China, Exporter—United States, Importer

The global economy has evolved in troubling ways, at least from the U.S. perspective. In 2021, the United States accounted for a whopping 78 percent of the total trade deficit among industrial-based, deficit-running nations. In other words, America was the importer of last resort for much of the world, buying cars, machine tools, drugs, computers, and the like and giving T-bills in exchange.

In contrast, despite a long-standing ruse by the CCP leadership to promise “rebalancing” (fewer exports and more domestic consumption), China accounted for 45 percent of the total trade surplus among industrial-based surplus-running nations. The CCP has no intention of changing this because running trade surpluses provides China with financial and technological power.

This situation reflects the United States’ decreasing global competitiveness and China’s enormously successful, decades-long innovation mercantilism effort. As such, it is unstainable if America does not want to turn into a vassal state.

This pattern is not serendipitous. It is not related to U.S. or Chinese savings rates. And it is not benign. It is problematic, and it stems from 1) conscious decisions on the part of the CCP to expand industrial output at the expense of the United States and 2) a failure of the United States to develop, implement and fully fund a robust manufacturing competitiveness strategy.

The moderate-to-long-term result of this trend continuing will be to bring Alexander Hamilton’s worst fears to fruition: America as a “hewer of wood and drawer of water” (in this case, exporting principally agricultural products, energy, tourism, and waste paper) and China as the new Britain: the global advanced industry behemoth of the 21st century.

The United States accounts for a considerable, disproportionate share of the cumulative trade deficit of deficit-running industrial-based economies—i.e., economies not overly reliant on natural resources or niche industries such as tourism. Overall, the process for inclusion was subjective, with countries being selected as industrial if they had reasonably significant manufacturing output and low to moderate levels of natural resource output. Resource-reliant economies are defined here as those for which profits from natural resources account for at least 1.5 percent of gross domestic product per World Bank data. The table below lists the deficit-running industrial-based economies considered.

Table 1: Deficit-running industrial-based economies

|

Albania |

Jordan |

North Macedonia |

|

Bangladesh |

Kenya |

Pakistan |

|

Bosnia and Herzegovina |

Kosovo |

Philippines |

|

Cambodia |

Lebanon |

Serbia |

|

El Salvador |

Moldova |

Ukraine |

|

Georgia |

Montenegro |

United Kingdom |

|

Japan |

Nicaragua |

United States |

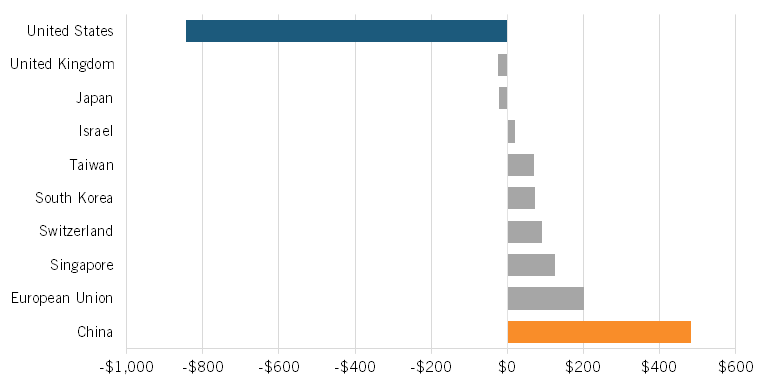

In 2021, the United States accounted for 78 percent ($845 billion) of the group’s combined deficit. In contrast, the other two major economies in the group, Japan in the United Kingdom, each account for only 2 percent of the group’s deficit.

China’s trade surplus accounts for almost half of the total for the surplus-running industrial-based economies (listed below). Specifically, China accounted for 45 percent ($484 billion) of the group’s surplus in 2021. The European Union accounted for an additional 19 percent ($201 billion), primarily because of Germany. Figure 1 below shows the 2021 trade balances for each major industrial-based economy.

Table 2: Surplus-running industrial-based economies

|

China* |

Panama |

Taiwan |

|

Costa Rica |

Singapore |

Thailand |

|

European Union |

South Korea |

Turkey |

|

Israel |

Switzerland |

*Note: China includes mainland China, Hong Kong, and Macao.

Figure 1: Trade balances of major industrial-based economies, 2021 ($US billions)

Sources: World Bank, Taiwan Bureau of Foreign Trade

As economist Herb Stein once famously stated, “If something cannot go on forever, it will stop.” This is undoubtedly true about the United States’ massive trade imbalance, particularly with China. The real issue is how much damage to the U.S. advanced industry base, especially relative to China’s, will occur before this happens. The CHIPS and Science Act (and related tax credits for investing in semiconductor equipment), coupled with the tax credits in the Inflation Reduction Act, were good starts, but much more is needed to get U.S. competitiveness back on track and the U.S. trade balance back under control.