US Technology Companies Should Keep Operating in China

When U.S. technology companies compete in China, they capture revenue, learn technologies and trends from a critical market, and extend U.S.-built ecosystems. Forcing them out of China would weaken U.S. global competitiveness and give Chinese firms greater scale to shape technology ecosystems.

KEY TAKEAWAYS

Key Takeaways

Contents

Mapping the Activities of U.S. Companies in China. 3

Why It Matters: The Benefits of Having U.S. Companies in China. 12

Criticism Against U.S. Companies Operating in China. 18

Introduction

Many voices in Washington argue that U.S. companies should not be in China. This idea, which would represent a de facto decoupling from China, is not a consensus view, but it has support from various constituencies. In 2022, Senator Rick Scott (R-FL) urged U.S. companies to “redirect supply chains and decouple their businesses from Communist China before its planned invasion of Taiwan.”[1] Furthermore, during his first administration, president Trump posted on social media that ‘ordered’ U.S. companies to “immediately start looking for an alternative to China.”[2] Biden’s secretary of commerce, Gina Raimondo, stated in 2023 that U.S. companies complained that China was becoming “uninvestible.”[3] Others advocate incentives for companies to exit China, arguing that keeping investments there “creates a dangerous business risk environment for U.S. companies.”[4] Yet, few policymakers and pundits make the case that there is still a rationale for U.S. companies to do business in China, especially in the Chinese market.

To be sure, some U.S. investments have helped build China’s manufacturing capacity and train skilled engineers who now compete against American businesses, and U.S. companies should not be involved in supply chains that engage in forced labor.

However, U.S. companies producing in China to serve the Chinese local market should not be controversial. The Bureau of Economic Analysis (BEA) estimates that 70 percent, or $441 billion, of what U.S. companies in China produced in 2023 was sold in the Chinese market. These are revenues that otherwise would be captured by Chinese companies. For U.S. interests, it is better to have American firms in China supplying that local market than Chinese firms occupying that space.

This report argues that the discussion of forcing companies to exit the Chinese market is an overreaction and fails to account for ways in which having American companies in China serves the U.S. national interest. First, having a presence in the Chinese market is valuable because it helps U.S. companies increase revenue and gain market share, which would otherwise accrue to Chinese companies. The Chinese Communist Party (CCP) imposes unfair restrictions on accessing the Chinese market, and producing in China for that market is one way U.S. firms can sell there. Second, there is a correlation between sales in China and global investment in research and development (R&D). Third, there is a reverse technology spillover effect—in which foreign investments by U.S. companies serving local markets benefit the country where the company is headquartered—wherein the learning can be transferred back to America. Fourth, the spread of some U.S. technologies in Chinese markets creates dependencies or ‘lock-ins’ among Chinese companies and users. Finally, having a presence in China can provide U.S. firms with valuable access to high-quality talent and important insights into national technological developments and market trends.

The discussion of forcing companies to exit the Chinese market is an overreaction and fails to account for ways in which having American companies in China serves the U.S. national interest.

The report begins with a summary of aggregated outcomes for U.S. companies in China, including revenues, capital expenditures, R&D investments, and other key indicators. It then addresses some of the boundaries of doing business in China, starting by outlining restrictions on doing business with specific companies and how the People’s Republic of China (PRC) coerces U.S. companies. The report then outlines the benefits of American companies in China for U.S. interests and briefly describes some backlash American companies have faced for operating there. Finally, the report suggests narrow policy interventions oriented at incentivizing offshoring production that does not serve the Chinese market, avoiding “asymmetrical competition” between U.S. and Chinese technology companies, improving transparency, and retaining Chinese top talent in America. However, the most important policy recommendation is for the U.S. government not to attack or pressure U.S. companies producing in China for the Chinese market.

Mapping the Activities of U.S. Companies in China

Business relations between the United States and China date back to before the restoration of diplomatic relations in 1979.[5] BEA has identified 1,950 U.S. companies with affiliates in mainland China and 921 with affiliates in Hong Kong that had assets, sales, or net income exceeding $25 million in 2023.[6] Because BEA’s data does not distinguish between companies with activities in both jurisdictions, it is impossible to determine the total number of U.S. companies in mainland China and Hong Kong. Despite this limitation, the total economic activity of U.S. companies in mainland China and Hong Kong can be included. This report refers to China as the aggregate of activities in mainland China and Hong Kong.

BEA’s data considers U.S. affiliates in China, a specific statistical definition. BEA has stated that a “‘foreign affiliate’ is a foreign business enterprise in which there is U.S. direct investment, that is, in which a U.S. person directly or indirectly owns or controls 10 percent of the voting securities or the equivalent. Foreign affiliates comprise the foreign operations of a U.S. multinational enterprise over which the U.S. parent is presumed to have a degree of managerial influence.”[7] This definition is a subset of what is more commonly called a “U.S. company,” which includes, for example, representative offices. Despite this subtle difference, there are no significant distinctions between a “U.S. company” and a “U.S. affiliate” in China for this analysis, as technology and manufacturing companies fall into both categories.

Calcbench, a financial data provider, identified 173 publicly listed U.S. companies that reported revenues directly from China in 2024.[8] Although this is a helpful source of data, the number has limitations and likely undercounts many publicly listed U.S. companies’ activities in China, as they are only required to disaggregate earnings between the United States and overseas markets in their annual 10-K reports to the Securities and Exchange Commission (SEC). It is up to company executives to decide whether to publicly disclose their revenues from China or any other specific country. Oracle, for example, reports to the SEC revenues from Germany, Japan, and the United Kingdom in its Form 10-K filing, while maintaining over 30 offices in China.[9] By extension, it is also not possible to determine the revenues of private U.S.-owned technology companies with a presence in China, such as Databricks or Stripe.

Sales of U.S. Companies in China

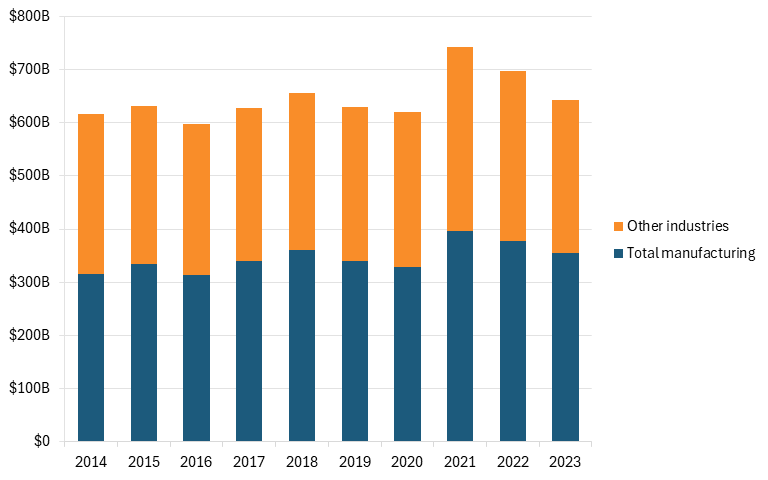

BEA determined that, in 2023, U.S. affiliates in China generated over $640 billion in revenue, an 8 percent decline from the previous year. (See figure 1.) Sales in China peaked at $668 billion in 2021 (equivalent to $742 billion in 2023 dollars) and have since declined. The manufacturing sector accounted for 55 percent of U.S. companies’ sales in China in 2023, the highest proportion reported over the last 10 years. The COVID-19 recovery period constituted the two years with the highest sales, 2021 and 2022, which coincided with executives of U.S. companies in China reporting the highest levels of optimism and documented increases in profitability and investment prospects.[10] Sales in 2023 were at similar levels to those in the previous years before the COVID-19 pandemic.

Figure 1: Total sales of U.S. affiliates derived from activities in China (2023 prices)[11]

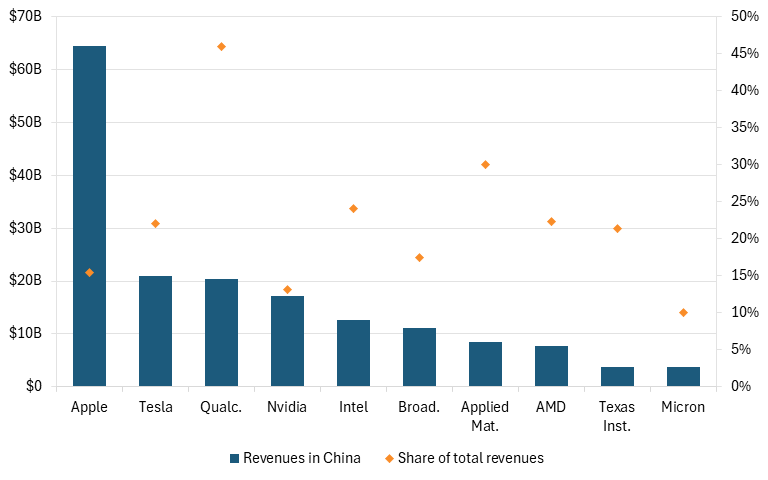

Another alternative for measuring U.S. companies’ sales in China is to analyze Form 10-K filings, which are mandatory for U.S.-headquartered public companies. Calcbench analysis suggests that, in 2024, revenues from China for 173 publicly listed companies totaled over $307 billion.[12] Figure 2 shows the Information Technology and Innovation Foundation’s (ITIF’s) analysis of a select group of U.S. technology companies with relevant operations in China, with China revenues exceeding $170 billion for 2025.

Figure 2: Revenues in China from a selected group of U.S. technology companies in 2025[13]

* Apple’s revenue includes mainland China, Hong Kong, Macau, and Taiwan.

** Qualcomm, Nvidia, Broadcom, AMD, and Micron all include mainland China and Hong Kong.

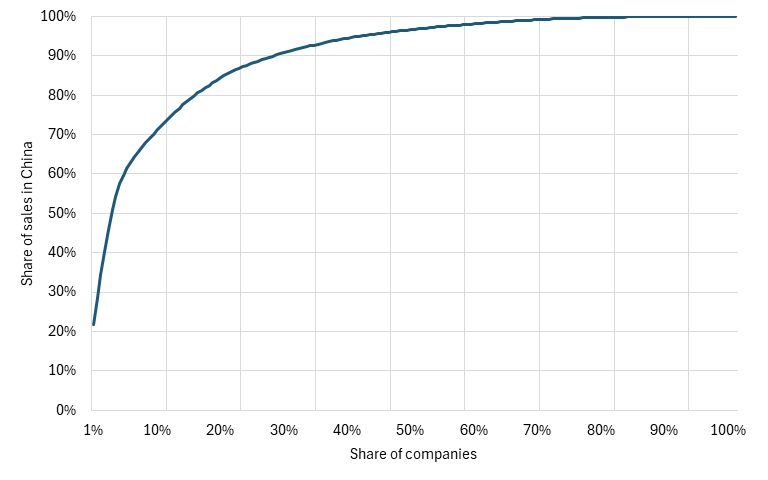

Total sales in China are concentrated among a few companies. Using Calcbench’s dataset for 2024, Apple accounted for 22 percent of the total revenue, and the top 10 companies made up 61 percent of the total revenue. (It is important to note that Apple reports revenues for Greater China, including Taiwan.) Figure 3 shows this concentration, indicating that, at the other end of the distribution, over 100 companies accounted for only 5 percent of the sample’s total revenues in China.

Figure 3: Cumulative sales in China of a selected group of publicly listed U.S. companies (2024)[14]

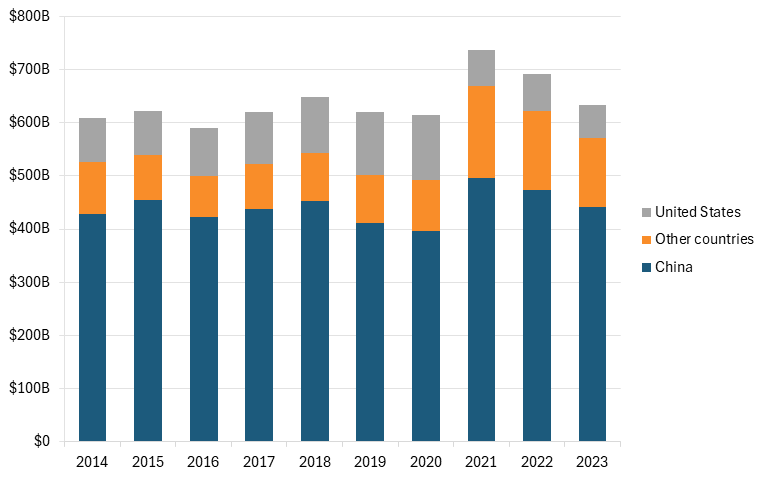

Figure 4 captures 10-year sales from U.S. companies producing in China by destination market. About 10 percent—or $62 billion—of the products and services supplied by U.S. affiliates in the PRC served the U.S. market in 2023, and 21 percent served markets outside China and the United States. The seemingly low share of sales to the U.S. market is explained by the way the data was collected, which does not capture U.S. companies’ production through contract manufacturing (i.e., outsourcing to Chinese companies) or minority-owned joint ventures. Value added would be a preferable measure of production, but BEA does not publish it at the country level disaggregated by destination.

Figure 4: Goods and services supplied by U.S. affiliates by destination (2023 prices)[15]

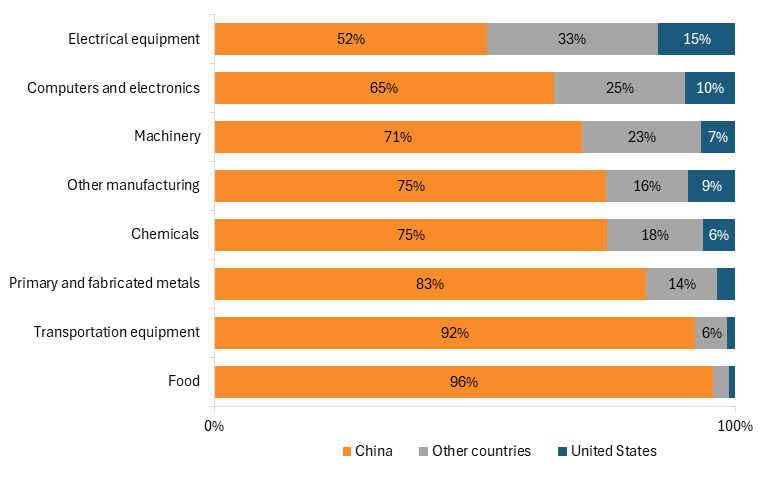

There exists variation among U.S. companies in China across manufacturing industries in how they serve the Chinese market. Figure 5 shows the composition of U.S. affiliates’ sales in China by destination market. U.S. manufacturers of electrical equipment along with those of computers and electronics serve only the Chinese market, representing 52 percent and 65 percent of their total sales, respectively. On the other hand, 96 percent of the sales of U.S. food producers and 92 percent of the sales of U.S. transportation equipment producers in China serve that local market.

Figure 5: Manufacturing goods sold by U.S. affiliates in China, by destination and type of good, 2023[16]

Capital Expenditure and R&D Investments in China

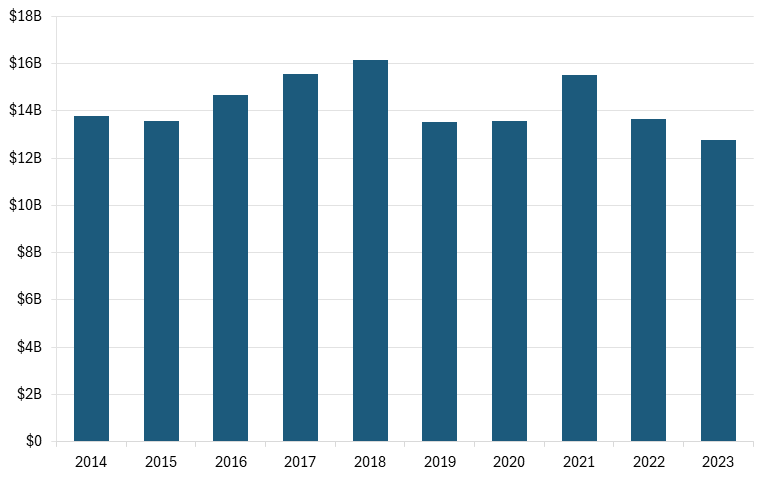

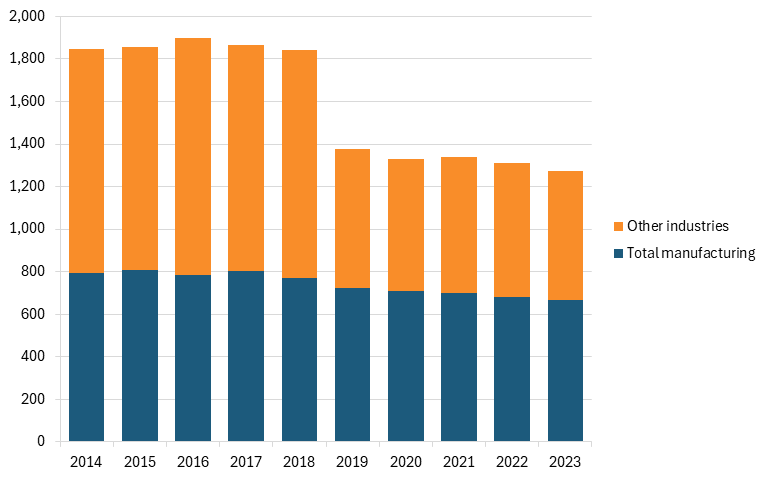

Over the last 10 years, annual capital expenditure by U.S. affiliates in China has fluctuated between $11 billion and $14 billion. Figure 6 shows the expenditure on property, plants, and equipment (capital expenditure or CAPEX) of U.S. companies in China from 2014 to 2023. Despite geopolitical and trade tensions over the past several years, U.S. companies’ capital expenditure in China in 2023 was slightly higher than in 2017.

Figure 6: Expenditures on property, plant, and equipment (CAPEX) of U.S. affiliates in China (2023 prices)

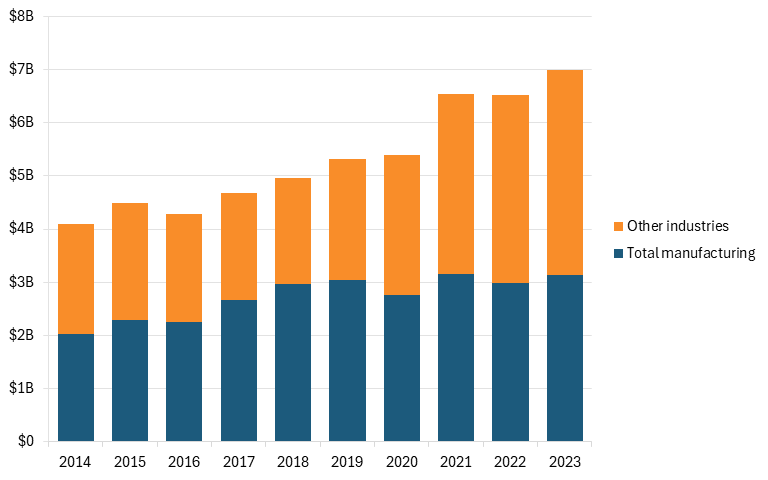

U.S. affiliates in China have more than doubled their R&D investments over the past 10 years. Figure 7 shows that annual R&D investments rose from just over $3 billion in 2014 to nearly $7 billion in 2023. In addition, R&D investments in China by U.S. non-manufacturing industries have increased by nearly 40 percentage points more than those of manufacturing industries. Non-manufacturing industries include information, finance and insurance, mining, professional and scientific services, retail, wholesale trade, and an “other” category.

Figure 7: R&D performed by U.S. affiliates in China (2023 prices)[17]

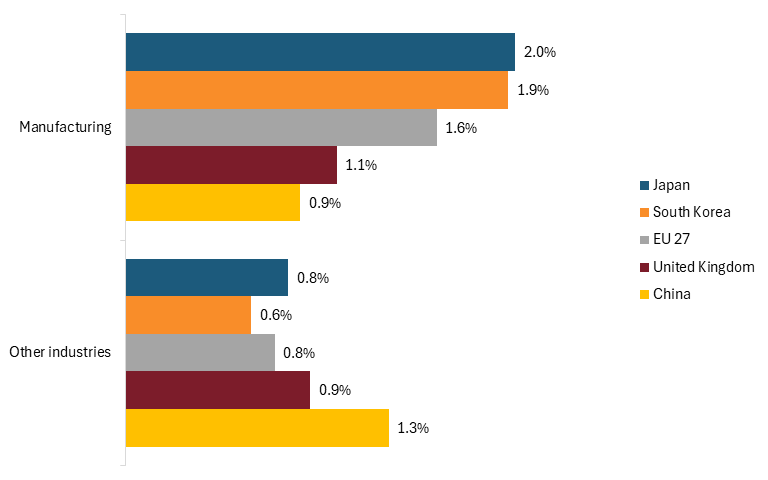

In relative terms, R&D investments by U.S. affiliates in China’s manufacturing industries are considerably lower than in other key markets, but R&D investments in nonmanufacturing industries are relatively higher in China than in other relevant jurisdictions. R&D intensity—the amount of R&D relative to total sales—is an effective measure for comparing R&D expenditure. Although this measure is usually analyzed at the company level, BEA’s dataset enables an overall analysis by sector. In this context, figure 8 displays R&D intensity for manufacturing and nonmanufacturing industries of U.S. companies in China, the European Union, Japan, South Korea, and the United Kingdom. R&D intensity in China’s manufacturing sector is less than half that of Japan and South Korea, and lower than that of any other jurisdiction in this sample. Conversely, R&D intensity in China’s non-manufacturing industries surpasses that of all other markets, as shown in figure 8.

Figure 8: R&D intensity of U.S. affiliates in 2023, by jurisdiction and sector[18]

U.S. Companies’ Employees in China

The trade and geopolitical tensions between the United States and the PRC seem to be reflected in the total number of staff employed by U.S. companies in China. Figure 9 shows that between 2016 and 2023, employment reported by U.S. affiliates in China declined every year, except in 2021, the year of the post-COVID-19 recovery, which still increased by only 1 percent. There was a sharp 25 percent decline in employment between 2018 and 2019, coinciding with the escalation of trade tensions, sanctions against Chinese companies, and increased pressure on U.S. multinationals to diversify their supply chains. BEA data shows that the 2018–2019 decrease occurred in nearly all sectors; still, this decline is explained by over 80 percent by the decrease in employment in “other industries.”

Some scholars point out that job creation by multinational companies (MNCs) in countries with adversarial diplomatic relations—as is the case with the United States and the PRC—may also be a strategy to gain legitimacy. In this context, hiring personnel can strategically “reduce the uncertainty, timing, and costs surrounding the establishment and expansion of R&D centers that could be influenced by bureaucracy and a volatile political landscape. Hence, a job creation strategy can be treated as an insurance policy when managing legitimacy concerns under techno-nationalism.”[19] While this argument might sound reasonable in certain contexts, it contradicts the previously discussed data, as employment at U.S. companies in China has fallen precisely during periods of increased geopolitical and trade tensions.

A significant share of AmCham China members (84 percent) have a top management team composed of at least three-quarters Chinese nationals. For tech and R&D-intensive AmCham China members, the share rises to 93 percent.

All in all, U.S. affiliates employed over 1.2 million people in China in 2023, 52 percent of whom were in the manufacturing sector.

Figure 9: Employment reported by U.S. affiliates in China (in thousands of employees)

Additionally, U.S. companies in China predominantly hire local talent. The American Chamber of Commerce in China (AmCham China) has consistently reported that its members’ top management in China is predominantly native to mainland China. The latest AmCham China 2026 China Business Climate Survey reports that 84 percent of its members have a top management team composed of at least three-quarters Chinese nationals.[20] For tech and R&D-intensive AmCham China members, the share rises to 93 percent.

Profitability of U.S. Companies in China Has Declined in Recent Years

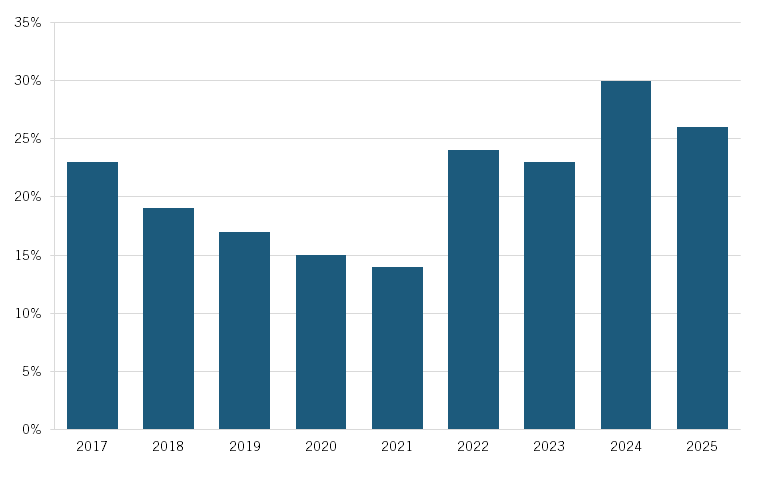

The 2025 annual survey from the U.S.-China Business Council (USCBC), an advocacy group representing 270 American businesses in China, reports that 18 percent of its members’ operations in China were unprofitable. As figure 10 shows, there was an increase in the number of companies reporting losses after 2022, coinciding with the consolidation of U.S. tariffs during the Biden administration and China’s recovery from “zero-COVID-19” controls. In 2022, 87 percent of USCBC members reported that U.S.-China tensions impacted their operations.[21]

Figure 10: Share of USCBC members that had losses in China in the previous year[22]

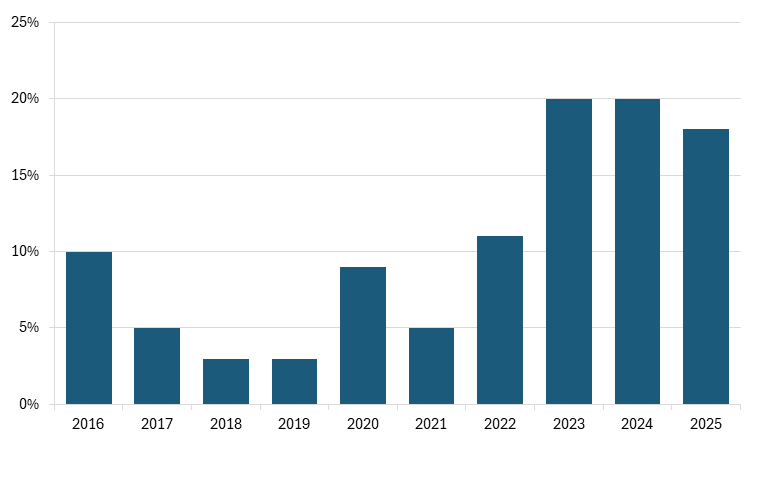

The growing number of U.S. companies in China reporting losses appears to be prompting more firms to consider abandoning their operations in the country. As figure 11 exhibits, AmCham China has reported that, in 2022, 24 percent of U.S. affiliates in China considered or had already begun the process of reshoring outside China—a 71 percent increase from the previous year. Over the last four years (2022–2025), on average, more than one-quarter of U.S. companies in China were considering or had already begun relocating operations outside the country.

Figure 11: Share of U.S. companies with operations in China that are considering or have already begun the process of relocating manufacturing or sourcing outside China[23]

Why It Matters: The Benefits of Having U.S. Companies in China

For the U.S. national interest, there are many advantages to having American companies with a certain presence in the Chinese market, especially if most of that presence focuses on either serving the Chinese market or utilizing China’s key STEM (science, technology, engineering, and math) talent for U.S. corporate R&D and innovation. To be sure, in the short term, U.S. investment in China benefits the Chinese economy by creating jobs, demand for suppliers, and, to a certain extent, new knowledge and training. These are the traditional benefits of foreign direct investment (FDI). But the reality is, if U.S. companies were not serving that market, Chinese companies would and there would be no net change in jobs or sales.

The Geostrategic Context: National Power Industry War

To understand why it is important for U.S. technology companies to be able to operate in China, policymakers also must recognize the broader context of the techno-economic war that China is waging to wrest global leadership from the United States in the advanced, traded-sector industries that provide the foundation for national strength and security in the 21st century.[24]

As ITIF has documented extensively over the past two decades, China’s goal has long been to dominate the very advanced, strategic industries. To achieve its goal, China has not just invested in building up the requisite foundations of its own domestic innovation ecosystem, but also has engaged in a devastatingly effective campaign of innovation mercantilism, subverting the rules of the global trading system by misappropriating foreign intellectual property, forcing technology transfers in foreign direct investments, lavishing subsidies on domestic champions, and other means.[25] As a result, it is now on course to outpace the United States in many advanced industries.[26] Prohibiting U.S. technology companies from operating in China would hasten that outcome by undercutting their global scale and allowing Chinese competitors to step into the void and capture their market share. It may already be too late for the United States to move ahead of China, but it is not too late to avoid falling too far behind.[27]

However, U.S. companies operating in China also benefit America. Although it is not possible to accurately measure these cost benefits, it is possible to analyze them as a matter of national interest.

Access to Scarce STEM Talent

U.S. investments in China can serve as an “offramp” for the best Chinese talent to exit the Chinese ecosystem and contribute to the West. From the PRC government’s perspective, this is a brain drain of its top talent. A 2022 report reveals that 47 percent of top AI talent was produced in China, compared with 18 percent in the United States.[28] Having facilities and affiliates in China helps to access and recruit from the Chinese talent pool. Some U.S. companies are doing this through R&D centers, although at a lower intensity. In 2021, the Center for Security and Emerging Technology (CSET) determined that 10 percent of the AI research labs of Google, IBM, Meta, and Microsoft were in China.[29] (IBM closed its R&D activities in China in 2025.)[30]

These R&D centers utilize Chinese talent, just as a Chinese tech firm operating in Silicon Valley would utilize U.S. talent. This occurs directly (through internal transfers) and indirectly (by building reputation). An example of the latter is Microsoft Research, opened in 1998 in Beijing to “draw on the immense high-tech talent pool in China.”[31] Recent reports suggest that Silicon Valley is no longer an attractive destination for Chinese tech talent, as China now offers appealing professional opportunities, reinforcing the need for U.S. companies to be present in China.[32] Furthermore, a sign that efforts to attract Chinese talent have damaged the Chinese ecosystem is the recent reports of Chinese tech companies attempting to “poach” top talent with Chinese roots currently working in the United States.[33]

U.S. investments in China can serve as an “offramp” for the best Chinese talent to exit the Chinese ecosystem and contribute to the West. From the PRC government’s perspective, this is a brain drain of its top talent.

Chinese Market Revenues

Techno-economic national power is, to a great extent, a zero-sum competition for dominating markets. This is particularly relevant in advanced industries with high fixed costs, wherein scale is crucial to leading, as unit cost depends on it. This cost structure creates a positive spiral. The larger the revenues and the larger the market share, the more resources are available to invest in R&D and new generations of products, which helps companies maintain their existing market share. In a zero-sum context, the revenues U.S. companies can capture and the market share they can gain are resources available for R&D to maintain American leadership and simultaneously represent part of the Chinese market that Chinese companies are not capturing.

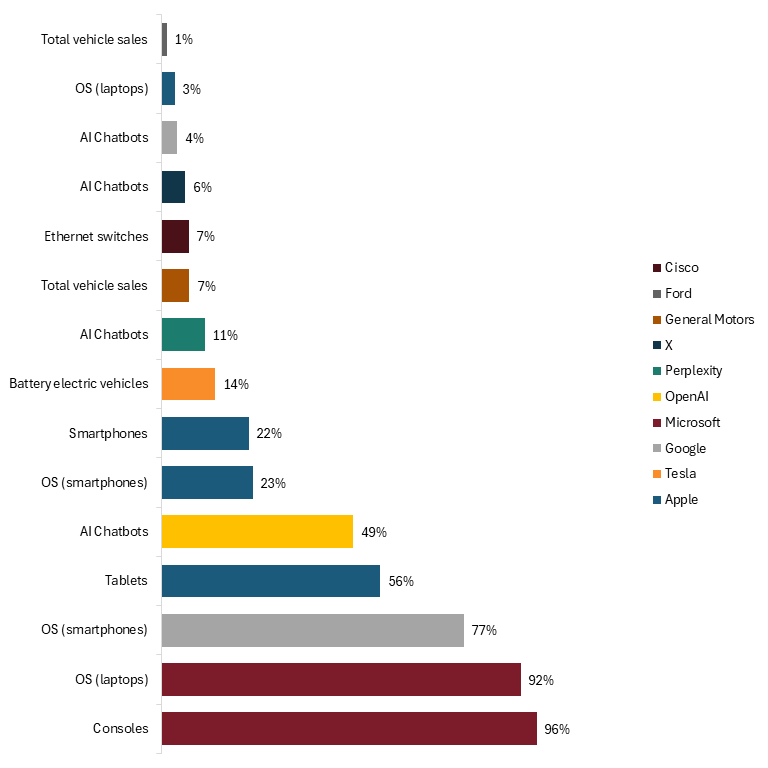

Some U.S. companies have a notable presence in the Chinese market. Figure 12 shows that American firms are particularly strong in gaming devices (i.e., consoles) and operating systems for both laptops and smartphones. However, the market share of U.S. companies in operating systems is not secure. Huawei’s operating system, HarmonyOS, has already been installed in more than a billion devices. Other products of U.S. companies with a relevant market share in China are Apple’s smartphone (22 percent) and Tesla’s EVs (14 percent).

Figure 12: Market share in China for a selected group of U.S. companies, by type of product[34]

* Data for AI chatbots only available for Hong Kong

Revenues from the Chinese market can be reinvested in U.S. R&D activities. Furthermore, to effectively compete in China, companies often need a presence there to gain a deeper understanding of the market.[35] Significant revenues from major markets globally allow U.S. big tech companies to invest more in R&D than most countries and the federal government’s nondefense research budget does, providing the scale necessary to pursue frontier technologies that require massive up-front investment.[36] The relationship works in both ways—more sales increases R&D investment, and more R&D investment boosts firm growth. For example, a recent study of U.S. high-tech companies finds that a high ratio of R&D investment to sales (also known as R&D intensity) can lead to short-term growth and revive the growth of declining firms, allowing firms to further invest in R&D and keep growing.[37]

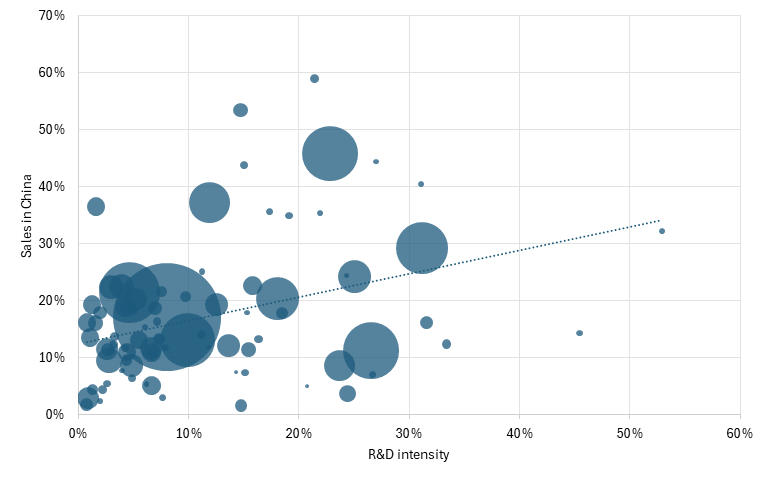

Companies with a larger share of their sales in China tend to have higher R&D intensity.

The data from 173 publicly listed U.S. companies that report sales in China suggests a moderate correlation between sales in China and R&D intensity. Indeed, figure 13 shows companies’ sales in China as a share of total sales (y-axis) and their R&D intensity (x-axis), suggesting that companies with a larger share of their sales in China tend to have higher R&D intensity. There is no relationship between a company’s total sales (bubble size) and the percentage of sales in China or R&D intensity. Additionally—as shown in the characterization of U.S. companies with activities in China—they tend to invest less in R&D in China than in other jurisdictions, such as the EU, Japan, South Korea, or the United Kingdom. This suggests the likelihood that a larger share of sales in China is allocated to R&D investment elsewhere, including in the United States, than to U.S. activities in other countries.

Figure 13: Correlation between sales in China and R&D intensity (2024)[38]

The Chinese Market as a “Listening Post”: Outward FDI Spillovers

The Chinese market can serve U.S. companies as a source for corporate intelligence—to better know consumers and technological trends, learn from peer companies, and generally identify “what’s happening” in the world’s largest economy. There is evidence that American companies in China are implementing this strategy. For example, Caterpillar, an American construction and mining equipment manufacturer, promotes its Caterpillar China R&D Center as a means to “get closer to customers and take advantage of regional engineering talent to develop leading products.”[39]

A hypothesis regarding the value of outward spillovers is that “outward FDI provides a way to source new technologies in foreign countries.” In other words, foreign investment can serve as a “listening post.”

Ford has officially acknowledged the value of the Chinese market to keep pace with vehicle electrification and market demand trends. This is reflected in specific product improvements. For example, in 2021, the company signaled that it would incorporate a “unique smart digital cabin experience” in response to “feedback from Chinese customers.”[40] Ford operates in China through a joint venture with Changan, a Chinese automaker, called Changan Ford Automobile Co, established in 2001. ITIF has previously reported how Ford established its operations in China under nonmarket conditions; for example, when Ford sought to open a production facility in China, “the Chinese government required Ford to open an R&D laboratory employing at least 150 Chinese engineers.”[41]

This learning process is also understood as reverse spillovers. There is a vast body of academic literature demonstrating the spillover benefits of FDI for local capabilities. As inward foreign investment often brings new technologies, knowledge, and managerial practices, local firms slowly adopt these techniques and improve their productivity. Conversely, a subset of this literature examines “outward FDI spillovers”—the notion that FDI also has positive effects on the country of origin. This concept is also known as “reverse technology spillover.” A hypothesis regarding the value of outward spillovers is that “outward FDI provides a way to source new technologies in foreign countries.” In other words, foreign investment can serve as a “listening post.”[42]

Chinese foreign investment has indeed benefited from reverse spillovers, and Chinese scholars have advanced conceptualizations of the mechanisms by which knowledge is transferred from Chinese MNCs investing abroad back to mainland China. Li and authors, for example, have proposed that reverse spillovers can occur in three stages of FDI: during acquisition or investment deployment, during a so-called transfer stage, and during the diffusion stage.[43] Table 1 summarizes the different mechanisms through which reverse technology spillover can occur and the benefits to the economy of the MNCs’ headquarters’ countries. These spillovers also apply to U.S. companies investing overseas, especially in countries with a scale and technological sophistication similar to China market.

Table 1: Stages of the process of reverse technology spillover[44]

|

Stage |

Main mechanism |

How it works |

|

Technology acquisition |

Cross-border M&As |

MNCs use outward FDI to obtain patents, production processes, R&D capabilities, and tacit knowledge from foreign markets. |

|

Overseas R&D cooperation |

MNCs establish R&D centers overseas and collaborate with local universities to access advanced resources and monitor frontier technological developments. |

|

|

Industrial agglomeration |

MNCs invest to enter technology-intensive industrial clusters abroad, where proximity to other advanced firms enables learning, communication, and imitation. |

|

|

Technology transfer |

Knowledge transfer from subsidiary to parent company |

A foreign subsidiary sends information, technical knowledge, and R&D results back to headquarters, where its parent firm absorbs and applies them. |

|

Government policy incentives |

Governments create preferential policies for MNCs investing in advanced-technology sectors overseas to decrease investment costs and attract talent from abroad. |

|

|

Two-way personnel flow |

MNCs send domestic technicians overseas for training to master overseas skills and then return to apply what they have learned. Conversely, a parent company can also directly introduce talents from an overseas subsidiary to exchange and work domestically. |

|

|

Technology diffusion |

Screening and selection |

MNCs identify which foreign technologies are valuable and suitable for domestic use. |

|

Localization and adaptation |

MNCs localize imported technologies and integrate them into production processes. |

|

|

Application |

Adapted technologies are deployed across a parent company and potentially the wider domestic industry. |

Presence in China to Lock In the Chinese Market With U.S.-Built Ecosystems

The diffusion of certain U.S. technologies into the Chinese ecosystem is itself a benefit to American companies. The widespread use of U.S.-built tools, such as operating systems and frameworks required to operate in certain semiconductor ecosystems, has the potential to effectively “lock in” parts of the Chinese market’s supply chain. In other words, the diffusion of U.S. technologies can accustom Chinese suppliers, companies, and talent to working within ecosystems that reinforce American companies’ leadership, thereby increasing the costs of operating under other frameworks.

An example is PaddlePaddle, a deep-learning platform primarily oriented toward Chinese users and developers.[45] NVIDIA supports this tool through its graphics processing unit (GPU) software ecosystem, allowing users to build and scale workloads using NVIDIA chips—reinforcing the lock-in on NVIDIA’s stack.[46] It has been reported that PaddlePaddle serves more than 23.3 million developers and 760,000 companies and generates 1,100,000 models.[47]

The case of U.S. dominance in laptop and smartphone operating systems illustrates dominance within specific ecosystems. As intermediaries between hardware, applications, and users, operating systems define how devices work. Switching from one operating system to another is costly and time-consuming for users. For service firms, even updating their operating system to a new generation of the same brand entails high costs (which can be recovered in about a year and a half).[48] For smartphone users, the average estimated cost of switching from one operating system to another is roughly 45 percent of the mean smartphone price.[49] On the other hand, competing against established operating systems requires large investments with uncertain returns. Huawei has been investing in developing its in-house operating system, HarmonyOS, since 2012, and was technically forced to launch it in 2019 due to U.S. export controls that limited Huawei’s access to American technologies.[50] HarmonyOS is used in more than one billion devices in China, which demonstrates both how difficult it is for a company to compete with existing players in this market and how shortsighted U.S. policies can undermine American dominance in the Chinese market.

The reliance of the Commercial Aircraft Corporation of China (COMAC), a leading Chinese aircraft manufacturer, on American technology for the engines of its main product, the C919, clearly illustrates how American technology sold in the Chinese market can provide leverage for U.S. companies. COMAC’s history and the Chinese government’s financial support, along with subsidized domestic demand for the C919 aircraft, are well-reported.[51] The majority shareholder of COMAC is the Aviation Industry Corporation of China (AVIC), a Chinese state-owned aerospace and defense conglomerate. The C919 model is equipped with two LEAP-1C engines, produced by CFM International, a joint venture between GE Aerospace and Safran Aircraft Engines.[52] While GE Aerospace has a decades-long presence in China and reports having trained over 10,000 mechanics, the LEAP-1C is manufactured and exported from the United States.[53]

The examples of how China is subsidizing and intervening in its markets in favor of Huawei and COMAC reveal both how difficult it is to change once a technology is locked in and how the PRC is undertaking massive efforts to break the dependency on U.S. technologies.

The United States is not exempt from dependencies on Chinese goods in its supply chain. Many of the U.S. economy’s internal value chains remain anchored in China. Despite recent reshoring efforts, such as the “China-Plus-One” strategy—a supply chain management strategy in which a firm retains substantial production capacity in China while shifting production to at least one other country to reduce risk.[54] This reflects the strategic value of locking in, as doing so significantly increases switching costs, making the status quo economically preferable to jumping to other ecosystems or supply chains.

The fact that U.S. presence in China benefits the United States is reflected in PRC policy. The CCP won’t allow any foreign company to have a dominant market share in its local market in the long term—especially Western companies in strategic industries. Part of China’s strategy is to become technologically self-reliant by explicitly supporting domestic companies.[55] There is no room for relative growth of foreign companies in this context. China seeks to “carve out and protect the Chinese market for Chinese firms, excluding foreign competitors once domestic champions can reasonably serve the entire Chinese market.”[56]

There are precedents in which the PRC government has forced foreign competitors to scale back their operations to privilege Chinese companies. ITIF has reported that China’s protectionism and active non-market policies—such as currency manipulation, preferential treatment of local companies through subsidies and procurement, and tax incentives—have reduced the market share of Ericsson and Nokia in both the Chinese and global markets.[57] Furthermore, the reduced market share that European companies enjoy in the Chinese telecommunications market reflects a strategy to coerce and exert leverage over European governments.[58] Thus, the minimization of foreign companies’ role in the Chinese market is a key feature of China’s innovation mercantilism: enjoying open market conditions overseas while imposing discriminatory and protectionist measures to capture the local market and later compete globally.

Criticism Against U.S. Companies Operating in China

U.S. companies have been subject to scrutiny, criticism, and even boycott campaigns for their activities in the PRC. One of the most significant cases is Google’s attempt to re-enter the Chinese market during the late 2010s—because it was blocked by the Chinese authorities—with a search engine tool coded Project Dragonfly, tailored to comply with the PRC’s censorship rules.[59] Google controlled 40 percent of the Chinese search market before shutting down in 2010, and its exit “enabled Baidu to comfortably conquer the market.”[60] Project Dragonfly, which was canceled, faced opposition primarily from Google employees who were reluctant to be involved in a project that would “help China suppress free expression.”[61] This initiative also faced political opposition in the United States.[62] Indeed, the PRC is an authoritarian regime that overtly restricts access to information, but whether a U.S.-based company provides PRC-compliant tools has no negative impact on censorship.

Many other companies have faced criticism for their activities in China. Some of these arguments equate U.S. companies with repressive PRC practices, for example, in forced labor supply chains. As previously mentioned in this report, U.S. companies should not be involved in supply chains that work under forced labor. There is space for policy improvement in this issue.

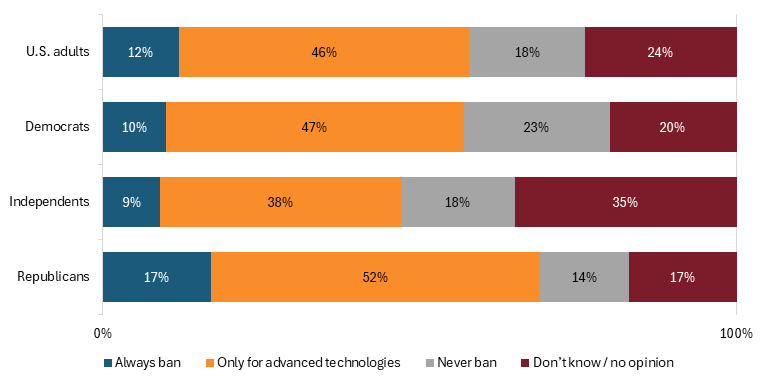

More Americans agree that there should never be a ban on U.S. companies investing in China (18 percent) than favor a blanket ban (12 percent), and a significant share supports a narrow restriction focused only on advanced technologies (46 percent).

The Department of Homeland Security has released the “Uyghur Forced Labor Prevention Act Entity List” (UFLPA Entity List), a list of companies associated with human rights violations in the PRC that are fully prohibited from entering the U.S. market or exporting goods to the United States.[63] The UFLPA Entity List has been effective in deterring U.S. companies from doing business with listed firms and creating reputational costs.[64] However, since this is mostly an import ban, there are no theoretical limitations on U.S. companies doing business with Chinese companies on the UFLPA Entity List overseas, as long as neither the production nor its output enters the United States.

However, U.S. citizens’ views on China are generally nuanced. Most Americans (79 percent) express that they are worried about China’s unfair trade practices, according to a 2025 survey conducted by the Reagan Institute.[65] Yet another 2025 survey by the Chicago Council on Global Affairs also found that a majority of U.S. citizens believe the United States should maintain “friendly” cooperation and engagement with China.[66] In terms of economic relations, only 15 percent of Americans support a complete ban on Chinese companies doing business in the United States, according to Morning Consult.[67] Conversely, more Americans agree that there should never be a ban on U.S. companies investing in China (18 percent) than favor a blanket ban (12 percent), and a significant share supports a narrow restriction focused only on advanced technologies (46 percent), according to Morning Consult.[68] Figure 14 shows that there is generally bipartisan agreement on a narrow ban on advanced technologies involving U.S. companies in China. (Republicans are more in favor of a total ban of U.S. companies in China than no bans at all, but within the survey’s 3 percentage-point margin of error.)

Figure 14: Americans’ support for banning U.S. companies from investing in China[69]

Policy Recommendations

Techno-economic realism—the pragmatic notion of using science, technology, and innovation to advance U.S. national power by improving America’s productive capacity and gaining a strategic advantage over China—should supersede idealism. Some analysts define the idealist view of foreign policy as advocating the reflection of a country’s internal values in its approach to others. Yet, banning American companies from operating in China—beyond certain technology rules and from supply chains that rely on human rights violations—reflects values rather than outcomes. As ITIF has stated before, “It does not make human rights in China better if U.S. technology companies are not there.”[70]

The U.S. government should continue to update clear boundaries around the narrow set of technologies and knowledge to be restricted from China and specify which companies are blacklisted, such as those with links to the Chinese military or to forced-labor practices. However, not every economic activity or transaction in China poses a national security risk.

The nuanced views of the American people seem to recognize that U.S. companies operating in China under narrow, well-defined restrictions on advanced technologies serve U.S. interests. This is a narrative that is missing in Washington. The policy messaging should follow Americans’ views—having U.S. companies operating in China to serve the Chinese market is perfectly compatible with (and often advances) American interests, and policy tools could accelerate the offshoring of production to other markets to minimize the positive spillover benefits. If U.S. policymakers or public campaigns push companies to leave China, it will have a positive impact on the PRC—sales and market share would likely be captured by Chinese companies, and the established production capacity would remain in China.

The nuanced views of the American people seem to recognize that U.S. companies operating in China under narrow, well-defined restrictions on advanced technologies serve U.S. interests. This is a narrative that is missing in Washington.

U.S. policymakers can implement policy actions to improve how U.S. companies operate in China, aligned with the view that advanced technologies should be restricted, and to incentivize the offshoring of production that does not serve the Chinese market. For example:

▪ To prevent “asymmetric competition,” the U.S. Office of the Trade Representative (USTR) should use Section 301 of the Trade Act authorities to enforce “immediate reciprocity,” banning Chinese companies from the U.S. market in sectors where U.S. companies lack access to the Chinese market.[71] USTR should consider using Section 301 import controls to address Chinese sectors that restrict or limit access for foreign competitors. A clear example of this is social media platforms, where U.S. companies are barred from entering the Chinese market. If there are clear instances where U.S. firms are being wholesale blocked from competing in China’s market, then the United States should impose the same conditions on Chinese firms that would compete in the U.S. market.

▪ The U.S. Securities and Exchange Commission (SEC) should require a more standardized reporting of U.S. activities in China. As this report discusses, publicly listed companies are only required to report revenues for the United States, and for the rest of the world as a whole, whereas they may disclose regional or country-level information at their discretion. Form 10-K, which reports annual activities, should require companies to disclose at least the revenues and the number of full-time employees in China, including Hong Kong.

▪ The Department of State should establish an expedited green card pathway for temporary visa holders, particularly those graduating in computer science and engineering, as doing so would directly strengthen the U.S. workforce at a time of acute demand.[72] Such a policy would allow the United States to retain top Chinese talent already trained and already contributing to domestic research labs, university programs, and industrial innovation.

Conclusion

The debate among U.S. policymakers should not focus on whether American companies should fully withdraw from China or treat the PRC as just another market economy. Instead, it should center on whether U.S. company affiliates, operating within narrow, clearly defined national security limits, can participate in the Chinese ecosystem in ways that serve the national interest. This report highlights at least four compelling reasons to support this view: it provides access to China’s top talent, it allows for the capturing of revenues and market share that would otherwise go to Chinese companies, it fosters reverse technology spillovers that benefit the U.S. economy; and it helps lock in certain U.S. technologies among Chinese firms and consumers—making reverse engineering costly for them.

Acknowledgments

The author would like to thank Robert Atkinson, Stephen Ezell, Chris Gragg, Trelysa Long, and Meghan Ostertag for sharing insights.

About the Author

Rodrigo Balbontin is an associate director covering trade, IP, and digital technology governance at ITIF. He has extensive experience in policy design and research on science, technology, and innovation governance in the Americas and the Asia-Pacific regions. He earned a master’s degree in science and technology policy from the University of Sussex and a bachelor’s degree in economics from the University of Chile.

About ITIF

The Information Technology and Innovation Foundation (ITIF) is an independent 501(c)(3) nonprofit, nonpartisan research and educational institute that has been recognized repeatedly as the world’s leading think tank for science and technology policy. Its mission is to formulate, evaluate, and promote policy solutions that accelerate innovation and boost productivity to spur growth, opportunity, and progress. For more information, visit itif.org/about.

Endnotes

[1]. Rick Scott, “Sen. Rick Scott to Business Leaders: Decouple From Communist China Before its Planned Invasion of Taiwan,” press release, March 17, 2022, https://www.rickscott.senate.gov/2022/3/sen-rick-scott-to-business-leaders-decouple-from-communist-china-before-its-planned-invasion-of-taiwan.

[2]. Donald Trump (@realDonaldTrump), X post, August 23, 2019, https://x.com/realDonaldTrump/status/1164914959131848705.

[3]. “US companies in China struggle with raids, slow deal approvals, anti-espionage law,” Reuters, August 29, 2023, https://www.reuters.com/business/raids-exit-bans-us-companies-face-growing-hurdles-china-2023-08-29/.

[4]. Kenneth Rapoza, “House Committee on the CCP Says China Risks are Rising for American Companies,” Coalition for a Prosperous America, July 19, 2023, https://prosperousamerica.org/house-select-committee-ccp-hearing-china-risks-elevated/.

[5]. “About,” The US-China Business Council, accessed March 10, 2026, https://www.uschina.org/about/.

[6]. Bureau of Economic Analysis, Worldwide Activities of U.S. Multinational Enterprises: Preliminary 2023 Statistics, accessed February 20, 2026, https://www.bea.gov/worldwide-activities-us-multinational-enterprises-preliminary-2023-statistics.

[7]. Bureau of Economic Analysis, Worldwide Activities of U.S. Multinational Enterprises: Preliminary 2023 Statistics, accessed February 20, 2026, https://www.bea.gov/international/usdia2023p-info.

[8]. “Fresh Data on China Revenue Exposure,” Calcbench Blog, March 11, 2025, https://www.calcbench.com/blog/post/blogger8039018928154968118/Fresh-Data-on-China-Revenue-Exposure.

[9]. Oracle Corporation, Oracle Corporation Fiscal Year 2025 Form 10-K Annual Report (Austin, Texas: Oracle Corporation, 2025), https://d18rn0p25nwr6d.cloudfront.net/CIK-0001341439/7455eba6-bb80-41d3-96b7-12111eae648c.pdf; “APAC Field Offices,” Oracle APAC, accessed March 6, 2026, https://www.oracle.com/apac/corporate/contact/field-offices/#china.

[10]. “AmCham Shanghai Releases 2021 China Business Report,” AmCham Shanghai, September 22, 2021, https://www.amcham-shanghai.org/en/article/amcham-shanghai-releases-2021-china-business-report.

[11]. Bureau of Economic Analysis, Worldwide Activities of U.S. Multinational Enterprises; 2023 prices were calculated using the Federal Reserve Bank of St. Louis’s Gross Domestic Product: Implicit Price Deflator, https://fred.stlouisfed.org/series/GDPDEF#.

[12]. “Fresh Data on China Revenue Exposure,” Calcbench Blog.

[13]. Based on each company’s 10-K annual report for 2025.

[14]. Own elaboration based on Calcbench data.

[15]. Bureau of Economic Analysis, Worldwide Activities of U.S. Multinational Enterprises; 2023 prices are calculated using the Federal Reserve Bank of St. Louis’s Gross Domestic Product: Implicit Price Deflator, https://fred.stlouisfed.org/series/GDPDEF#.

[16]. Ibid.

[17]. Ibid.

[18]. Ibid.

[19]. Hyungseok David Yoon et al., “More jobs for our foes? Global R&D strategy in the age of techno-nationalism,” Research Policy 54, no. 4 (May 2025): 105196, https://doi.org/10.1016/j.respol.2025.105196.

[20]. AmCham China, 2026 China Business Climate Survey Report (AmCham China, January 2026), https://www.amchamchina.org/wp-content/uploads/2026/01/BCS2026.pdf.

[21]. US-China Business Council, “Member Survey 2022” (US-China Business Council, August 26, 2022), https://www.uschina.org/wp-content/uploads/2022/08/uscbc_member_survey_2022-1.pdf.

[22]. US-China Business Council, “Member Survey 2025” (US-China Business Council, July 16, 2025), https://www.uschina.org/wp-content/uploads/2025/07/2025-Member-Survey-EN-1.pdf.

[23]. “Business Climate Surveys,” AmCham China, accessed March 6, 2026.

[24]. Robert D. Atkinson, “Marshaling National Power Industries to Preserve America’s Strength and Thwart China’s Bid for Global Dominance” (ITIF, November 2025), https://itif.org/publications/2025/11/17/marshaling-national-power-industries-to-preserve-us-strength-and-thwart-china/.

[25]. Robert D. Atkinson, “Why China Needs To End Its Economic Mercantilism,” HuffPost, January 30, 2008, https://www.huffpost.com/entry/why-china-needs-to-end-it_b_84028; Robert D. Atkinson, “Enough is Enough: Confronting Chinese Innovation Mercantilism” (ITIF, February 2012), https://itif.org/publications/2012/02/28/enough-enough-confronting-chinese-innovation-mercantilism/; Robert D. Atkinson and Stephen Ezell, “False Promises: The Yawning Gap Between China’s WTO Commitments and Practices” (ITIF, September 2015), https://itif.org/publications/2015/09/17/false-promises-yawning-gap-between-chinas-wto-commitments-and-practices/; Stephen Ezell, “False Promises II: The Continuing Gap Between China’s WTO Commitments and Its Practices” (ITIF, July 2021), https://itif.org/publications/2021/07/26/false-promises-ii-continuing-gap-between-chinas-wto-commitments-and-its/.

[26]. Robert D. Atkinson, “China Is Rapidly Becoming a Leading Innovator in Advanced Industries” (ITIF, September 2024), https://itif.org/publications/2024/09/16/china-is-rapidly-becoming-a-leading-innovator-in-advanced-industries/; Meghan Ostertag, “US National Power Industries Are at Risk” (ITIF, November 2025), https://itif.org/publications/2025/11/17/us-national-power-industries-are-at-risk/.

[27]. Robert D. Atkinson, “Mobilizing for Techno-Economic War, Part 1: The Case for Policy Transformation” (ITIF, February 2026), https://itif.org/publications/2026/02/02/mobilizing-for-techno-economic-war-part-1-the-case-for-policy-transformation/.

[28]. Yingyi Ma, “US security and immigration policies threaten its AI leadership,” Brookings, April 4, 2024, https://www.brookings.edu/articles/us-security-and-immigration-policies-threaten-its-ai-leadership/.

[29]. Bill Drexel and Klon Kitchen, “Pull US AI Research Out of China,” Defense One, August 10, 2021, https://cset.georgetown.edu/article/pull-us-ai-research-out-of-china/.

[30]. Kate Irwin, “IBM Pulls Research Operations Out of China, Lays Off 1,000 Employees,” PCMag, August 26, 2024, https://www.pcmag.com/news/ibm-pulls-research-operations-out-of-china-lays-off-1000-employees.

[31]. “Celebrating 20 years of MSR in Asia with Dr. Hsiao-Wuen Hon,” Microsoft Research Podcast, Microsoft Research, November 7, 2018, https://www.microsoft.com/en-us/research/podcast/celebrating-20-years-of-msr-in-asia-with-dr-hsiao-wuen-hon/.

[32]. Viola Zhou, “DeepSeek’s rise shows why China’s top AI talent is skipping Silicon Valley,” Rest of World, February 5, 2025, https://restofworld.org/2025/china-ai-talent-deepseek-rise-us-dominance/.

[33]. Coco Feng, “China’s tech giants pursue AI, semiconductor talent in US as competition intensifies,” South China Morning Post, February 21, 2026, https://www.scmp.com/tech/big-tech/article/3344212/chinas-tech-giants-pursue-ai-semiconductor-talent-us-competition-intensifies.

[34]. “Statcounter Global Stats,” accessed March 6, 2026, https://gs.statcounter.com/; “Website Traffic Checker,” Similarweb, accessed March 10, 2026, https://www.similarweb.com/website/; General Motors Company, Form 10-K Annual Report for the Fiscal Year Ended December 31, 2025 (General Motors Company, January 27, 2026), https://investor.gm.com/static-files/90d2621e-4571-4431-87a1-5ff3035894f6; Ford Motor Company, Form 10-K Annual Report for the Fiscal Year Ended December 31, 2025 (Ford Motor Company, February 10, 2026), https://d18rn0p25nwr6d.cloudfront.net/CIK-0000037996/34de982b-4464-440c-b0a8-7e1b7a0e02b9.pdf; Elina Gong, “2023 Q1 China Ethernet Switch Market Report: H3C wins, Huawei follows closely behind!,” Router Switch Blog, July 17, 2023, https://blog.router-switch.com/2023/07/2023_q1_china_ethernet_switch_market_report_h3c_wins_huawei_follows_closely_behind/.

[35]. Daniel Zipser et al., “2023 McKinsey China Consumer Report: A Time of Resilience,” McKinsey, December 8, 2022, https://www.mckinsey.com/cn/our-insights/our-insights/2023-mckinsey-china-consumer-report.

[36]. Hilal Aka, “Tip of the Iceberg: Understanding the Full Depth of Big Tech’s Contribution to US Innovation and Competitiveness” (ITIF, October 6, 2025), https://itif.org/publications/2025/10/06/tip-of-the-iceberg-understanding-big-techs-contribution-us-innovation-competitiveness/.

[37]. Drini Morina, Henning Lucas, and Stefanie Heiden, “Unraveling the impact of R&D investment on corporate growth: Empirical insights on intensity- and growth rate-based differences,” Finance Research Letters 74 (March 2025): 106722, https://doi.org/10.1016/j.frl.2024.106722.

[38]. Elisabeth Nindl et al., “2025 EU Industrial R&D Investment Scoreboard” (European Commission, December 22, 2025), https://iri.jrc.ec.europa.eu/scoreboard/2025-eu-industrial-rd-investment-scoreboard; “Fresh Data on China Revenue Exposure,” Calcbench Blog, March 11, 2025.

[39]. “Caterpillar China Facilities,” Caterpillar, accessed March 10, 2026, https://www.caterpillar.com/en/company/global-footprint/china/china-facilities.html.

[40]. “Ford EVOS Premieres at Auto Shanghai; Accelerates China 2.0 Plan for Electrification, Intelligence and Customer Experience,” Ford Media Center, April 18, 2021, https://media.ford.com/content/fordmedia/fap/cn/en/news/2021/04/19/ford-evos-premieres-at-auto-shanghai.html.

[41]. Robert D. Atkinson and Stephen Ezell, Innovation Economics: The Race for Global Advantage (New Haven, Connecticut: Yale University Press, 2011).

[42]. Wolfgang Keller, “Knowledge Spillovers, Trade, and FDI” (working paper 28739, National Bureau of Economic Research, April 2021), http://www.nber.org/papers/w28739.

[43]. Yan Li et al., “The Influence of Reverse Technology Spillover of Outward Foreign Direct Investment on Green Total Factor Productivity in China’s Manufacturing Industry,” Sustainability 14, no. 24 (December 9, 2022): 16496, https://doi.org/10.3390/su142416496.

[44]. Ibid.

[45]. “NVIDIA NGC Catalog: PaddlePaddle 24.12-py3,” NVIDIA, accessed March 20, 2026, https://catalog.ngc.nvidia.com/orgs/nvidia/containers/paddlepaddle?version=24.12-py3.

[46]. NVIDIA, PaddlePaddle Release Notes (March 2026), https://docs.nvidia.com/deeplearning/frameworks/pdf/PaddlePaddle-Release-Notes.pdf.

[47]. PaddlePaddle, “Paddle,” GitHub, accessed March 20, 2026, https://github.com/PaddlePaddle/Paddle.

[48]. Forrester Consulting, “The Total Economic Impact™ of Microsoft Windows 11 Enterprise: Cost Savings and Business Benefits Enabled by Windows 11 Enterprise” (commissioned by Microsoft, March 2024), https://tei.forrester.com/go/microsoft/windows11enterprise/docs/The-Total-Economic-Impact-Of-Microsoft-Windows11Enterprise-March2024.pdf.

[49]. Seungwhan Chun, “State Dependence and Complementarities in Smartphone Choices” (job market paper, October 28, 2025), https://tarheels.live/swchun/wp-content/uploads/sites/7672/2025/10/JMP_swchun-18.pdf.

[50]. Rodrigo Balbontin, “Backfire: Export Controls Helped Huawei and Hurt U.S. Firms” (ITIF, October 2025), https://itif.org/publications/2025/10/27/backfire-export-controls-helped-huawei-and-hurt-us-firms/.

[51]. Trelysa Long, “Tracking R&D Leadership: US Advantage Narrowing as China Gains Ground” (ITIF, February 2026), https://itif.org/publications/2026/02/09/tracking-rd-leadership-us-advantage-narrowing-as-china-gains-ground/.

[52]. Commercial Aircraft Corporation of China, C919 Aircraft Characteristics for Airport Planning (ACAP) (October 17, 2025), https://www.comac.cc/fujian/c919acap_en.pdf.

[53]. “Overview,” GE Aerospace, accessed March 6, 2026, https://www.geaerospace.com/overview-china; “GE Aerospace LEAP Engine Facility,” CSO, accessed March 6, 2026, https://www.csoinc.net/projects/ge-aviation-leap-engine-facility/.

[54]. Eli Clemens, “Internal Value Chains Remain Dependent on China Even as Multinationals Shift Production to America” (ITIF, February 23, 2026), https://itif.org/publications/2026/02/23/internal-value-chains-dependent-china-multinationals-shift-production-to-america/.

[55]. Rogier Creemers et al., “Translation: 14th Five-Year Plan for National Informatization – Dec. 2021,” DigiChina, January 24, 2022, https://digichina.stanford.edu/work/translation-14th-five-year-plan-for-national-informatization-dec-2021/.

[56]. Atkinson, “Marshaling National Power Industries.”

[57]. Robert D. Atkinson, “How China’s Mercantilist Policies Have Undermined Global Innovation in the Telecom Equipment Industry” (ITIF, June 22, 2020), https://itif.org/publications/2020/06/22/how-chinas-mercantilist-policies-have-undermined-global-innovation-telecom/.

[58]. Ibid.

[59]. “Google’s Project Dragonfly ‘terminated’ in China,” BBC News, July 17, 2019, https://www.bbc.com/news/technology-49015516.

[60]. Leo Sun, “Google Abandons Its Chinese Search Engine...but Not the Chinese Market,” The Motley Fool, December 20, 2018, https://www.fool.com/investing/2018/12/20/google-abandons-its-chinese-search-engine-but-not.aspx.

[61]. “Google employees criticise ‘censored China search engine’,” BBC News, August 16, 2018, https://www.bbc.com/news/business-45216554.

[62]. Ryan Gallagher, “Google’s Secret China Project ‘Effectively Ended’ After Internal Confrontation,” The Intercept, December 17, 2018,https://theintercept.com/2018/12/17/google-china-censored-search-engine-2/.

[63]. “Uyghur Forced Labor Prevention Act Entity List,” U.S. Department of Homeland Security, accessed March 6, 2026, https://www.dhs.gov/uflpa-entity-list.

[64]. Laura T. Murphy and Charlotte Tate, “Assessing the Impact of the Uyghur Forced Labor Prevention Act After Three Years” (CSIS, August 29, 2025), https://www.csis.org/analysis/assessing-impact-uyghur-forced-labor-prevention-act-after-three-years.

[65]. Ronald Reagan Institute, “Reagan Institute Summer Survey” (Ronald Reagan Institute, summer 2025), https://www.reaganfoundation.org/cms/assets/1750606380-rri_2025-summer-survey_digital_pages.pdf.

[66]. Dina Smeltz et al., “The Growing Partisan Divide on US Foreign Policy” (The Chicago Council on Global Affairs, January 28, 2026), https://globalaffairs.org/sites/default/files/2026-02/2025%20Chicago%20Council%20Survey%20Annual%20Report_2.pdf.

[67]. “Tracking American Sentiment on U.S.-China Relations,” Morning Consult, accessed March 10, 2026, https://pro.morningconsult.com/trackers/tracking-us-china-relations.

[68]. Ibid.

[69]. Ibid.

[70]. Robert D. Atkinson and Nigel Cory, “Time for Competitive Realism,” The International Economy, Winter 2023, https://www2.itif.org/2023-tie-competitive-realism.pdf.

[71]. Rodrigo Balbontin, Eli Clemens, and Stephen Ezell, “Comments to USTR for Its Section 301 Investigation of China’s Implementation of Commitments Under the Phase One Agreement,” December 1, 2025, https://itif.org/publications/2025/12/01/comments-to-ustr-section-301-chinas-implementation-of-poa-commitments/.

[72]. Trelysa Long, “The United States Should Retain International Graduates to Meet Demand for STEM Talent,” ITIF, December 23, 2025, https://itif.org/publications/2025/12/23/the-united-states-should-retain-international-graduates-to-meet-demand-for-stem-talent/.

Editors’ Recommendations

September 16, 2024

China Is Rapidly Becoming a Leading Innovator in Advanced Industries

November 17, 2025

US National Power Industries Are at Risk

January 30, 2008

Why China Needs To End Its Economic Mercantilism

February 28, 2012