China’s Burgeoning Biopharmaceutical Competitiveness Demands a US Response

China has become an increasingly capable competitor in the global biopharmaceutical industry. To remain competitive, the United States should double down on policies to ensure that it offers the world’s leading environment to support private sector life sciences innovation.

KEY TAKEAWAYS

Key Takeaways

Contents

China’s Biopharmaceutical Ecosystem. 4

China’s Growing Biopharmaceutical Competitiveness 8

Introduction

China has set its sights on becoming the world’s leader in biopharmaceutical innovation. While such a goal might seem fanciful to some, the reality is China has set similar goals—and achieved them—in industries ranging from electric vehicles (EVs)/batteries and solar panels to nuclear power and telecommunications networking equipment.[1] In recent years, China has developed a comprehensive national strategy to strengthen its biopharmaceutical innovation capacity, which features a wide range of policy instruments, including subsidies, financial incentives, high-tech science parks, startup incubators, talent recruitment schemes, regulatory reforms to expedite drug review, enhanced intellectual property (IP) protections, and increased science funding. Overall, China’s government has explicitly prioritized science and biotechnology as engines of national power, identifying biotechnology as a leading technology of “new-quality productive forces.”[2]

China has set its sights on becoming the world’s leader in biopharmaceutical innovation.

China began to seriously target the biopharmaceutical sector as early as 2007, when the Chinese Communist Party (CCP) announced plans to “set up high-tech industrial bases for biotechnology.”[3] In 2011, as part of its 12th Five-Year Plan (2011–2015), China designated biotechnology as a “strategic emerging industry” and also introduced a coordinated national strategy to accelerate biotech innovation and competitiveness.[4] Under its 14th Five-Year Plan (2021–2025), China committed to increasing research and development (R&D) investment by more than 7 percent annually and set a goal of raising R&D’s share of China’s gross domestic product (GDP) to about 3 percent (a figure that currently stands at 2.8 percent).

In 2021 alone, China’s basic science research investment rose by 10.6 percent—part of a deliberate push to build long-term scientific capacity. That same year, Beijing also launched new national laboratories and innovation centers in strategic fields such as artificial intelligence (AI), biopharmaceuticals, and genomics.[5]

In 2022, China for the first time issued a five-year plan specifically for the bioeconomy, articulating broad goals for 2025 in biopharma, bio-agriculture, bio-manufacturing, and bio-security. This Bioeconomy Development Plan established biomedicine as a strategic pillar alongside agriculture and biomanufacturing, targeting a 10 percent annual growth rate in these industries through 2025.[6] Also in 2022, the National Natural Science Foundation of China (NSFC), the country’s largest public science funder, increased its investment to RMB 32.7 billion (about $4.5 billion), up from RMB 31.2 billion ($4.2 billion) the previous year, supporting over 51,000 research projects, with at least 34 percent of its budget invested in research in life science and healthcare.[7] By 2023, Chinese government R&D investment in science reached $110 billion—far exceeding the $65 billion invested by the U.S. government in intramural research.[8] In short, China is channeling massive public funds into biopharmaceutical innovation as it seeks to position itself as a global science leader by 2035—a trajectory that directly challenges U.S. leadership in the sector.

China is rapidly ascending across virtually all measures of biopharmaceutical competitiveness, and if such trends continue unabated, China could achieve its goal of wresting biopharmaceutical leadership from the United States within the coming decade.

These public sector investments have translated into significant growth. China’s biopharmaceutical industry’s market size has grown from an estimated RMB 1.21 trillion ($178.7 billion) in 2010 to RMB 2.97 trillion ($412.7 billion) in 2024.[9] Chinese institutions have also succeeded in attracting highly qualified biopharma talent, with about 30 percent of the world’s top academic talent in the sector working in Chinese universities and labs between 2019 and 2023. In comparison, the United States had 27 percent and Europe 12 percent of such researchers.[10] China is also producing more top-cited, high-impact biotechnology research publications than ever before, surpassing the United States. Moreover, China’s biopharma patents have surged by more than 300 percent over the past decade.

Chinese firms have also utilized process innovation and regulatory streamlining to excel in drug clinical trial testing. The time it takes to secure approval for human trials in China has shrunk from 501 days to just 87. Human trials themselves, usually the slowest stage in the development of a new drug, also move faster. A vast patient pool makes enrollment easier, and a large network of trial centers further speeds things along.[11] As a result, in 2025, Chinese companies conducted nearly one-third of global clinical trials for the most-innovative drugs, an increase of over sixfold from the 5 percent they had accounted for just a decade earlier.[12]

It’s true that, overall, China still trails the United States in many key measures of biopharmaceutical competitiveness. For instance, in 2024, China accounted for only 4.8 percent of the global biotech market, significantly less than for the United States (35 percent) or Europe (31 percent).[13] Moreover, China accounted for only 7.5 percent of global pharma sales in 2023, again far less than that of the United States and Europe, at 53 percent and 23 percent, respectively.[14] As of 2025, the United States still led China in global share of clinical trials for the most-innovative drugs, albeit only by 3 percentage points, 33 percent versus 30 percent. The same can be said for new drug development, wherein Chinese firms developed more than 1,250 new drugs in 2024, the second most in the world behind the United States, which developed 1,440.[15] Nevertheless, the trendlines are starkly clear: China is rapidly ascending across virtually all measures of biopharmaceutical competitiveness, and if such trends continue unabated, China could achieve its goal of wresting biopharmaceutical leadership from the United States within the coming decade.

In short, China’s rise in the global biopharmaceutical industry has been unprecedented in its speed and scale, threatening America’s global leadership in this critical sector. This report first examines the ecosystem assets that have helped enable China’s swift biopharmaceutical growth and then evaluates the extent of that growth by assessing key indicators including scientific publications and patents, R&D investments, global market shares and value-added output, clinical trial activity, drug development, and China’s innovativeness in key emerging fields of biopharmaceutical medicine. Lastly, the report concludes with a series of policy recommendations the United States could enact to help its biopharmaceutical industry better compete with the growing challenge from China.

China’s Biopharmaceutical Ecosystem

Since China began prioritizing the development of its biopharmaceutical industry in 2007, it has pursued a deliberate strategy to strengthen every major input into the sector: infrastructure, incentives, capital accumulation, R&D investments, and workforce development, among others. Some of the measures used to build this ecosystem—including regional cluster initiatives, tax incentives, and talent recruitment programs—are certainly legitimate and consistent with the global rules-based trading system. Other practices, however, raise significant concerns. Indeed, China has deployed a panoply of “innovation mercantilist” practices such as IP theft, industrial subsidization, and the sale of unregulated products, enabling Chinese firms to operate outside the constraints faced by competitors in market-based economies.

Legitimate Practices

Science Parks and Regional Clusters

The Chinese government has intensively supported biotechnology innovation through the construction of science parks, which provide infrastructure, laboratories, talent pools, and financial support. These science parks help reduce the high upfront costs of R&D facilities for start-ups. Locations include the Zhangjiang Hi-Tech Park in Shanghai, the Zhongguancun Life Science Park in Beijing, and BioBay in Suzhou.[16] Changping’s “Life Valley,” which includes Zhongguancun Life Science Park, hosts more than 900 pharmaceutical enterprises, 40 university research facilities, 100 annual conferences, and 4 unicorns (start-ups valued at over $1 billion).[17]

These biotech parks have received funding from both national and local governments. For example, Shanghai, the most advanced of China’s biotech clusters, has invested $15 billion in R&D and promised free leases on land and support for equipment purchases.[18] Between 2016 and 2020, the number of biotech science parks in China grew from about 400 to over 600, and the total value of their output grew more than 80 percent during that period.[19] In the 15th Five-Year Plan, released in March 2026, China declared its intention to continue deploying and building regional science and technology innovation hubs.[20]

The emergence of a new type of organization in the 1990s, known as the contract research organization (CRO), has also spurred the development of China’s biotech industry.[21] CROs provide a wide variety of research services to biotech companies. In recent years, these services have shifted from technology transfer and customized production to a more cooperative R&D model between companies and CROs.[22]

George Baeder, a biotech executive with 30 years of experience in China, has explained that, while early Chinese CROs were not very sophisticated, recently, high-quality, innovative, local CROs have emerged, with a wide range of capabilities, including running clinical trials.[23] These CROs have become instrumental as China has become an ideal locale for clinical trials thanks to the rapid speed and low costs that can be realized in China.

A study of 66 CROs finds that many of them are located among biotech companies in high-tech parks where they can leverage the parks’ infrastructure, incubators, R&D facilities, and government support. The agglomeration offered by high-tech parks, pooling scientific expertise, state-of-the-art technological facilities, biotech companies, incubators, and financial resources, supports the development of CROs, which in turn spurs biotech innovation.[24] Nowadays, CROs and contract development and manufacturing organizations provide services ranging from discovery biology and preclinical research through to biologics manufacturing at both clinical and commercial volumes.

Between 2016 and 2020, the number of biotech science parks in China grew from about 400 to roughly 600, and the total value of their output grew more than 80 percent during that period.

Additionally, China has seen the recent emergence of biotechnology clusters, which facilitate knowledge and resource sharing, playing a critical role in transforming scientific ideas from the laboratory into commercial products, such as novel therapeutics. According to a McKinsey Biocentury report, four leading biotechnology clusters have arisen in China: 1) the Bohai Rim Cluster, located in Beijing, Tianjin, and Jianin; 2) the Yangtze River Cluster, located in Shanghai, Suzhou, and Hangzhou; 3) the Mid-West Cluster, in Wuhan and Chengdu; and 4) the South China Cluster, located in Shenzhen, Guangzhou, and Xiamen. Over 8,500 biotech and biopharma companies are found in these leading Chinese biohubs.[25]

State-Backed Gene and Cell Banks

The Chinese government has also invested heavily in gene and cell banks, also known as “biobanks,” to bolster its domestic biopharmaceutical industry. Biobanks represent massive repositories of genes, cells, and other biomedical samples and data used in drug development—and they are critical in drug R&D, particularly for more complex diseases and therapeutic modalities, including personalized medicine, gene therapy, and cancer.[26]

The United States has long been a leader in biobanking, creating and maintaining some of the world’s largest repositories, including through the NIH’s All of Us research program. However, China has made rapid strides to close this gap. As it stands, China’s National Biobank, which was launched just a decade ago in 2016, is already one of the world’s largest biobanks, containing 10 million blood and cell samples from humans, animals, and other living organisms. Similarly, the National Genomics Data Center, based in Beijing, has doubled in size and integrated eight major databases over just two years. These banks also benefit from China’s large population of over 1.4 billion people, which helps these banks rapidly obtain large amounts of data.

Through its substantial investments in biobanking and data collection, China is laying the groundwork to accelerate drug discovery in the years to come, putting it in a better position to compete with the United States.[27]

Tax Incentives

Chinese biopharma firms have benefited from extensive tax incentive schemes designed to increase biopharmaceutical innovation and competitiveness. Firms in this industry qualify for “high- and new-technology enterprise” (HNTE) status, allowing them to access specific tax incentives. For example, HNTEs are eligible for a reduced corporate income tax rate of 15 percent, rather than the usual 25 percent.[28] HNTEs also qualify for extended tax-loss carry-forward consideration. Under this policy, biopharma firms can carry forward qualified losses for up to 10 years, double the amount for normal enterprises.[29] This is particularly beneficial to firms in the biopharma industry, as losses incurred during the clinical trial stage of drug development can often be extensive, and a great many biotech firms are pre-revenue.

Biopharma firms also qualify for China’s R&D super deduction, which allows for firms making qualified R&D expenditures to deduct 200 percent of the value from their taxable income.[30] These incentives amount to significant savings for firms. Hengrui, a leading Chinese pharmaceutical company, received approximately $5.8 million in tax incentives in 2023, about 10 percent of the total government benefits it received.[31]

Talent Development Programs

China has focused intently on increasing the number of scientists and engineers working in key technology industries, including the life sciences. In 2020, China awarded 338,000 master’s or Ph.D. degrees in science, technology, engineering, and mathematics (STEM) fields, compared with U.S. universities’ awards of 222,000 such degrees. China doesn’t publish graduate data in specific fields, only broad fields such as engineering, science, and agriculture. In 2022, 33.5 percent of Ph.D.s awarded by Chinese universities were in the sciences, which includes the biomedical and life science fields.[32] In the United States, Ph.D. graduates in the biological and biomedical sciences specifically accounted for 16 percent of the total.[33]

China’s Thousand Talents Program is a state-supported initiative designed to attract and incentivize top-tier individuals in their fields to immigrate and work in China, with a specific emphasis on strategic and emerging sectors. Of the more than 7,000 scientists and entrepreneurs recruited by the program since its inception in 2008, 1,400 have been for the life sciences section, making it one of the largest cohorts in the program. They include founders of leading companies, chief scientific officers, and career academics.[34] Anecdotal evidence suggests that recruits through the program have had an outsized impact on China’s biopharmaceutical industry, helping to reverse the brain drain that plagued the country for decades.[35] According to Dan Zhang, former secretary-general of the Thousand Talents Program, recruits are “behind the majority of drug approvals in China … they fill peer review committees and life-science faculties, and … many are made university deans.”[36]

China’s talent strategy has also benefited from a reverse brain drain. Many founders and executives leading China’s most prominent biopharmaceutical firms received their scientific training or early-career experience in the United States or Europe before returning home, meaning that much of China’s contemporary biopharmaceutical leadership was, in effect, educated and credentialed by Western institutions.

Illegitimate Practices

While the preceding policies certainly represent legitimate practices countries can use to grow their life sciences sectors, China has also turned to a range of innovation mercantilist practices that are not consonant with China’s commitments to trade partners under World Trade Organization rules.

IP Theft

There have been many reports of Chinese biomedical researchers working at U.S. universities, often on National Institutes of Health (NIH) grants, and taking the IP developed in their labs back to China.[37] For example, in 2020, the U.S. Department of Justice charged the chair of Harvard University’s Chemistry and Chemical Biology Department, Charles Lieber, with aiding China with “one count of making a materially false, fictitious and fraudulent statement” regarding his work with organizations tied to the Chinese government, while on NIH funding.[38] Also in 2020, Ohio citizen Yu Zhou was sentenced to prison for conspiring to steal trade secrets concerning the research and treatment of different medical conditions, including cancer, from Nationwide Children’s Hospital’s Research Institute to sell to China.[39]

Moreover, Chinese state-sponsored actors have targeted biopharma firms for IP theft, including through cybertheft and rogue employees.[40] That theft is sometimes through direct means whereby scientists working at U.S. biopharma companies steal IP and then transfer it to China. For instance, in 2018, Yu Xue, a leading biochemist working at a GlaxoSmithKline research facility in Philadelphia, admitted to stealing company secrets and funneling them to Renopharma, a Chinese biotech company funded in part by the Chinese government.[41] In October 2023, intelligence chiefs from the Five Eyes countries—Australia, Canada, Great Britain, New Zealand, and the United States—accused China of IP theft in sectors including biotechnology.[42]

Subsidies

China devotes billions of dollars in state subsidies to prop up companies that would not withstand normal market forces.[43] In an analysis conducted by Stanford University’s Center on China’s Economy and Institutions, researchers found that among the firms that accounted for 82 percent of China’s R&D investment, 99 percent had received subsidies from the government. It’s therefore unsurprising that Chinese subsidies account for about one-fifth of all R&D expenditures in the country.[44]

Many of the subsidies provided to biotechnology firms come from state and local governments. For example, Shanghai’s regional government introduced a series of incentives specifically for biopharmaceutical companies. These include financial support for eligible R&D projects on innovative drugs, with a maximum award value of RMB 30 million ($4.2 million), a 50 percent subsidy on low-interest loans for firms investing in technological transformation or production expansion, and a subsidy of 20 percent of investment value for firms starting major projects in emerging industries in the city.[45]

Junshi Biosciences, a leading biopharmaceutical firm headquartered in Shanghai, is one of many firms in the industry to benefit from extensive subsidies. In 2025, Junshi received over RMB 16 million ($2.2 million) for “government grants related to property, plant, and equipment” and an additional RMB 39 million ($5.4 million) in subsidies from the People’s Republic of China (PRC) for R&D activities. This also doesn’t include the RMB 167 million ($23.2 million) the company reported in deferred subsidies, meaning the subsidies had been received by Junshi but not yet fully recognized as income.[46]

Selling Unregulated Products on Gray Markets

Chinese firms have also engaged in selling unregulated products in U.S. markets, and often at price points (often one-fifth retail prices) that undermine legitimate competitors. This is particularly evident in the peptide industry, which has seen the emergence of a large, ill-regulated Chinese export market.[47]

Driven by global demand for weight-loss drugs, anti-aging treatments, and performance-enhancing compounds, hundreds of Chinese vendors now sell peptide products directly to Western consumers through social media, messaging platforms, and e-commerce channels, often sourcing from a small number of manufacturers while obscuring the underlying supply chain. Many of these compounds have not undergone rigorous clinical testing, are not approved for human use in major Western markets, and are sold outside established pharmaceutical distribution channels. Chinese factories bypass international drug regulations by labeling injectable peptides as “for research use only” or “not for human consumption.” This thin legal fiction allows Chinese manufacturers to export compounds directly to consumers or Western domestic intermediaries without seeking proper regulatory approval, as authorities do not oversee chemicals explicitly labeled as nonmedicinal.

This trend not only exposes consumers to potential safety risks associated with contamination, improper handling, and uncertain product quality, but also underscores the strategic importance of strengthening trusted domestic and allied biopharmaceutical manufacturing capacity and improving cross-border oversight of emerging therapeutic technologies.

China’s Growing Biopharmaceutical Competitiveness

As this report’s introduction laid out, China’s biopharmaceutical competitiveness is rapidly growing across virtually all dimensions. This section examines China’s output in innovation input indicators such as patents and scholarly articles, R&D investments, global market share, location quotients (LQs), trade balances, and value-added output in pharmaceutical products. It then examines China’s growth in clinical trial activity and development of innovative drugs.

Patents and Scholarly Publications

The United States continues to lead the world in a number of biopharmaceutical innovation indicators, but its lead is declining. And in certain indicators, such as scientific publications, America’s lead has disappeared altogether.

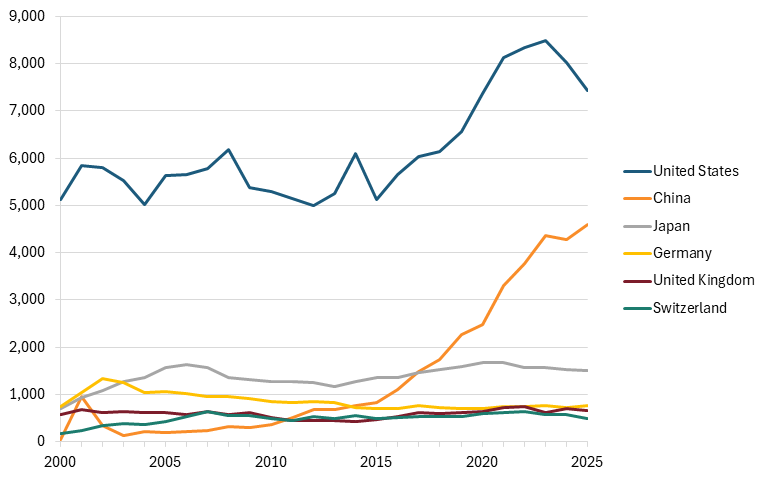

As of 2025, the United States led the world in patenting activity, but China has made great strides. In 2000, China accounted for just 14 patent publications in biopharmaceuticals under the Patent Cooperation Treaty (PCT), including 5 in biotechnology and another 9 in pharmaceuticals. But by 2025, this total had ballooned to 4,595, the second-highest number in the world behind the United States, whose innovators published 7,431 patents that year. Notably, the PCT publishes patents prior to their examination, so published patents are not necessarily granted.[48] (See figure 1.)

Figure 1: PCT patent publications in biotechnology and pharmaceuticals, 2000–2025[49]

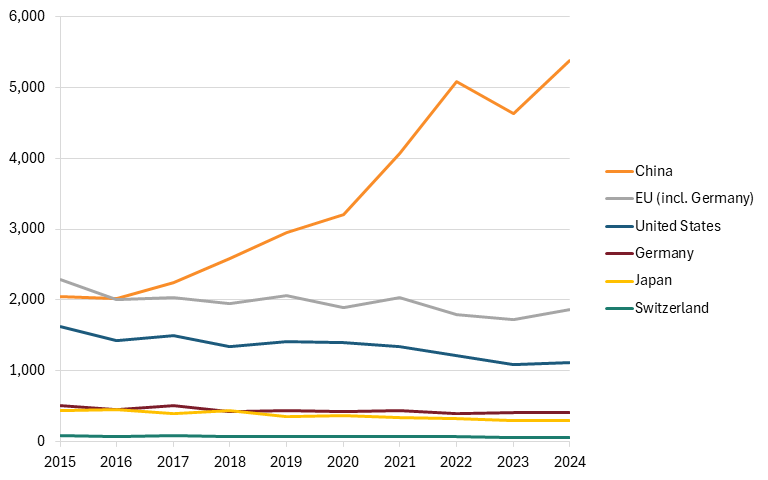

Though the United States leads China in patent activity, China has considerably surpassed the United States (and the rest of the world) in scientific publications in biotechnology. Over the decade from 2015 to 2024, the number of biotechnology publications in China increased by 162 percent, from about 2.1 million to 5.4 million. Over the same period, publications in the European Union and the United States declined by 19 percent and 31 percent, respectively.[50] (See figure 2.)

Figure 2: Scientific publications in biotechnology, 2015–2024[51]

A country’s number of publications in absolute terms in a given field is a less-than-ideal measure of innovation, given that China’s population is roughly four times that of the United States and the prevalence of “paper mills” in China increases the likelihood of fraudulent publications by Chinese institutions.[52] However, the Organization for Economic Cooperation and Development (OECD) provides data on highly cited publications by technology area, which can control for the prevalence of fraudulent papers.

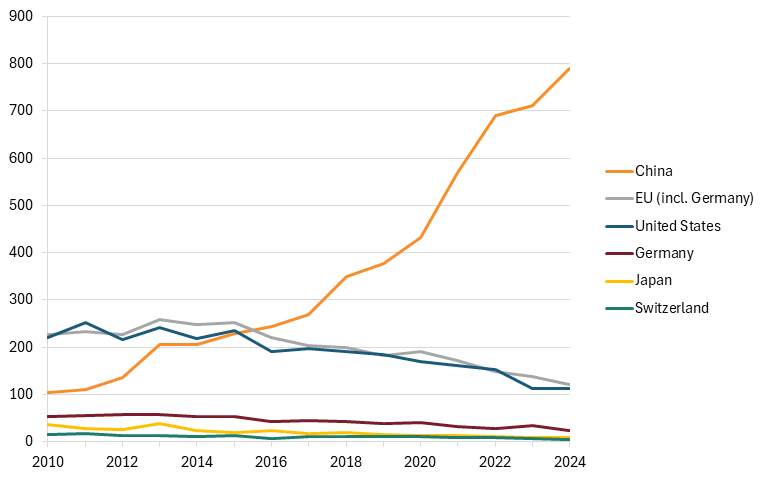

In 2024, China also led the world in highly cited biotech publications, with nearly 800 papers, compared with the next-closest region, the EU, at 122. The United States had 112.[53] (See figure 3.)

Figure 3: Biotech publications among the top 10 percent of the world’s most cited publications, 2015–2024[54]

Research and Development

The biopharmaceutical industry is heavily reliant on R&D investment, with the average Western firm investing about 20 percent of its annual revenue in R&D. Interestingly, Chinese firms invest just half that, or 10 percent of their annual revenue.[55]

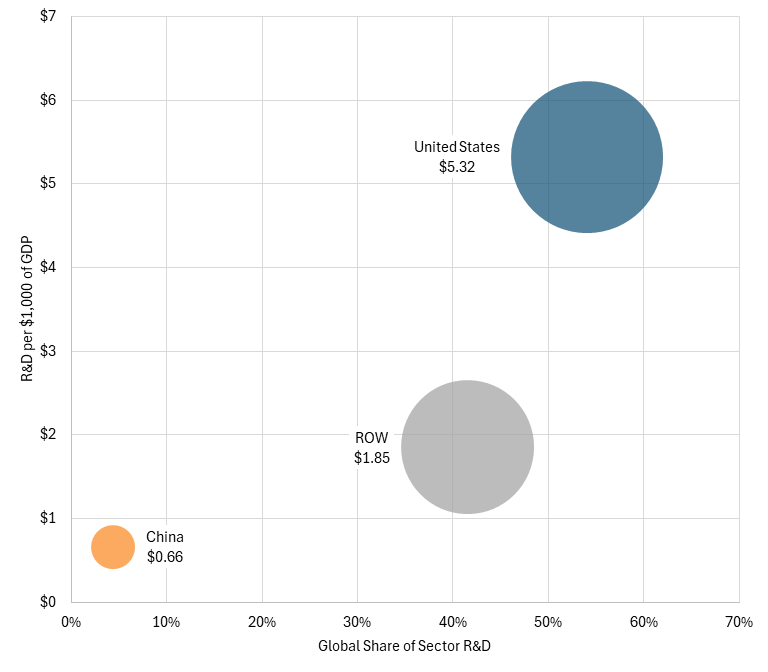

The United States leads the world in private sector R&D investment in the biopharmaceutical sector by a sizeable margin. In 2024, U.S. firms invested $153 billion in R&D, equivalent to 54 percent of global R&D investment in this sector. In comparison, Chinese firms invested about $12 billion, or 4 percent of global investment and just 8 percent of U.S. private-sector investment. When controlling for GDP, U.S. firms invested $5.32 per $1,000 of GDP, compared with just $0.66 per $1,000 of GDP for Chinese firms.[56] (See figure 4.) China also invested less than the rest of the world (ROW) did, which averaged $1.85 per $1,000 of GDP.

However, China is rapidly closing the gap. Between 2014 and 2024, Chinese firms’ share of global biopharmaceutical R&D investment quadrupled, while the United States experienced only a 20 percent increase. Additionally, it’s important to recognize that, on a wage-adjusted basis, every dollar of R&D investment in China goes further than in the United States. For every $100,000 in R&D investment, the United States supports 1 R&D worker while a Chinese firm can deploy 2.3 workers, thereby increasing the amount of research that can be conducted with the same investment.[57]

Figure 4: U.S. and Chinese firms’ R&D investments in pharmaceuticals and biotechnology, 2024[58]

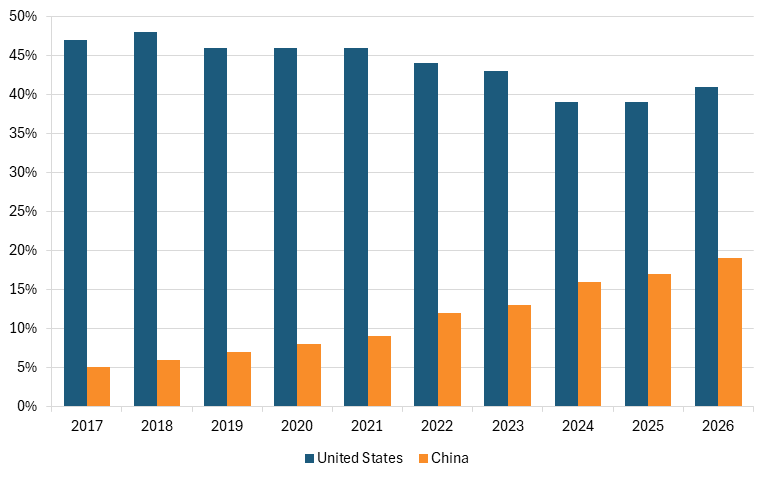

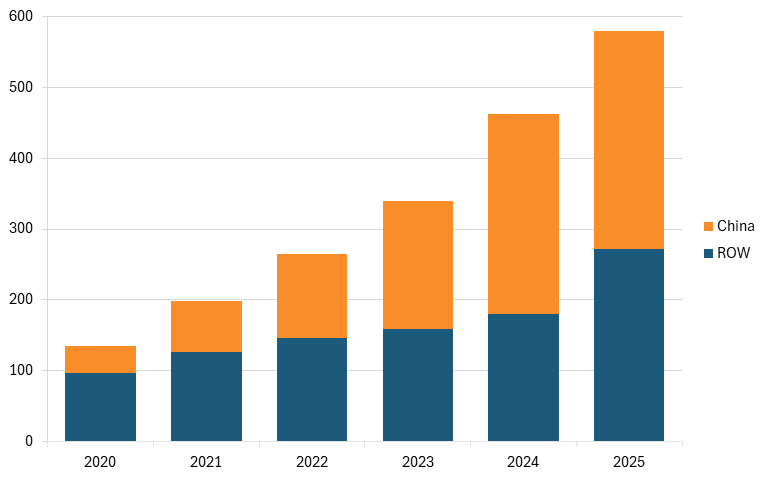

The number of biopharma firms engaged in R&D in China has also grown in recent years, in tandem with R&D investment. From 2017 to 2026, the share of global companies involved in biopharmaceutical R&D in China has grown from just 5 percent to nearly 20 percent, while the share of firms in the United States has declined from a high of 48 percent to 41 percent in 2026.[59] (See figure 5.)

Figure 5: Share of global companies involved in biopharmaceutical R&D, 2017–2026[60]

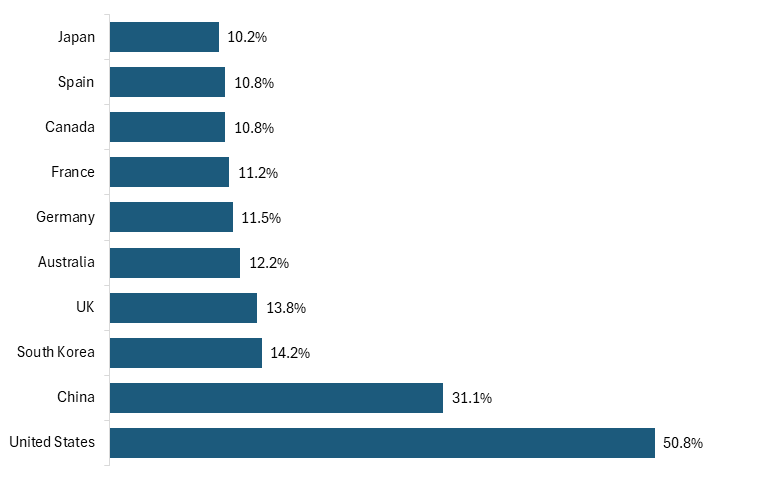

While firms may invest heavily in biopharmaceutical R&D, that research is not necessarily conducted in the country where the company is headquartered. Understanding where drug development actually occurs provides a more complete picture of the scientific workforce, research infrastructure, and innovation resources supporting the industry. Figure 6 shows what percentage of the global drug pipeline is developed by each country. (Notably, as drugs can be developed in more than one country, the percentages do not add to 100 percent.) More than 50 percent of drugs under development globally, or 11,662, were at least partially developed in the United States in 2026, an increase from 2025. Comparatively, China accounts for 7,141 drugs, or 31.1 percent, of the new drug pipeline.[61] (See figure 6.)

Figure 6: Share of global drug development conducted by country, 2026[62]

International Competitiveness Comparisons

This section analyzes international comparisons of national biopharmaceutical competitiveness, assessing global market shares, LQs, trade balances, and value-added output.

Share of Global Pharmaceutical Industry Output

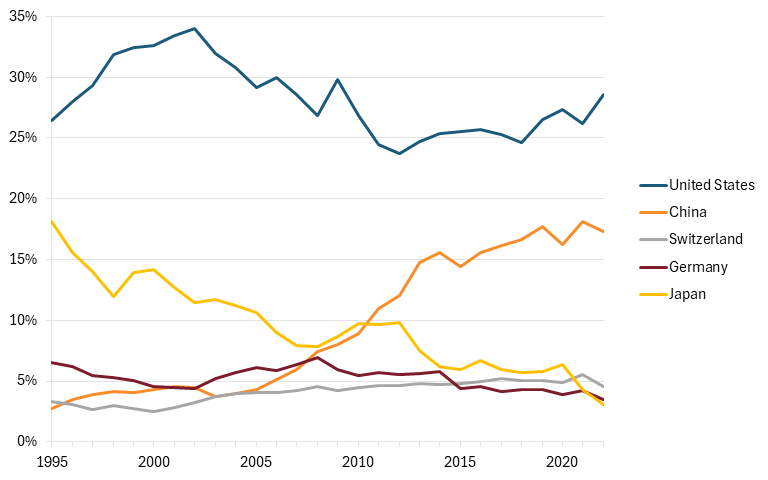

As Chinese firms have ramped up investment in biopharmaceutical R&D, China’s share of global output (i.e., global market share) has grown accordingly. OECD’s Trade in Value Added dataset includes data on value-added output for selected industries from 1995 to 2022. Over this period, China’s global market share increased over sixfold, from an insignificant 2.7 percent to 17.3 percent, second only to the United States. The United States, meanwhile, saw its market share increase only marginally, from 26.5 percent to 28.6 percent, though it is still the dominant leader on this metric.[63] (See figure 7.) Japan’s contraction in share of global pharmaceutical industry output was quite pronounced over this period.

Figure 7: Countries’ share of global pharmaceutical industry output, 1995–2022[64]

Location Quotient

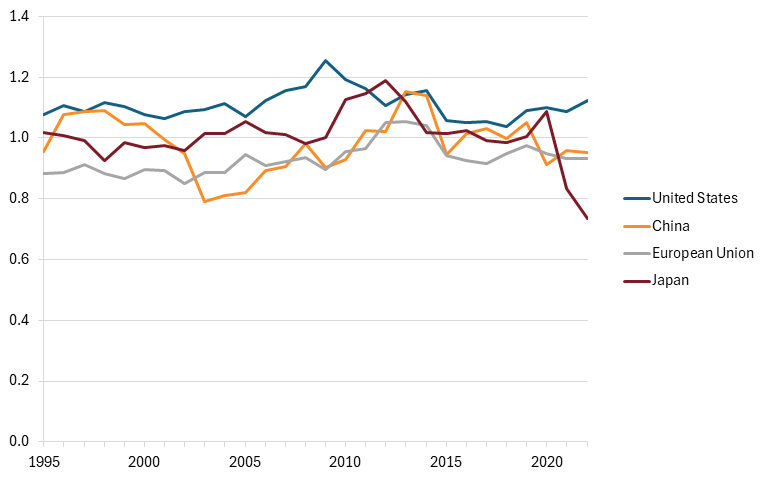

An LQ measures any region’s level of industrial specialization relative to that of a larger geographic unit—in this case, an industry within a country relative to the rest of the world.[65] An LQ of 1 for a given industry indicates that that industry contributes as much to a nation’s economy as that industry contributes to the global economy. The indicator thus demonstrates countries’ relative specializations in certain industries and how their industries are performing relative to the global norm.

As with global market share, the United States leads China in terms of LQ, with a score of 1.12, overperforming the global average, while China posts an LQ of 0.95. China’s LQ fluctuated around average for much of the period from 1995 to 2022, starting at 0.96 in 1995, falling to a low of 0.79 in 2003, and reaching a high of 1.15 in 2013 before settling at its current level, demonstrating that its pharmaceutical industry is growing at or near the same pace as the rest of its economy. (See figure 8.) China’s LQ exceeds that of the EU and Japan, which post LQs of 0.93 and 0.74, respectively.

Figure 8: Selected countries’ LQ in pharmaceuticals, 1995–2022[66]

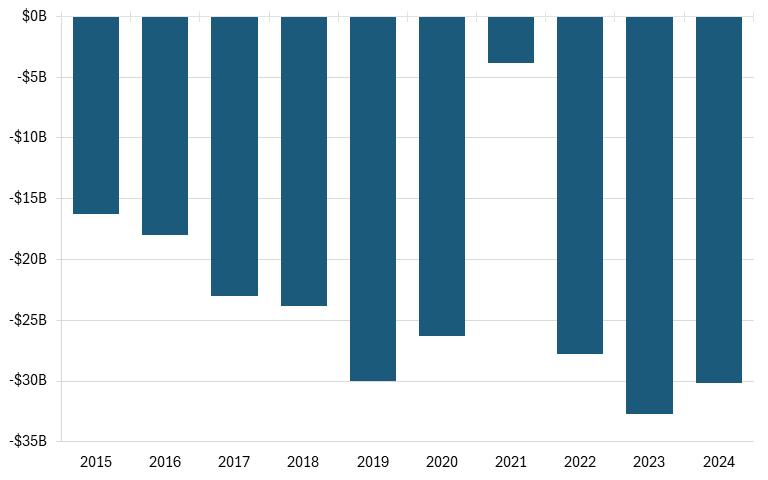

Trade Balances

In terms of trade, China ran a persistent trade deficit in pharmaceutical products over the decade from 2015 to 2024. In inflation-adjusted terms, China’s deficit remained above $15 billion annually except in 2019, peaking at nearly $33 billion in 2023. Between 2015 and 2024, China accumulated a $232 billion trade deficit in pharmaceutical products (one-quarter of the United States’ deficit in this sector).[67] (See figure 9.)

However, the United States remains highly dependent on China for key starting materials (KSMs) used to develop active pharmaceutical ingredients (APIs), with 41 percent of KSMs originating in China.[68] (A subsequent section of this report examines China’s API leadership.) Despite this, China runs a trade deficit with the United States due to its dependence on high-value finished medications imported from the United States. As Chinese firms continue to develop innovative, high-value pharmaceuticals, there is potential for China’s deficit to decrease (if not reverse).

Figure 9: China’s trade balance in pharmaceutical products, 2015–2024 (2024 dollars)[69]

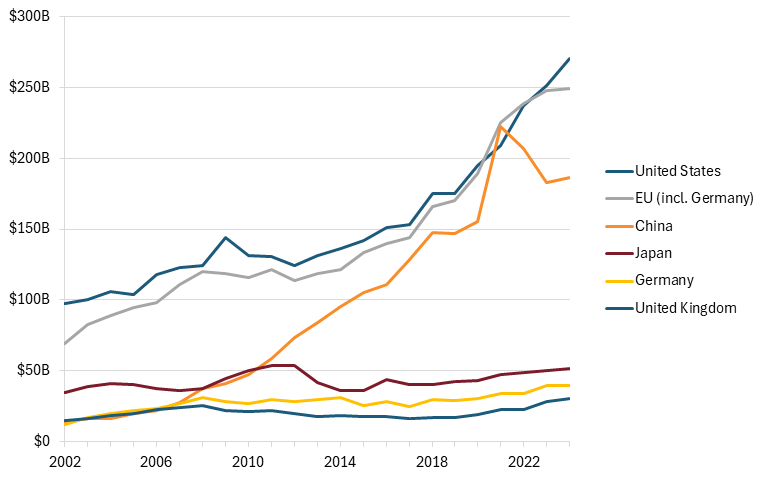

Value-Added Output

The cumulative effect of China’s investments in research, talent, clinical development, and advanced therapeutic technologies is increasingly visible in measures of industry output. While the United States remains the world’s leading biopharmaceutical producer, China’s industry has expanded dramatically over the last two decades and is now competing directly with established pharmaceutical powers in Europe, Japan, and North America.

From 2002 to 2024, China’s value-added output in the global pharmaceuticals industry grew nearly 13-fold, from $14.5 billion to $187 billion.

Though the United States continues to generate the highest level of pharmaceutical output globally, China’s output increased from just $14.5 billion in 2002 to nearly $187 billion in 2024, representing a more than 13-fold increase over the period. Overall, China’s value-added output in the pharmaceutical industry increased by 94 percent between 2022 and 2024, about 10 percent annually.[70] (See figure 10.)

Figure 10: Select countries’ value-added output in pharmaceuticals, 2022–2024[71]

China’s growing biopharmaceutical capabilities are increasingly being reflected in the world’s largest drugmakers by pipeline size. Pipeline size measures the number of active drug candidates a company has under development. While U.S. and European firms continue to dominate the rankings, 3 Chinese companies now rank among the world’s 20 largest pharmaceutical pipelines. Jiangsu Hengrui Pharmaceuticals ranks 12th globally with 178 active drug candidates, while Sino Biopharmaceutical and CSPC Pharmaceutical rank 15th and 16th, respectively. Notably, each Chinese firm has either maintained its position or moved up the rankings since 2025, with Jiangsu Hengrui moving from 13th to 12th and CSPC Pharma rising from 19th to 16th.[72] (See table 1.)

Table 1: Top 20 pharma companies by size of pipeline, 2026[73]

|

2026 Position (vs. 2025) |

Company |

Country of HQ |

Active Drugs, 2026 (vs. 2025) |

Originated Drugs, 2026 |

|

1 (2) |

Roche |

Switzerland |

262 (261) |

147 |

|

2 (4) |

AstraZeneca |

United Kingdom |

261 (241) |

166 |

|

3 (1) |

Pfizer |

United States |

257 (271) |

163 |

|

4 (5) |

Sanofi |

France |

251 (233) |

135 |

|

5 (3) |

Novartis |

Switzerland |

244 (254) |

137 |

|

6 (7) |

Eli Lilly |

United States |

233 (224) |

138 |

|

7 (6) |

Bristol Myers Squibb |

United States |

214 (227) |

124 |

|

8 (8) |

Merck & Co. |

United States |

207 (216) |

103 |

|

9 (11) |

AbbVie |

United States |

200 (190) |

76 |

|

10 (9) |

Johnson & Johnson |

United States |

198 (200) |

111 |

|

11 (10) |

GSK |

United Kingdom |

185 (194) |

88 |

|

12 (13) |

Jiangsu Hengrui Pharmaceuticals |

China |

178 (173) |

163 |

|

13 (12) |

Takeda |

Japan |

167 (187) |

61 |

|

14 (14) |

Boehringer Ingelheim |

Germany |

143 (133) |

90 |

|

15 (15) |

Sino Biopharmaceutical |

China |

119 (125) |

93 |

|

16 (19) |

CSPC Pharmaceutical |

China |

117 (102) |

96 |

|

17 (22) |

Novo Nordisk |

Denmark |

109 (97) |

70 |

|

18 (17) |

Gilead Sciences |

United States |

107 (106) |

67 |

|

19 (16) |

Otsuka Holdings |

Japan |

107 (114) |

57 |

|

20 (18) |

Bayer |

Germany |

100 (104) |

65 |

Clinical Trials and Drug Development

Increases in R&D investment and innovation outputs have contributed to China’s growing success in the biopharmaceutical industry, but these are not the only factors. China has developed efficiencies in the clinical trial phase of drug development that have contributed to legitimate time and cost savings for drug developers. For example, the China Food and Drug Administration, the precursor to what is now the National Medical Products Administration (NMPA), adopted and gradually implemented the International Council for Harmonization of Technical Requirements for Pharmaceuticals for Human Use guidelines, enabling China’s drug administration to align with international standards.[74] NMPA also instituted a series of reforms designed to accelerate drug development, including expanding reviewer capacity, modernizing the registration classification system, and allowing researchers to begin testing drugs quickly rather than waiting several months for clearance (as is the case in Western nations).[75] From 2015 to 2018 alone, the time it took to secure approval for human trials in China shrank from 501 days to 87.[76] Additionally, patient enrollment in Chinese tertiary hospitals is 5 to 10 times higher than at American academic medical centers, increasing patient availability and the speed of trial enrollment. Per-patient costs are also lower in China.[77]

Chinese firms can now take a drug from discovery to the start of human trials in about half the global industry’s average time.

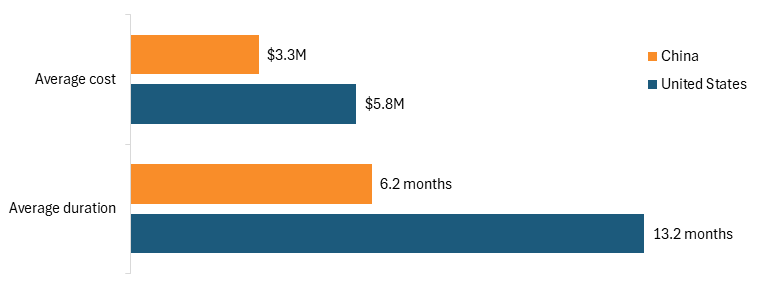

According to a McKinsey report, these process improvements have sped up the timeline from early discovery to new drug application in China by 50 to 70 percent.[78] In total, Chinese firms can now take a drug from discovery to the start of human trials in about half the global industry’s average time.[79] Research from PhRMA finds that the average duration of a phase I clinical trial conducted in China in 2025 was over 50 percent shorter than phase I trials conducted in the United States. Similarly, the average cost of a phase I clinical trial in China was 43 percent less expensive than a phase I trial in the United States.[80] (See figure 11.)

Figure 11: Average cost and duration of U.S. and Chinese phase I clinical trials, all disease areas, 2025[81]

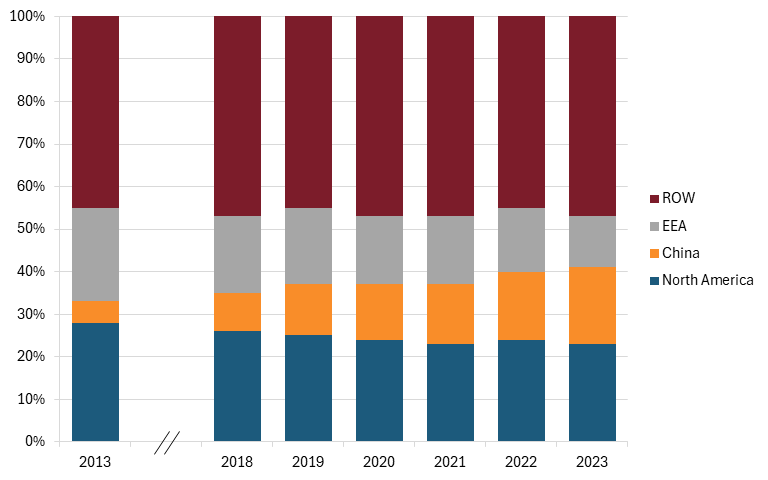

Given the comparative advantage Chinese firms have in completing clinical trials faster and more cheaply than American competitors can, it’s unsurprising that Chinese firms have continued to increase the number of clinical trials they’ve started each year since 2013. In 2013, clinical trial starts in China accounted for 5 percent of all global trials, compared with 28 percent in North America (the majority of which occurred in the United States). By 2023, China accounted for 18 percent of all clinical trials, just 5 percentage points behind North America and more than double the European Economic Area (EEA), which accounted for just 12 percent, a decline from its high of 22 percent in 2013.[82] (See figure 12.)

Figure 12: Percentage of global commercial clinical trial starts by region, 2013–2023[83]

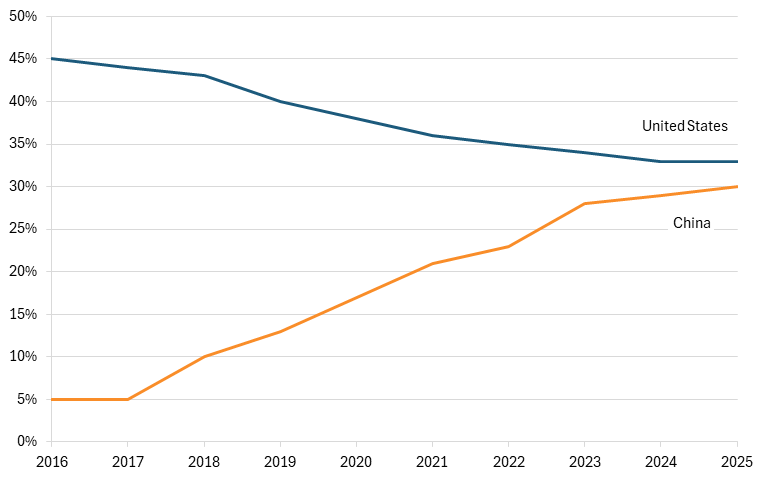

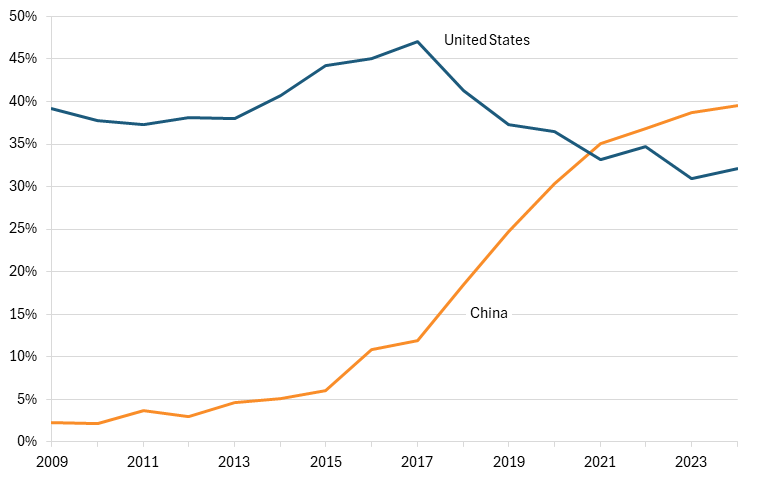

Beyond clinical trials broadly, China is also catching up to the United States in trials of the most-innovative drugs, including those with new mechanisms of action or that use advanced technologies to treat diseases. In 2016, just 5 percent of global clinical trials for innovative drugs were conducted in China, compared with 45 percent in the United States. This gap has now shrunk substantially, with 30 percent of all innovative drug trials taking place in China—a 500 percent increase—compared with 33 percent in the United States.[84] (See figure 13.)

Figure 13: China and U.S. companies’ share of worldwide clinical trials for innovative drugs, 2016–2025[85]

China is catching up to the United States in trials of the most innovative drugs, including those with new mechanisms of action or that use advanced technologies to treat diseases.

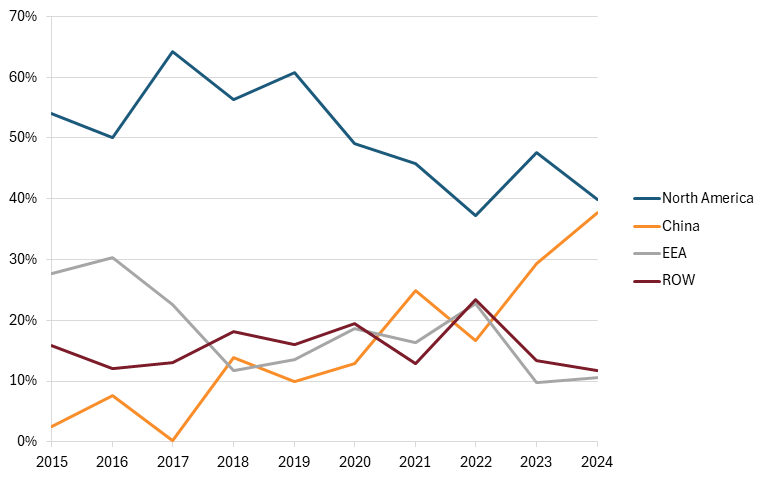

Not only are innovative drugs in China being tested in clinical trials in large numbers, but also those trials are yielding approvals. Approvals of innovative drugs out of China in 2015 accounted for just 3 percent of global drug approvals. North America, by comparison, was responsible for 54 percent, while the EEA was responsible for 28 percent. But in the years since, the quantity of innovative drugs approved in China has ballooned, increasing almost every year. Between 2023 and 2024 alone, the share of global approvals in China skyrocketed, increasing from 29 percent to 38 percent, while North American approvals fell from 48 percent to 40 percent. Just 11 percent of global drug approvals originated from the EEA in 2024.[86] (See figure 14.)

Figure 14: Percentage of first global approvals of innovative drugs, 2015–2024[87]

Out-Licensing Deals

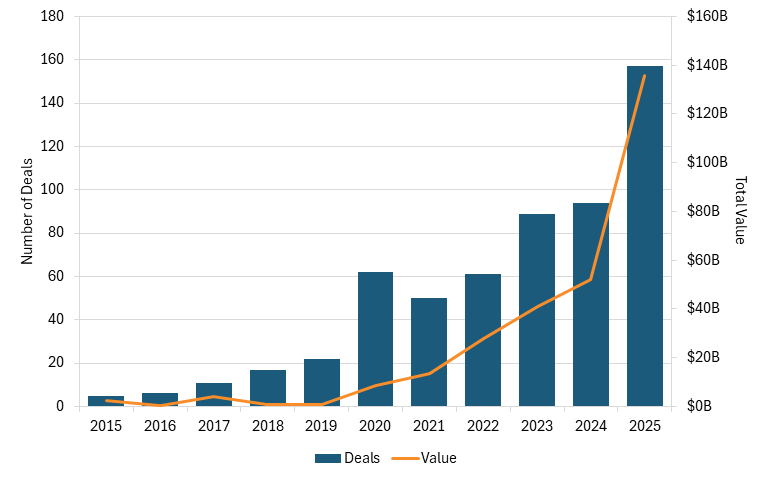

Out-licensing deals occur when a company that developed a treatment grants another organization the rights to develop, manufacture, or market that asset, allowing the developer to monetize their product. From 2015 to 2025, the number of out-licensing deals from China increased by a factor of 31, from 5 deals to 157. The value of these deals increased at an even greater rate. Between 2015 and 2025, the value of out-licensing deals increased by a factor of 54, from $2.5 billion to $135.7 billion, demonstrating the sheer financial growth of the Chinese biopharmaceutical industry over this time period. (See figure 15.) In the first quarter of 2026 alone, out-licensing deals were valued at $60 billion.[88]

Figure 15: China’s out-licensing deals and value, 2015–2025[89]

Between 2022 and 2026, the average upfront value of individual licensing deals between Chinese and Western companies more than tripled, from $52 million to $172 million.[90] In January 2026, AstraZeneca paid CSPC Pharmaceuticals $1.2 billion upfront for its portfolio of weight loss drugs, with the promise of an additional $13.8 billion in milestone payments.[91] In May, Bristol Myers Squibb partnered with Hengrui Pharma to jointly develop 13 programs, paying $600 million upfront and promising up to $15.2 billion should the treatments achieve commercial targets.[92]

From 2015 to 2025, the number of out-licensing deals from China increased by a factor of 31, from 5 deals to 157.

Similarly, in-licensing allows a firm to license the rights of a product from another firm. In 2025, China accounted for 48 percent, nearly half, of global pharmaceutical in-licensing deals, up from a mere 5 percent five years prior.[93]

Emerging Therapies

China is no longer merely a low-cost manufacturer of pharmaceutical products; it is increasingly competing in some of the industry’s most advanced and commercially valuable therapeutic areas. These emerging modalities often command premium prices and generate higher profit margins, making them attractive targets for investment and research. Chinese firms have strategically focused on identifying high-growth therapeutic categories and emerging technologies wherein future demand and commercial potential are greatest.[94] As a result, Chinese biopharmaceutical companies have established leading positions in several cutting-edge fields, demonstrating a growing capacity not only to manufacture medicines, but also to innovate at the technological frontier.

The following section explores China’s advancements in four of these therapeutic areas: oncology, RNA interference (RNAi), antibody drug conjugates (ADCs), and gene therapies.

Oncology

Among therapeutic areas, China has become particularly competitive in oncology drug development, throwing much of its biopharmaceutical weight at the field. Several of China’s largest biopharmaceutical firms, including BeiGene, the largest pharmaceutical R&D investor in the country, specialize in oncology and immune-oncology drug development.[95] BeiGene has developed three approved drugs, including one, Brukinsa, that has been approved in over 70 countries and regions, including the United States.[96]

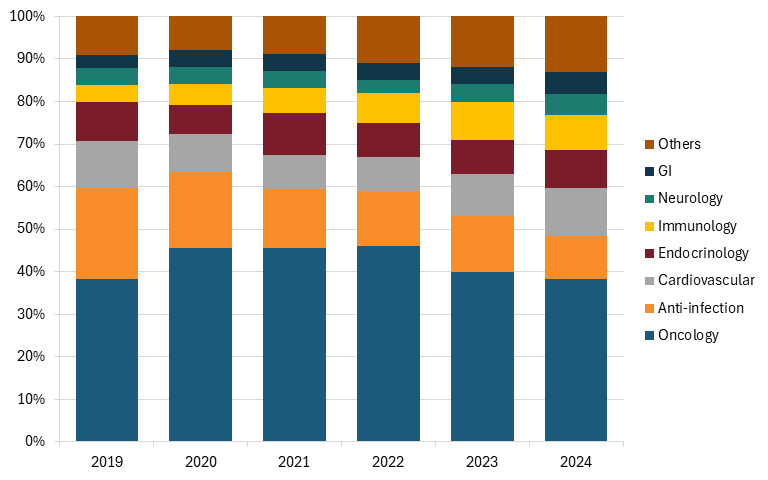

Between 2019 and 2024, oncology clinical trials in China accounted for as much as 46 percent of all clinical trials in the country, although that share fell to 38 percent in 2024. However, compared with other therapies, oncology was over three times higher than the next closest therapeutic area, cardiovascular treatments, in new clinical trial starts.[97] (See figure 16.)

Figure 16: Share of newly started clinical trials in China by therapeutic area, 2019–2024[98]

Chinese cancer therapies have been especially attractive for licensing and approval for U.S. pharma companies. In July 2025, Pfizer licensed a cancer treatment from 3SBio for $1.25 billion, $4.8 billion in milestone payments, and $100 million in equity.[99] In May, Pfizer paid Innovent $650 million upfront, with possible payouts of $9.85 billion, to partner on the development of 12 cancer medications.[100] Overall, oncology drugs accounted for nearly 50 percent of all global licensing deals made by China in 2024, or 23 drug therapies. (See table 2.)

One of the drugs that has gotten particular attention from pharmaceutical companies globally is ivonescimab, an experimental lung cancer drug developed by Chinese firm Akeso Biopharma.[101] The drug, which was licensed by the U.S. firm Summit Therapeutics, reduced the risk of death by 34 percent in patients who received it in a late-stage clinical trial, keeping patients alive for four months longer than the control treatment did.[102]

Table 2: Number of global licensing deals by Chinese firms by therapeutic area[103]

|

Therapeutic Area |

2020 |

2024 |

|

Oncology |

11 |

23 |

|

Immunology and inflammation |

1 |

14 |

|

Cardiometabolic |

1 |

7 |

|

Infectious diseases |

3 |

1 |

|

Ophthalmology |

1 |

0 |

In many respects, China is now beating the United States in oncology R&D. In 2024, China overtook the United States in research output in oncology for the first time, with over 2,600 research publications compared with 2,481 from the United States.[104] Additionally, according to a report from IQVIA, China-based companies accounted for 39 percent of global oncology clinical trial starts in 2024, up from only 5 percent in 2014. (See figure 17.) China surpassed the United States in share of global oncology clinical trial starts in 2021, now accounting for a 7 percentage point higher share than the United States. Between 2020 and 2024, China launched 84 new active substances in oncology, more than double the 37 it had launched from 2015 to 2019.[105]

Figure 17: Share of oncology trial starts by company headquarters location, 2009–2024[106]

Despite China’s great strides in oncological drug development, barriers remain. Though a few drugs, such as the Chinese medications Fruzaqla and Ryzneuta, have been approved for the U.S. market, there are still high barriers to approval, with some U.S. Food and Drug Administration (FDA) regulators simply refusing to approve drugs based on data that was collected in China.[107] There is also a lack of evidence that Chinese cancer drugs, such as ivonescimab, are more effective than existing U.S. therapies. In clinical trials, ivonescimab was tested against a control drug that is not approved in the United States, and it was not compared with the typical immunotherapy drug offered in the United States, Merck’s lung cancer medication Keytruda. Therefore, it’s unclear if ivonescimab is more effective and extends lives longer than Keytruda does.[108]

U.S. companies were the first to create multicancer early detection (MCED) technologies that could drastically improve cancer detection and treatability.[109] MCEDs have the potential to detect dozens of cancers accurately and provide a novel avenue to identify cancers that lack routine screening approaches. Cancers not only remain a significant health challenge to Americans, but also cause significant economic burden, making it imperative that the United States continue to lead in cancer detection tools such as MCEDs.

However, a growing number of highly competitive Chinese companies are becoming key innovators in the MCED space. The recent PROFOUND MCED study sponsored by Shanghai Weihe Medical Laboratories in collaboration with Peking University demonstrates that their emerging liquid biopsy-based MCED test could be relatively effectively tailored to 16 types of cancer that account for approximately 85 percent of total cancer incidences in China, showing an overall sensitivity of 70.6 percent.[110] This study is not just a one-off success story; numerous other Chinese companies are becoming increasingly competitive in the MCED space—including Burning Rock DX, Berry Oncology, and Geneseeq—allowing China to rapidly approach dominance in the MCED sector.

Leadership in MCED technology is still unfolding, but U.S. leadership in this critical field can’t be taken for granted as Chinese competitors become increasingly more entrenched. U.S. leadership in MCED technology not only prevents reliance on foreign adversaries for access to cancer-screening tools, but also safeguards the personal genomic data of U.S. citizens.

RNA Interference

RNAi is a cutting-edge therapeutic technology that uses short RNA strands to selectively silence disease-causing genes before they produce harmful proteins. Unlike traditional small-molecule therapies, RNAi therapies intervene earlier in the disease process, enabling treatment of conditions that were previously difficult or impossible to address. The technology represents one of the most promising areas of modern biopharmaceutical innovation, leading to the development of multiple approved therapies and attracting significant investment.

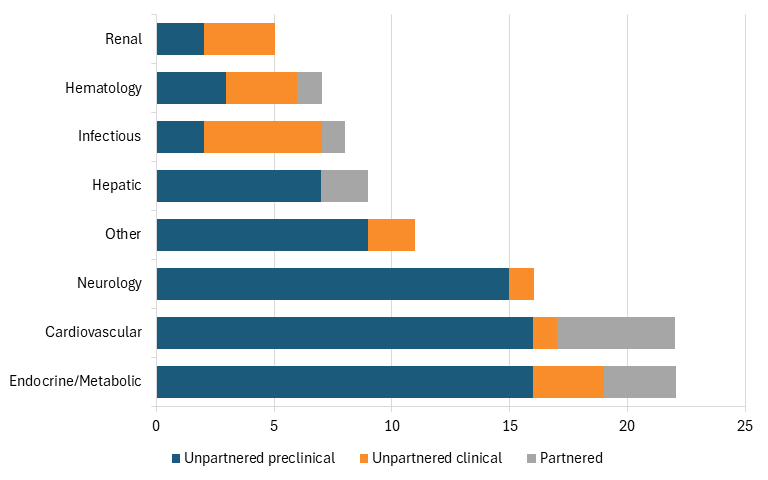

RNAi is likely to play an increasingly important role in the next generation of medicines, particularly in China. Chinese firms pursuing RNAi programs have become increasingly plentiful, with at least 12 RNAi development companies in China in 2025, most of which were founded in the last decade and 4 of which were founded since 2020. (See table 3.) Since 2024, four licensing deals for RNAi programs developed in China have been announced, each with the potential to generate $1 billion in value. There is also still substantially more activity occurring in the Chinese RNAi pipeline beyond these four programs. Chinese RNAi firms collectively are now operating 22 clinical-stage programs, 75 preclinical programs, and 11 partnered programs as of 2025. Considering this, there is a high potential for more high-value RNAi deals coming from China in the future.[111]

Table 3: China’s RNAi products, 2025[112]

|

Company |

Founded |

Lead Stage |

Clinical Programs |

Preclinical Programs |

Partnered Programs |

Private/Public |

|

Argo |

2021 |

Ph II |

7 |

34 |

4 |

Private |

|

Ribo |

2007 |

Ph II |

7 |

11 |

3 |

Private, in HKEX IPO queue |

|

Rona |

2021 |

Ph II |

3 |

12 |

0 |

Private |

|

Hengrui Pharmaceuticals |

1970 |

Ph II |

1 |

0 |

0 |

Public |

|

Hepa Thera Bio |

2021 |

Ph II |

1 |

0 |

0 |

Private |

|

Anlong Bio |

2019 |

Ph I |

1 |

11 |

3 |

Private |

|

Haichang |

2013 |

Ph I |

1 |

0 |

0 |

Private |

|

Sino Biopharm |

2000 |

Ph I |

1 |

0 |

0 |

Public |

|

SiranBio |

2022 |

Preclin |

0 |

4 |

0 |

Private |

|

Ractigen |

2016 |

Preclin |

1 |

0 |

0 |

Private |

|

Mabwell |

2017 |

Preclin |

0 |

1 |

1 |

Public |

|

Junshi |

2012 |

Preclin |

0 |

1 |

0 |

Public |

|

Total |

|

22 |

75 |

11 |

|

China’s RNAi development pipeline is growing in scale and breadth. The largest concentrations of programs are in endocrine and metabolic diseases and cardiovascular treatments, each accounting for roughly one-quarter of all Chinese RNAi programs. There is also a significant amount of activity in the neurology sector, with about 16 programs. (See figure 18.) Importantly, RNAi research activity in China spans both clinical and preclinical stages, suggesting that Chinese firms are building a long-term pipeline of RNAi assets.[113]

Figure 18: China’s biotech RNAi programs, 2025[114]

Antibody Drug Conjugates

ADCs represent a type of biologic drug used to treat cancer by combining targeted antibodies with cytotoxic small-molecule drugs. These emerging drug treatments have demonstrated higher efficacy rates in treating cancer and also present a safer form of treatment than chemotherapy does. ADC development has grown substantially over the past several years, with first disclosures increasing from 406 in 2021 to a high of 795 in 2024, nearly a 100 percent increase.[115]

China surpassed the United States in the share of global oncology clinical trial starts in 2021, now accounting for 39 percent of global trials, compared with 32 percent in the United States.

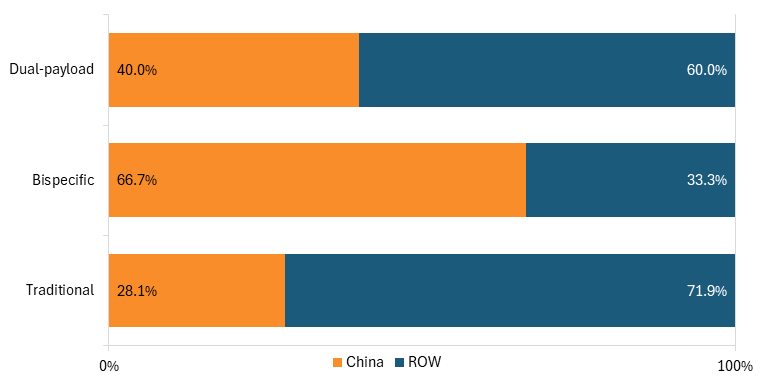

ADCs represent a class of drugs that Chinese companies have intentionally targeted, making China the world leader in the ADC pipeline with more than 42 percent of the global share.[116] Chinese firms have gained particular dominance in next-generation ADC modalities, including bispecific and dual-payload ADCs, accounting for 67 percent and 40 percent of all first drug disclosures, respectively, in 2025. (See figure 19.)

Figure 19: Number of ADC drug disclosures by China and elsewhere, 2025 (through October)[117]

ADC drug trials have also grown rapidly, with the number of global trials increasing by 34 percent annually. Yet the rate of trial growth has been even greater in China, with trials growing at a rapid 54 percent annually. As with clinical trials generally, Chinese ADC developers benefit from the lack of regulatory and logistical hurdles in clinical trial facilitation in China, including low trial costs and access to a large patient pool.[118] As of 2023, ADC clinical trials in China accounted for over half of all global ADC trials. (See figure 20.)

Figure 20: ADC trials initiated in China and elsewhere, 2020–2025[119]

Due to its leadership in ADC innovation and development, China has also become established as a key market for deal-making. Deal-making is a critical component of pharmaceutical innovation and commercialization, with over 70 percent of revenue from new drug development coming from externally sourced, or licensed, products.[120] The number of ADC deals in China grew at an average rate of 18 percent annually between 2015 and 2025, with deal value reaching $24 billion in 2025. Licensing agreements alone were valued at over $60 billion cumulatively from 2020 to 2025.[121]

China’s leadership in ADCs is indicative of a broader shift in the global biopharmaceutical landscape. The country’s dominance in drug disclosures, clinical trials, and licensing activity suggests that Chinese firms are becoming increasingly capable of identifying, developing, and commercializing frontier therapies at scale.

Gene Therapy

Gene therapies constitute a class of treatments that modify a patient’s genetic material to treat diseases. Unlike traditional pharmaceuticals, gene therapies target the underlying genetic cause of a disease by replacing, repairing, inactivating, or introducing genes in a patient’s cells.[122] Gene therapies are also among the most expensive pharmaceutical therapies because they require complex, bespoke manufacturing and often target only small patient populations, resulting in costs of millions of dollars per dose.[123] And due to these high fixed costs, gene therapies were long considered “competition-proof.”[124]

U.S. and other North American firms have historically led in gene therapy manufacturing, with 9 of the top 10 most expensive gene therapy treatments produced by firms headquartered in the United States (the 10th is produced by the U.K. firm Orchard Therapeutics).[125] However, Chinese biopharmaceutical firms have entered the gene therapy market and begun producing therapies at a fraction of the cost of their Western competitors. One such firm, Belief BioMed, developed the first domestically manufactured gene therapy treatment for hemophilia in China. The product sold for just 1/10th the price of the U.S.-produced rival therapy.

In an analysis of the 10 most expensive gene therapies, Endpoints News found that 48 of the 77 competitor drugs in development are from China. In comparison, 21 of the competitor drugs in development are from the United States, and only 7 are from Europe.[126] And the scale of Chinese competition is extensive. Four of the most expensive gene therapy treatments—Zynteglo, Roctavian, Casgevy, and Elevidys—each have at least seven Chinese competitors.[127]

As in other areas of biopharmaceutical development, China’s regulatory and cost advantages have enabled its firms to advance gene therapies more quickly and at a lower cost than Western competitors have. The regulatory path for first-in-human dosing is much faster in China than in Western countries, while the cost per patient is about 50 percent lower, enabling companies to pursue gene therapies for diseases that were previously seen as too high-risk.[128]

Though Chinese firms have succeeded in developing gene therapies, they are not yet at the level of U.S. and European firms in terms of commercialization. Demand for gene therapies within China remains constrained by their high cost, limiting the size of the domestic market for many treatments. Moreover, Chinese therapies have faced challenges entering the U.S. market due to difficulties obtaining FDA approval. Historically, the FDA has been reticent to approve Chinese therapies, creating a roadblock for firms looking to bring their drugs to wealthier markets.[129] Nevertheless, China’s growing capabilities in gene therapy development, combined with its advantages in clinical research and manufacturing, position its firms as increasingly formidable competitors to Western leaders in this strategic field.

Policy Recommendations

As this report explains, U.S. leadership of the global biopharmaceutical industry is at a clear and present risk. If the United States is going to maintain its lead in the field, it’s going to have to develop a serious biopharmaceutical competitiveness strategy, replete with a number of specific policy interventions. The United States needs to develop a comprehensive, whole-of-government strategy, with strong cross-agency collaboration, to advance U.S. biopharmaceutical competitiveness. This report offers policy recommendations grouped into four broad categories: ensuring U.S. biopharmaceutical innovation leadership; achieving biopharmaceutical manufacturing security; coordinating with allies to promote biopharmaceutical leadership in market-oriented, rule of law-based nations; and addressing the China biopharmaceutical threat specifically.

Ensuring U.S. Innovation Leadership

Most don’t realize that the United States was once a global “also ran” in biomedical innovation.[130] Indeed, in the latter half of the 1970s, European-headquartered enterprises introduced more than twice as many new drugs to the world as did those headquartered in the United States.[131] And throughout the 1980s, fewer than 10 percent of new active substances (i.e., new drugs) were first introduced to the world in the United States.[132] And, as recently as 1990, the global research-based pharmaceutical industry invested 50 percent more in Europe than in the United States.[133]

But in recent decades, the United States has flipped the script and come to clearly lead the world in both biopharmaceutical R&D and new drug innovation. For instance, life sciences companies operating in the United States are responsible for 55 percent of global R&D investments and 65 percent of development-stage funding.[134] Since 2020, PhRMA member companies have invested over $1 trillion in biopharmaceutical R&D. In 2021, the R&D intensity of life sciences companies conducting R&D in the United States reached 34 percent.[135] That research drives drug innovation. One study finds that U.S. innovators were solely responsible for 61 percent of medicines approved by the FDA from 2011 to 2020.[136] And those innovative medicines have been made available to Americans first. For instance, considering the availability of new medicines first launched globally from 2011 through 2019, 87 percent were available first in the United States.[137]

That the United States has become the global leader in life sciences innovation has been the result, in no small part, of a series of conscientious and intentional public policies designed to make it so.

That the United States has become the global leader in life sciences innovation has been the result, in no small part, of a series of conscientious and intentional public policies designed to make it so. These policies include significant federal investment in basic life sciences research (complementing and spurring private-sector investment), robust IP protections, effective technology transfer and commercialization policies, investment incentives, and, importantly, drug pricing policies that enable companies to invest in high-risk drug development. Unfortunately, each of these pillars of American biopharmaceutical innovation leadership is under threat.

Public Investment in Biopharmaceutical R&D

The U.S. federal government has long led the world in biopharmaceutical R&D investment. For instance, in 2023, NIH received a budget of $47.7 billion for medical research in service of the American people, 82 percent of which was awarded through extramural research via almost 50,000 competitive grants to more than 300,000 researchers at more than 2,500 universities, medical schools, and other research institutions in every state.[138] NIH investments have provided a powerful engine of economic growth.[139] Over the past decade, NIH funding has generated more than $787 billion in new economic output and supported an average of 370,000 jobs annually across all 50 states.[140] In 2024 alone, NIH awarded approximately $37 billion in research funding, supporting over 408,000 jobs and producing an estimated $94.5 billion in economic activity.[141]

Some contend that NIH investment crowds out private-sector life sciences R&D investment. For instance, a recent CATO report asserts, “This government domination [i.e., extensive NIH research funding] has reduced the effectiveness of biomedical research by crowding out new and innovative research.”[142] But the reality is quite the opposite. In fact, each NIH dollar invested yields roughly $2.50 in short-term economic returns and stimulates an additional $8.30 in long-term private-sector R&D investment, underscoring the strong multiplier effect of public science funding.[143] In short, public R&D investment stimulates private sector R&D investment and provides an indispensable catalyst for U.S. life sciences innovation.

Unfortunately, the Trump administration’s proposed FY 2026 budget proposal sought to reduce NIH funding by 40 percent, from roughly $48 billion in 2025 to about $27 billion in 2026—a staggering cut that called for elimination of entire institutes, including the National Institute on Minority Health and Health Disparities and the National Institute of Nursing Research.[144]

Fortunately, Congress rejected these proposals, providing NIH with a total program funding level of $47.49 billion in FY 2026.[145] Nevertheless, the Trump administration has persisted in calling for cuts to NIH funding, with the administration’s proposed FY 2027 budget, released on April 3, 2026, calling for 12 percent NIH cuts in FY 2027.[146]

But NIH cuts carry serious downstream implications for biopharmaceutical innovation. They prompt universities to pause or cancel hiring, delay clinical trials, and scale back or shut down labs. Because of this, modeling studies indicate that a sustained 10 percent reduction in NIH funding could reduce new drug launches by 4.5 percent a year—equivalent to roughly two fewer lifesaving medicines being developed annually.[147] For this reason, Congress should continue to reject calls for NIH funding cuts. Moreover, Congress should fund NIH in excess of $50 billion in FY 2027 and further assure that NIH funding in future years will increase, at the very least, at the rate of inflation.

Advancing U.S. Biopharmaceutical Innovation

In reports such as “Ensuring U.S. Biopharmaceutical Innovation,” the Information Technology and Innovation Foundation (ITIF) has laid out a comprehensive policy agenda for technology policy to support U.S. biopharmaceutical innovation. The following briefly summarizes some of these proposals.[148]

First, policymakers should pass legislation similar to the CHIPS Act for the biopharmaceutical industry, including allocating at least $5 billion to states to provide incentives for the establishment of new biomedical production facilities and supporting the launch of a joint industry-university-government R&D partnership to reduce the cost of drug development and production. This is akin to the recommendation made by the National Security Commission on Emerging Biotechnology in April 2025 that “the U.S. government should dedicate a minimum of $15 billion over the next five years to unleash more private capital into our national biotechnology sector.”[149]

Further, policymakers should expand U.S. National Science Foundation (NSF) support to university-industry research centers working on biopharma production technology and potentially establish new centers.[150] In particular, policymakers should increase funding for NSF’s Division of Engineering and target much of the increase to the Chemical Process Systems Cluster and Engineering Biology and Health Cluster.[151] The administration should also encourage the creation of the biopharma equivalent of the Semiconductor Research Corporation, a public-private consortium that develops long-term semiconductor technology roadmaps.[152] Lastly, the Trump administration should stand up another Manufacturing USA Institute alongside the National Institute for Innovation in Manufacturing Biopharmaceuticals that would focus on manufacturing innovations for APIs and generic drugs—fields in which China currently leads.

A Market-Based Drug Pricing System

America’s life sciences companies are devoted to developing innovative drugs that tackle some of the most difficult problems in biomedical science, including solutions to heretofore intractable challenges such as Alzheimer’s, Parkinson’s, pancreatic cancer, and rare diseases (which affect small patient populations of less than 10,000). But the work is difficult. That’s why developing a new medicine can take 10 to 15 years and, on average, cost upwards of $2.6 billion.[153] Life sciences companies need to earn revenues from their successful medicines in order to recoup the R&D costs of both their successful and failed efforts, and so they can garner revenues to invest in future generations of biomedical innovation. That’s why research finds a statistically significant positive relationship between a biopharma firm’s profits from the previous year and its R&D expenditures in the current year.[154] Other research makes this linkage direct, finding that every $2.5 billion of additional biopharmaceutical revenue leads to one new drug approval.[155]

If they persist over a 10-year period, MFN drug pricing policies could result in the loss of 210 new drug approvals, together with 290 post-approval indications, resulting in a combined loss of 500 drugs, or 50 per year, leading to approximately 6.6 million lives lost worldwide.

But recent drug price controls introduced by both the Biden and Trump administrations have disrupted market economics and are already having a significant deleterious impact on innovation. Drug price controls in the Biden administration’s Inflation Reduction Act (IRA) had an immediate and swift deleterious impact on drug innovation, especially for small molecule drugs.[156] Research firm Vital Transformations finds that, from September 2021 to 2024, small-molecule investment funding dropped by 70 percent (in the wake of the promulgation of the IRA legislation).[157] That coincided with a 2023 PhRMA study in which 78 percent of PhRMA member respondents reported that they expected to cancel early-stage small-molecule pipeline projects.[158] The IRA has already forced companies to halt more than 55 drug R&D programs since it became law.[159]

Most-Favored Nation (MFN) drug pricing policies proposed by the Trump administration could be even more damaging to U.S. biopharmaceutical innovation than the IRA drug price controls have been because they would apply to all drugs, not just the specific ones selected for price controls in the IRA. Tomas Philipson and his colleagues at the University of Chicago have found that applying MFN pricing policy to existing drugs in Medicare and Medicaid would reduce U.S. pharmaceutical revenues by 49 percent. They further found that if the drug price controls persisted over a 10-year horizon, the revenue shortfall would result in the loss of 210 new drug approvals, together with 290 post-approval indications, resulting in a combined loss of 500 drugs, or 50 per year. The authors associate this large cut in innovation with a loss of 516 million life-years, corresponding to approximately 6.6 million lives lost worldwide.[160] Especially in the face of burgeoning Chinese biopharmaceutical competitiveness, policymakers should repeal the IRA drug price controls and reject the Trump administration’s various MFN drug pricing proposals.[161]

An Effective Drug Regulatory System

One reason the United States lagged behind in drug innovation in the 1970s and 1980s was that it lacked an effective drug regulatory system to support life sciences innovators. At the time, it was not uncommon for pharmaceutical companies to wait several years for their submissions of clinical trial data and efficacy studies for novel drugs to even be examined.[162] The FDA simply lacked the resources it needed to handle the caseload, particularly when a flood of applications arrived in response to the AIDS crisis of the late 1980s. That’s why, in 1987, the median approval time for a new medicines stretched to over two and a half years. Moreover, in the late 1980s, over 60 percent of new medicines were on the market overseas for at least one year before they received approval in the United States.

Especially in the face of burgeoning Chinese biopharmaceutical competitiveness, policymakers should repeal the Inflation Reduction Act drug price controls and reject the Trump administration’s various MFN drug pricing proposals.

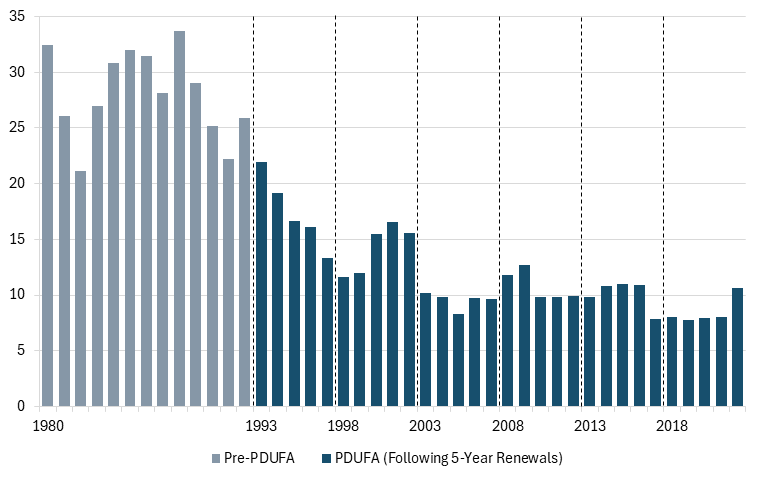

To help address this challenge, in 1992, Congress enacted the Prescription Drug User Fee Act (PDUFA), recognizing that industry user fees could supplement limited general-funds appropriations to ensure that the FDA had the needed resources at its disposal to review new drug applications in a timely manner. PDUFA paid dividends almost immediately. For instance, the U.S. General Accountability Office (GAO) found that the FDA increased its reviewer staff by 77 percent, and drug approval determination times dropped from 27 months to 14 months over the first 8 years of PDUFA.[163] By 2015, even while maintaining the FDA’s high standards for patient safety, the median drug approval time at the FDA had fallen by more than a year and a half (from 1992 levels) to under 10 months (a general timeframe that persists today).[164] (See figure 21.)

Figure 21: FDA new drug approvals median review time (in months), 1980–2022[165]

The United States should continue to explore possible reforms to streamline and accelerate clinical trial procedures, which will be important to consider as PDUFA comes up for reauthorization in 2027. Accelerating clinical trial timelines in the United States will require targeted reforms to regulatory processes that introduce delay without delivering commensurate gains in patient safety or scientific rigor. A central priority should be modernizing the investigational new drug (IND) process overseen by the FDA. Today, IND submissions often function as lengthy dossiers, even for early-stage studies, slowing trial initiation and increasing costs. The FDA should reorient the IND toward a high-level, risk-based document focused on essential safety information and establish a notification-based pathway for lower-risk studies, similar to Australia’s Clinical Trial Notification system, allowing sponsors to begin trials following Institutional Review Board (IRB) approval and notification. The agency has begun moving in this direction through a proposed Expedited IND pathway for certain Phase 1 trials, which would allow sponsors to rely more on existing preclinical data and reduce duplicative and time-consuming steps.[166] This approach would place greater reliance on IRBs to oversee early-stage trials and could be complemented by efforts to modernize IRB processes, including reducing administrative burden, improving review efficiency, and paying reviewers instead of relying solely on volunteers. Requiring a single, centralized IRB for multi-site trials would further help reduce duplicative review and avoidable delays.

Without reforms to clinical trial processes, the United States risks ceding a critical stage of the innovation pipeline; with them, it can accelerate time to proof of concept and retain a larger share of global R&D activity.

The United States could also increase the use of AI to improve clinical trial efficiency. Patient recruitment remains a major bottleneck, frequently delaying studies and increasing costs, with approximately 20 percent of trials failing to recruit the required number of participants. AI tools can identify eligible patients from electronic health records, optimize trial design, and predict high-enrollment locations. For example, Johnson & Johnson has used AI-driven platforms to improve site selection and recruitment efficiency.[167] More broadly, AI-enabled approaches can accelerate enrollment and improve the representativeness of trial populations.

These reforms are increasingly urgent from a competitiveness perspective. Early-stage clinical research is becoming more mobile, with phase I trials increasingly shifting to Australia and proof-of-concept studies increasingly conducted in China. In some cases, access to faster early-stage pathways has been decisive for whether new therapies receive funding. The United States should respond by reducing regulatory and administrative friction across the trial life cycle, including reforming policies that discourage patient participation, such as limits on compensation and gaps in coverage of trial-related costs. Without these changes, the United States risks ceding a critical stage of the innovation pipeline; with them, it can accelerate time to proof of concept and retain a larger share of global R&D activity.

Robust Intellectual Property Rights

Given the time, expense, and uncertainty that accompanies biopharmaceutical innovation, IP rights such as patents, exclusivities, and trade secrets are essential to incentivize innovators to undertake the risky and difficult proposition of life sciences innovation. This section briefly touches on several IP issues U.S. policymakers must get right in order to continue to ensure America leads in biopharmaceutical innovation.

The Bayh-Dole Act of 1980 created a framework for public-private collaboration, allowing universities to patent and license inventions arising from federal grants and becoming one of the most successful technology-transfer laws in history.[168] However, despite Bayh-Dole’s success, in recent years, some policymakers have sought to reinterpret one provision of the act: march-in rights, which allow the government, under limited circumstances, to require patent holders to license their inventions to others.[169] Recently, policymakers have asserted that march-in rights grant the government authority to regulate drug prices, although the law’s authors made clear that the authority was intended instead to ensure that inventions are actually developed and commercialized. The architects of the legislation, Senators Birch Bayh and Bob Dole, explicitly rejected the idea that march-in rights should be used to ensure “reasonable prices,” and the statute contains no such language.[170]

Despite this, proposals have emerged to use march-in rights as a drug-price control mechanism. For instance, the Biden administration floated draft guidance in 2023 that would have permitted governmental use of march-in rights on the basis of the resulting price of a product (though fortunately, it ultimately did not finalize the policy).[171] But weakening the certainty of access to IP rights provided under Bayh-Dole by employing march-in to address drug pricing issues—especially if doing so would give government entities the authority to walk in and retroactively commandeer innovations that private-sector enterprises invested hundreds of millions, if not billions, to create—would significantly diminish private businesses’ incentives to commercialize products supported by federally funded research.[172]

The first Trump administration directed the National Institute of Standards and Technology to review federal policies aimed at bolstering the return on federal R&D investments. That review reaffirmed that march-in rights both are a last resort and had never been used since the act’s passage to control prices.[173] NIH similarly determined that using march-in rights to control drug prices “was not within the scope and intent of the authority.”[174] Fortunately, the second Trump administration has signaled no plans to use march-in rights for this purpose. In January 2025, Department of Health and Human Services (HHS) Secretary Robert F. Kennedy Jr. stated that employing march-in rights to lower drug prices “would not be an appropriate use of march-in rights.”[175] Policymakers should continue to reject calls for the use of Bayh-Dole march-in rights to artificially control drug prices.

Related to this, some have called for misusing Section 1498 of the U.S. code, claiming it gives the government a right of eminent domain in all U.S. patents and, thus, the power of compulsory licensing over those patents. For instance, the civil society organization Public Citizen in February 2026 called on HHS to use Section 1498 to compulsorily license IP related to GLP-1s (glucagon-like-peptide-1 receptor agonists) in order to control the cost of weight-loss drugs.[176] The advocates sought to use Section 1498 to lower drug prices by asking the government to authorize a generic company to manufacture copies of the patented GLP-1 invention, presumably get those copies approved by the FDA, and then sell them at a low price for the government’s use. But this misreads (and indeed turns on its head) the entire intent and purpose of Section 1498.

Section 1498 states the following: