Internal Value Chains Remain Dependent on China Even as Multinationals Shift Production to America

Advanced manufacturers based in East Asia are expanding investment into the U.S. economy. Yet, many of their internal value chains remain anchored in China, giving the PRC significant leverage over U.S. interests. U.S. policymakers should respond both defensively and offensively.

KEY TAKEAWAYS

Key Takeaways

Contents

Case Study Evaluations of China-Plus-One in the AI Economy 16

Introduction

The primary arena of U.S.-China competition today is industrial.[1] In the techno-economic-trade war, American and Chinese firms compete in global markets amid a backdrop of Schelling-style economic warfare.[2] Longstanding PRC cyber and economic espionage on industry is pulling firms into this conflict, whether they are prepared for it or not.[3] And U.S. and PRC policymakers deploy sanctions, export controls, and control over key commodities as chokepoints.[4] In his recent book Chokepoints, Edward Fishman wrote that “economic warfare, now a baseline feature of our world, will permeate other areas of foreign policy, global economics, domestic politics, and business.”[5]

This report supplies evidence that the next area U.S.-China economic warfare will permeate into is China’s leverage over non-American multinationals’ internal value chains. Over the last decade, U.S. firms have recognized their exposure to China and have taken at least some steps to reshore production, decrease their investments in China, and secure their supply chains.[6] Similarly, U.S. policy has emphasized de-risking first-degree dependence on Chinese supply chains in recent years, but less so second-degree dependence through allied nations’ multinationals.[7] Yet East Asian multinationals with longstanding investments in China have been slower and less able to reduce their PRC regulatory, market, and dependence risks.[8]

This reality is unchanged by U.S. policymakers’ attempts to reshore and increase foreign direct investment (FDI) following decades of offshoring. The Biden and second Trump administrations have sought to bring back advanced manufacturing to the United States through industrial policy and trade pressure. While inward FDI announcements have led to the perception that such investment strengthens U.S. independence from China, the reality is that the internal value chains of many advanced manufacturing multinationals are deeply anchored in China and not easy to relocate. These include accumulated manufacturing process know-how, talent, and IP.

If U.S. reshoring success is defined by the ability to sustain power industry value chains, protect advanced manufacturing know-how, and maintain operational resilience in the event of a future potential U.S.-China decoupling event, then this report argues that most existing approaches fall short.

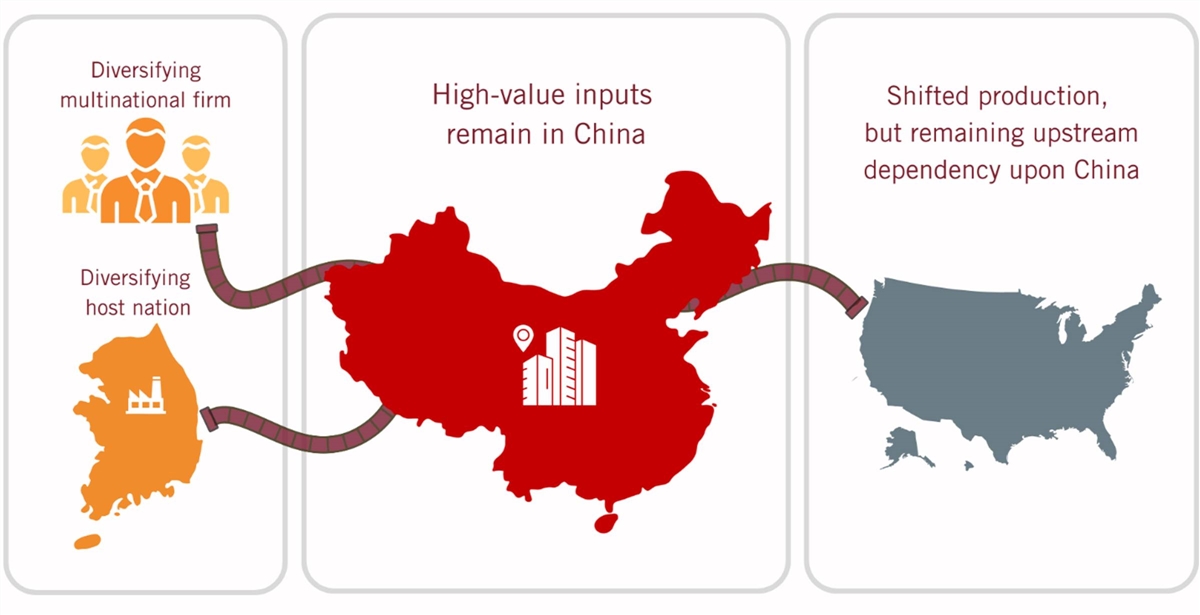

This dependency is a chokepoint, which Trinh Nguyen in her review of Fishman’s Chokepoints defines as “non-substitutable domains dominated by a single state or small coalition.”[9] The PRC could—and likely will—weaponize this chokepoint against the United States, just as it has weaponized its chokepoint of rare earth mining, processing, and refining.[10] U.S. policymakers have been slow to realize this vulnerability, partly due to the recent flurry of greenfield inbound investment announcements. However, many of these deals will relocate some production without reducing dependence on China for the most valuable parts of firms’ supply chains, thereby falling short of “securing America’s technological and industrial leadership,” as one recent trade deal touted.[11] Conversely, the PRC has explicitly allowed geographic dispersion of production so long as control over key links in value chains remain anchored inside China.

This report examines recent U.S. inbound investment through this lens. Focusing on three case studies—Taiwan’s Inventec, Japan’s Resonac, and South Korea’s LS Cable & System (LS C&S)—it traces how multinational firms critical to U.S. industrial goals have diversified geographically but retained higher-value capabilities and significant risk in China. To be clear, none of these firms have deliberately harmed either American or their home nation’s interests. In most cases, they have made the best decisions available based on global regulations and business incentives.

For U.S. policymakers, the question should not be whether the United States should welcome inbound investment from non-Chinese firms with China dependency. It should. The question should be how the United States defines success when it receives such investment. If success is measured primarily by capital inflows, job counts, or production capacity, then many recent inbound investments are successes. If success is defined by the ability to sustain power industry value chains, protect advanced manufacturing know-how, and maintain operational resilience in the event of a potential U.S.-China decoupling event, then most existing approaches fall short.[12]

Policymakers can and should take more defensive and offensive measures against potential PRC weaponization of multinationals’ dependence on China. Defensively, U.S. policymakers should redefine success regarding China-Plus-One and attempt to build what that success looks like into U.S. strategy on inbound investment, supply chains, and economic security. Offensively, policymakers should proactively work with multinationals and their home countries to wrest back value chain independence from China wherever possible. How U.S. policymakers address multinationals’ dependence on China will shape the next phase of industrial competition with China and determine whether these same firms’ new greenfield investments in the United States contribute meaningfully to long-term competitiveness against China.

The China-Plus-One Strategy

The PRC’s ability to wield leverage over multinationals’ China-dependent internal value chains is best understood under the framework of “China-Plus-One,” a supply chain management (SCM) strategy in which a firm retains substantial production capacity in China while shifting production to at least one other country to reduce risk.[13] The term originated in early-2000s Japan as a public-private risk-management response to rising costs and political uncertainty for Japanese businesses operating in China.[14] Operating under a China-Plus-One strategy, a firm can theoretically hedge against regulatory and institutional risks in China while avoiding full offshoring in order to preserve access to China’s market, talent, and industrial ecosystems.[15]

The most recent wave of China-Plus-One has featured more global diversification, as evidenced by permutations of the original strategy such as China-Plus-Two, China-Plus-Many, China-And-Many, and China-Plus-N.[16] As the China-Plus-One concept spread from Japan to the United States in the 2010s, multinationals tended to shift production from China to Southeast Asia or India in search of lowered risk and labor costs.[17] Yet, in the 2020s, the United States has emerged as a Plus-One recipient economy due less to China risk and more to U.S. tariffs, industrial policy incentives, threats of punitive action, and corporate hedging in U.S.-China competition.[18]

In addition to these geographic shifts, China is no longer simply a low-cost labor-intensive manufacturing hub and has emerged as an innovative techno-economic power with aspirations to globally dominate power industries, which are advanced industries that underpin 21st century national power.[19] China has arrived at this point in part through PRC strategy and its natural economic strengths. Yet, another factor has been technology transfer—both through legal auspices and through PRC economic espionage—from multinationals, especially those with significant operations in China.[20] As China has steadily climbed up the value chain ladder, it has cultivated multinational dependence on its market and industrial ecosystem along the way.[21]

Now as a Plus-One recipient economy, the United States has not fully adapted to this reality. Industrial policy programs such as the CHIPS and Science Act (CHIPS Act), the Inflation Reduction Act (IRA), and the Stargate Project have focused primarily on where and what new capacity is built, rather than the degree to which the new capacity meaningfully decreases China dependence. As The Asia Group has noted, tariff uncertainty has altered firms’ investment calculus, in some cases incentivizing U.S.-based production to preserve market access, even where high-value China-based dependencies remain intact.[22]

In practice, China-Plus-One has increased geographic diversification of production without meaningfully decreasing supply chain dependency on China.

The result is investment that has somewhat expanded U.S. domestic capacity while leaving the most strategic parts of multinationals’ internal value chains and underlying dependency anchored in China. In general, China-Plus-One investment benefits the United States, as every dollar moved out of China—whether it ends up in India or the United States—can weaken the PRC’s industrial leverage at the margin. Yet, in practice, China-Plus-One has increased geographic diversification of production without meaningfully decreasing supply chain dependency on China.

This gap is especially consequential because the United States relies heavily on foreign multinationals—particularly from Taiwan, Japan, and South Korea—for advanced manufacturing that underpins U.S. national power.[23] These firms are indispensable partners for the United States. They are also among the most sophisticated practitioners of China-Plus-One strategies, with longstanding operational ties to China’s manufacturing and talent ecosystems.

Origins of China-Plus-One

“China-Plus-One” originated in Japan as an academic, industry, and government term for diversifying supply chains beyond China. As early as 2002, the Japan Machinery Center for Trade and Investment (JMC)—the foremost industry association representing Japan’s machinery sector—warned Japan’s government that its member companies were increasingly facing risks with their dependence on China’s economy.[24] JMC described Japanese investments in China as having “already gone beyond the mere relocation of production functions, extending to R&D [research and development], procurement, and sales functions.”[25]

JMC wrote that “in China, as industrial clusters develop and activities such as procurement, production, and sales become increasingly self-contained within China, all profits of Japanese companies shift to their Chinese subsidiaries.”[26] According to JMC, this and other dependencies highlighted institutional risk, as China’s “system remains opaque, and in many cases investigations and adjustments are conducted in ways that are inconsistent with international rules or are arbitrary.”[27] Presciently, JMC warned that if Japan’s government did not to pay attention to the risks of over-extending Japanese supply chains to China, the consequence would be no less than “the deterioration or hollowing-out of Japanese headquarters’ functions.”[28]

Although JMC did not explicitly mention China-Plus-One, its warning laid the groundwork for the China-Plus-One strategy that emerged shortly thereafter in reaction to the newly realized risks of making China a production base. By 2003, Japanese policymakers and academics had begun using the term China-Plus-One.[29] That year, Kayoko Kitamura, the then-director of the Japan Society for International Development, published a commentary titled “China-Plus-One: Which country will be chosen?” in the government-affiliated Japan External Trade Organization’s business journal.[30] The concept took root and throughout the 2000s, many Japanese companies began to diversify away from China toward Southeast Asia, as well as to explore India as a potential investment hub, in many cases directly citing China-Plus-One as their strategy.[31]

The 2008 RAND report “Pacific Currents: The Responses of U.S. Allies and Security Partners in East Asia to China’s Rise,” summarized Japan’s governmental view of China-Plus-One as a message of complementarity: “China has great promise as both a market and a production base, but business should hedge its bets against overexposure.”[32] The historical record shows that Japan’s conception of the China-Plus-One strategy was aimed to reduce exposure to China-related shocks, but it was never designed to fully prevent against China dependence.

Recent U.S. Reshoring and Tariff Policies Fail to Address China Dependency Risk

Following China-Plus-One’s origins as a public-private hedge against overexposure to China in Japan, the term became a global industry SCM trend in the 2010s.[33] The concept has also influenced policy globally. While governments around the world rarely use China-Plus-One officially, they apply the SCM framework to trade and industrial policy. For example, South Korea’s 2026 Framework Act on Supply Chain Stabilization for Economic Security set a quantitative target to reduce import dependence on any single country for key items to below 50 percent by 2030.[34]

In the U.S. context, policymakers have evaluated China-related supply-chain risk through language such as reshoring, nearshoring, friendshoring, economic security, de-risking, and supply chain stabilization.[35] While these concepts overlap, they are not synonymous, and their conflation has obscured whether current policies meaningfully address upstream China-supply-chain dependence in national power industries.[36] For example, the Biden administration promoted the CHIPS Act as a measure to “strengthen supply chains and counter China,” and included guardrails preventing subsidy recipients from expanding certain semiconductor facilities in China.[37] However, the program had comparatively little to say about the degree of subsidy recipients’ reliance on upstream China-based inputs, materials, tooling, and components.[38]

Stargate Project has reflected this same pattern. With the backing of the Trump administration, OpenAI has framed Stargate Project as an effort that “will not only support the re-industrialization of the United States but also provide a strategic capability to protect the national security of America and its allies.”[39] Yet, the initiative’s request for proposals did not require any disclosures or information regarding applicants’ upstream China dependency, despite requesting full transparency for corporate and compute ownership.[40]

As academics Laura Alfaro and Davin Chor argued in a 2023 analysis of recent U.S. efforts to reconfigure global value chains through friendshoring, nearshoring, and FDI, “it is unclear if these measures will reduce U.S. dependence on supply chains linked to China.”[41] Answering the question of what share of recent U.S. inbound investment is China-dependent from a macroeconomic standpoint is difficult, especially since FDI announcements do not always translate into actual capital flows, or do so very slowly.[42] Given these limitations, this report approaches the question primarily from a microeconomic and firm-level perspective, using case studies to assess how China-Plus-One operates in practice.

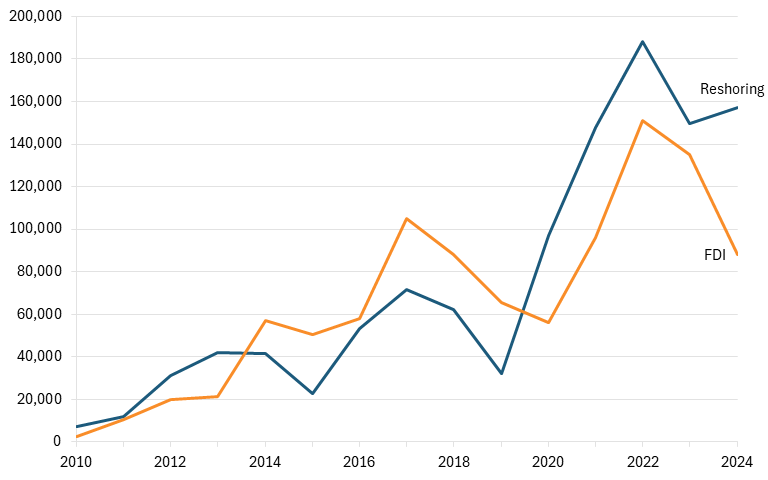

Still, what is clear is that U.S. inbound investment job announcements have significantly risen in recent years.[43] As seen in figure 1, the Reshoring Initiative, which measures corporate job announcements to look at the quantity and makeup of reshoring and FDI in the U.S. economy, has found that both reshoring and FDI job announcements have increased over the last decade, with FDI job announcements reaching a high of 154,409 jobs in 2022. Since 2022, FDI job announcements have continued to make up a large share of total reshored and FDI job announcements, but both types of job announcements have fallen off in recent years following 2022’s IRA and CHIPS Act.[44]

Figure 1: Reshoring and FDI job announcements in the United States, 2010–2024[45]

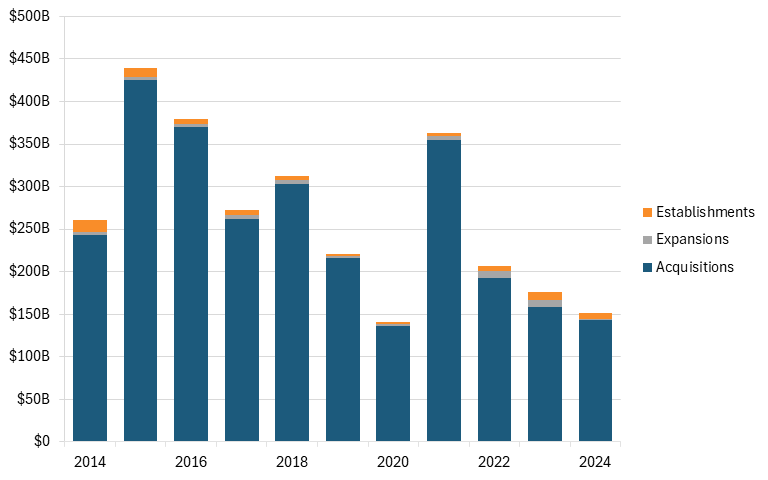

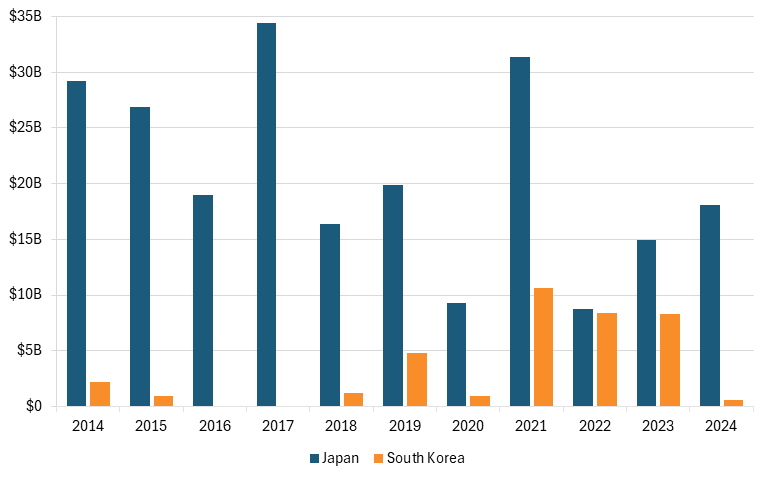

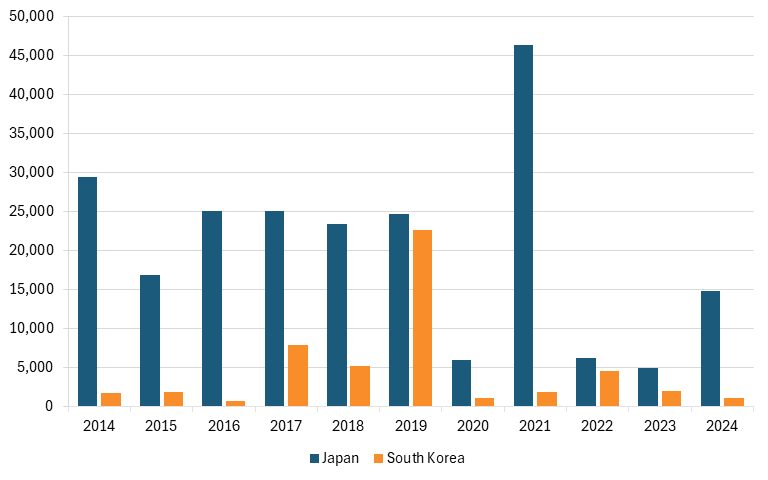

However, as seen in figure 2, most FDI over the last decade has come in the form of acquisitions rather than establishments or expansions. Japan is the largest FDI contributor to the United States, with one academic estimate stating that Japan accounts for close to 15 percent of the stock of all U.S. inward FDI.[46] Beyond Japan, in terms of other East Asian allies (data on Taiwan’s FDI is limited), South Korea has also been a steady FDI contributor, both in terms of first-year expenditures as well as current employment associated with new FDI in the U.S. economy over the last decade, as seen in figure 3 and figure 4.

Figure 2: Total FDI investment by type, 2014–2024[47]

Figure 3: First-year U.S. expenditures from Japan and South Korea, 2014–2024[48]

Figure 4: Japan and South Korea, current employment associated with new U.S. FDI , 2014–2024[49]

The second Trump administration’s tariffs are similarly unlikely to mitigate China-dependency risks. As World Bank researchers found in a study of U.S. trade flows from 2017 to 2022, specifically looking at U.S. tariffs’ effect on diversification away from Chinese supply chains, “the reorientation of trade is consistent with a ‘China + 1’ strategy, as opposed to diversified sourcing across multiple countries.”[50] The authors concluded that “to displace China on the export side, countries must embrace China’s supply chains.”[51] In other words, U.S. tariffs have often shifted production to alternative countries that remain deeply integrated in China’s supply networks. While this has somewhat reduced U.S.-China bilateral trade exposure, it has not meaningfully reduced systemic dependence on China.

How to Evaluate Success in China-Plus-One

In a 2011 article, business scholar Peter Enderwick characterized China-Plus-One as a balanced win-win-win paradigm for three stakeholders. As he wrote:

A China-Plus-One strategy appears to be beneficial to both firms that seek to pursue it for reasons of risk diversification, cost reduction or avoidance of overreliance on China, for China in that it frees up resources which can be applied to other higher value activities, and for Plus-One host economies which gain the benefits of inward investment.[52]

Enderwick’s framework is useful, but reflects the optimism of Globalization 1.0, in which most policymakers and academics still believed China was converging toward market norms and discounted the risk of nations being protectionist toward their markets and firms.[53] While Enderwick acknowledged risk from China’s “variability in government policy and in particular, attitudes towards foreign business,” he did not account for China’s explicit use of industrial policy to capture market share.[54] Enderwick also omitted firms’ host countries as a stakeholder.[55]

Updating Enderwick’s framework for 2026 requires three additional components:

1. China’s possession of chokepoints in the form of multinationals’ internal value chain dependencies

2. The backdrop of U.S.-China techno-economic-trade war in which gains for one stakeholder may directly undermine another

3. The addition of diversifying multinationals’ host nations as additional actors in the paradigm, with occasionally differing strategic priorities than the firm’s choices

Figure 5 updates Enderwick’s framework for situations in which the United States is the Plus-One recipient economy and the diversifying firm is an advanced manufacturer. The conception rightfully places China at the center of the China-Plus-One framework. China, not the United States—nor the diversifying firm or its host nation—holds the most leverage in the paradigm. In most cases, this framework is not a mutual win. Instead, it tends to result in a win for China, a mixed picture for the diversifying firm and its host nation, and a loss for the United States.

Figure 5: An updated conception of Enderwick’s China-Plus-One framework for 2026

How the United States Wins in China-Plus-One

The United States wins as the recipient economy of China-Plus-One firm-level diversification when inbound investment contributes to a Globalization 2.0 strategy.[56] This means that inbound investment prioritizes advanced industries and leads to technology transfer of critical IP and manufacturing processes, creating both supply chains resilient to geopolitical shock and alignment with allied production ecosystems.[57] Most foreign investment in the United States within the last two administrations fits most of these criteria.

However, there is one more criterion. In high-fixed-cost sectors such as semiconductors, AI infrastructure, and aerospace, competition with China is structurally winner-take-most.[58] As the Information Technology and Innovation Foundation (ITIF) has observed, China’s use of subsidies, closed markets, and nonmarket practices allows it to capture market share that would likely otherwise be won by more genuinely innovative foreign competitors.[59] Every sale of a single-aisle passenger jet China’s state-owned COMAC makes is one less sale for Airbus or Boeing.[60] In this context, U.S. success should be evaluated relative to China’s success, not in isolation. Therefore, a China-Plus-One outcome in which China retains control over key inputs, standards, or ecosystems, while final assembly or lower-value processes shift to the United States, cannot be considered a U.S. “win.”

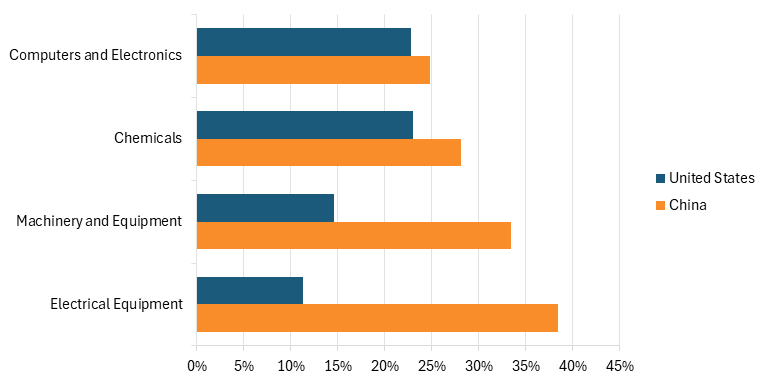

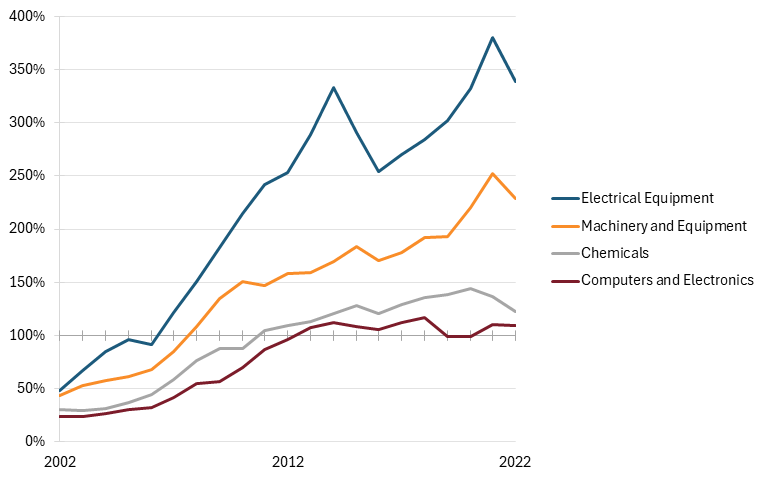

In industries to which the United States is welcoming significant East Asian inward FDI, such as electrical equipment, machinery, computers and electronics, and chemicals, China is already well ahead of the United States globally.[61] The PRC has prioritized industries such as semiconductors, data-center infrastructure, specialty chemicals, critical minerals, and undersea cables in industrial policy plans such as Made in China 2025, and wants to occupy critical positions in global supply chains of these sectors.[62] Sectoral output figures show that China captured global shares of value-added output between approximately 25 and 39 percent of these industries by 2022, and largely increased its lead in global shares over the United States between 2002 and 2022, as seen in figure 6 and figure 7.[63]

A China-Plus-One outcome in which China retains control over key inputs, standards, or ecosystems, while final assembly or lower-value processes shift to the United States, cannot be considered a U.S. “win.”

Figure 6: U.S. global shares of selected advanced industries versus Chinese shares, 2022[64]

Figure 7: China’s increasing global market share in select advanced industries relative to the U.S. global share[65]

Yet, there is hope for the United States. These figures show output and quantity, not value or quality within these sectors. For the United States, winning in China-Plus-One means ensuring that critical IP, manufacturing processes, and infrastructure can be sustained on U.S. or allied soil in case of any exogenous geopolitical event that would leave the United States and China decoupled. Within the China-Plus-One paradigm, the United States does not need to dominate every node of the value chain, nor far outpace China in global share of output. But at a minimum, it should strive to match China’s capabilities in the segments that determine control, standards, and scalability rather than competing primarily for final assembly or downstream capacity.

How China Wins in China-Plus-One

The PRC does not view China-Plus-One dispersion as a neutral business decision decided by market forces and instead views it as a supply chain security risk requiring active management. The PRC’s approach in this regard rests on two core principles. First, China’s government recognizes that some degree of supply-chain migration out of China is inevitable, whether due to Chinese firms expanding overseas or multinational companies attempting to implement China-Plus-One strategies. In 2023, Chinese president Xi Jinping remarked in a speech that “currently, the global industrial system and supply chains are characterized by diversification.”[66] Xi added that economic and historical trends are shaping this trend in a way that “proceeds independently of individual will.”[67]

Second, China’s government recognizes that not all parts of a value chain are equally important. Speaking at the fifth plenary session of the 19th Communist Party Central Committee, held in 2020, Xi Jinping stated, “Even when relocating operations abroad, every effort must be made to retain key segments of the supply chain domestically.”[68]

While this statement was aimed at Chinese firms, reflecting concern over industrial hollowing out, it shows PRC recognition of quality’s importance relative to quantity in value chains. Xi additionally articulated the recognition that supply chains create chokepoints in a 2016 speech, warning that “[when] core technologies are detached from their industrial chains, value chains, and ecosystems, and when upstream and downstream links are broken, even [major research and development] efforts may go to waste.”[69] Together, these statements show a consistent view that strategic value comes from maintaining control over the highest-value inputs and processes in global value chains that connect R&D to production and commercialization.

As a result, China is highly defensive of its own highest-value supply chain inputs. In March 2025, Wang Lizong, a member of the National Committee of the Chinese People’s Political Consultative Conference (CPPCC) and president of the Guangdong High-Tech Industry Chamber of Commerce, said that “it is necessary to clarify which industrial chains and specific links can be established overseas, and which should be strictly controlled for relocation.”[70]

For foreign multinational enterprises, China’s approach is less defensive and more opportunistic. The PRC sees foreign firms’ investment in China as reinforcing China’s position at the center of global supply chains. In a February 2025 commentary, CPPCC member Zheng Yali wrote that international cooperation on industrial and supply chains can “promote the dissemination of China’s technical standards and rules,” and that success in this area would “form an orderly international division of labor chain with China as the mainstay,” or in other words, make China the central node in global value chains.[71]

Even as some multinationals pursue China-Plus-One strategies, the PRC attempts to leverage its advantages as a manufacturing and export base to retain their integration. Reporter Yan Lanfei of the International Business Daily—a newspaper sponsored and published by the PRC’s Ministry of Commerce—observed in 2024 that “even companies adopting a ‘China-Plus-N’ supply chain strategy prioritize stabilizing and strengthening their presence in China.”[72] Chinese policymakers and academics often use “stickiness” as a term of art to refer to the strategy of retaining multinationals’ integration in China’s supply chains. For example, Zhou Xiaoyong, a professor at Xi’an Jiaotong University who has had over 20 policy recommendations adopted by the PRC, recommended in 2024 that China “enhance the stickiness of supply chains” and “continuously strengthen the connection between [China’s] industrial chains and international ones.”[73]

China wins in China-Plus-One not by preventing supply chain diversification, but by shaping its terms. Beijing accepts that production will disperse geographically, yet works to retain control over high-value technological chokepoints. At the same time, the PRC actively encourages certain foreign multinationals to deepen their integration into China’s industrial ecosystem, creating supply chain stickiness so that China preserves its position as the central node in global supply chains.

How a Diversifying Firm Wins in China-Plus-One

A diversifying firm that chooses to pursue a China-Plus-One or China-Plus-Many strategy makes its choice based on an individual SCM and risk-management strategy as informed by geopolitical conditions but does not make its choice solely due to geopolitics. Firms win when diversification improves both short-term performance and long-term strategic resilience. As a result, successful China-Plus-One diversification is less to do with abandoning China than hedging concentration risk while protecting prior sunk-cost advantages.

In the short term, diversifying firms win when diversification delivers tariff mitigation, regulatory compliance, investor reassurance, or access to new pools of capital or subsidies. These benefits are often financial and immediate, making China-Plus-One attractive even when deeper structural risks remain unresolved.

In the long term, diversifying firms win if diversification supports durable market expansion, global competitiveness, or other strategic bets that pay off over time. For most multinationals, this means balancing new capacity outside China with continued engagement inside China, and preserving access to the Chinese market and the ecosystem advantages accumulated over decades of investment. Firms that overcorrect by exiting China too aggressively risk forfeiting scale efficiencies, supplier relationships, and participation in China’s increasingly strong science and technology talent pool that justify their original China-centric manufacturing strategies.[74]

How a Diversifying Firm’s Host Nation Wins in China-Plus-One

For host nations of firms undertaking a China-Plus-One strategy, specifically U.S. allies or partners, China-Plus-One creates a complex set of tradeoffs, with three simultaneous challenges.

First, the host nation must balance its economic and diplomatic relationships with both the United States and China. Among other incentives, China offers manufacturing ecosystem depth and cost advantages, while the United States offers security alignment and market access.[75] Second, host nations play a role in bridging institutions across two increasingly incompatible techno-economic trade blocs. As U.S.- and China-centered ecosystems diverge in standards, technology stacks, and security requirements, host nations’ firms operating across both face rising compliance, coordination, and political costs.[76] Third, policymakers often lack visibility into how exposed their domestic firms are to China, making it difficult to assess whether overexposure poses strategic risks.

Altogether, a host nation partially wins when its firms can maintain operational flexibility across both blocs, capture value from U.S. and Chinese markets, and leverage government support to strengthen domestic industrial capabilities. In the longer term, host nations face the same techno-economic-trade threat from the PRC that the United States does in their own specialized industries, so their firms’ China dependence creates chokepoints that the PRC can weaponize.

Case Study Evaluations of China-Plus-One in the AI Economy

With a few exceptions, there is limited evidence on the degree to which multinationals are or become dependent on China across supply and value chains, or how they implement a China-Plus-One strategy. This section provides policymakers with case study evidence of these topics.

Methodology

This report’s case studies focus on AI infrastructure industries with high fixed costs, steep learning curves, scale-driven reinvestment, and potential for standards lock-in—or in other words, sectors wherein China-Plus-One decisions carry the greatest economic and strategic significance.

Three firms are examined:

1. Taiwan’s Inventec

2. Japan’s Resonac

3. South Korea’s LS C&S

All three of these firms meet the following criteria:

▪ Belong to advanced industries that underpin national power in the 21st century[77]

▪ Have deeply embedded manufacturing bases in China

▪ Are actively expanding investment in the U.S. economy as part of a China-Plus-One or China-Plus-Many strategy, with the United States as a Plus-One recipient

The evaluation considers three perspectives:

1. China: How dependent are these multinationals on China?

2. United States: Is the United States winning as multinationals invest into its economy?

3. Firms and host nations: How do firms and their host nations fare as multinationals execute China-Plus-One strategies?

This report draws its evidence from open source information, including corporate financial and sustainability statements and reports, Chinese, Japanese, and Korean language sources, and limited access to WireScreen’s China-focused business intelligence platform.

Inventec

Inventec is a Taiwanese contract manufacturing company that was listed at 1,831 in the 2025 Forbes Global 2000 ranking with a $4.44 billion market capitalization value.[78]

Inventec: China as the Manufacturing Base

Inventec’s manufacturing base is deeply anchored in China. As of 2023, approximately 60 percent of its production capacity was based there.[79] At Inventec’s 2023 shareholders’ meeting, executives said that the future proportion of production capacity outside China would increase close to 50 percent.[80] Inventec’s geographic shares of long-term assets such as property, equipment, and other long-lived investments appear to show that the company is indeed diversifying its global footprint, with a shrinking plurality of assets remaining in China and a growing majority of long-term assets outside the country, as seen in figure 8.[81]

Figure 8: Inventec’s long-term assets by geographic region, FY 2022–2023[82]

Inventec additionally has strong localization of IP in China through collaborations and partnerships. These initiatives likely provide the firm with a strong pipeline of IP, innovation, and talent. However, it is fair to question how much they help Inventec relative to its Chinese competitors and China’s contract manufacturing sector. In 2019, Inventec’s Tianjin-based subsidiary helped jointly establish the Industry 4.0 Center of the Nanjing Tsingyan Institute of Green Manufacturing.[83] The co-establisher of the Industry 4.0 Center was e-Works Manufacturing Information Technology, a Chinese contract manufacturer.[84] According to WireScreen, 16.1 percent of e-Works’s ownership can be traced back indirectly to PRC state entities.[85] Moreover, the Industry 4.0 Center’s stated goal is to “promote the transformation and upgrading of China’s manufacturing industry.”[86]

Similarly, in 2023, Inventec co-launched the Shunwei Technology Server R&D Center within the state-owned Chongqing Xiyong Microelectronics Industrial Park, along with Chinese contract manufacturer Guangzhou Trusme Electronic Technology.[87] Shunwei’s goal is to develop high-performance servers for cloud computing, edge computing, and AI use cases.[88] Yet, according to WireScreen, Trusme owns 80 percent of Shunwei, leaving just 20 percent to Inventec.[89] Additionally, Shunwei’s general manager was previously a Trusme executive.[90]

In terms of revenue, Inventec performs well in China’s market, especially in its AI server product line.[91] In June 2025, an Inventec executive stated that the company’s China market share had reached 25 to 30 percent for servers.[92] Inventec attempts to showcase its most “cutting-edge technologies” at expositions in China, which increasingly include AI servers and liquid cooling equipment that target China’s rapidly developing AI industry.[93] Inventec is well-placed to grow its market share moving forward, having entered into AI server supply chains for China’s biggest hyperscalers—Baidu, Alibaba, Tencent, and ByteDance—by early 2025, and in particular becoming Alibaba’s main server supplier.[94]

While these developments mean Inventec’s performance in China’s market is strong in the near term, they could lock Inventec more into China’s market in the long run. As TrendForce has reported, U.S. export controls on advanced chips have pushed Chinese hyperscalers to build proprietary AI stacks using domestic chips, interconnects, and system architectures.[95] These companies could in turn request Inventec to develop increasingly China-specific server designs and manufacturing processes that are not exportable.

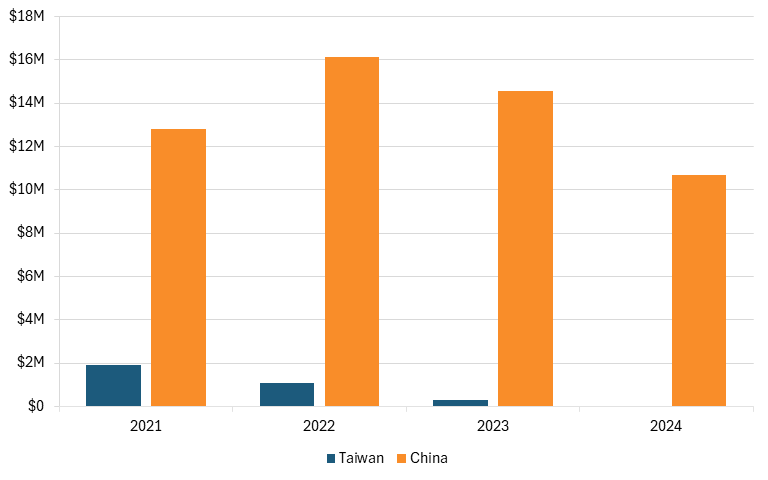

Through 2024, Inventec also received large and sustained subsidies from China’s government, as seen in figure 9.[96]

Figure 9: Inventec’s government subsidies from Taiwan and China, 2021–2024[97]

That support is helping Inventec automate and power its factories in China. In 2023, a Chongqing Daily journalist visited Inventec’s Chongqing-based subsidiary, located in the state-owned Western (Chongqing) Science City and as seen in figure 10.[98] According to the journalist, Western (Chongqing) Science City supported Inventec in “initiating an intelligent transformation and upgrade, advancing innovative development through non-hazardous raw materials, cleaner production processes, waste resource utilization, and low-carbon energy systems.”[99]

Figure 10: Inventec’s Chongqing-based subsidiary, 2023[100]

Inventec’s presence in China shows that the “China” component in China-Plus-One is not a passive legacy manufacturing base that can easily be shifted away, but rather an active, state-supported ecosystem that increasingly shapes firms’ capital allocation, technology development, and future market-orientation decisions.

Inventec: United States as a Plus-One Node

Inventec has had a long-standing supply chain diversification strategy that has gone hand in hand with the firm’s global expansion. In 2006, the firm opened a subsidiary in the Czech Republic to sell into the European market, and in 2007, it began operations in Mexico.[101] More recently, Inventec has diversified its supply chains more due to geopolitical factors. In the company’s 2024 annual report, Inventec’s highest-ranked risk was rising global trade protectionism and geopolitical risks.[102]

In interviews between President Trump’s election victory and inauguration, Inventec’s CEO, Jack Tsai, explained that Inventec would take a wait-and-see approach before deciding whether to build out production capacity in the United States or instead use one of Inventec’s many global locations to avoid high tariff costs.[103] In its 2024 annual report and based on other comments from Tsai, Inventec had stated that “[in order] to counter U.S. trade protectionism, [Inventec] is actively evaluating plans to establish production lines in the United States,” specifically mentioning Texas.[104]

Based on this evidence, Inventec’s SCM strategy can therefore be interpreted as more of a risk mitigation and global expansion sales strategy than a dedicated China-Plus-One strategy. But even if that is how Inventec has approached its SCM strategy, it is still operating within a China-Plus-One reality. This is seen most evidently in terms of China’s human capital hold on Inventec’s global talent flows.

Job postings indicate that Inventec relies heavily on Chinese nationals and China-based engineers to stand up and support Inventec’s global operations. For example, Inventec’s Shanghai and Chongqing subsidiaries have posted multiple hiring notices for intermediate and senior engineer roles to be based out of Shanghai or Chongqing but spend up to half the year in Mexico, with Chinese as the working language on-site.[105] The job responsibilities for these roles include directly assisting the head of Inventec’s Mexico subsidiary’s materials department and “standards creation and improvement,” which is important, as fixture and functional testing are crucial to manufacturing’s internal processes.[106] In 2025, Inventec’s Shanghai subsidiary posted hiring notices for an information and communication technology fixture maintenance engineer to “train new employees” at “overseas factories,” and a process engineer to “lead the introduction of new models into production” in Inventec’s Thailand or Mexico operations.[107]

In 2015, Tsai “insisted on sending a group of Taiwanese managers to Mexico,” which helped smooth out issues that Inventec was facing on the ground.[108] While Inventec’s Taiwan’s operations occasionally hire engineers to support overseas subsidiaries—such as a recent job posting from Inventec’s Taoyuan facility to support production line testing and training in Mexico, Thailand, and Shanghai—Inventec’s recent hiring trends show a distinct preference to send Chinese engineers to assist with processes in Mexico and Inventec’s other overseas businesses.[109] One exception was an international business-focused job posting for an engineer who could help with technical localization tasks in “North America, Europe, Japan, South Korea, Southeast Asia, and the Middle East.”[110] While the role explicitly called for a Taiwanese national with a U.S. visa, the role was to be based out of Inventec’s Shanghai subsidiary, once again showing human capital dependence on China.[111]

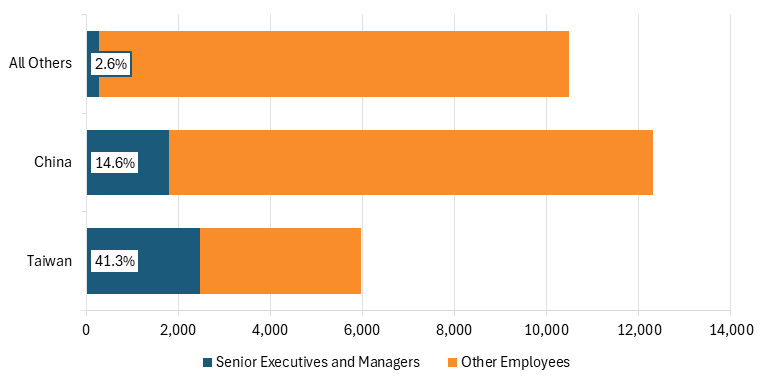

These hiring trends show that Inventec, whether due to lower costs of labor or other business-related decisions, is keeping critical know-how concentrated in China and, as a result, has partially designed its overseas operations—especially Mexico’s—to depend on China-origin engineering and technical support. While this is logical, considering Inventec’s manufacturing base is in China, it also shows that China’s model of creating stickiness in supply chains extends to talent chains as well. Data shows that Chinese nationals constituted a large share of executive positions within Inventec as of 2024, as seen in figure 11.[112]

Figure 11: Inventec employees by nationality and level of seniority, 2024[113]

More precisely, while Taiwanese nationals account for the strongest share of seniority in Inventec, at 41.3 percent, Chinese nationals are far and away in second place. As seen in figure 12, 14.6 percent of Chinese Inventec employees were senior executives or managers in 2024, compared with approximately 2.5 percent for all other nationalities.

There are three likely explanations for this. First is influence resulting from PRC strategic supply chain stickiness. The second is path dependency, as a result of Inventec having outsourced to China longer than to other countries. As scholar Yaping Gong noted, an overseas subsidiary’s “longer operation reduces agency costs, deepens local isomorphism, and therefore decreases reliance on expatriate parent country nationals.”[114] Gong also touched on the third explanation, which is cultural and linguistic overlap between Taiwan and China, stating that “[as] cultural distance increases, complete and accurate information about subsidiary actions and performance becomes more difficult and expensive to obtain.”[115]

Figure 12: Inventec senior executives and managers as share of total workforce by nationality, 2024[116]

Whether Inventec will continue such management and human capital trends for its U.S.-based operations remains to be seen. In April 2025, Inventec’s board approved a plan for an $85 million expansion of its operations in the United States, which until that point were largely limited to a service and distribution center in California with 16 employees.[117] Other reporting has suggested that Inventec’s U.S. expansion could be as high as $251 million and create as many as 2,353 new jobs.[118] So far, the expansion has completed phase one and is currently in phase two.

Based on early evidence, Inventec’s U.S. expansion looks much like its other overseas nodes, including Mexico, Malaysia, and beyond: a “China-plus-many” model in which critical engineering and process knowledge remains anchored in China.

Phase one of the investment occurred between September and October 2025, and retrofitted 39,390 square feet in an “interior remodel of open warehouse to electronic component assembly” of a 540,000 square foot prior bulk distribution center and factory that Inventec is leasing.[119] From that description, phase one looks to have built out final assembly capacity to serve the U.S. market and mitigate tariffs; in May 2025, Inventec stated that its new plant in Texas would assemble its B300 server “in order to comply with the ‘Made in America’ policy and in accordance with commitments to investment and procurement amounts” and be ready to ship to U.S. customers by Q1 of 2026.[120] It is unclear how this will intersect with Inventec’s Mexican subsidiary, which according to Taiwanese reporting, produces complete machine assembly and system testing of its back-end L10 servers and already sells tariff-free into the U.S. market.[121]

Phase two, which began in October 2025, is expected to cost $50 million and is projected to be completed in June 2026.[122] Phase two plans to renovate and alter 216,950 square feet of the Houston-area facility, and coupled with its nine-month timeline, is likely to be more advanced and build out more upstream processes than phase one.[123] Phase two’s description vaguely describes the project as focused on “computer assembly,” so it is an open question what products Inventec will ultimately manufacture in its new Texas facility.

Based on this early evidence, Inventec’s U.S. expansion looks much like its other overseas nodes, including Mexico, Malaysia, and beyond: a China-Plus-Many model in which critical engineering and process knowledge remains anchored in China. With higher labor costs and relatively higher techno-economic objectives in the United States, it remains to be seen how far up the value chain Inventec’s Texas facility will go, and whether the investment will rely on China-origin talent for standards setting and other manufacturing inputs. From a U.S. geopolitical and policy standpoint, Inventec’s inbound investment is a success, but when evaluated within the China-Plus-One paradigm, the investment currently looks like another node in Inventec’s China-dependent value chain.

Inventec: Firm and Taiwan’s Stakes

Inventec faces significant risk from its deep exposure to China, especially in terms of human capital. From the perspective of Taiwan’s government, this risk is less than ideal for the health of Taiwan’s contract manufacturing sector. China is increasingly innovative in global display and other industries within which Inventec and other Taiwanese contract manufacturers compete.[124] China’s growing strength in contract manufacturing and Taiwanese firms’ China dependence risk test the long-term resilience of Taiwan’s contract manufacturing industry.

Resonac

Resonac is a Japanese chemical company whose legacy traces back to the founding of Showa Denko in 1939.[125] In 2023, Showa Denko and its subsidiary Showa Denko Materials merged to create Resonac.[126] The company’s market capitalization as of January 2026 was approximately $8 billion.[127]

Resonac: China as the Manufacturing Base

In a December 2025 interview, Resonac’s CEO, Hidehito Takahashi, stated that the company is “ring-fencing China” by on one hand increasing production capacity in China to meet the PRC’s push for a domestic semiconductor supply chain and simultaneously attempting to lower reliance on Chinese rare earths.[128] Despite this dual-track approach, Resonac remains strongly dependent on China.

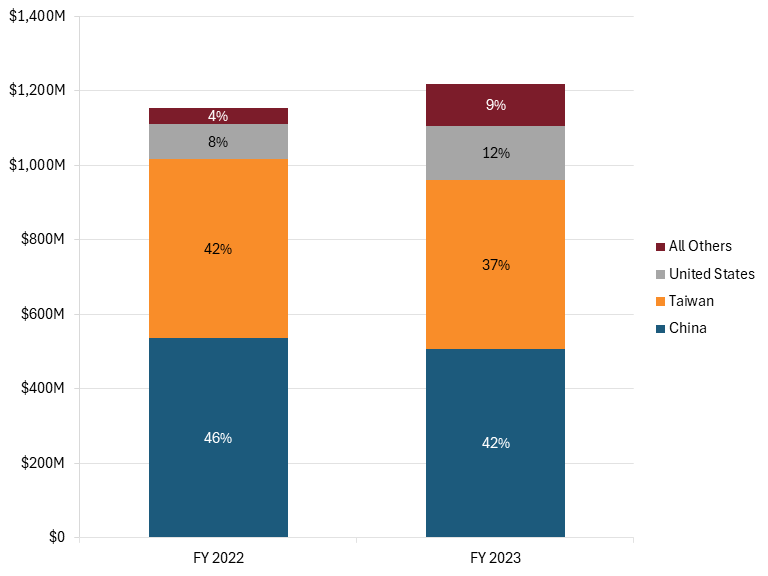

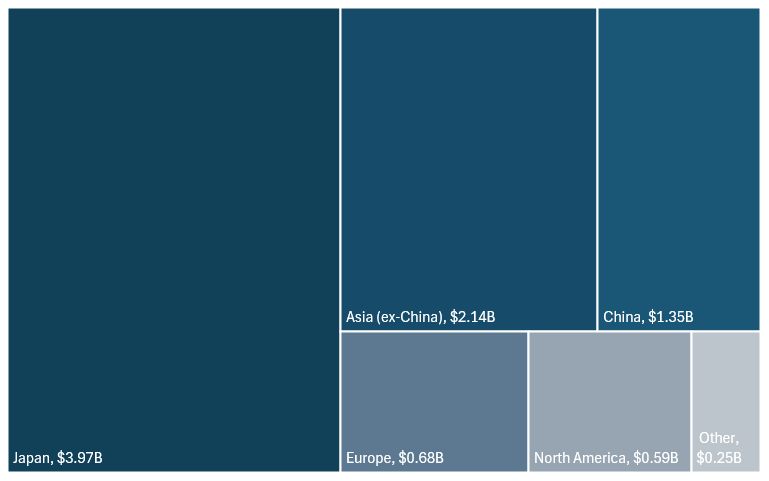

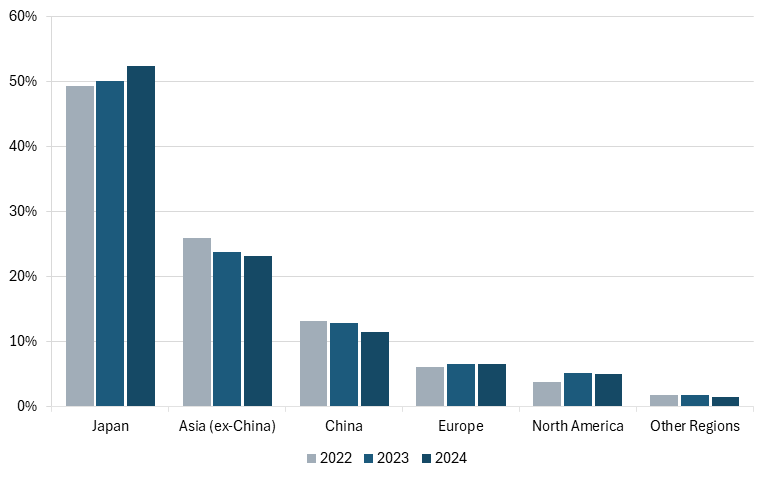

In terms of revenue, Resonac’s sales revenue from the Chinese market was approximately $1.35 billion in 2024, which accounted for approximately 15.1 percent of Resonac’s total 2024 sales revenue, as seen in figure 13.[129] That figure was up from 13.5 percent total 2023 sales to China’s market, which maps to Takahashi’s comments on recent opportunities in China.[130]

Figure 13: Resonac’s sales revenue by region, 2024 ($9 billion, total)[131]

Resonac maintains a dense manufacturing footprint across China, with 20 of its 59 global subsidiaries based in China and Hong Kong as of 2026.[132] Some of these subsidiaries are deeply embedded local suppliers that have only limited exports to the rest of Resonac’s global markets. For example, the subsidiary Resonac Materials (Dongguan), which specializes in the manufacturing of dry film photoresist, was selling more than 90 percent of its output domestically into China’s market as of 2024.[133]

Other Resonac China-based subsidiaries, such as Resonac Materials (Suzhou), both supply China’s market and are key cogs for Resonac’s global supply chain. The state-operated industrial park that hosts Resonac Materials (Suzhou) referred to the subsidiary in February 2025 as the “globally most important manufacturing base for semiconductor packaging materials and photosensitive dry film products.”[134]

In terms of human capital, in 2024, Resonac employed 2,747 employees in China, approximately 11.5 percent of its global labor share. That figure is in line with a multiyear relative downsizing of labor share to Resonac’s China-based businesses, in contrast to a growing share of Japan-based employees, as seen in figure 14.[135]

Figure 14: Resonac labor share by region, 2022–2024[136]

This data paints a picture that Resonac’s operations in China are important for the company’s global production but only offer a solid market foothold amid a slowly shrinking relative share of global employee headcount. But Resonac is strongly dependent on China for producing and maintaining its IP. As seen in figure 15, Resonac filed approximately 1,072 patents to the World Intellectual Property Organization between 2023 and 2026, of which approximately 30 percent—319 patents—were filed in China, only surpassed by 37 percent, or 393 patents, filed in Japan.[137]

Figure 15: Resonac published patents by region, 2023–2026 (1,072 filings, total)[138]

Quantity of patents does not always translate to quality or necessarily represent innovation.[139] But in Resonac’s case, qualitative data points to the company holding significant sectoral IP competitiveness through its patent base in China. For example, in 2024, the PRC government entity Shanwei Municipal Administration for Market Regulation published an “Early Warning Briefing” of patents within what the PRC calls the “new materials” industry and highlighted Resonac’s China-filed patent “Photosensitive resin composition and manufacturing method thereof” as a “top 10 most valuable patent” within the new materials sector.[140] Furthermore, Resonac has a strong track record of weaponizing its patents defensively, and places strong importance on the Chinese patent ecosystem, with the company’s Intellectual Property Department internally having a “high demand for translating Chinese patents.”[141]

While Resonac has comparatively less human capital tied up in China than Inventec does, it remains highly dependent on China for key IP and know-how. This is unlikely to change moving forward. As a senior executive at one of Resonac’s China subsidiaries wrote in September 2025, “[Resonac is] optimizing its local production and consumption system in China and deepening its presence in the high-value-added markets for mobility materials and innovative materials.”[142]

Resonac: United States as a Plus-One Node

Resonac’s presence in the U.S. economy is limited and deliberately cautious. With a few small exceptions, Resonac’s U.S. activities are concentrated in research collaboration, sales, and customer interface rather than standalone manufacturing.[143] The company has no large-scale U.S. production facilities for its core semiconductor materials, including photoresists, epoxy molding compounds, or other materials used in the semiconductor back-end process.[144]

Resonac’s main footprint in the U.S. economy in recent years has come in the form of creating or joining numerous consortia, rather than significant capital expenditure. In July 2024, the company launched US-JOINT, a consortium of five Japanese and five U.S. companies working together with the shared goal “to collaborate on next-generation semiconductor packaging in Silicon Valley.”[145] As Resonac CEO Takahashi wrote in 2025, US-JOINT will lead to “building interfaces with businesses we have had limited interaction with,” acknowledging that Resonac has not historically focused significantly on the U.S. market.[146] The consortium also plans to establish an R&D center in Union City, California, to be fully operational in 2025, but as of 2026, US-JOINT has yet to announce whether the R&D center was built, despite the consortium having grown to include 12 companies.[147]

In September 2025, Resonac announced the establishment of JOINT3, “a co-creation evaluation framework formed by a consortium comprising Resonac and 26 other companies from Japan, the United States, Singapore, etc.”[148] This followed Resonac’s pre-merger predecessor company, Showa Denko Materials, having created a Japan-based consortium, JOINT2, in 2021.[149] In 2025, Resonac CEO Takahashi wrote that the reason why Resonac is well-placed to form and lead consortia such as US-JOINT, JOINT2, and JOINT3 is the company’s vertical integration: “We offer a lineup that covers approximately 80%, presumably, of the key semiconductor back-end process materials.”[150]

In November 2023, Resonac joined a consortium of semiconductor-related manufacturers hosted by The University of Texas at Austin and named Texas Institute for Electronics (TIE), which has the goal “to advance the roadmap of cutting-edge semiconductor systems by five years, and to develop them in the United States.”[151] In 2024, the Defense Advanced Research Project Agency (DARPA) selected TIE “to develop the next generation of high-performing semiconductor microsystems for the Department of Defense,” with the Department of War (DOW) and State of Texas funding TIE with a combined investment of $1.45 billion.[152] Resonac is one of seven strategic partners in TIE, with it and Canon being the only Japanese firms.[153]

Ventures such as US-JOINT, JOINT3, and TIE are safe and beneficial choices for Resonac from a China-Plus-One perspective. They promise to help the company access U.S. talent, IP, and government funding, and also are low cost since they are in collaboration with other firms, are mostly focused on R&D, and allow Resonac to test the waters before making any more capital-intensive investments. At the moment, Resonac is employing a tentative China-Plus-One strategy: The same vertical integration that Resonac claims helps it lead consortia rests on a significant share of tightly coupled manufacturing, testing, and human-capital capabilities that remain concentrated in China.

CEO Takahashi said in February 2025 that the company “is not currently considering manufacturing materials in the United States,” something he said would only change with a notable increase in U.S. demand.[154] Taken together, Resonac’s intent is clear: It is willing to invest time, expertise, and limited capital in U.S.-based R&D ecosystems but remains unwilling to commit to high-value manufacturing in the United States—in the process, likely shifting more production out of China—absent stronger demand and clearer policy signals.

Resonac: Firm and Japan’s Stakes

Resonac’s 2025 annual report provides insight into how the company evaluates China risk. Resonac revealed that the company views the “disruption of global markets due to the acceleration of U.S.-China economic security policies” as one of its highest-tier risks.[155] Specifically toward China, Resonac listed “[e]xport restrictions on China are expanded to include not only semiconductors and their manufacturing equipment and technology, but also semiconductor materials” as its primary China-related risk.[156] Resonac additionally launched a team dedicated to U.S.-China decoupling in 2023.[157] While Resonac surely evaluates other China-related risk internally, it is notable that the only publicly-listed China country-level risk is vis-à-vis U.S. policy, and does not mention China-policy-related risks, outside a formulated Taiwan contingency evacuation plan that does not mention China.[158]

However, Resonac’s IP strength in its China operations has created significant risk for the company. Two lawsuits show how Resonac faces intense IP theft and regulatory risk in China’s market that threaten its long-term market share prospects.

In December 2023, Resonac and its subsidiary Resonac Materials (Dongguan) filed a patent infringement lawsuit in the Shenzhen Intermediate People’s Court.[159] The lawsuit sought “an injunction against the sale in China of photosensitive films manufactured and sold by” four Chinese photosensitive film firms that Resonac claimed infringed upon “a Chinese patent held by the company relating to photosensitive films.”[160]

Three months before Resonac filed the patent infringement lawsuit, one of the four named co-defendants changed its name from Hunan Wujo High-Tech Materials to Hunan Initial New Materials (Initial NM).[161] In 2021, a local PRC government profiled Initial NM, lauding the company for having helped China “overcome a critical ‘bottleneck’ technology, contributing to the security of the national electronic information industry chain” after the company successfully produced a photosensitive dry film for integrated circuit (IC) packaging substrates. The article went on to note that, before Initial NM’s breakthrough, “dedicated photosensitive dry films [had only been] produced in countries such as the United States and Japan.”[162] The bottleneck mention was in reference to a PRC Ministry of Education summary of 35 different bottleneck technologies that a Chinese government-run newspaper published in 2018.[163]

Around the time of Resonac’s patent lawsuit, Initial NM had what one journalist described as “a concentrated burst of 15 patent grants that was obtained [by Initial NM] between 2024 and September 2025.[164] As of 2024, Initial NM’s global market share for photosensitive dry film was 13.2 percent, making it the lead Chinese firm in the sector, and third globally behind Taiwanese firm Eternal Materials and the global leader Resonac.[165] According to WireScreen, 18.1 percent of Initial NM’s ownership can be traced back to state entities, with the PRC State Council itself indirectly holding a 3.7 percent share of the company.[166]

Of the other three Chinese firms that Resonac named as codefendants, one is closely related to Initial NM, with executives from the same Chinese family, the Xiaos, and shared supply chains, patents, and financing.[167] Another company, Shenzhen Technology Trust Precision Industry (TTST), is 9.4 percent PRC state-owned and also is 3.3 percent indirectly owned by China’s leading domestic chipmaker, Semiconductor Manufacturing International Corporation, according to WireScreen.[168] In 2024, TTST began exporting its products—which include equipment and machinery used for IC substrate and related dry film processes—to Taiwan, Japan, and South Korea.[169]

As of 2026, Resonac’s patent lawsuit remains unresolved. However, the precedent for enforcing IP in China as a foreign multinational firm is not in Resonac’s favor. Nor does Resonac’s own historical precedent provide much optimism. Showa Denko Materials, one of the two firms that merged to create Resonac in 2023, filed a patent infringement lawsuit in China against Beijing Kehua New Materials (Scienchem) for its white epoxy molding compounds in 2021.[170] Showa Denko Materials requested Scienchem cease infringement and provide compensation for economic losses, but Scienchem challenged the patent with the PRC National Intellectual Property Administration (CNIPA).[171] In January 2022, CNIPA invalidated Showa Denko Materials’ patent entirely.[172] Five years later, the legal case has now moved to the PRC’s Supreme People’s Court, with no resolution in sight, leaving Resonac, as the post-merger successor company to Showa Denko Materials, responsible for pursuing two unresolved patent infringement lawsuits.[173]

Like Initial NM and TTST, Scienchem is PRC state owned: the Institute of Chemistry, Chinese Academy of Sciences (ICCAS) founded the company with the goal to develop the PRC’s domestic epoxy molding compounds capabilities, and according to WireScreen, ICCAS owns 41.9 percent of Scienchem.[174] As of 2026, Scienchem has grown continuously, and its subsidiary, Zhongke Kehua, is applying for an initial public offering (IPO) on China’s Shanghai Stock Exchange STAR Market.[175]

Resonac’s two ongoing IP disputes underscore the persistent risk faced by foreign multinational firms operating in China, and particularly those—like Resonac—with technology that China still cannot manufacture domestically.

In Zhongke Kehua’s IPO prospectus, the company identifies Resonac as a key competitor in the epoxy molding compounds sector, writing that “the global mid-to-high-end epoxy molding compound market remains dominated by two Japanese manufacturers” (Resonac, as well as Japanese company Sumitomo Bakelite).[176] Zhongke Kehua went on to write:

The company’s mid-range products have successfully replaced Japanese competitors, and its supply volume to multiple customers has surpassed that of Sumitomo Bakelite and Resonac. While the company’s high-end products can now replace Japanese competitors, the product introduction cycle remains lengthy due to factors such as customer Product Change Notification procedures. It is anticipated that large-scale replacement will gradually be achieved in the future, driving business growth.[177]

Resonac’s two ongoing IP disputes underscore the persistent risk faced by foreign multinational firms operating in China, and particularly those—like Resonac—with technology that China still cannot manufacture domestically. These disputes and the state-backed competitive environment illustrate why the China component of China-Plus-One is both strategically essential and operationally risky for Resonac. On one hand, Resonac is competing to stay ahead of Chinese, state-backed competitors such as Zhongke Kehua. From Resonac’s perspective, its incremental approach to offshoring from China is rational. Relocating more production from its established Asian facilities, especially those such as Resonac Materials (Dongguan) that are already tightly integrated into customer supply chains, would impose significant risks.

On the other hand, Resonac is bleeding valuable IP that is likely ending up precisely with competitors such as Zhongke Kehua. As a long-term threat that is unlikely to show up on quarterly balance sheets, that risk is most concerning not for Resonac, but for Japan’s government, which needs to ensure the long-term health of its domestic but globally connected semiconductor packaging and chemistry sectors.

LS C&S

LS C&S is a subsidiary of the South Korean conglomerate LS Corp and primarily manufactures energy, industrial cable, and telecommunications products.[178] LS Corp was listed at 1,830 in the 2025 Forbes Global 2000 ranking with a $2.41 billion market value.[179]

LS C&S: China as the Manufacturing Base

At a high level, LS C&S’s footprint in China appears no larger than other countries in which LS C&S has operations. The company operates two large manufacturing subsidiaries in China, LSHQ in Hubei province and LSCW in Jiangsu province, as well as four sales offices.[180] LS C&S has two manufacturing plants in Indonesia and Vietnam, so rather than a China manufacturing hub with global spokes, it would appear that China is just one of many diversified supply chain nodes LS C&S has globally. While LS C&S relies on Chinese suppliers of specialty materials at the process level, it is not particularly reliant on China as an overall source of upstream suppliers.[181] In 2024, LS C&S purchased approximately $37 million of goods and services—including commodities, raw materials, construction services, manufacturing, and equipment—from China, amounting to a mere 1.6 percent of its total global purchase amount.[182]

Yet, this assessment understates the strategic importance of LS C&S’s China operations to the company’s bottom line for two reasons: LS C&S’s two manufacturing plants in China are without a doubt the heart of its global production capabilities, and China is a huge and important market to LS C&S.

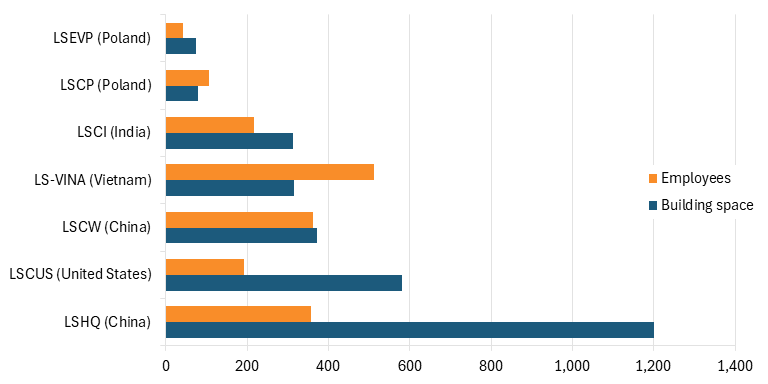

As of 2019—the last year LS C&S published data on its subsidiaries’ employee count and building area—the company’s China-based subsidiary LSHQ was far and away the largest manufacturing facility out of any LS C&S global subsidiary.[183] As seen in figure 16, LSHQ is a massive plant at 1,200,713 square feet of building area, despite having fewer employees than other, smaller manufacturing subsidiaries.[184]

Figure 16: LS C&S global subsidiaries by numbers of employees and thousands of square feet, 2019[185]

LSHQ is one of LS C&S’s most technologically sophisticated global subsidiaries. Established in 2009 as a Chinese-foreign joint venture through LS C&S’s acquisition of a controlling stake in the former state-affiliated Hubei Red Flag Cable Factory, LSHQ combines legacy PRC industrial capabilities with LS C&S’s proprietary cable technologies.[186] LS C&S framed the deal as “glocalization,” and indeed, over the years, the acquisition allowed LS C&S to increase its institutional roots, workforce continuity, and access to national infrastructure projects in China.[187] As of 2026, according to WireScreen, LS C&S holds a 92.7 percent direct share of LSHQ in 2026, with the PRC state-affiliated China Citic Financial Asset Management Company Limited owning the remainder.[188]

LSHQ, as of 2019, operated advanced production lines for ultra-high-voltage (220kV–500kV) cables, submarine power and fiber-optic composite cables, and DC transmission systems. LSHQ is one of only a handful of manufacturers in China capable of producing ultra-high-voltage and submarine cable systems at scale, making it central not only to LS C&S’s China strategy but also to its global high-end cable portfolio.[189] LSHQ additionally “attaches great importance to the development of overseas markets,” seen most clearly in its successful bid in 2019 for a substantial project in Ecuador.[190]

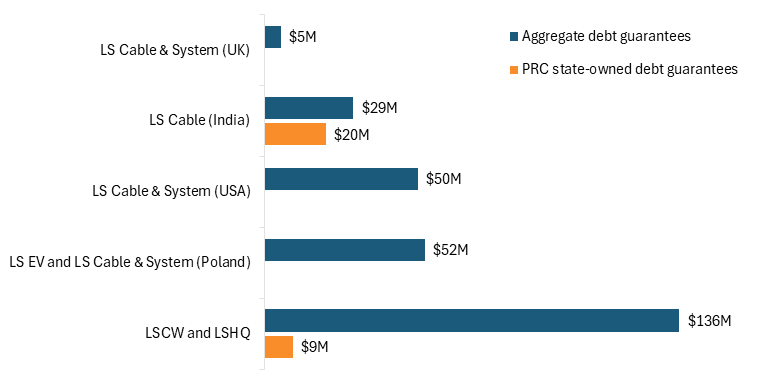

Debt guarantee data also shows how LS C&S’s global scale of operations tilts toward its China subsidiaries. In 2020, LS C&S financed LSCW and LSHQ with an aggregate total of approximately $135.8 million in debt guarantee, with coverage extending through 2021.[191] As figure 17 illustrates, this amount disproportionately exceeded the capital that LS C&S directed toward other global branches between late 2019 and late 2020. While the COVID-19 pandemic likely influenced these figures, they overall correlate to a strong operational dependency on China. LS C&S channeled much of this funding through South Korean policy and commercial banks, with PRC state-owned banks holding approximately 11 percent of LS C&S’s total debt guarantees during this stretch, with much of that exposure directed to LS C&S’s India-based subsidiary.[192]

Figure 17: Debt guarantee financing, LS C&S global subsidiaries, 2019–2020[193]

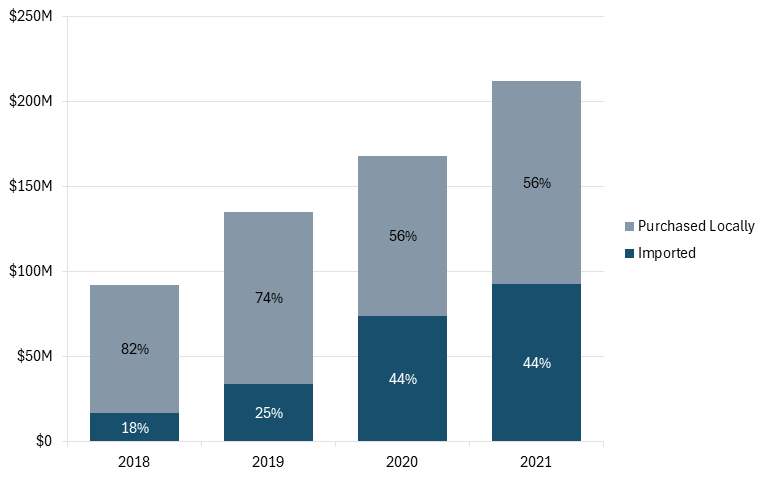

Between 2018 and 2021, LS C&S’s China subsidiaries appeared to grow in scale. As seen in figure 18, LSCW and LSHQ steadily increased their procurement of raw materials.[194] Additionally, the share of raw materials imported into China versus sourced locally rose from 18 percent in 2018 to 44 percent in 2020 and 2021.[195] Although LS C&S has not released comparable granular data since 2021, the upward trajectory of material imports indicates an aggressive expansion of either manufacturing scale, technical complexity, or both.

Figure 18: LS C&S raw materials procurement in China-based subsidiaries, 2018–2021[196]

Second, LS C&S has long viewed China’s market opportunity as important to the company’s future fortunes. In 2010, the company predicted that “China will be a key market to realize our vision of becoming the global No. 1 cable manufacturer.”[197] While LS C&S does not publish region-specific revenue data, it appears to have been successful in the Chinese market for two reasons. The first is it understands how to compete in China’s market. For example, in 2016, LS C&S partnered with the state-owned Chinese electric vehicle (EV) company BAIC Group to supply it with EV harnesses.[198] An LS C&S executive, Jae In Yoon, said at the time, “[W]e were able to be selected as a partner, beating out major Chinese electrical equipment companies, by quickly providing products that reflect customer requirements.”[199]

LS C&S has also likely beaten out Chinese competitors at the highest levels in China. In 2015, the National People’s Congress (NPC) Procurement Center—the centralized procurement body serving China’s national legislature—awarded LSHQ a contract for approximately $475,000 to supply power cables for the Great Hall of the People.[200] Although the tender did not disclose competing bidders, a contemporaneous government-backed cable procurement in 2015 shows LSHQ as the only foreign multinational among 14 bidding cable companies, suggesting that LSHQ prevailed over domestic suppliers.[201] Given that the Great Hall of the People is the seat of the NPC and one of the PRC’s most politically sensitive government facilities, LS C&S’s selection indicates a high degree of technical credibility and institutional trust.[202]

LS C&S is also embedded within China’s technical standards ecosystem. LSHQ has served as a drafting organization for multiple PRC national cable standards for insulation types, voltage classes, testing protocols, and tolerances.[203] The PRC often modifies these standards to adopt international norm bodies’ standards—such as the International Electrotechnical Commission’s 60502-1—but localizes them under national PRC standards committees.[204] Acting as a drafting unit goes well beyond passive compliance and puts LSHQ in a position to be involved in, and also influenced by, the technical rulebook governing China’s cable market.[205]

While LS C&S’s overall manufacturing footprint and global supplier network appear more diversified than Inventec’s and Resonac’s, its China-based subsidiaries remain central to the company’s global production capabilities, technical know-how, and standards ecosystem, making the firm still substantially dependent on China.

LS C&S: United States as a Plus-One Node

LS C&S’s U.S. investments are sizable, ambitious, and illustrative of what successful China-Plus-One investment can look like when the United States is the plus-one recipient nation.

Over 2024 and 2025, LS C&S announced three major new investments in the U.S. economy. First was a 750,000-square-foot submarine power cable manufacturing factory to be operated by the U.S. subsidiary LS GreenLink, which the company announced in July 2024 and broke ground on in April 2025.[206] The factory, a rendering of which is shown in figure 19, will be located in Chesapeake, Virginia, will cost approximately $681 million, and is expected to create 330 new jobs.[207] The project stands to benefit from substantial public support, including $99 million in IRA tax credits, $48 million in Virginia state-level subsidies and tax relief, and $13.2 million for Chesapeake to assist the project.”[208]

Figure 19: LS GreenLink Chesapeake, Virginia, facility, rendering[209]

LS C&S announced its second major new investment in November 2025, stating that it had secured a $345.3 million, three-year contract with an unnamed U.S. tech company “to supply high-capacity power distribution systems to artificial intelligence data centers.”[210] This announcement is light on details, but dovetails with LS C&S’s multi-year effort to embed itself within the U.S. data-center power ecosystem. In November 2025, LS C&S separately appointed Empire Electric Sales as its representative in northern California, explicitly citing the region’s “explosive data center growth due to AI and cloud computing.”[211]

The third investment is an additional factory in Chesapeake that is expected to cost $689 million, create 430 new jobs, and produce copper rods, magnet wires, and rare earth magnets.[212] Both Chesapeake and LS C&S will have access to relatively modest public subsidies to assist the project.[213] However, LS C&S and the state of Virginia had slightly different messages during the announcements of the project. On December 12, 2025, Virginia governor Glenn Youngkin announced “plans for a significant additional investment,” while on December 15, 2025, LS C&S announced that it “is reviewing the feasibility of the project, and has formally begun cooperation discussions with the State of Virginia,” with a representative adding the qualifier, “if the business becomes a reality.”[214] LS C&S has started marketing employment at its new Virginia investments to potential South Korean national employees.[215]

From a U.S. perspective, these three investments are unequivocally positive. LS C&S appears to be taking as many precautions as possible to make sure its localization into the U.S. economy goes smoothly. For its submarine cable factory, LS GreenLink is hiring a bilingual “Organizational Development Specialist (Cross-Cultural Integration)” who can “serve as a bridge between [South] Korean headquarters and U.S. operations” and “support [South] Korean expatriates in adapting to the U.S. business environment and help local employees understand [South] Korean business culture.”[216]

U.S. policy, however, threatens the investment’s potential. LS C&S’s initial plan to build the submarine cable factory occurred under the Biden administration and IRA framework.[217] The state of Virginia and LS C&S framed the investment purely in terms of clean energy potential, with the facility’s future subsea cables planned to transmit electricity generated from offshore wind farms to onshore grids.[218] President Trump has consistently expressed skepticism toward offshore wind projects and, in 2025, reversed policy aimed at increasing U.S. wind capacity.[219]

In contrast, in 2025, Virginia governor Youngkin said that LS C&S’s more recent, rare earths factory investment “will create a new and growing domestic supply chain … that bypasses the monopoly of Chinese suppliers,” and directly mentioned rare earth dual-use functionality.[220] LS C&S has also adapted its language toward how it discusses its U.S. investment, for instance, noting in March 2025 that its subsidiaries do not use Chinese aluminum or copper in its supply chain.[221] Speaking about U.S. tariff risk, LS C&S president Koo Bon-kyu said in April 2025, “Can we de-risk everything? No, but I think we can de-risk quite a lot of it.”[222]

LS C&S appears ready to adapt its U.S. investments to evolving policy conditions, and it is positive that, with the new administration’s direction in the United States, its three investments have increasingly considered China-related supply chain risks. In this, LS C&S sees opportunity, stating in March 2025 that the U.S. government’s “China phase-out” policies are helping LS C&S and other LS Corp subsidiaries in “their conquest of the U.S. market.”[223]

Still, continued policy volatility could prompt the company to reassess the scale and timing of future projects. While LS C&S’s U.S. investments are massive, it is still reserving some capacity. LS GreenLink is developing approximately half of the 96-acre site it purchased to build a submarine cable factory, but the company is “reserving the remainder for future phases of development,” which the company has said will allow it “to expand its production capacity and technological capabilities in response to evolving global infrastructure requirements.”[224] Those “global infrastructure requirements” will likely depend, in part, on U.S. policy direction.

If fully realized, LS C&S’s Chesapeake investments would localize manufacturing processes and supply chain capabilities that China has recently dominated, while embedding the company within U.S. energy and AI ecosystems.

Taken together, LS C&S’s U.S. investments largely align with the conditions under which the United States can “win” China-Plus-One in this context. The company’s projects target advanced, high-fixed-cost infrastructure sectors where scale, reliability, and industrial know-how matter more than low-cost assembly. If fully realized, LS C&S’s Chesapeake investments would localize manufacturing processes and supply chain capabilities that China has recently dominated, while embedding the company within U.S. energy and AI ecosystems.[225]

LS C&S: Firm and South Korea’s Stakes

LS C&S is attempting to hedge between market opportunities and other benefits to its presence in China while simultaneously diversifying and expanding its international business ambitions. It is a narrow line to walk.

More so than Inventec or Resonac, open source documentation points to LS C&S gaining benefit after benefit within the Chinese market, perhaps due to the institutional trust that allowed it to win a sensitive PRC contract in 2015. LS C&S gets preferential access to financing from banks and state-backed programs.[226] LS C&S appears to be involved in the PRC’s Belt and Road Initiative.[227] The company enjoys hundreds of millions of renminbi in government subsidies on a consistent basis, from reward subsidies to disaster relief to insurance facilitation.[228] China’s government rewards LS C&S China subsidiary executives for “maintain[ing] a firm and long-standing friendly stance towards China.”[229] The Yichang Municipal Bureau of Economy and Information Technology has “provid[ed] cable demand information to facilitate production and sales connections” to LS C&S.[230]

At the same time, LS C&S is pivoting strongly toward the United States. Its investments far outsize Resonac’s various consortia and even Inventec’s sizeable Texas-based factory. LS C&S has sizeable investments in many other regions, but they do not compare in scope to its U.S. investments, making the company’s approach truly China-Plus-One. These investments go beyond business decisions, showing a geopolitical tilt; while there is no evidence that it has taken place on U.S. soil, LS C&S participated in the U.S. defense-industrial base in 2023, with the U.S. Navy awarding LS C&S $41,175 to repair a ship in South Korea.[231]