machines.

Globally, this sector grew by 157 percent in nominal U.S. dollars, though slower than the rate of global GDP growth—229 percent—while total value added output in this industry reached $1.3 trillion in 2022. OECD nations lost significant market share in this industry, falling from holding 89 percent of the global market in 1995 to just 56 percent in 2022.

Looking at individual countries, China leads the world and has done so for nearly a decade and a half. China holds over one-third of global market share, followed, not closely, by the United States, which holds just 14.6 percent. Other high-ranking nations are Japan (10.1 percent), Germany (9 percent), Italy (3.6 percent), and South Korea (3.3 percent).

China’s growth in this industry is unmatched, having captured 29 percentage points of global market share over the past 27 years. This rapid growth has led to a corresponding increase in the Belt and Road Initiative’s global market share, of which China is a part. Japan has suffered the greatest decline in market share, losing 18.2 percentage points, while other OECD countries, such as Germany (5.7 percentage points), the United States (5.1 percentage points), the United Kingdom (1.8 percentage points), and France (1.8 percentage points) have also lost market share.

Figure 26: Top 10 producers’ historical shares of global output in machinery and equipment, 1995–2022

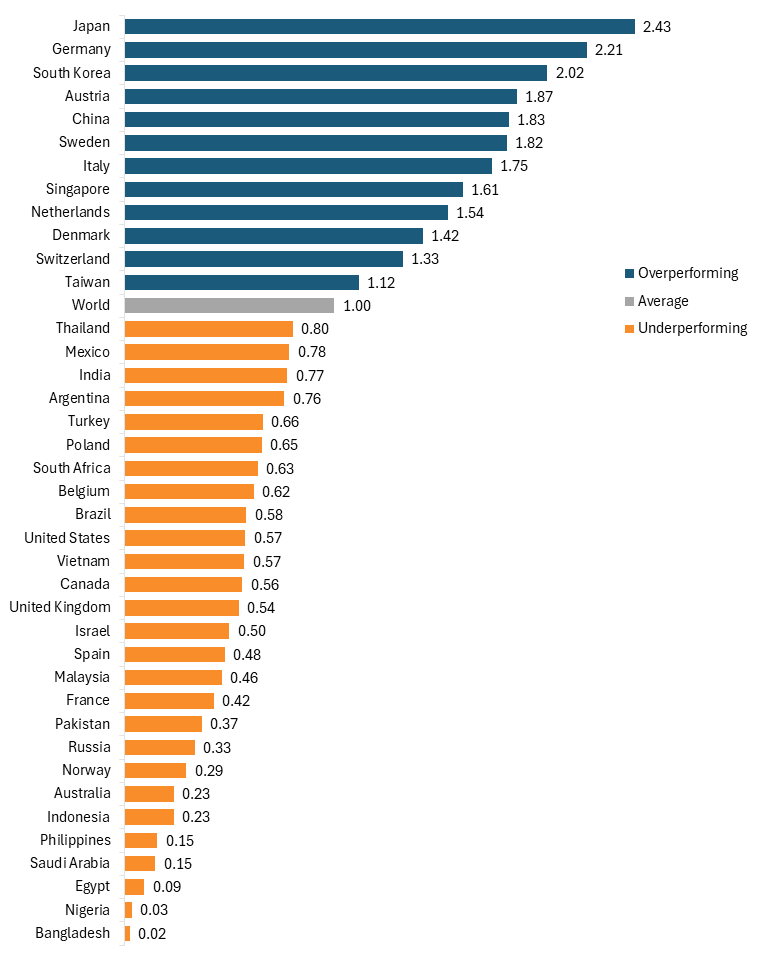

Despite its loss of substantial market share, Japan leads the world in industrial specialization with an LQ of 2.43. In fact, its LQ has actually increased since 1995, from 1.59, due in part to the decline in Japan’s GDP over this period. Germany also exhibits high industrial specialization with an LQ of 2.21, followed by South Korea (2.02), Austria (1.87), China (1.83), and Sweden (1.82). The United States performs poorly in this industry, as much of the heavy manufacturing activity that used to occur in the United States has been offshored. Other developed nations that perform poorly include Belgium (0.62), Canada (0.56), the United Kingdom (0.54), and Australia (0.23).

The Netherlands experienced the largest percentage-point increase in its LQ from 2013 to 2022, rising by 54 percentage points. Other nations that experienced high growth include Sweden (52 percentage points), Japan (50 percentage points), South Korea (27 percentage points), and Vietnam (25 percentage points). The United States and several other developed nations declined over this period, including the aforementioned poor performers, while China’s LQ fell by just 5 percentage points.

Looking at this data with a geopolitical lens, the OECD, when excluding the United States, actually overperforms in this industry with an LQ of 1.21, and, relatedly, the EU (excluding Ireland) also overperforms with an LQ of 1.31. Alliances and trade organizations that include the United States, such as the United States-Mexico-Canada Agreement (USMCA), the Quad, and AUKUS (which includes Australia, the United Kingdom, and the United States), all underperform with LQs of 0.80 or lower.

Figure 27: Relative performance in machinery and equipment (2022 LQ)

Figure 28: Net change in relative performance in machinery and equipment (LQ difference, 2013–2022)

Basic Metals

The basic metals industry comprises metals commonly used in industrial production, including copper, aluminum, and iron. The sector is strategically important because of its applications across several downstream power industries.

Globally, this industry grew by 253 percent between 1995 and 2022, faster than global GDP, which grew by 229 percent. Total value-added output in this industry reached $1.2 billion globally. China and other non-OECD nations have become the leading producers of basic metals, controlling 66 percent of the global market share; meanwhile, the market share of OECD nations fell by 44 percentage points over this period, from 78 percent to 34 percent.

Individually, China leads the world in basic metal production by a wide margin, holding 42 percent of the global market share, up from 6.5 percent in 1995. Other leading producers are the United States (10 percent), Japan (7.5 percent), India (5.6 percent), Russia (4.7 percent), and South Korea (3 percent). Lagging nations in this industry largely include developed nations that are concentrated in more high-tech industries, such as Denmark, Israel, Singapore, and Switzerland.

China and other non-OECD nations have become the leading producers of basic metals, controlling 66 percent of the global market share.

China’s growth in this industry, driven by its push for domestic industrialization and increased manufacturing output following its WTO accession, has come at the expense of almost every other nation. U.S. market share in this industry declined by 7.9 percentage points, while Japan (17.2 percentage points), Germany (4.9 percentage points), Italy (2.5 percentage points), and France (1.8 percentage points) also experienced declines. India and Russia each saw their global market share increase by about 2.5 percentage points.

Figure 29: Top 10 producers’ historical shares of global output in basic metals, 1995–2022

When it comes to industrial specialization, the trends are quite similar. China leads the world with an LQ of 2.31, once again reflecting its absolute leadership in the industry, followed by Russia (LQ of 2.08), South Korea (1.84), Japan (1.79), and India (1.71). Once again, developed nations tend to underperform in this industry, with Spain, Norway, France, the United States, and Australia among a slew of countries with an LQ of 0.50 or below. However, Nigeria has the lowest LQ of 0.07.

Over the decade from 2013 to 2022, Brazil experienced the greatest increase in LQ, with it increasing by 50 percentage points, more than double the next-most-improved nation of Russia (37 percentage points). Very few other nations saw their LQ increase over this decade, with Norway (14 percentage points), Italy (12 percentage points), Canada (7 percentage points), and Spain (6 percentage points) among the select few.

Despite its leading LQ, China actually exhibited one of the largest declines in relative performance, with its LQ falling 19 percentage points. In fact, China’s LQ fell 110 percentage points between 2002 and 2022, as the growth of China’s economy still outpaced its basic metals industry. South Korea, India, and Taiwan also overperform in this industry but have seen their LQ fall over the past 10 years.

Unsurprisingly, with so many OECD nations underperforming, the OECD collectively underperforms with an LQ of 0.57, having declined by nearly 40 percentage points since 1995. Conversely, non-OECD nations perform far above average, with an LQ of 1.62. The EU has also seen a substantial decline in relative performance, with its LQ declining from 0.84 in 1995 to 0.52 in 2022.

Figure 30: Relative performance in basic metals (2022 LQ)

Figure 31: Net change in relative performance in basic metals (LQ difference, 2013–2022)

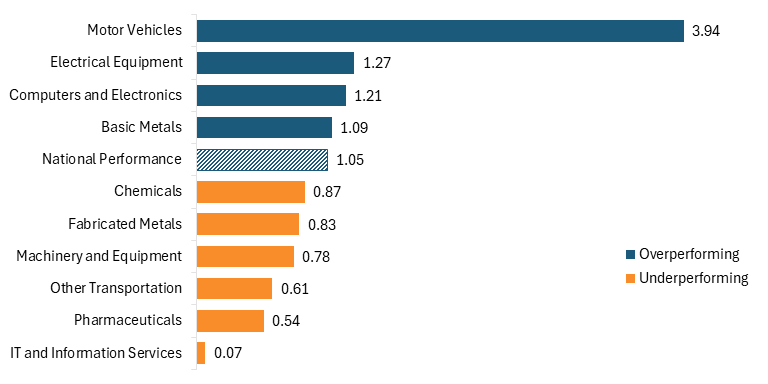

Motor Vehicles

The motor vehicle industry includes car and truck assemblers and suppliers, as well as motor vehicle parts manufacturing. It has become a more innovative sector due to new developments in electric vehicles (EVs), self-driving cars, and software-defined vehicles.

The sector grew more slowly than the nominal global GDP between 1995 and 2022, with value-added output increasing by 161 percent to $1.2 trillion, while global GDP grew by 229 percent. The industry is highly concentrated among a few key car manufacturing nations, including China (25.2 percent), Germany (14.4 percent), the United States (13.8 percent), and Japan (8.7 percent). The latter three nations are home to the largest and most well-known car brands, including Ford and General Motors in the United States, Nissan and Honda in Japan, and BMW and Volkswagen in Germany. China, on the other hand, has become well known in recent years for its collection of EV companies that have come to dominate the global EV industry, including industry giant BYD. It is the growth of China’s EV industry, spurred largely by generous subsidies from federal and local governments, that has propelled China to the lead in global market share.

Mexico, which holds 5.6 percent of global market share, ranks fifth. It has seen its global market share triple over this period, despite having no domestic car manufacturing companies; rather, it is a key offshoring location for American brands.

Figure 32: Top 10 producers’ historical shares of global output in the motor vehicles industry, 1995–2022

China’s global market share has increased by 22.5 percentage points since 1995, with the largest jump occurring in 2009, when the Chinese government began heavily subsidizing its EV industry.[7] Over the same period, Japan’s market share declined by 15.2 percentage points, the United States’ market share by 8.9 percentage points, and Germany’s market share by 1.3 percentage points. South Korea’s market share increased by 1 percentage point, while India’s, which has become one of the largest car manufacturers by unit in the world, increased by 3 percentage points. The OECD, which held over 88 percent of the global market share in 1995, has seen its share fall to just 60 percent in response to the growth of China and India.

China’s booming EV industry, which has received substantial subsidies from federal and local governments, has propelled it to the lead in global market share. It controls over 25 percent of the global market share.

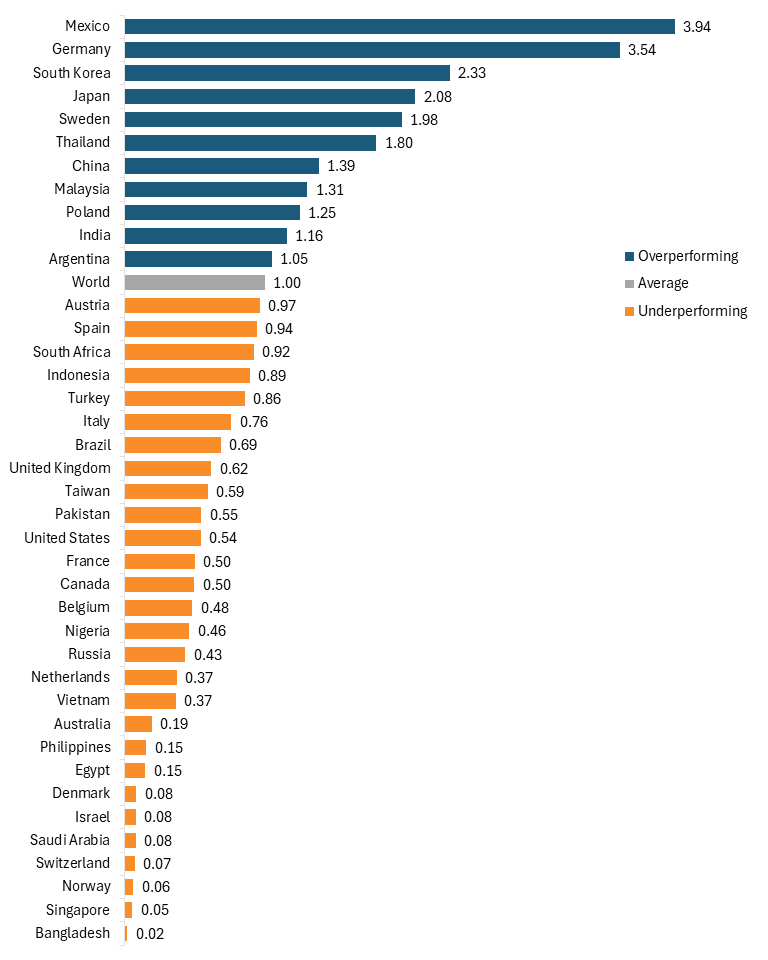

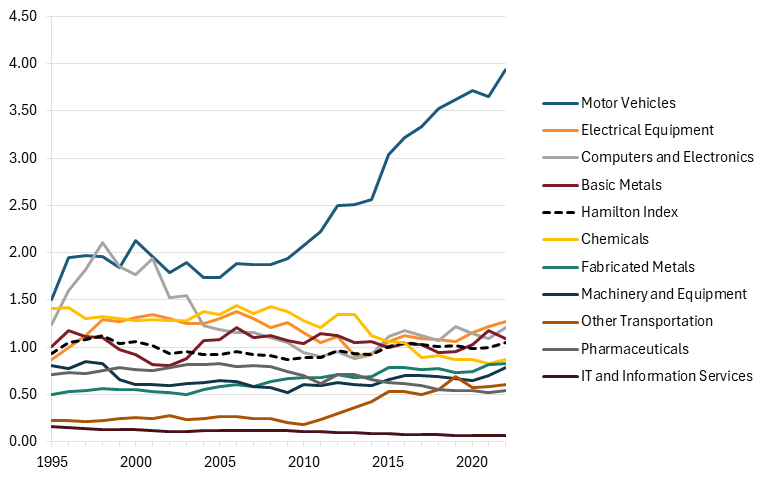

When it comes to relative performance, Mexico is the leader by a good margin with an LQ of 3.94, meaning Mexico’s output of motor vehicles is 294 percent more than would be expected based on the size of its economy. Other nations with high industrial specializations include Germany (3.54), South Korea (2.33), Japan (2.08), and Sweden (1.98), which is home to Volvo. China overperforms in industrial specialization, with an LQ of 1.39, while the United States’ LQ of 0.54 highlights its weakness in this industry.

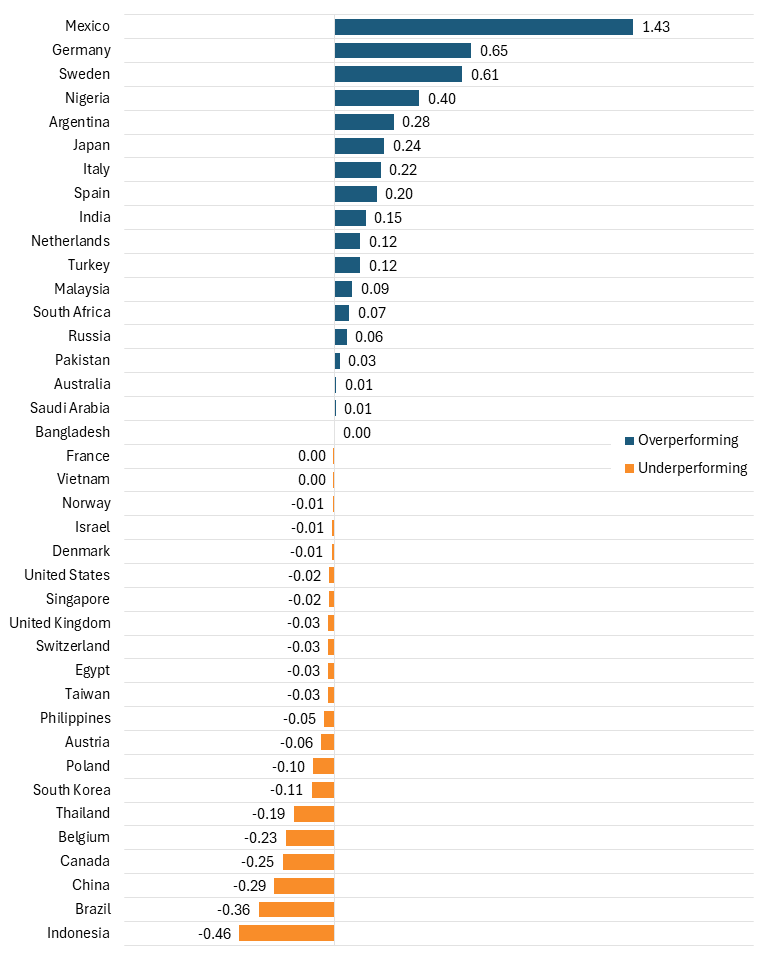

Mexico’s LQ increased the most (143 percentage points) over the previous decade due to the growing practice of offshoring American automobile production to Mexico, where labor and capital costs are lower. Germany (65 percentage points), Sweden (61 percentage points), Nigeria (40 percentage points), and Argentina (28 percentage points) experienced the next greatest increases in industrial specialization. The United States’ LQ declined by 2 percentage points over this period; however, comparing the U.S.’s 1995 LQ to 2022, the United States’ relative performance fell by nearly 40 percentage points, demonstrating the trough the U.S. auto industry found itself in during and after the Great Recession. Conversely, China’s LQ declined by 29 points from 2013 to 2022, but increased by 38 percentage points from 1995 to 2022.

Geopolitically, the OECD overperforms in motor vehicle production, with an LQ of 1.02, up 2 percentage points since 2002. The EU-10 (the 10 nations that joined after 2004) is highly specialized in this industry with an LQ of 1.91, while the broader EU-27 has an LQ of 1.53.

Figure 33: Relative performance in motor vehicles (2022 LQ)

Figure 34: Net change in relative performance in motor vehicles (LQ difference, 2013–2022)

Fabricated Metals

The fabricated metals sector includes the manufacturing of metal parts. It’s a strategically important industry, as its products often act as intermediate goods for manufacturers in other advanced and national power industries.

Internationally, this industry grew by 159 percent between 1995 and 2022, slower than global GDP, which grew by 229 percent. In 2022, value-added output in this industry exceeded $1 trillion. China shot to the top of this industry ahead of the United States in 2016 and now holds 26.7 percent of global market share. Conversely, the United States held 17.7 percent of the global market share in 2022, a marked decline from 1995, when the U.S. market share was 25.1 percent. The OECD’s share of this industry has also declined considerably, with its global market share falling from 87.9 percent in 1995 to 52.6 percent in 2022.

Behind China and the United States are Germany, with 6.1 percent of the global market; Italy, with 4.2 percent; Indonesia, with 4 percent; and Japan, with 4 percent. Several developed nations lag behind in this industry, with the Netherlands, Austria, Sweden, Israel, and Belgium among those each controlling less than 1 percent of global market share.

Many nations in the top 10 lost market share over the 27-year period, with Germany’s market share falling by 5.4 percentage points, Italy’s by 1.4 percentage points, Japan’s by 13.8 percentage points, and France’s by 3.3 percentage points.

Figure 35: Top 10 producers’ historical shares of global output in fabricated metals, 1995–2022

With several OECD countries in the top 10, it’s unsurprising that the OECD still holds the majority of global market share. However, this share has fallen substantially, from 87.9 percent to 56.2 percent. Conversely, the Belt and Road Initiative saw its global market share increase from 16.8 percent in 1995 to just over 50 percent in 2022, a threefold increase. While much of this growth was driven by China, whose market share increased from 2 percent to nearly 27 percent, Indonesia, Russia, and Poland saw their market shares rise by 3 percentage points, 1.4 percentage points, and 1.2 percentage points, respectively.

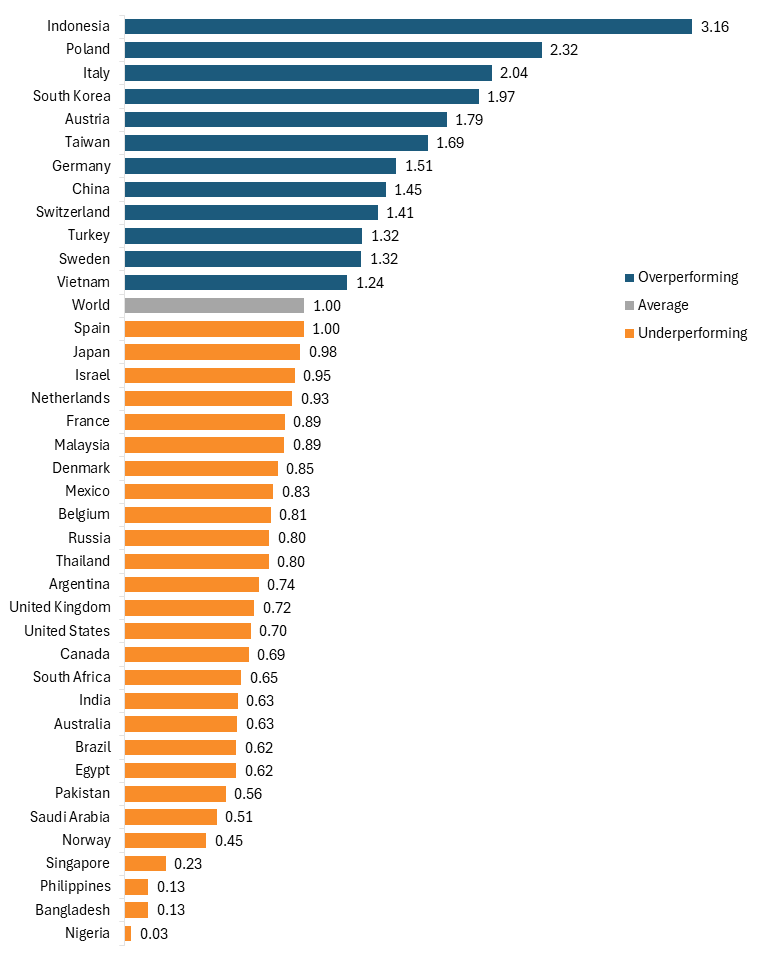

The picture looks quite different when considering industrial specialization. Indonesia leads the world with an LQ of 3.16, meaning its output of fabricated metals is 216 percent above what would be expected based on its economy’s size. Behind Indonesia are Poland (2.32), Italy (2.04), South Korea (1.97), Austria (1.79), and Taiwan (1.69). China also overperforms in this industry with an LQ of 1.45, while the United States and most European nations underperform. Lagging nations include Singapore, the Philippines, Bangladesh, and Nigeria, all of which have an LQ below 0.25.

Since 2013, Indonesia has experienced the greatest increase in LQ, increasing from 2.17 in 2013 to 3.16 in 2022, a 99 percentage-point increase. Other countries with a large boost to their LQ include Poland (65 points), China (28 points), Italy (26 points), and Russia (25 points). The U.S. LQ declined over this period, falling 16 percentage points.

Looking at industrial specialization from a geopolitical perspective, the EU-10 highly overperforms, with an LQ of 2.11, up 29 points over the previous decade. The broader EU-27 also overperforms, but to a lesser extent, with an LQ of 1.37, down 6 percentage points over the same period. The OECD, dragged down by the United States’ low LQ, underperforms with an LQ of 0.95.

Figure 36: Relative performance in fabricated metals (2022 LQ)

Figure 37: Net change in relative performance in fabricated metals (LQ difference, 2013–2022)

Pharmaceuticals

The pharmaceutical industry includes medicinal chemicals and botanical products. It is a strategically important sector given that much of it is high wage, traded across borders, and a key driver of innovation.

The output of the pharmaceutical industry increased by 312 percent from 1995 to 2022, more than global GDP, which increased by 229 percent over the same period. In 2022, pharmaceutical output was $872 billion. The OECD nations have lost market share, from 84 percent in 1995 to 71 percent in 2022; however, this decline was much more moderate than is apparent in other industries.

The United States is the leader in global market share, led by world-leading companies such as Amgen, Moderna, Pfizer, and Eli Lilly. In 2022, U.S. global market share was 28.6 percent, a moderate increase from 1995, when it was 26.5 percent, although down from a high of 34 percent reached in 2002. China is in second place, holding 17.3 percent of global market share, followed by Switzerland (4.5 percent), Germany (3.5 percent), Japan (3.1 percent), and India (2.5 percent). Lagging nations are nearly all developing countries, such as South Africa, Saudi Arabia, the Philippines, and Malaysia, which all have less than 1 percent of the global market.

Figure 38: Top 10 producers’ historical shares of global output in pharmaceuticals, 1995–2022

China has experienced the most dramatic rise in market share in pharmaceuticals, increasing by 14.6 percentage points. This massive increase has been catalyzed by China’s concerted effort to become the world leader in pharmaceutical production. In 2025, China conducted about 1,000 more clinical trials for pharmaceuticals than did the United States, demonstrating its increase in not just pharmaceutical manufacturing but also pharmaceutical innovation.[8] Switzerland also increased its global market share in this industry by 1.2 percentage points, while Germany lost 3 percentage points in market share and Japan experienced the greatest decline, seeing its share fall by 15.1 percentage points.

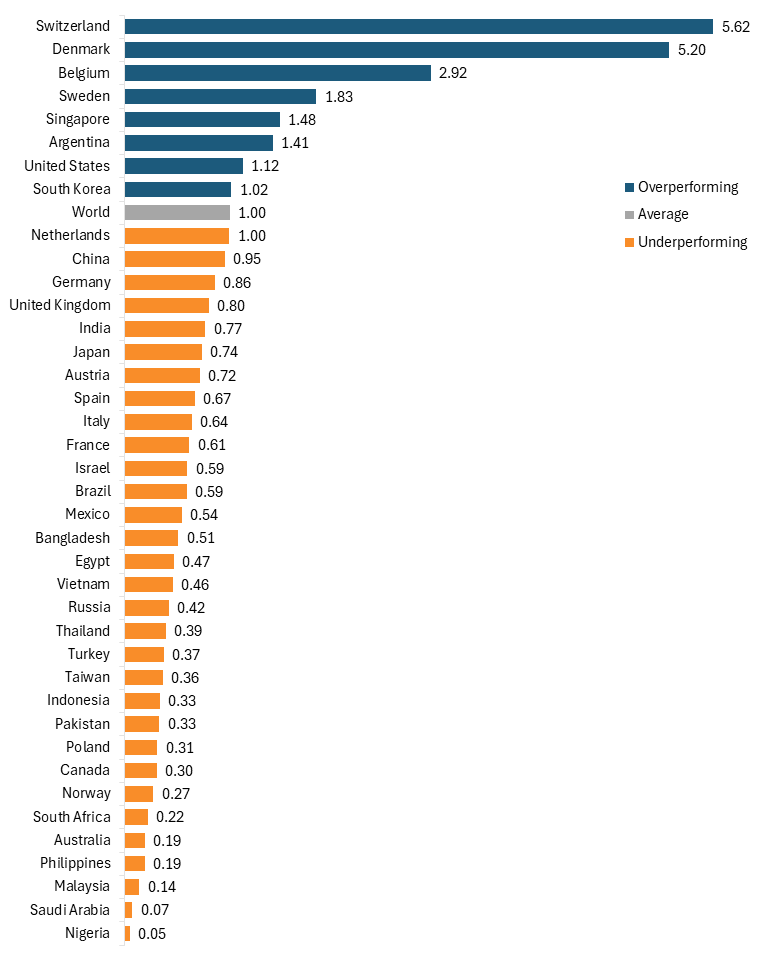

In terms of industrial specialization, the story is different. Switzerland led the world in 2022 with an LQ of 5.62, followed by European nations Denmark (5.20), Belgium (2.92), and Sweden (1.83). Argentina, the United States, and South Korea also overperform with LQs above 1. Notably, the OECD overperforms in this industry with an LQ of 1.20, while non-OECD nations underperform collectively, with an LQ of 0.71. Many of the lagging countries are developing nations, such as the Philippines, Malaysia, Saudi Arabia, and Nigeria, all of which had LQs below 0.2. China had an LQ of 0.95, which, while close to the world average, was still underperforming.

China experienced the most dramatic increase in pharmaceutical market share, rising by 14.6 percentage points. This massive increase has been catalyzed by China’s concerted effort to become the world leader in pharmaceutical production.

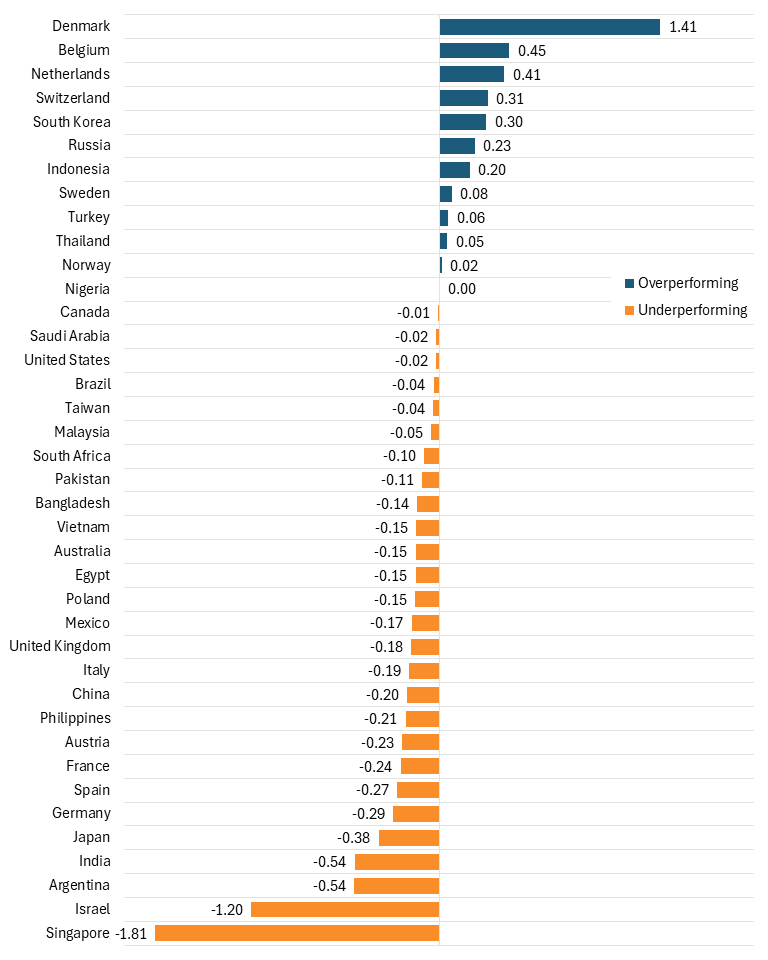

Looking at the change in industrial specialization, Denmark saw the largest increase in LQ since 2013, rising by 141 percentage points. This is more than triple that of the second-fastest grower, Belgium, which saw its LQ grow by 45 percentage points. By contrast, Singapore saw the largest decline in LQ, falling by 181 percentage points, with the steepest declines occurring between 2018 and 2022. Other nations that saw large declines were India (54 percentage points), Argentina (54 percentage points), and Israel (120 percentage points).

The OECD’s LQ increased by 10 percentage points over this same period, unsurprisingly given the growth of several OECD nations. Conversely, the LQ of the Commonwealth Nations of Australia, Canada, New Zealand, and the United Kingdom fell by 12 points, largely driven by the large decline in the United Kingdom. Despite several highly specialized countries, the EU also saw its LQ decline, falling by 12 percentage points over the previous decade.

Figure 39: Relative performance in pharmaceuticals (2022 LQ)

Figure 40: Net change in relative performance in pharmaceuticals (LQ difference, 2013–2022)

Electrical Equipment

The electrical equipment industry includes an array of electrical products, including batteries, electrical cables, relays, switchgears, and household appliances.

Globally, this sector has grown more slowly than GDP, rising 142 percent in nominal U.S. dollars since 1995, compared with 229 percent over the same period. Still, the sector was valued at $680 billion dollars in 2022. The OECD, which was once the overwhelming leader in this industry and held over 89 percent of the global market share, has seen its dominance decline over the 27-year period. In 2022, the OECD controlled just 46.9 percent of the global market share.

China is the leader in the industry in terms of market share, controlling 38.5 percent. The next closest country to China is the United States, which held only 11.3 percent of the market share in 2022. Japan (8 percent), Germany (7.4 percent), South Korea (4.4 percent), and India (2.5 percent) are also leaders in the industry; however, their market influence pales in comparison with China. The EU-27 (excluding Ireland), which once held nearly 30 percent of the global market share, has seen its share fall to 18 percent.

China has been the leader in this industry since 2007, when it passed Japan to become the largest producer of electrical equipment. Over the period from 1995 to 2022, China’s global market share increased from 3.7 percent to 38.5 percent, a total of 34.8 percentage points. Meanwhile, Japan suffered the greatest loss in market share, falling 26 percentage points from the world leader to third place. Though not as dramatic, the German and U.S. market shares also fell by 7.5 and 5.1 percentage points, respectively.

Figure 41: Top 10 producers’ historical shares of global output in the electrical equipment industry, 1995–2022

Although not an absolute frontrunner in the industry, South Korea leads in the industrial specialization of electrical equipment, with an LQ of 2.68. Other high relative performers include Vietnam (2.19), China (2.11), Japan (1.93), and Austria (1.93). The United States significantly underperforms in this industry, with an LQ of just 0.45 in 2022, while most lagging nations are developed, less industrialized countries such as Norway (0.23), Singapore (0.22), and Australia (0.20). Nigeria has almost no electrical equipment manufacturing activity.

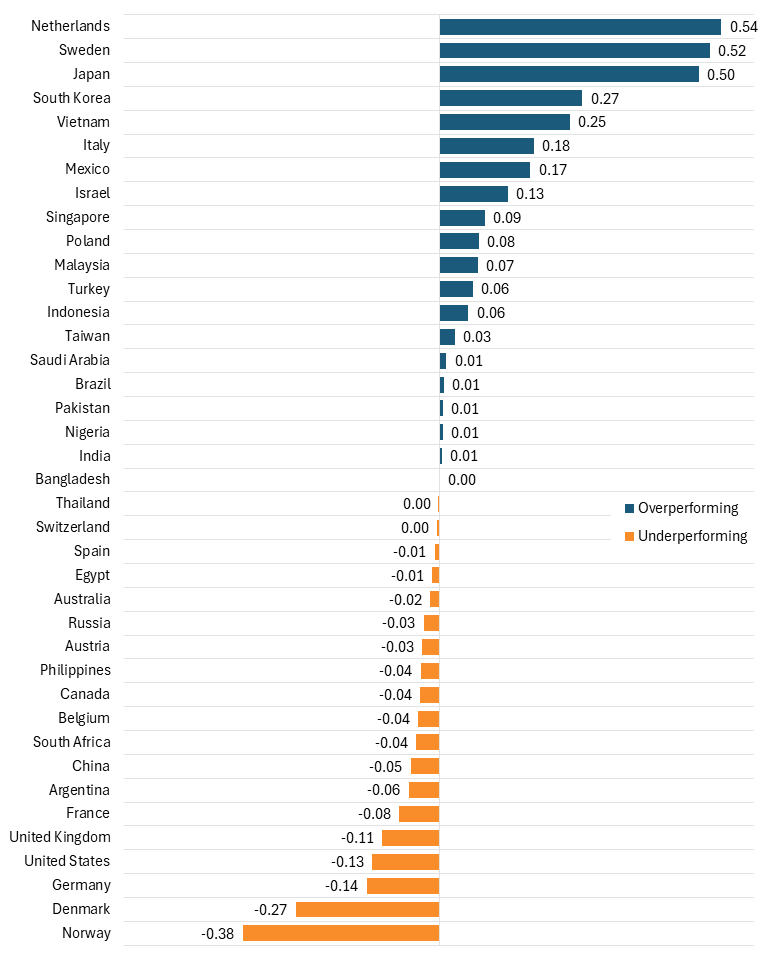

Vietnam experienced the greatest increase in relative performance, increasing by 109 percentage points since 2013. The other nations with the fastest percentage point growth in their LQs over this period were Poland (77 percentage points), Malaysia (37 percentage points), and Mexico (36 percentage points). In aggregate, OECD nations saw a 7 percentage-point decline in their LQs. Among the nations whose LQs declined are Belgium (22 percentage points), Germany (26 percentage points), China (32 percentage points), Switzerland (36 percentage points), and Austria (42 percentage points).

Geopolitically, the EU-10 saw the greatest increase in industrial specialization, with its LQ increasing by 45 points from 1.33 to 1.78. Conversely, the EU-17, which comprises countries with relatively more jobs in the knowledge economy than in manufacturing, saw its LQ fall by 7 points, from 0.92 to 0.85.

Figure 42: Relative performance in electrical equipment (2022 LQ)

Figure 43: Net change in relative performance in electrical equipment (LQ difference, 2013–2022)

Other Transportation Equipment

The other transportation sector includes all rail, air, and sea transportation equipment.

Between 1995 and 2022, the global other transportation industry’s output increased by 183 percent, reaching $423 billion. However, this growth was slower than the global GDP, which grew by 229 percent. The OECD controlled the vast majority of the global market share in this industry, holding nearly 71 percent.

Other transportation is one of the few industries wherein the United States holds a clear majority over China. Largely due to its dominance in the aviation industry, led by defense and commercial manufacturers such as Boeing, Lockheed Martin, and Pratt & Whitney, the United States controls 37.6 percent of the global market share, more than twice China’s 14.2 percent. Other leading nations are France (5.1 percent), Germany (4.4 percent), and Russia (4.3 percent). Japan, which was once second in the world behind the United States, controlled 3.1 percent of global market share, down from 16 percent in 1995.

Though China controls a much smaller share of the global market than the United States, its power in this industry is evident. China’s market share has increased from 1.8 percent in 1995 to 14.2 percent, driven by its expansion in high-speed rail and shipping, and its recent push to become a leader in the aerospace industry through its national firm, COMAC. U.S. market share in this industry has increased by 3.6 percentage points since 1995, though it remains far below its peak of 43.7 percent in 2001.

Figure 44: Top 10 producers’ historical shares of global output in other transportation equipment, 1995–2022

As a group, the OECD’s market share has fallen by nearly 16 points since 1995, from 86.2 percent to 70.2 percent, while the Quad’s market share also has declined by over 8 percentage points. In contrast, the Belt and Road Initiative has gained 12 percentage points, a significant share.

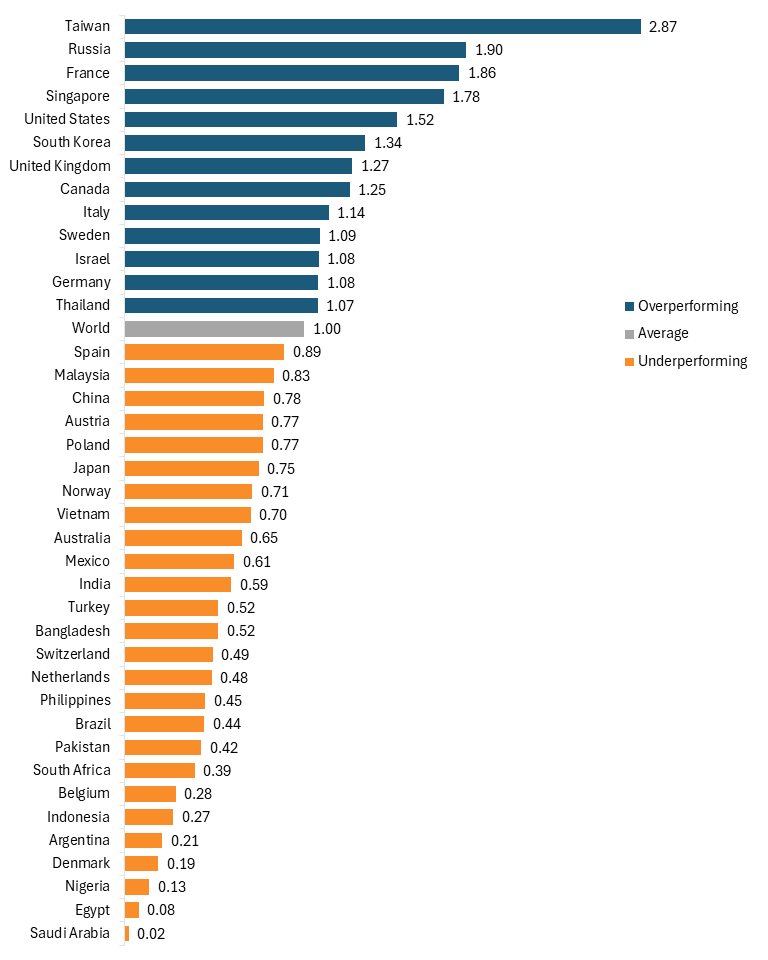

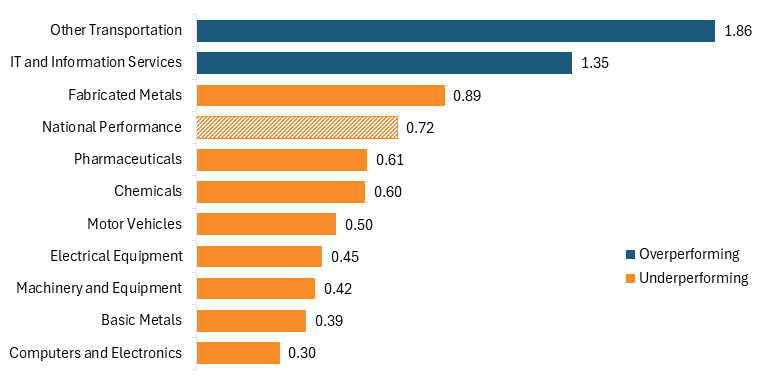

The story is much different when it comes to industrial specialization. Taiwan leads the world with the highest LQ of 2.87, followed by Russia (1.90), France (1.86), Singapore (1.78), and the United States (1.52). While China underperforms with an LQ of 0.78, that is still an increase from 1995, when its LQ was just 0.62. Additionally, given China’s continued dominance across the three other transportation industries, China’s LQ is likely to continue increasing in the coming years.

Led by defense and commercial manufacturers such as Boeing, Lockheed Martin, and Pratt & Whitney, the United States controls 37.6 percent of the global market share in other transportation, more than twice China’s 14.2 percent.

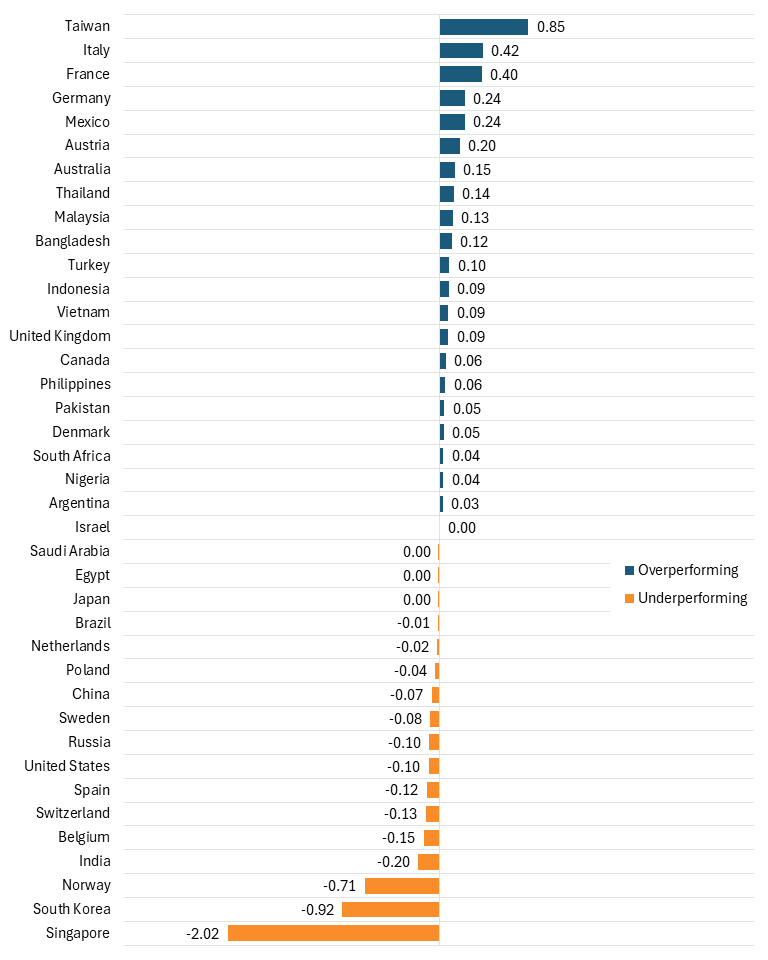

Taiwan is also the nation that has experienced the greatest increase in industrial specialization, with its LQ rising by 85 percentage points since 2013. Following Taiwan is Italy (an increase of 42 percentage points), France (40 percentage points), Germany (24 percentage points), and Mexico (24 percentage points). The U.S. LQ has declined moderately over this period, falling by 10 percentage points.

Looking at the industry from a geopolitical perspective, USMCA nations perform well with an LQ of 1.44, driven by the overperformance of the United States and Canada. The Quad also overperforms with an LQ of 1.29. The EU, while not the best-performing relative to other geopolitical groups, has seen the greatest growth, with its LQ rising by 16 percentage points since 2013.

Figure 45: Relative performance in other transportation equipment (2022 LQ)

Figure 46: Net change in relative performance in other transportation equipment (LQ difference, 2013–2022)

Top 10 Producer Profiles

This section assesses the top 10 nations in terms of aggregate advanced industry output in 2022, in order of output.

Data Visualizations for All Countries and Regional Groupings

Use the accompanying data visualization tool to browse the complete dataset for every country and regional grouping in this report: “The Hamilton Index, 2026: Data Visualization for Countries.”

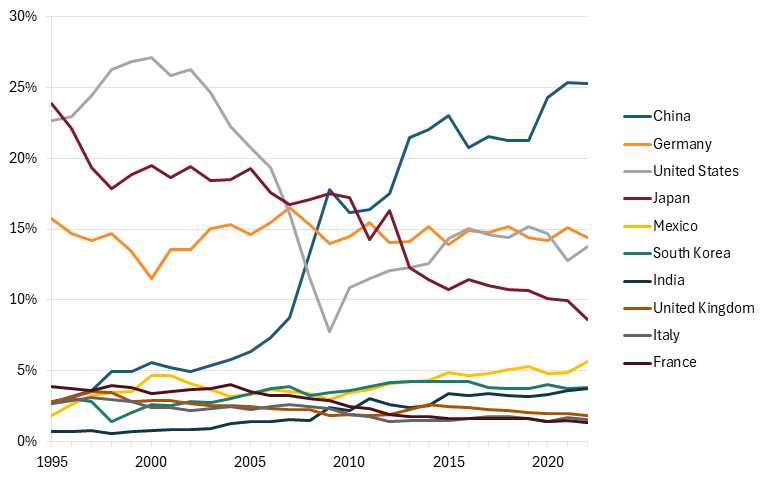

China

China has been seeking to become the global leader in advanced industries for over two decades and is close to that goal. In 2013, China overtook the United States as the leader in advanced industry output and has continued to increase its lead. As of 2022, Hamilton Index industries accounted for 15.8 percent of China’s economy, over 4 percentage points more than the world average. (See figure 47.)

Figure 47: Hamilton industries’ shares of China’s economy, 1995–2022

China’s leadership is further evident when considering global market share. Since 1995, China’s advanced industry output has skyrocketed, with every industry undergoing intense growth. Even its smallest industry, IT and information services, has nearly quintupled in size, with China’s market share rising from 2.1 percent to 9.3 percent, making it second in the world. China is either the first- or second-most powerful country in every advanced industry by market share, and in almost every industry, its market share looks on track to continue increasing. (See figure 48.)

Figure 48: China’s global market shares in Hamilton industries, 1995–2022

Looking at relative performance, China overperforms in 7 of the 10 Hamilton Industries, with just pharmaceuticals, other transportation, and IT and information services having LQs below one. However, it’s not unreasonable to assume that these industries (at the very least, pharmaceuticals and other transportation) will be overperforming in the next few years. China’s pharmaceutical industry has grown from a manufacturer to an innovator over the past several years and has shown signs of closing the gap with the United States.[9] Additionally, its other transportation industry is likely to be buoyed by growing federal support and, consequently, by the growth of its state-sponsored aviation firm, COMAC.[10]

China is either the first- or second-most powerful country in every advanced industry by market share, and in almost every industry, its market share looks on track to continue increasing.

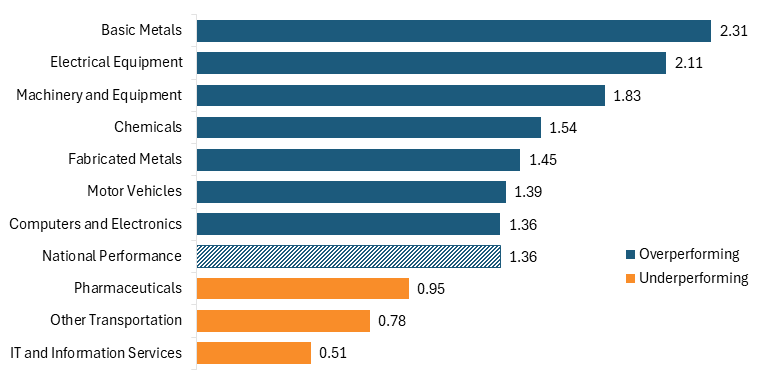

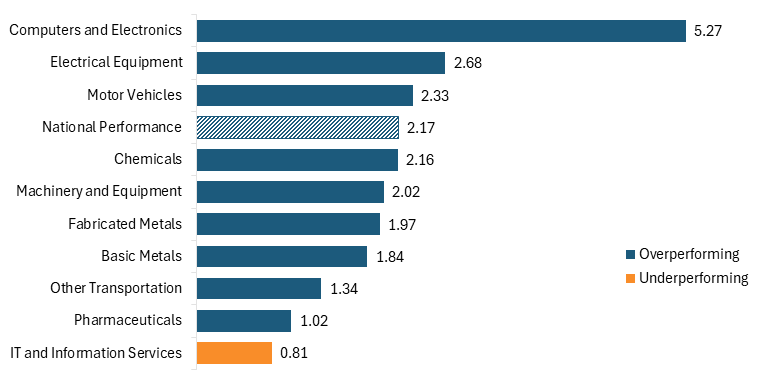

China’s strongest industry is basic metals (LQ of 2.31), including steel production, an industry the Chinese government has subsidized at roughly five times the rate of comparable economies.[11] China has also shown its prowess in other heavy manufacturing industries, including electrical equipment, which includes home appliances, many of which the U.S. government has placed tariffs on since 2018, and machinery and equipment.[12] (See figure 49.)

Figure 49: China’s relative performance in Hamilton Index industries (2022 LQ)

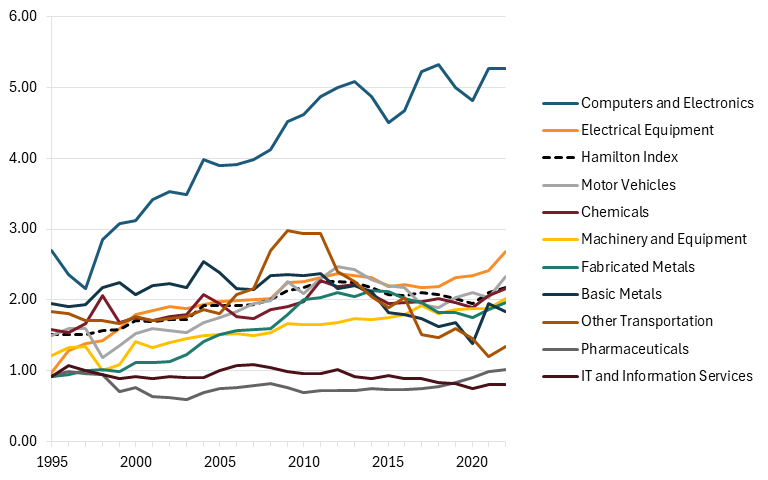

The trends of China’s advanced industries LQs loosely follow an upside-down-U shape, with many peaking around the global financial crisis in 2008 and then declining in the years since. As previously stated, the recent decline in China’s LQs is not a sign that China’s advanced industry output is declining, but rather reflects the fact that its advanced industries are growing more slowly than the overall economy. As evidenced by its across-the-board increase in global market share over the past decade, China’s advanced industries are growing at a rapid pace. However, its economy has grown faster, nearly quadrupling since 2008. So although China has become less specialized in advanced industries since the mid 2000s, it is no less of a dominant leader in advanced industries. Additionally, when considering China’s LQ trend since 1995, China’s LQ has increased significantly, by 12 percentage points, more than the United States or the OECD.

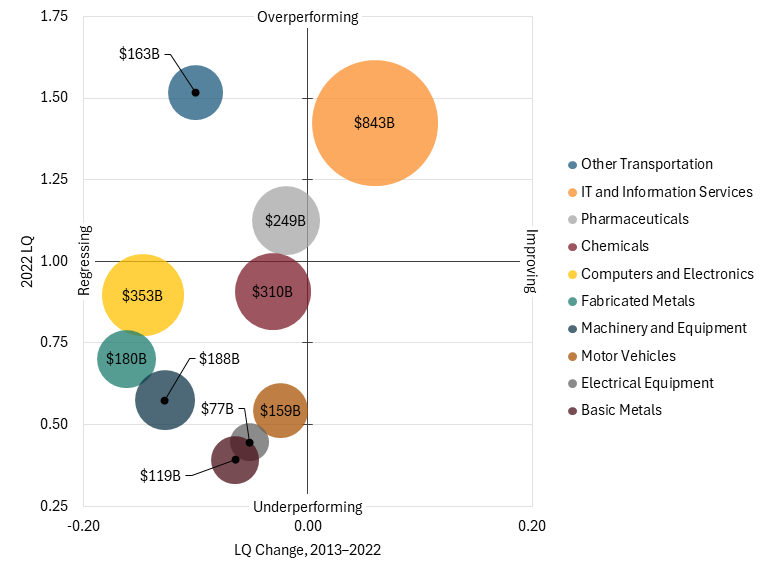

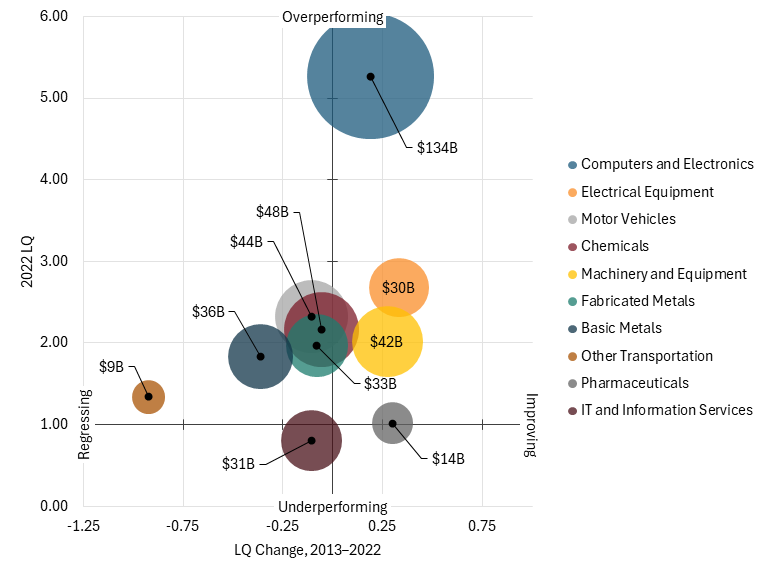

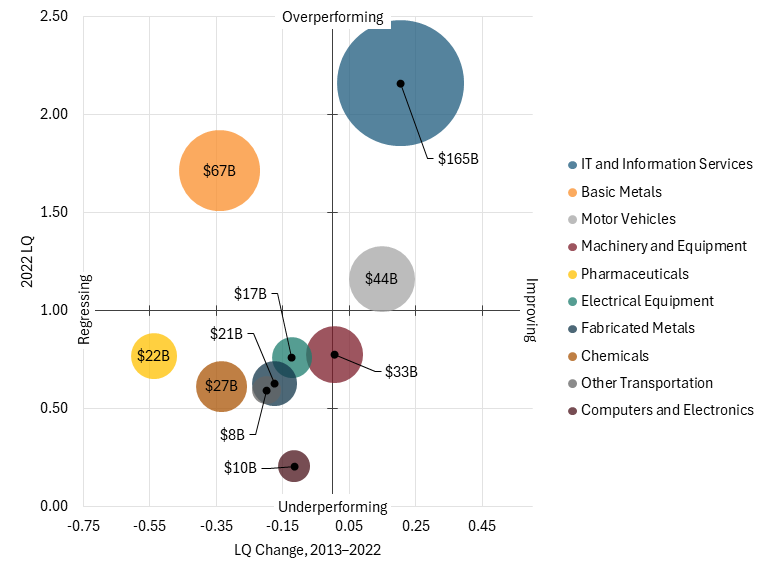

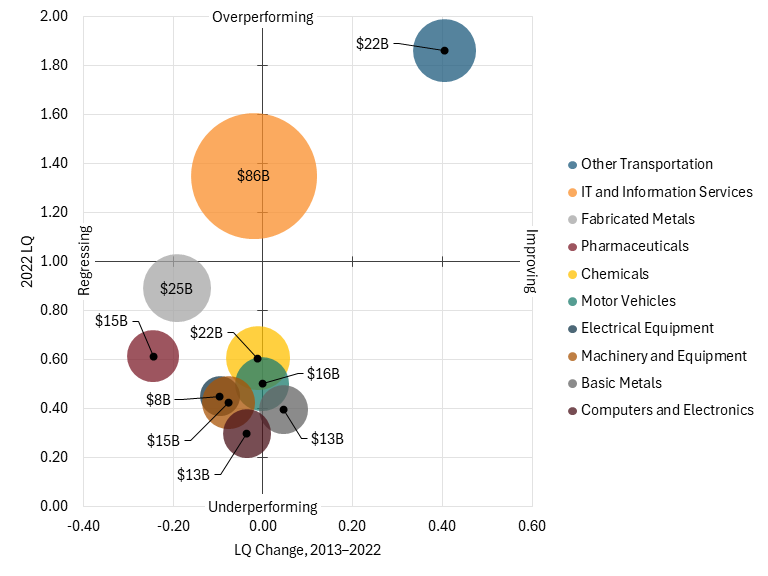

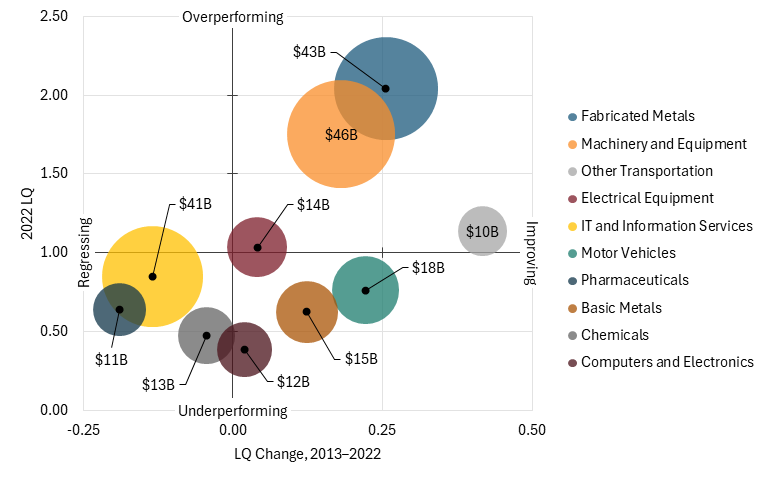

Figure 51 shows the net improvement or regression in the relative performance of China’s Hamilton industries since 2013, scaled to their output in 2022. In this figure, each industry can be assessed by its LQ, change in LQ since 2013, and size, measured by output in 2022. Industries in the upper left quadrant are overperforming, but their LQs have regressed; this quadrant houses the majority of China’s industries, including its biggest industries: basic metals and machinery and equipment. Industries in the upper right quadrant are overperforming and their LQs have increased; only fabricated metals falls into this category. The bottom right quadrant shows industries that are underperforming and improving; no industry is located in this quadrant. And the bottom left shows industries that are underperforming and regressing; this includes China’s pharmaceuticals and other transportation industries, although, as stated previously, these industries are likely to overperform in the next several years.

It’s important to note that, although surprising that the Made in China 2025 plan and previous five-year development plans have not led to an increase in relative performance over the past several years, overall, China’s LQ has still increased since 1995. And what’s more, given China’s LQ of 1.36, China’s output in advanced industries is 36 percent more than what is expected based on the size of its economy.

Figure 50: China’s relative historical performance in Hamilton Index industries (LQ trends, 1995–2022)

Figure 51: China’s net performance in Hamilton industries since 2013 (scaled to 2022 output)

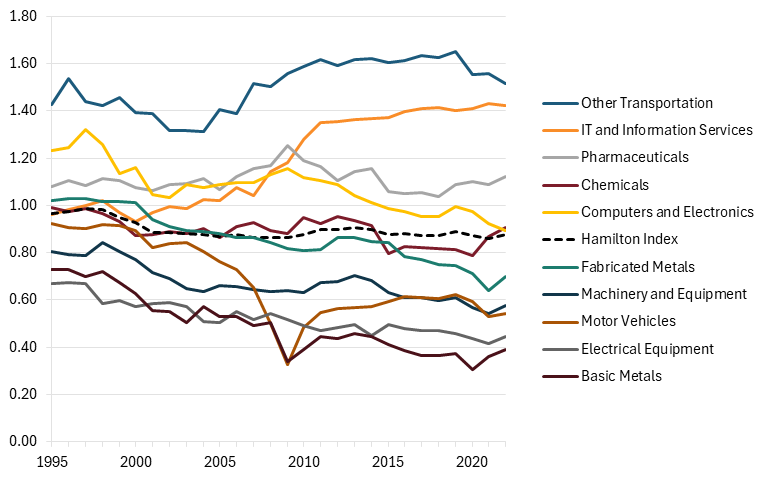

United States

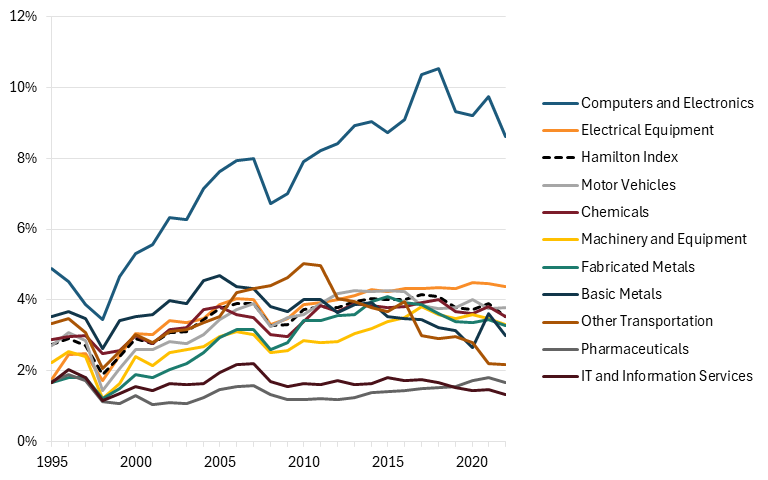

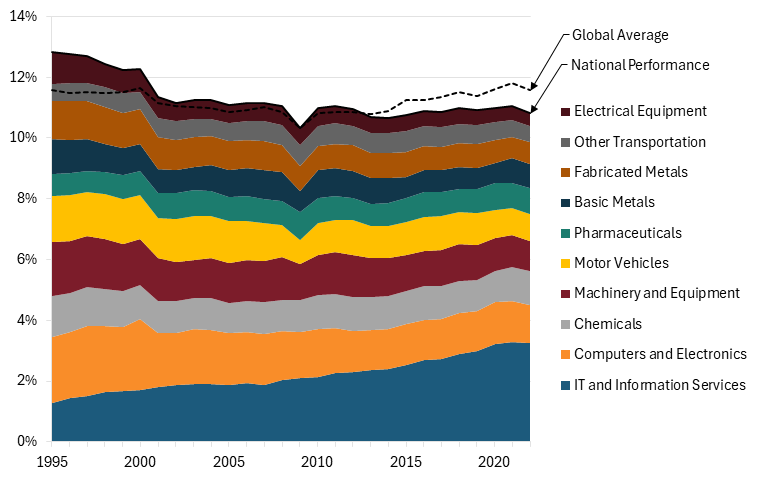

The United States is no longer the world leader it once was. A lack of industrial policy and a shift from a producer to a services-based economy have left the United States weak in advanced industries. The industries in the Hamilton Index together accounted for 10.2 percent of the U.S. economy in 2022, less than the global average of 11.6 percent and a 9 percent decline from 1995, when Hamilton industries accounted for 11.2 percent of the U.S. economy. (See figure 52.) Although Hamilton Industries’ share of the U.S. economy has been on a steady rise since 2009, almost all of that increase can be attributed to the IT and information services sector, the industry in which the United States is most dominant. Excluding this share, Hamilton industry output as a share of the U.S. economy fell from 7 percent in 2009 to 6.9 percent in 2022.

Figure 52: Hamilton Index industries’ shares of the U.S. economy, 1995–2022

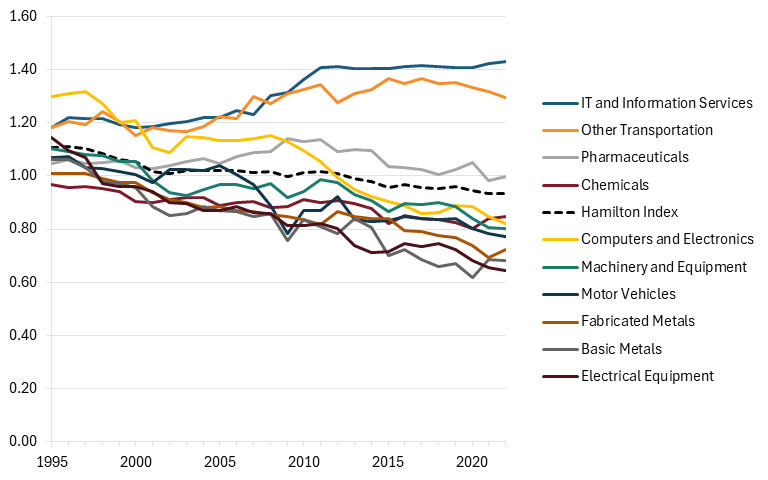

When it comes to global market share, the United States is a story of stagnation, if not decline. Seven of the 10 advanced industries experienced declines, ranging from 1 percentage point (chemicals) to 9 percentage points (motor vehicles). Only IT and information services experienced a marked rise in output and market share, with U.S. global market share in the industry growing nearly 13 percent since 1995.

Figure 53: America’s global market shares in Hamilton industries, 1995–2022

To illustrate the outsized impact IT and information services have on the U.S. advanced industry economy, see figure 54. In terms of overall global market share, U.S. output fell from a peak of 28.1 percent in 2000 to 22.3 percent in 2022. However, from 2011 to 2022, that share increased from a nadir of 18.8 percent, but almost all of that growth was driven by the IT services industry. When excluding this sector, U.S. global shares of advanced industries peaked in 2000 at 28.1 percent and then fell steadily, just as American firms began offshoring to China. Without IT, American global market share reached a low of 17.2 percent in 2011 and then rose slightly to 18.9 percent in 2022. Given this, it’s evident that the United States’ strength in IT services hides a real structural weakness in advanced manufacturing.