Canada's Missing R&D Firms

Ask a Canadian policymaker about innovation, and they will proudly point to more federal innovation programs than you can count, the world’s first national AI strategy, and perhaps how Canada is second only to the United Kingdom in scientific publications per capita. But ask where the firms are, and Canada is largely absent from the global league of companies that turn research into products and services at scale.

ITIF recently analyzed the EU Industrial R&D Investment Scoreboard, which tracks the top 2,000 corporate R&D investors and accounts for roughly 90 percent of global business R&D. Canadian firms accounted for just 1 percent of global advanced industry R&D in 2024: US$7.3 billion, or US$3.27 per $1,000 of GDP, compared with a global average of US$11.73 and the U.S. figure of US$23.48. Canada's top firms invest in R&D at one-seventh the rate of their American counterparts.

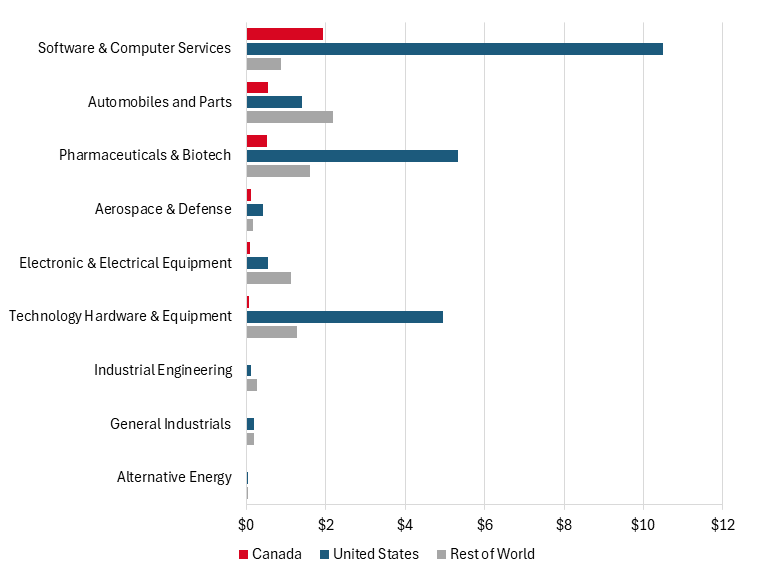

The gap runs across the full range of advanced industries. Canada sits far below both the United States and the rest of the world (the 43 other countries hosting firms in the Scoreboard) in eight of the nine advanced sectors measured in the Scoreboard. (See figure 1.) Moreover, in alternative energy, general industrials, and industrial engineering, not a single Canadian firm appears among the top global R&D investors. Software is Canada's strongest category, but even there it remains well below the U.S. level. Pharma and autos are present, but marginal.

Figure 1: Canadian, United States, and rest-of-world R&D per $1,000 of GDP in advanced industries, 2024

Rest of world: Scoreboard countries excluding Canada and the United States.

Rest of world: Scoreboard countries excluding Canada and the United States.

The gap is not evenly distributed across firm size. Global business R&D is heavily concentrated at the top of the Scoreboard: The top 50 firms account for 44 percent of total R&D among the 2,000 companies tracked, and the top 200 account for 67 percent. Canada has one firm in the top 200, Constellation Software. Shopify sits at 201. Every other Canadian firm is further down the list.

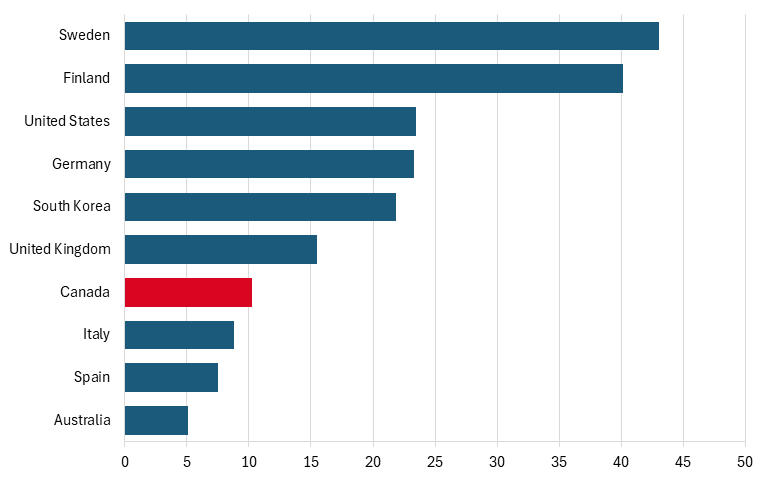

The country is not short of firms doing some R&D. Roughly 23,000 firms filed claims under the Scientific Research and Experimental Development (SR&ED) tax incentives in 2025, and yet only 23 Canadian firms appear in the global top 2,000 R&D performers. Even on that broader measure of firm count rather than size, Canada ranks 24th of the 45 countries with any Scoreboard presence, hosting 10 Scoreboard firms per trillion dollars of GDP. (See figure 2.) And those 23 firms spend less on R&D than the Scoreboard average: They account for 1.15 percent of Scoreboard firms but only 0.59 percent of Scoreboard R&D spending.

Figure 2: Number of firms in the global top 2,000 R&D performers, per trillion USD of GDP, 2024

The countries above Canada in the chart are the economies that host large R&D-intensive firms: Sweden, Finland, the United States, Germany, South Korea, and the United Kingdom. The countries below are Italy, Spain, and Australia, advanced economies with known R&D weaknesses. On this measure, Canada sits among its structural peers, not the economies it aspires to resemble.

A wide base of small R&D performers cannot anchor the ecosystems that drive sustained R&D growth—the research absorption, specialized talent, supplier anchoring, and domestic reinvestment needed to reach industrial weight. Raising R&D broadly across small and mid-sized firms can improve individual capabilities, but it cannot substitute for the scale at which most corporate R&D is concentrated.

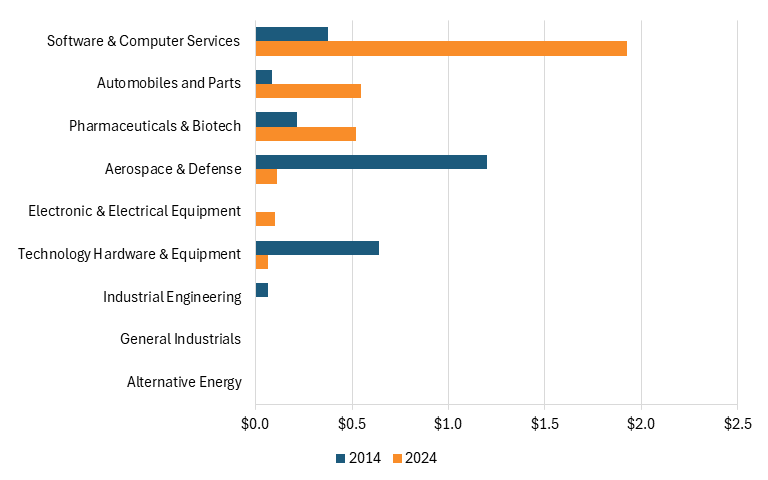

This is not just an unlucky one-year snapshot, but a structural pattern over the past decade in which Canada’s position has barely improved. (See figure 3.) Between 2014 and 2024, Canadian advanced industry R&D intensity rose from US$2.58 to US$3.27 per $1,000 of GDP, a gain of 69 cents. The United States gained US$8.07 over the same period, and the rest of the Scoreboard countries gained US$1.65. Canada did not close the gap with its peers; the gap widened, both in absolute and relative terms.

Figure 3: 10-year change in Canadian R&D per $1,000 of GDP in advanced industries

Software grew meaningfully, from $0.37 to $1.92 of R&D per $1,000 of GDP. The gain is concentrated in three firms: Constellation Software, Shopify, and Open Text, which together account for roughly $3 billion of R&D spending, more than Canada's entire Scoreboard total in 2014, even after adjusting for inflation. Autos and pharma also rose, albeit from low bases. But those gains were largely offset by a collapse in the aerospace sector.

Aerospace fell from $1.20 to $0.11 per $1,000 of GDP, and Bombardier's exit from commercial aviation between 2018 and 2020 accounts for virtually the entire decline. In 2014, Bombardier was the single largest R&D performer in Canada, ranked 76th globally and spending $2.6 billion in 2024 dollars, roughly a quarter of all Canadian advanced industry R&D that year. After a financing crisis and a trade dispute with Boeing, Bombardier sold its C Series program to Airbus and retreated to business jets. By 2024, its R&D spending had fallen to $125 million, and Canada went from having a globally significant aerospace R&D performer to having none. Nothing has filled that gap since: Canada had one firm in the global top 100 in 2014, and none by 2024.

Canada is underrepresented in global business R&D, and that gap has barely narrowed over a decade. The following reforms would change the conditions under which Canadian firms invest in R&D at scale:

1. Reform SR&ED to stop penalizing scale and start rewarding growth. SR&ED’s enhanced rate is designed for small, privately held Canadian firms (CCPCs), and the structure penalizes growth in two ways. First, firms that scale up lose eligibility if they go public or take on significant foreign investment. Second, firms that grow their capital base phase out of the enhanced rate before they reach the size where R&D actually compounds. Removing the enhanced rate and using the savings to raise the base rate for all firms would stop penalizing firms for growing.

2. Build sector strategies around existing footholds. Software is the one sector where Canada gained ground. Autos and pharma are small but present. Each foothold sector needs a roadmap identifying where Canadian firms sit in global value chains, where scale-up stalls, and what mix of procurement, regulation, capital, and private-sector demand pull would change the trajectory. The zero-presence sectors require a different lens: enabling adoption and building linked capabilities rather than expecting domestic R&D champions to appear from nothing.

3. Tie university research funding more closely to downstream commercial results. Canada’s universities produce plenty of research. What they do not produce often enough are the patents, spinouts, and industry links that help turn that research into firms that scale. Public funding for research-intensive universities should reward commercialization outcomes, not just academic activity, so institutions have a reason to care whether their research generates economic capacity in Canada. Universities that respond to these incentives would produce more spinouts and more licensed technologies, but those firms still need patient capital, anchor customers, and time to reach the size where R&D compounds. The upstream incentive is necessary, not sufficient.

Until policy is reoriented around scale, Canada will keep producing research without producing enough firms that can commercialize, reinvest, and compete globally.

Editors’ Recommendations

September 25, 2023

Comparing Canadian and U.S. R&D Leaders in Advanced Sectors

May 28, 2024

The Untapped Technological Patent-ial of Canada

Related

December 18, 2023