Investments in research and development drive innovation, growth, and competitiveness. Moreover, the lion’s share of the benefits from these investments accrues to society, not to individual firms, so tax incentives that encourage such expenditures serve as an important public good. Yet the tax provision allowing firms to fully expense their research and development (R&D) costs in the year of investment expired at the end of 2021, decreasing firms’ incentive to invest in this key driver of economic growth and competitiveness.

Indeed, data from the National Science Foundation shows that the business sector’s annual increase in R&D investment since the expiration of full R&D expensing is only a fraction of what it was beforehand. Congress should pass the American Innovation and R&D Competitiveness Act of 2025 to restore the immediate deductibility of R&D expenses.

The loss of full R&D expensing disincentivizes firms from significantly increasing their R&D investments because the cost of those investments has risen. As a previous ITIF report explains, under full expensing, a firm that spends $50,000 on R&D in the first year can deduct the full real value of the expense from its taxable income. However, under a depreciation schedule, the deduction is spread across ten years as ten $5,000 deductions. The value of each $5,000 deduction diminishes over time, reducing the real value of the total deduction. Under such a depreciation schedule, the firm would be able to write off only about 75 percent of the present real value of the R&D expense. As such, the expiration of full expensing effectively raises the cost of performing R&D, reducing firms’ incentives to invest at a faster pace.

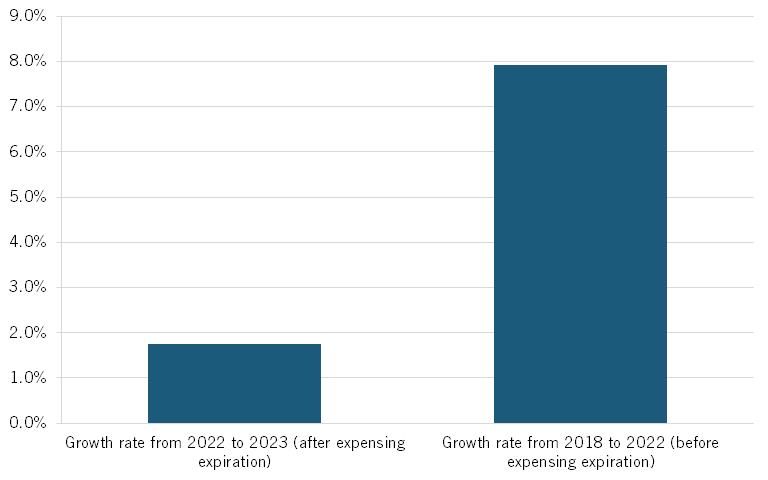

Data from the National Science Foundation confirms that the U.S. business sector is no longer increasing its R&D investment at the same rate as it did prior to the expiration of full R&D expensing. From 2018 to 2022, the average annual growth rate for the business sector’s R&D expenditures was 7.9 percent. Yet after the expiration, the average growth rate dropped to just 1.7 percent, signaling a sharp slowdown in their R&D investments. (See figure 1.)

This is especially concerning because the business sector has long been the primary driver of R&D expenditures in the United States, accounting for more than 70 percent of total U.S. R&D expenditures since 2013. It should be noted that this decline in growth rate is a correlation with the end of full expensing, not definitive evidence of causation. Nevertheless, the trend is strongly suggestive of the policy’s impact on R&D growth rates.

Figure 1: Business sector R&D expenditures' annual growth rate before and after the expiration of full R&D expensing

Congress should pass the American Innovation and R&D Competitiveness Act of 2025 to restore the immediate deductibility of R&D expenses—or ensure that this provision is included in the “Big Beautiful Bill.” Doing so would not only boost economic growth, as businesses introduce new products and processes that increase productivity, but also strengthen U.S. competitiveness against China, which is an especially urgent priority.

As ITIF’s Hamilton Index shows, China is rapidly overtaking the United States in production across many advanced industries. Moreover, another ITIF analysis indicates that China has likely already surpassed the United States in total R&D spending. Now is the time for policymakers to incentivize, rather than disincentivize, the business sector to increase its investments in R&D.