China Is Rapidly Becoming a Leading Innovator in Advanced Industries

There may be no more important question for the West’s competitive position in advanced industries than whether China is becoming a rival innovator. While the evidence suggests it hasn’t yet taken the overall lead, it has pulled ahead in certain areas, and in many others Chinese firms will likely equal or surpass Western firms within a decade or so.

KEY TAKEAWAYS

Key Takeaways

Contents

The Nature of Innovation Industries and Competitive Positioning 8

The Contrasting Western and Chinese Economic Models 65

How the United States Might Not Lose More. 111

Introduction

Perhaps the most critical question for the United States vis-à-vis China’s economic and technology challenge is whether China can become a real innovator. If China has difficulty becoming an innovator and remains largely a copier, then the threat to the United States and other allied technology economies is less. In this case, as long as the United States (and allies) can innovate at a robust-enough rate, they can likely maintain the lead on advanced technologies, even if China quickly copies foreign innovations. But if China can develop new-to-the-world innovations ahead of, or at the nearly the same time as, the United States and allied nations, its potential to displace U.S. (and allied) technology-based companies and capabilities becomes much more likely, especially because China benefits from significant economies of scale and a government laser focused on global best-in-class science and technology policy for competitiveness.

To date, this issue has been widely discussed, but, with the exception of analysis of a variety of innovation input indicators (e.g., research article citations, research and development (R&D) personnel, patents, etc.), it has not been rigorously examined. To remedy that, the Information Technology and Innovation Foundation (ITIF), with the support of the Smith Richardson Foundation, has conducted an analysis of the extent to which Chinese companies are innovating and already possess the capabilities to be global innovation leaders.

Overall, we find that, for the most part, while Chinese firms and industries are not as innovative as the global leaders in Western nations (defined as developed, democratic nations), they are catching up, in many cases at an extremely rapid pace—and the scale of their efforts is massive.[1] As the China Institutes of Contemporary International Relations wrote somewhat modestly in 2021, “China still has a not insignificant gap to close with the United States in the fields of science and technology, but the [Chinese] growth rate is rapid and there is potential for development.”[2] To use an analogy, it’s as if we were to look out at the ocean and see calm waves, but over the horizon is a tsunami of hundreds of strong, innovative, and lower-cost Chinese firms in dozens of industries seeking to grab global market share from established leaders.

For the most part, while Chinese firms and industries are not as innovative as the global leaders in Western nations, they are catching up, in many cases at an extremely rapid pace—and the scale of their efforts is massive.

These research findings suggest that it’s time to reject the often ideologically based view that “China can’t innovate.” While China is ruled by a communist party, China is not the Soviet Union, and its firms have considerable degrees of freedom to act, as long as they are working to achieve the goal of making China the world innovation leader. The reality is that China is much more akin to where the Asian Tigers (Hong Kong, South Korea, Singapore, and Taiwan) were 20 years ago, only in this case, China is not a tiger, but rather a fire-breathing dragon on government-provided steroids.

Why This Matters

China became the world’s manufacturing workshop on the basis of a combination of low costs, a large and rapidly growing domestic market, and aggressive efforts to recruit foreign manufacturers. While that process led to considerable manufacturing decline in the United States, most of it (with the exception of consumer electronics) was in more traditional industries such as plastics, metals, textiles and apparel, toys, and furniture.[3] While this was hard on the U.S. workers and communities that lost to China, it did not mean a significant weakening of U.S. techno-economic strength and dual-use (civilian and military) capabilities, particularly in U.S.-headquartered firms. And it certainly did not mean a high level of strategic dependency on China. If a conflict came, the worst that could happen would be no more McDonald’s Happy Meal toys.

China is much more akin to where the Asian Tigers were 20 years ago, only in this case, China is not a tiger, but rather a fire-breathing dragon on government-provided steroids.

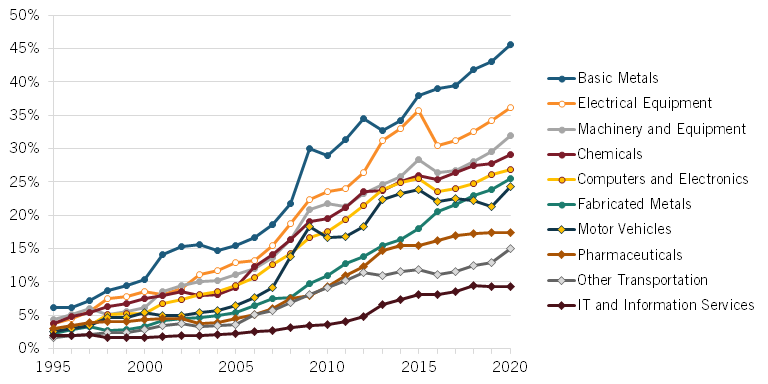

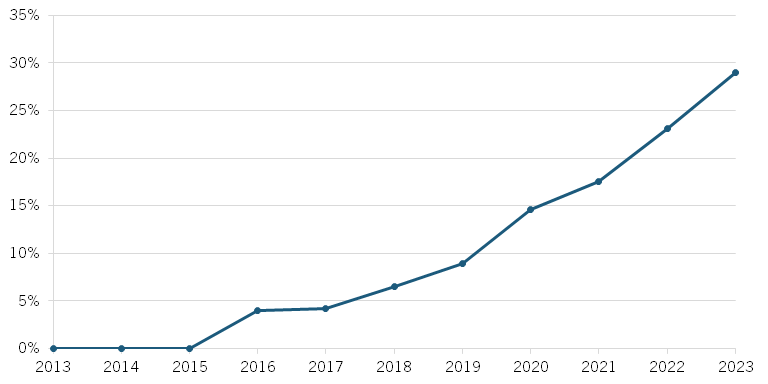

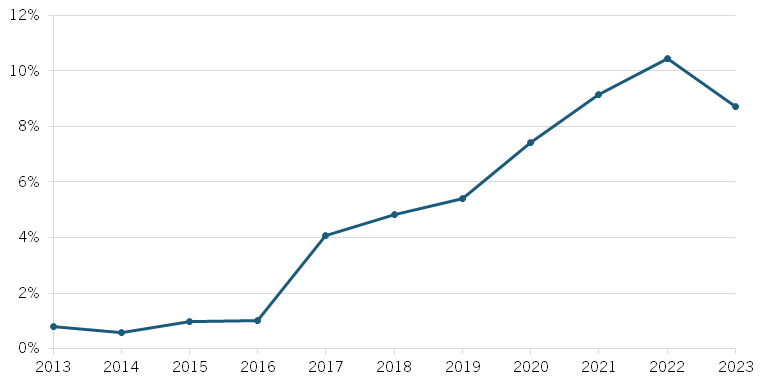

However, the last decade has shown that China can be a globally competitive producer of technologically complex goods, such as telecom equipment, machine tools, computers, solar panels, high-speed rail, ships, drones, satellites, heavy equipment, and pharmaceuticals. In all these industries, China has gained significant global market share—and it is making rapid strides in emerging industries such as robotics, AI, quantum computing and biotech. Indeed, as ITIF’s Hamilton Index shows, China’s global share of advanced industries has grown dramatically over the last 25 years. (See figure 1.)

Figure 1: China’s global market shares in advanced industries

In most of these industries, China has been able to gain market share through the advantages of scale economies in its often-protected home market, combined with significant subsidies to Chinese firms. This is why, in 2020, in 7 of 10 advanced industries, China led in global production, with the United States leading in only 3. (See table 1.)

Table 1: Hamilton Index industry leaders, 2020

|

Industry |

Global Output (Billions) |

Leading Producer |

Leader’s Share |

|

IT and Information Services |

$1,900 |

USA |

36.4% |

|

Computers and Electronics |

$1,317 |

China |

26.8% |

|

Chemicals |

$1,146 |

China |

29.1% |

|

Machinery and Equipment |

$1,135 |

China |

32.0% |

|

Motor Vehicles |

$1,093 |

China |

24.3% |

|

Basic Metals |

$976 |

China |

45.6% |

|

Fabricated Metals |

$846 |

China |

25.6% |

|

Pharmaceuticals |

$696 |

USA |

28.4% |

|

Electrical Equipment |

$602 |

China |

36.1% |

|

Other Transportation |

$386 |

USA |

34.5% |

|

Composite Hamilton Index |

$10,097 |

China |

25.3% |

On many measures, China already leads the United States and can be considered a co-equal economic superpower. It’s gross domestic product (GDP) is more or less equivalent, it has significantly more exports, and its manufacturing sector is vastly larger. But with all that strength, China still lacks two things: high productivity and the ability to outcompete innovative leaders.

China’s productivity will no doubt continue to grow faster than the United States’ over the next three decades, probably at least until it gets to about 80 percent of U.S. levels. But that will come about almost entirely through domestic-serving industries (e.g., agriculture, utilities, logistics, business services, retail trade, finance, etc.) using more technology and getting more productive. When that happens, China’s GDP will easily be double if not triple that of the United States. There is little the United States and allies can do to slow China’s productivity growth, because, for the most part, that growth does not depend on any chokepoint technologies controlled by allied nations. Moreover, that growth could have some benefits for the United States and allied advanced industries not only by boosting Chinese demand but also by creating a vast Chinese middle class that may seek more democratic rights, as was the case in countries such as Japan, South Korea, and Taiwan.

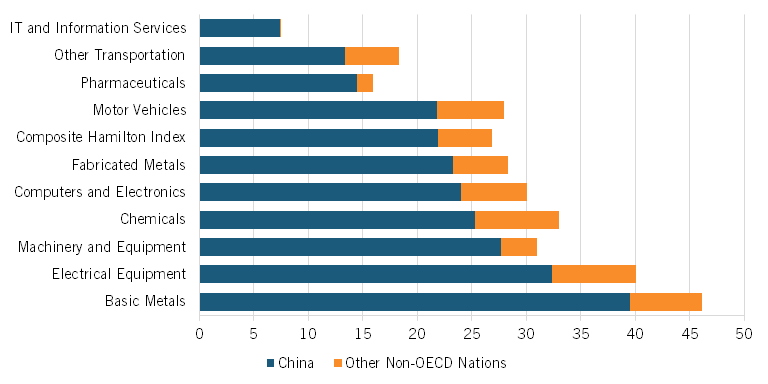

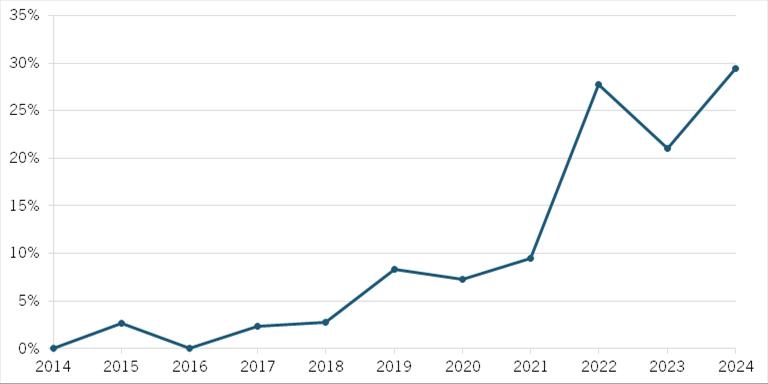

It is China’s progress on innovation that poses the more-significant challenge to the United States and its democratic allies. To date, much of China’s growth has come from copying the leaders and producing products that, while not as high quality, are priced more competitively. This has helped China gain market share, particularly in less-developed countries where price is a more important differentiating factor. This is one reason why China has taken almost all the growth in these industries from nations outside the Organization for Economic Cooperation and Development (OECD). (See figure 2.)

Figure 2: Non-OECD change in global market shares (percentage-point difference, 1995–2020)

However, going forward, if China can combine its cost advantage with an innovation advantage, or at least innovation parity, the challenge to innovative industries in Western nations will become much more significant. As such, a key question for these nations is to what extent China has become or will soon become an innovation leader, or at least on par with innovation leaders. If China can become an innovation leader, that development poses a significant threat to Western nations and their firms because China will be able to combine quality, innovation, and price.

This is a key reason why the threat from an innovative China is so significant. Historically, low- and middle-income countries were generally not innovators, and they competed either in more routine, older industries (e.g., textiles, commodity metal products, low-end electronics, assembly of goods, etc.) or in advanced industries by copying and being a generation or two behind the leaders and competing on lower-cost labor. And in this latter case, this was almost always through branch plant operations of firms in higher-income nations. As such, the knowledge diffusion to the host country was somewhat limited, and its domestic capabilities for competitiveness grew slowly, usually at around the same pace as the leaders.

In this sense, there was a global division of labor, with high-income nations (e.g., the United States, Commonwealth nations, the European Union, and, more recently, Japan, South Korea, Singapore, and Taiwan) specializing in industries and products that other countries did not have the technical capabilities to make.[4] This was one reason why they could sustain their cost disadvantage. But if China can compete across the board in an array of complex industries and produce new-to-the-world products, while also enjoying a significant cost advantage (Chinese labor costs around 25 to 30 percent of U.S. costs), that will be a major competitive threat to leading global innovation-based companies, and the economies that host them. And without these companies producing in the United States and other advanced economies, these nations’ techno-economic power will decline relatively, as there is simply no way for domestic (and often smaller) firms to take up the slack when multinationals lose significant market share.

If China can compete in an array of complex industries, while also enjoying a significant cost advantage, that will be a major competitive threat to leading global innovation-based companies, and the economies that host them.

China achieving innovation parity would have two major effects, one in China, and one in Western nations. First, it would mean that China would be much more self-sufficient in advanced industries and much less vulnerable to Western sanctions and other trade tools used in an attempt to discipline China. At the same time, it would also boost Chinese military capabilities even more, as civil-military fusion becomes stronger, and weapons systems companies could rely on cutting-edge technologies across a range of industries. Just as importantly, this commercial technology strength would also equate to increased power in foreign affairs, just as America dominated the globe for more than a half century after WWII, as its firms were the unalloyed leaders. It is China that might decide to impose export controls on the allied nations as punishment.

The Fisher Body Plant in Detroit, Michigan, manufactured automobiles from 1919 to 1984.[5]

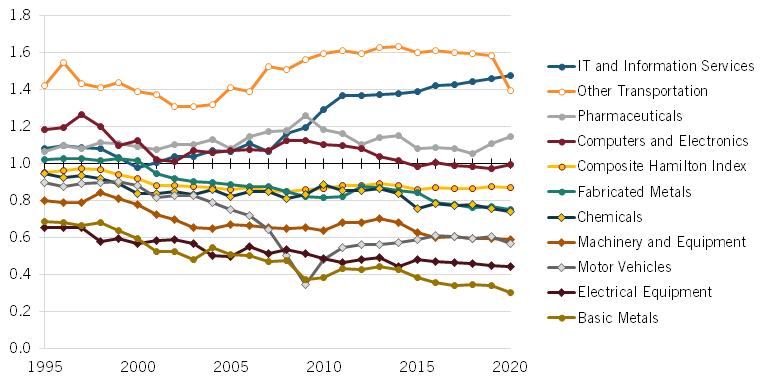

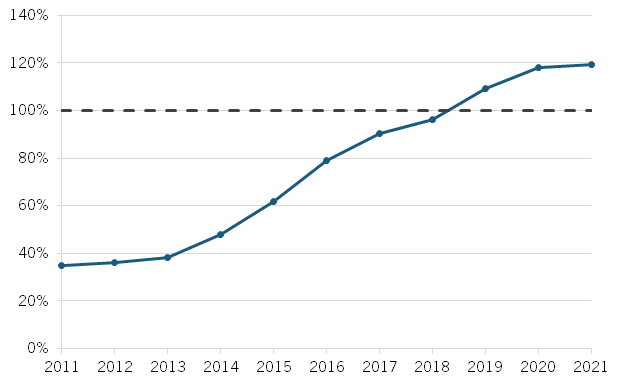

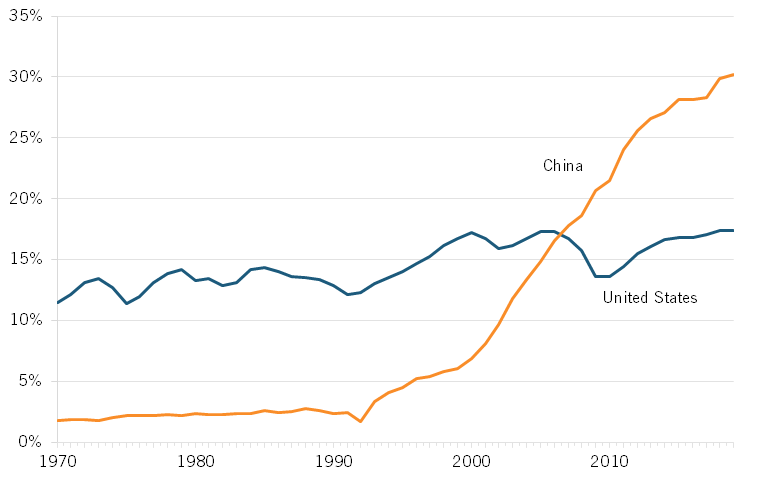

It is these foreign effects, particular on the United States (and other Western nations) that are potentially most important. If China can become an innovative leader in robotics, electric vehicles (EVs), airplanes, semiconductors, drugs, and more, it can dominate the global economy. If China makes serious inroads into the market share of current technology leaders (e.g., ABB in robotics, GM in cars, Boeing in airplanes, Intel in chips, Merck in drugs, etc.), the fundamental nature of the global economy shifts. The 200 year-long development of advanced industry in capitalist, democratic nations—first in the United Kingdom and Western Europe, and then in America, and then Japan, South Korea and Taiwan joining the “club”—could radically change. The West could very well become what Australia, Canada, the United Kingdom and parts of Europe (e.g.. Greece, Italy, Portugal, and Spain) have already become: largely hollowed-out economies with little advanced manufacturing, a weak technology sector, and an economy propped up by tourism, finance, agriculture, and natural resources.[6] This is the trend for the United States as the U.S. location quotient (the industry output as a share of the U.S. economy over the industry output as a share of the global economy) has fallen. (See figure 3.) With any kind of foresight, it’s easy to see the same fate befalling the United States if China can be an innovation peer.

Figure 3: America’s relative historical performance in Hamilton Index industries (LQ trends)

It is impossible to overstate the implications of this potential development, as it would entail a massive switch in the center of global economic power and innovation from a geopoint somewhere in the Atlantic Ocean to somewhere in China. To be sure, just as the United Kingdom still has some tech capabilities and firms after its half century of industrial decline, the allied nations will not completely become, as Alexander Hamilton warned, a hewer of water and drawer of wood, dependent on the innovation leader of the time, the United Kingdom. But if China can move to the frontier of global innovation—a destination all forces in China are pulling toward—the world economy and relative national power will be fundamentally transformed.

The Nature of Innovation Industries and Competitive Positioning

Such a change could be gradual, but if it happens, it would more likely be quite sudden (i.e., within a decade or two). The reason is because of the unique nature of innovation industries. These almost always have high fixed costs (e.g., R&D, product design, tooling setup) and lower marginal costs, where losing sales can lead to a death spiral of less revenue, less investment, and less innovation and then less revenue. The opposite is true for firms that are gaining revenue. Chinese innovation scholar Yin Li noted that “building these organizational capabilities inevitably entails high fixed costs that, for innovation to be successful, must be transformed into low unit costs, through accessing a large share of the market.”[7]

If China can move to the frontier of global innovation—a destination all forces in China are pulling toward—the world economy and relative national power will be fundamentally transformed.

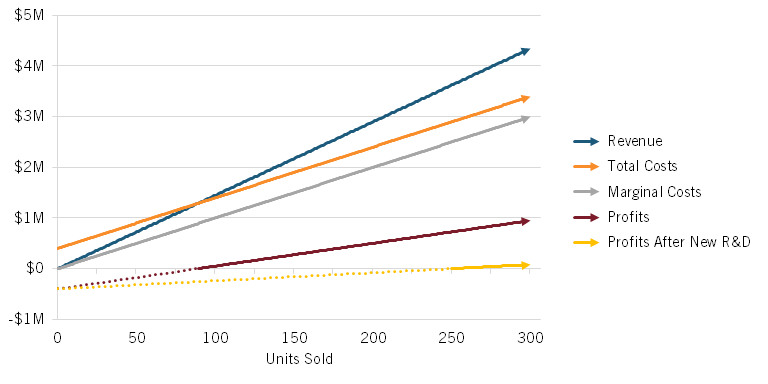

Figure 4 illustrates the cost structure of a hypothetical firm for which fixed costs are 40 times marginal costs—$400,000 and $10,000, respectively. In other words, the company must spend $400,000 on R&D, design, machinery, and other fixed costs before it can produce its first unit. It then costs $10,000 to make each unit in terms of energy, materials, and labor, and the company can sell them for $14,450 per unit. Because of its high fixed costs, the company loses money until it sells at least 88 units. At that point, it makes an increasing profit on each additional unit sold.

Figure 4: Hypothetical firm with fixed costs 40 times greater than marginal costs

For these industries, scale is everything. Imagine if, because of tougher, subsidized competition from China, sales of the U.S. firm go down to 75 units. In this case, the company would suffer a loss of $62,500. But if it faces less competition from China, then the company could earn a profit of $50,000 after selling 100 units. Meanwhile, whereas the total cost for producing the 75th chip would be $15,333, the total cost for producing the 100th chip would drop to $14,000. Now imagine the company needs to invest 20 percent of its revenues in new R&D to remain competitive. That moves the goalpost; it would require selling more than 250 units to become profitable.

This is why scale is so critical for advanced industries, and why a threat from a robust competitor can be so devastating so fast. Profits fall fast, so R&D and other core value creation capabilities are cut. As a result, the next generation of sales fall, and the downward cycle continues. We have seen this with a number of North American companies facing the China challenge (e.g., Lucent and Nortel) and industries (the U.S. solar panel industry), which fell from dominance astoundingly fast. If China can be an innovative leader and take market share from Western leaders, the latter’s ability to keep investing in innovation falls, as do future sales. The increased sales accruing to Chinese firms enables them to gain even more scale, allowing them to sell products for even lower prices and achieve higher profits (or lower levels of government-subsidized losses) to invest in next-generation products.

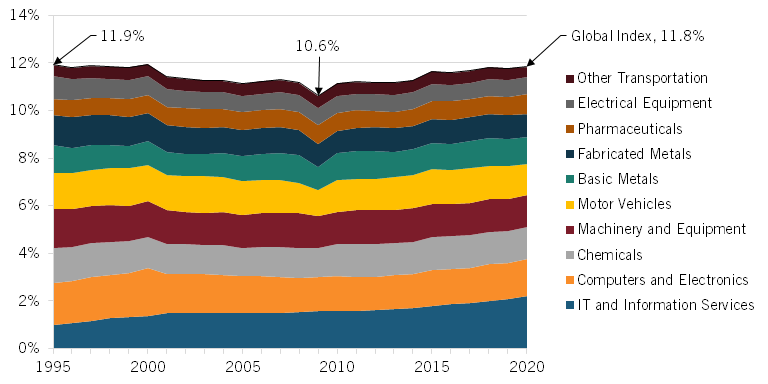

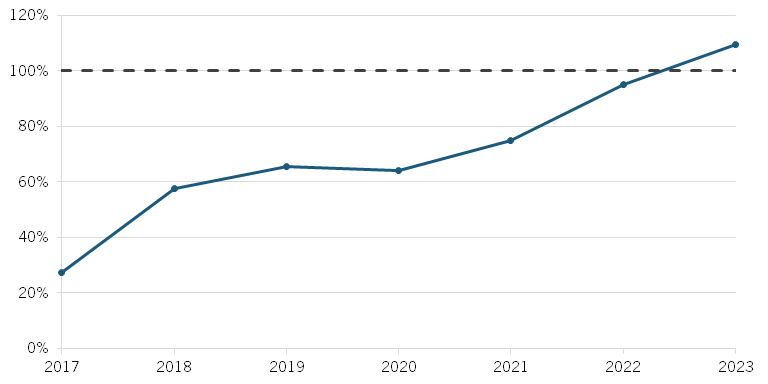

Some will respond that this exaggerates the threat and paints innovation as a zero-sum game. To be sure, if China develops a cure for cancer (or workable nuclear fusion, etc.) the world and America would benefit. But at the same time, it would mean reduced global market share from U.S. and Western-based drug companies. This is because the market for advanced industry goods is largely fixed as a share of global GDP. As figure 5 shows, 10 advanced industries accounted for 11.9 percent of global value-added output in 1995 and 11.8 percent in 2020. To the extent China captures more of the global sales in these industries, that by definition leads to less market share for non-Chinese firms, and potentially fewer actual sales.

Figure 5: Hamilton industry shares of the global economy

We have already seen such win-lose shifts. ITIF has identified the industries and countries where there was the most nominal decline in output from 2017 to 2020, not counting motor vehicles, which overall saw declines:

▪ In Austria and Switzerland, the biggest declines were in electrical equipment (declines of $1.15 billion and $115 million, respectively). During this period, China expanded its output by $42 billion.

▪ The nations where the largest loss was in machinery and equipment were Germany ($16.4 billion), Japan ($14 billion), Italy ($5.0 billion), Brazil ($4.1 billion), Argentina ($1.8 billion), Mexico ($1.5 billion), and the United Kingdom ($1.8 billion). China expanded its output by $69.4 billion.

▪ In computers and electronics, Denmark’s output fell $80 million, Japan’s fell $6.5 billion, and South Korea’s fell $18 billion. China’s output increased by $64.7 billion.

▪ In chemicals, Brazil’s output fell by $8.7 billion, Canada $900 million, Netherlands $1.4 billion, Norway $400 million, Pakistan $600 million, Singapore $5 billion, South Korea $5.6 billion, Germany $5.4 billion, and France $3.8 billion. China’s output increased $35.5 billion.

▪ In basic metals, Japan’s output fell $17.2 billion and Turkey’s $5.3 billion, while China’s increased $86.4 billion.

▪ In fabricated metals, Germany’s output fell by $7.1 billion, South Korea’s output fell by $4 billion, France’s by $3.4 billion, and Spain and Sweden $1.2 billion, while China’s increased $41.8 billion.

It’s time to move away from the focus on manufacturing per se and focus instead on advanced industry leadership.

Finally, it is important to clarify that this is not about manufacturing per se. Much of the competitiveness debate in the United State is fixated on manufacturing. The free-market globalists go to great pains to distort the data to show that U.S. manufacturing is healthy (or irrelevant) because they fear that acknowledgement of the truth could lead to an abandonment of their global idealist vision of the world as one large integrated price-mediated market. In contrast, the emerging worker nationalists stress manufacturing jobs—low-tech or high-tech—in part because of their solidarity with labor over capital. But the United States could have a robust manufacturing economy based around low value-added industries (e.g., textiles, metal parts, food products) and still be dependent on China for advanced industries and innovation. As such, it’s time to move away from the focus on manufacturing per se and focus instead on advanced industry leadership.

That matters not only for national power writ large—and for holding adversaries in check while increasing their dependence on the United States—but also, critically, for defense capabilities, particularly should the United States be forced into a long and protracted war. As retired U.S. Army Major General John G. Ferrari recently stated, he had “grave concerns” about America’s ongoing reliance on China to equip its military and said, “If we were in a war with China and it stopped providing parts, we wouldn’t be able to build the planes and weapons we needed.”[8]

What Is Innovation?

One reason why it has been difficult to answer the question, “How innovative is China?” is that there are multiple definitions of what it means for an economy to be “innovative.” Some equate it with doing well in innovation-based industries, even if that output is largely based on copying from leaders in other nations. Others argue it is strong performance in a variety of innovation metrics, such as patents, R&D, and venture capital (VC), even though these metrics are correlated with innovation but are not determinative. Still others argue that it is a nation’s firms gaining market share in first-to-the-world (or near-first-to-the-world) products and services. For the purposes of this report, it is this third definition that is most relevant because it is key to determining whether China can do more than copy and because even strong innovation metrics are not necessarily a sign of true innovation performance.

Another factor that can complicate the analysis is whether process or product innovation is the measure. Process innovation—developing and adopting new ways of producing a good or service—is an important factor in increasing labor productivity (e.g., output per labor hour), and that is key to being able to effectively compete with low-wage economies.

Product innovation refers to new and better products (and services). It enables higher-wage economies to compete on the basis of goods that do not compete largely on costs. For example, new pharmaceuticals can be priced higher than older generics if they provide better treatment. New 5-nanometer (nm) computer chips cost more than older 20 nm chips, but because of superior performance will often outcompete the older generations. Patent protection, trade secrets, and other knowledge advantages can provide somewhat sustainable advantages over lower-cost rivals.

However, product innovation is not very important if the innovation cannot be brought to market successfully. This requires adequate quality, a competitive cost structure, and a viable business model. As Clay Christensen pointed out in The Innovator’s Dilemma, it’s not enough to be successful in generating new ideas.[9] Even technological breakthroughs can become a dead end unless they can be translated into working products that are able to be delivered and deployed into the larger marketplace. What we really want to determine is China’s innovative capabilities as they relate to being early in bringing new products to widespread market adoption.

Finally, at one end are innovations that are transformative. The invention of nylon, the television, the first transistor, radar, and the personal computer are in this category. At another end are ideas that many other companies are already executing. This is why one factor in innovation is differentiating between breakthrough (sometimes termed exceptional, radical, or disruptive) innovations (e.g., the iPhone) and sustaining innovations (sometimes called incremental or continuous), such as a new generation of semiconductors that has higher performance than the current generation.[10] For example, consider the drivetrain of cars. The development by Tesla of the electric drivetrain was a breakthrough innovation. The development of a better electric motor that uses a small percentage less electricity is an incremental innovation, or what is termed sustaining innovation. Most innovation is sustaining, as companies seek to improve capabilities in existing markets and where they have a clear idea of what problems need to be solved. Disruptive innovations such as the iPhone are relatively rare and often usually relatively quickly enter into a stage of incremental innovation (e.g., better battery life, better displays, better cameras).

Disruptive innovation is perhaps the most threatening to companies. Blackberry did not go out of business because the iPhone was a similar phone with a better physical keyboard; it went out of business because the iPhone and the business model that went along with it (including the app store) was disruptive. The milk glass bottle industry did not go out of business because someone made slightly lighter glass bottles; it went out of business because paperboard cartons and then plastic bottles provided much better value.

In summary, innovation is not invention. It is not science. It is not necessarily entrepreneurship. It is bringing to market new products or services at scale. In addition, while that part of innovation is critical, so is its widespread diffusion and adoption, and so is the process of technology innovation.

Innovation is not invention. It is not science. It is not necessarily entrepreneurship. It is bringing to market new products or services at scale.

The Asian Tiger Path

One reason to be on the affirmative side of “can China innovate?” is that it is attempting to follow well-worn paths other developing Asian economies have followed to become innovation leaders. As Linsu Kim wrote in his definitive 1997 history of South Korean innovation upgrading, Imitation to Innovation: The Dynamics of Korea’s Technological Learning, there are several distinct stages a nation that is catching up to the leaders in innovation usually takes. The first involves the transfer of foreign technology to that nation—sometimes by foreign direct investment (FDI), sometimes by licensing, and often, as in the case of China, by theft or pressure on foreign firms seeking to sell in the market. The second stage involves “the effective diffusion of imported technology within an industry and across industries” which “is a second sequence in upgrading technological capability of an economy.”[11] The third stage “involves local efforts to assimilate, adapt, and improve imported technology and eventually to develop one’s own technology. These efforts are crucial to augmenting technology transfer and expediting the acquisition of technological capability. Technology may be transferred to a firm from abroad or through local diffusion, but the ability to use it effectively might not be there. This ability can only be acquired through indigenous technological effort.”[12]

The final stage is to become a global innovation leader. As Kim wrote:

Firms in catching-up countries that have successfully acquired, assimilated, and sometimes improved mature foreign technologies may aim to repeat the process with higher-level technologies in the transition stage in advanced countries. Many industries in the first tier of catching-up countries (e.g., Taiwan and [South] Korea) have arrived at this stage. If successful, they may eventually accumulate indigenous technological capability to generate emerging technologies in the fluid stage and challenge firms in the advanced countries.[13]

China is following this recipe/path, with its first step being to attract foreign investment. In the early 1980s, when Deng Xiaoping opened up the Chinese economy to foreign investment, his main economic development strategy sought principally to induce foreign multinationals to shift relatively low- and moderate-value production to China.[14]

China’s second step was to attempt to learn from foreign companies, in part by having them train Chinese executives, scientists, and engineers, and also by forced technology transfer, including through joint ventures. In 2015, 6,000 new international joint ventures, amounting to $27.8 billion in FDI inflows, were established in China.[15] And the sophistication and value of the technology the Chinese government has demanded is high. As the United States Trade Representative’s (USTR’s) Office pointed out in its 2018 Special 301 report on China, pressures on U.S. companies to form joint ventures and transfer technology “is particularly intense.”[16]

The third step was to support Chinese companies in their efforts to copy and incorporate foreign technology while building up domestic capabilities. One important marker for the transition from stage two to stage three was the publication in 2006 of the “National Medium- and Long-term Program for Science and Technology Development (2006–2020),” which called on China to master 402 core technologies—everything from intelligent automobiles to integrated circuits and high-performance computers. China moved to a “China Inc.” development model of indigenous innovation, which focused on helping Chinese firms, especially those in advanced, innovation-based industries, often at the expense of foreign firms.

The fourth and final step is to enable Chinese firms to become independent innovators—as Japan, Singapore, South Korea, and Taiwan have all become. China is attempting to do this through an array of plans and policies: “13th Five-Year Plan for Science and Technology,” “13th Five-Year Plan for National Informatization,” “The National Cybersecurity Strategy,” and “Made in China 2025 Strategy,” and most recently Xi Jinping’s call at the 20th Party Congress for “invigorating China through science and education ... for the strategy of innovation-driven development.”[17]

The last part of this is to then support these companies “going out” and taking market share in other parts of the world. Unfortunately, for gaining political support for a robust U.S. strategy to respond to China, the United States is among the last places Chinese firms will seek to enter. Rather, they are going after market share in places such as Latin America, Southeast Asia, Africa, and Eastern Europe, the “soft underbelly” of global markets. As their firms gain market share, Western—including U.S.—firms, lose market share, and tipping points can happen quite quickly.

Finally, it’s important to note that there are two key factors for innovation success. One is talent, and the other is revenue. More money makes innovation vastly easier. Companies with more money can invest more in R&D. They can acquire talent and technology. They can pay their talent more. And they can achieve scale. This is one of the main differences between the Asian Tigers and China: The Chinese market, and hence revenue, is vastly larger. Because China manages its market and limits foreign sales once its firms get to a certain scale, Chinese firms are blessed with massive, largely secure market revenues, and this does not take into account massive government subsidies.

Related to this is the massive efforts the Chinese government makes to ensure that Chinese society is a lead adopter of advanced and emerging technologies, including high-speed rail, digital and 5G-enabled manufacturing, robotics, smart cities, smart ports, EVs and autonomous vehicles (AVs), digital payments, healthtech, edtech, drones, satellites and space travel, and many more.[18] While China walks the talk when it comes to transforming its society through technology, and in the process creates massive capabilities and revenues for its technology companies, the United States doesn’t even slow-walk the talk, as all too often we are walking backward, banning and demonizing technology.[19]

Transitioning from “fast follower” to “global leader” in innovation is not easy, but a number of nations have done it. The United States accomplished this in the early part of the 1900s. Germany and Austria advanced from copying economies in the late 19th century to innovators, building on imports of skilled workers, advanced machinery and blueprints.[20] Japan achieved this by the 1980s, with South Korea, Taiwan, and Singapore doing so two to three decades later. The idea that copiers and followers cannot transition into innovation leaders is just not borne out by history. China is not there yet, at least in many sectors, as this report documents. But that is not for lack of trying and having the same kinds of conditions that other innovation transition economies have had.

The core insight needed to understand the Chinese economic strategy is as follows. China attaining global competitive advantage in virtually all advanced manufacturing industries requires significant “learning,” as the production “recipes” to make, for example, a wide-body jet, a computer chip, a genomics sequencer, a robot, or a biotech drug are incredibly complex and cannot be obtained from scholarly journal articles or other widely available sources of technical knowledge.

Because China manages its market and limits foreign sales once its firms get to a certain scale, Chinese firms are blessed with massive, largely secure market revenues—and this does not take into account massive government subsidies.

Even after China has gained global market share in a number of extremely complex, advanced technology industries such as jet aircraft, high-speed rail, solar panels, personal computers, supercomputers, telecommunications equipment, and Internet services, many will still dismiss China’s capabilities and assume China will be incapable of even partial success becoming a true innovator. While mastery of some particularly complex technologies such as semiconductor logic circuits remains a challenge for China, Chinese companies have made significant progress in an array of other technologies, including in certain kinds of semiconductors (e.g., chips for Internet-of-Things (IoT) devices). Moreover, the fact that nations such as Japan in the 1960s and 1970s, and Taiwan and South Korea in the 1980s and 1990s, could rapidly progress to become advanced technology economies using similar kinds of approaches (obtaining foreign technology and subsidizing and protecting domestic innovators until they are strong enough to compete on their own), suggests there is nothing inherently keeping China from making similar progress, especially given the massive amount of government support for the effort.[21]

One way to understand Chinese innovation is provided by the McKinsey Global Institute’s The China Effect on Global Innovation, which separates innovations into four categories: efficiency-driven, customer-focused, engineering-based, and science-based.[22] The report concludes that with its proven ability to produce goods at scale, adapt products to the Chinese market, and develop and adopt digital infrastructures such as mobile payment systems and e-commerce (sometimes even before more-developed economies), China has demonstrated that it is capable of efficiency-driven and customer-focused innovations. The challenge before it, the authors argued, is to catch up in the areas of engineering- and science-based innovations.

Can China innovate?

As far as can be determined, there have been no thorough studies of China’s innovation capabilities. There have been a host of studies, including from ITIF, that examine indicators of innovation, such as R&D spending, scientists and engineers, and patenting.[23] But these do not adequately answer the question of whether China is copying or innovating.

The question of whether China can innovate is a longstanding one, with analysts coming down on both sides. Some argue that China cannot really be innovative because its innovation system is deficient. This includes charges of weak intellectual property (IP) protection, it being too state directed, and having too little creativity due to rote learning and a hierarchical education system. Others argue that China can’t be innovative because its economy suffers from low productivity, even though the two factors are related but not codeterminant.[24] Still others embrace the popular narrative that we have reached “peak China” and it’s entering into a long, slow phase of decline. Indeed, the conventional wisdom until recently was that China could not innovate; at best, it could be a fast follower.

However, a growing number of analysts have challenged that conventional wisdom, with some arguing that, in certain cases, China is even more innovative than the United States, as exemplified by a 2021 Harvard Business Review article “China’s New Innovation Advantage.”[25] However, this article relies on metrics such as speed of attaining unicorn status. And with the largest population on earth, one would expect a fair number of Chinese unicorns. The authors also talked about how Chinese people like to adopt new technologies. But there is little evidence that this is greater than some other nations, including the United States. Finally, most of the examples given of Chinese innovation success are in a few narrow areas such as 5G (where China’s lead is actually much less than most people think), mobile payments, and smart scooters (technologies that are not as important to national power).[26]

China Cannot Innovate

For the most part, scholars studying the Chinese economy broadly, and their innovation capabilities specifically, have until recently largely argued that China is incapable of “true” innovation, at least at the global frontier. In general, the reasons given in support of this view are an education system that encourages rote memorization and represses creative expression, a risk-averse culture centered around a reverence for authority that is not conducive to disruption or drastic change, weak IP protections, and inefficient state involvement in markets. Proponents of these arguments believe that while China’s economic rise is impressive, it is bound to be at best a copier of innovations from the West, at least for the foreseeable future.

Examples of such arguments abound. In a 2014 article for The Diplomat, Kings College London Professor of Chinese Studies Kerry Brown wrote:

The Chinese government under Xi can pour all the money they want into vast research and development parks, churning out any number of world class engineers and computer programmers. Even with all of this effort, however, China is likely to produce few world-class innovative companies. The fundamental structural problem is that the role of the state and government in China is still very strong … The system that China currently has still rewards conformity.[27]

Likewise, a 2014 Harvard Business Review article titled “Why China Can’t Innovate” lists several reasons that explain why “China is largely a land of rule-bound rote learners—a place where R&D is diligently pursued but breakthroughs are rare.”[28] It cites the “unprecedented scale of [the Chinese government’s] failure to protect intellectual property rights.” The article also points out that Chinese schools emphasize test scores too heavily and do not prime students to be creative and design oriented. It goes on to note:

The Communist Party requires a representative to be present in every company with more than 50 employees. Every firm with more than 100 employees must have a party cell whose leader reports directly to the party in the municipality or province. These requirements compromise the proprietary nature of a firm’s strategic direction, operations, and competitive advantage, thus constraining normal competitive behavior, not to mention the incentives that drive founders to grow their own businesses.[29]

It further states that “the freedom to pursue ideas wherever they may lead is a precondition for innovation in universities.” Likewise, a recent Wall Street Journal op-ed also titled “Why China Can’t Innovate” lays the blame on the assertion that “communism is incapable of nurturing the curiosity that leads to innovation.”[30]

Others argue, with some justification, that input metrics such as research articles or even patents fail to effectively measure innovation. But then they go on to suggest that China therefore is not leading. A Defense News article argues that in America’s “thriving open market, a product of the U.S.’s commitment to an open society and the free exchange of ideas, metrics like commercial success, technology adoption and real-world impact become more telling than raw measures.”[31] Yet, the author failed to report any of these better metrics. He went on to note, with no real evidence, “The U.S. strives, though imperfectly, to offer opportunities to everyone who desires them, eschewing artificial barriers and quotas and avoiding intellectual conformity. This commitment fuels a dynamic, diverse workforce that is a wellspring of ingenuity and innovation.”[32]

In this same vein, an Atlantic Council report states, “China’s authoritarian top down political system poses the risk of restraining free thinking and sharing of ideas and information—both domestically and internationally—that are crucial in stimulating scientific research and discoveries.”[33] A recent article in Foreign Affairs just states it bluntly in the subtitle: “A Statist Economy Can’t Foster Creativity.”[34] The author went on to write that “an innovation-based industrial strategy may not be transformative if the government is unable to address basic systemic weaknesses such as youth unemployment, frailties in China’s banking and financial systems, and weak consumer demand.” It’s not clear how any of these relate to innovation, or are even true. Yasheng Huang argued in the Rise and Fall of the EAST that China’s repression, especially under Xi, is deeply problematic for Chinese innovation.[35]

Simon Gao wrote that “there is a bigger reason that China’s ambitious technology endeavors are failing: Its communist system stifles innovation.… If China can’t cultivate free thinkers, it will always be a follower and never a leader as the West imagines and invents the future.”[36]

Others see China as a “peaking power,” implying that it will continue to lag behind in innovation.[37] Likewise, a Washington Post series featuring experts reflects the new preferred wisdom that China faces a demographic crisis: Its young people are discontent and its economy has hit the wall, in part because of the current banking and real estate challenges; and the Chinese Communist Party (CCP) is only interested in its own power, not innovation.[38]

Studies criticizing China for a rote education system appear to overstate the case. For example, in China as an Innovation Nation, Zhou, Lazonick, and Sun argued that claims criticizing the Chinese education system for suppressing creativity are overblown because similar critiques exist of Japan and South Korea, though most regard both to be innovative nations.[39] At times, this view is similar to the view held in the 1960s and 1970s that Japan’s postwar economic miracle would never overtake the United States because the Japanese were an “imitative people” who were only capable of creating copies of goods the United States and the West developed (e.g. computers, TVs, automobiles, etc.), which proved disastrously wrong.

How many governments in the world have decided they’re going to become major innovation centers? None of them have succeeded. Unless you count Finland, Ireland, Israel, Japan, South Korea, Singapore and Taiwan.

Michael Pettis, a professor at the Guanghua School of Management at Peking University, bluntly stated, “This is not a country we can expect major innovations from. In the West we don’t have enough confidence about this. How many governments in the world have decided they’re going to become major innovation centers? None of them have succeeded.”[40] Unless you count Finland, Ireland, Israel, Japan, South Korea, Singapore and Taiwan. They all committed to becoming innovation centers, and they all succeeded.[41]

Pettis went on to say that China is doomed to stagnate, like he’s claimed Japan did, even if it has the best supply-side technology development policies, because of demand-side stagnation, which he’s said Japan suffered.[42] First, Japan had no demand-side stagnation, given that its unemployment rate from 1995 to the present was quite low.[43] Second, Chinese firms don’t rely just on the Chinese market (the same way Japanese firms didn’t); they rely on the growing global market.

Scott Kennedy of CSIS is also skeptical of China’s ability to turn willpower and resource allocation into innovation. Citing the lack of growth in China’s output score relative to its input score in the World Intellectual Property Organization’s (WIPO’s) Global Innovation Index between 2009 and 2016, Kennedy dubbed China a “fat tech dragon,” since its apparent inability to turn inputs into outputs is analogous to a low metabolism.[44] Kennedy also pointed out that, while plentiful, Chinese patents are of relatively little practical use. Licensing revenues from the use of patents are still minuscule, and the surge in patents filed is a response to government rather than market incentives. Despite these issues, Kennedy acknowledged that China now graduates more scientists and engineers from its universities than does any other country, a higher percentage of bank loans are going to private businesses rather than state-owned enterprises (SOEs), and IP protections are steadily expanding.[45] Nevertheless, Kennedy has argued, innovation appears to be a secondary goal to market expansion overseen by the state.

Others argue that China cannot be innovative because its productivity performance lags behind global leaders. In an article for Australia’s Lowy Institute, John West argued that notwithstanding the relatively high rank on global innovation for a number of Chinese companies, overall, China is not innovative because it is not highly productive.[46] But this wrongly equates innovativeness with productivity. China could in fact have highly innovative globally traded companies and still have low productivity, especially if its nontraded sectors lag behind in productivity. This describes Japan to this day, where its leading traded sector industries (e.g., electronics, autos, etc.) are highly productive and innovative, but its nontraded sectors (e.g., healthcare, retail, etc.) are generally not.

Still others now advance the narrative that China’s economic slowdown means that it is in the Japan phase of development and the threat has passed. For example, Council on Foreign Relations scholar Zongyuan Zoe Liu has argued that China has been “killed” by failed CCP policies.[47]

One might say that the most important kind of freedom for innovation is the ability to do innovation with generous funding, something that is much easier for Chinese scientists than for Americans, especially given the declining federal funding for R&D.

Finally, it’s important to understand the “freedom” argument that democratic freedom is essential to national innovation. China is not the Soviet Union, where Lysenkoism (the rejection of traditional Darwinian genetics because it did not fit with Soviet ideology) reigned supreme. It is not even the United States, where stem cell research using discarded embryos was banned for religious reasons. It is a place that gives its scientists and engineers enormous freedom to innovate, as long as it is in areas seen as in the public interest (as opposed to, for example, education apps that lead to an arms race among parents of one-upmanship) or does not criticize or get ahead of the CCP. Indeed, one might say that the most important kind of freedom for innovation is the ability to do innovation with generous funding, something that is much easier for Chinese scientists than for Americans, especially given the declining federal funding for R&D.

China Can Innovate

More recently, some assessments have argued that China can innovate—if not across the board, then at least in some select key technologies. For example, WIPO’s 2022 Global Innovation Index ranks China 11th most innovative in the world and states, “China stands out for producing innovations that are comparable to those of the high-income group.”[48] A recent article by IMD Professor Georges Haour tells us, “Why China is on the way to being a global innovator.”[49]

Others have argued that China may be an innovation leader in certain new technology areas, such as quantum computing, fusion, and AI.[50] For example, in the article “Why China will win the global race for complete AI dominance,” the author stated that Kai-Fu Lee believes:

We’re in the age of implementation, we’re in the age of data, and China has a better set, a larger set of implementers or good AI engineers who get the work done, who make the algorithms run fast, connect to business logic. The West needs to revise its view of Chinese technology companies being copycats of western products, and acknowledge that, in fact, some categories of Chinese technology are best-in-class. [51]

The biggest danger for Silicon Valley, according to Lee, lies in “solipsism and complacency in its own supremacy.” Lee also pointed out that China suffers much less from incumbents using their political power to prevent the adoption of new technologies. He also could have just as easily said that “neo-Luddite” forces in China resisting new technologies, such as AI, facial recognition, automation, and other disruptive technologies, are much less than in the United States, and to the extent they exist in China are suppressed by the state.

Likewise, a 2021 report from Harvard’s Belfer Center, “The Great Tech Rivalry: China vs the U.S.,” argues that China has become a serious competitor in the foundational technologies of the 21st century: AI, 5G, quantum information science (QIS), semiconductors, biotechnology, and green energy. The report notes, “In some races, it has already become No. 1. In others, on current trajectories, it will overtake the U.S. within the next decade.”[52] It attributes this to a strong R&D ecosystem as well as the top-performing Chinese universities that continue to improve.

China technology expert Dan Wang has argued:

China’s technological development is considerably more dynamic than the country’s image suggests. China remains behind in several critical areas, and some of its most important tech firms face regulatory squeezes—whether from Washington or Beijing itself. Regardless of these challenges, Chinese industries are reaching world-class standards, and the country’s science is steadily advancing. Along the way, Chinese firms have begun to make significant innovations of their own, including in strategic areas that the United States has prioritized.[53]

Tim Ruhlig argued that China is innovative and that the role of the CCP has been a plus, not a negative: “Although widely thought to hamper innovation, the role of the party-state should be considered the Fourth Virtue that has made China innovative. It is certainly true that central planning is an obstacle to creativity and thereby to innovation.”[54]

Matt Sheen, a fellow at the Carnegie Endowment for International Peace, argued that China is an “innovation powerhouse” because of its “large, semi-protected market; ties with researchers and companies around the world; and waves of financial, human, and physical capital invested in promising fields like AI,” all factors promoted by the government.[55]

There are also structural factors that suggest that China could emerge as a global innovation leader. Huang and Sharif argued that three factors will play a key role in making China a technology leader: China’s large market (which lets innovative firms drive down marginal costs faster than others), the centralized system of government that enables China to provide significant support to innovative firms, and China’s strong role in international markets to acquire advanced technologies while increasing its capacity to undertake advanced R&D, often in partnership with foreign interests seeking access to the Chinese market. They argued that these three factors will make China the global technology leader “over the long term.”[56]

A Harvard Belfer Institute study argues that “China’s whole-of-society approach is challenging America’s traditional advantages in the macro-drivers of the technological competition, including its technology talent pipeline, R&D ecosystem, and national policies.”[57]

Finally, as China technology expert Dan Wang wrote:

But amid these serious vulnerabilities, China is making rapid progress in many other technologies. Chinese firms have quickly gained ground against their European and Japanese counterparts in the production of advanced machine tools such as robotic arms, hydraulic pumps, and other equipment. As the iPhone demonstrates, China now rivals Japan, South Korea, and Taiwan in its mastery of the electronics supply chain. And in the digital economy, despite recent efforts by President Xi Jinping to tighten government control of Internet companies such as Alibaba, Tencent, and Didi, China remains strong. Chinese companies can still offer spirited competition to Silicon Valley’s tech giants, as ByteDance’s TikTok has been doing to Facebook. China leads the world in building modern infrastructure, including ultra-high-voltage transmission lines, high-speed rail, and 5G networks. In 2019, China became the first country to land a rover on the far side of the moon; a year later, Chinese scientists achieved quantum-encrypted communication by satellite, pushing the country closer to creating unbreachable quantum communications. These achievements are emblematic of China’s steady effort to master more and more difficult tasks.[58]

Innovation Analysis

Determining what to measure depends in large part on what question one wants to answer. Ideally, innovation should be defined as output and market share in new-to-the world products and services. In other words, invention is not a challenge to market leaders; only innovation is, with innovation being defined as successfully bringing a new product or process to market. Nor are innovation inputs and outputs to the innovation process, such as R&D spending and patents, a challenge to market leaders. Those are useful indicators, but ultimately, they are inadequate to truly measure innovation.

Given the lack of adequate Chinese data, it is not possible to measure output and market share for some, if not most, industries and technologies. But it is possible to assess the development of innovative products in many Chinese firms. Chinese-owned companies are the focus, not the Chinese economy, because foreign firm operations in China are much less of a threat to allied economies than Chinese firms are. Foreign firms may move some production and research to China, but their goal is not to displace themselves. In contrast, the goal of many Chinese-owned firms is, like most multinational firms, to win global market share. Moreover, over time, the role of foreign firms in China will continue to shrink as the Chinese government continues its progress with “indigenous innovation” (innovation by Chinese companies). That is why the focus is not on Chinese innovation, but rather on Chinese firm innovation. The notion that “China” can or cannot do something well is of course misleading.

But what do we mean by “new to the world”? Clearly there is a difference between innovation that is new to a firm or even new to a country. For example, surveys asking Chinese firms if they have innovated show similar, if not even higher, rates than firms in more advanced nations. But this only means that Chinese firms are doing something different than they had been doing, even if that means copying foreign innovations and technologies.

Unfortunately, there are no hard and fast definitions of “new-to-the-world” and “leading edge.” Moreover, for many products, firms incorporate many existing products and innovations, but also add some components and functions that are new. As a rough rule, ITIF defines “leading-edge innovation” as something a firm does no later than a year after something has been introduced somewhere else in the world. Anything longer risks picking up developments that are based more on copying. And a significant part of the new product must be innovative and new. Clearly assessing these factors involves a judgment call. There is no hard and fast rule as to how much copying a firm engages in would disqualify a technology from being defined as innovative. Almost no firm is a completely original innovator. Even Apple incorporated an array of prior innovations to develop the iPhone. But we define copying as largely and substantially using technology and features that are already in existing non-Chinese products, and innovation as the opposite.

Over time, the role of foreign firms in China will continue to shrink as the Chinese government continues its progress with “indigenous innovation.”

Unfortunately, with the exception of drug approvals for the biopharmaceutical industry, there is no readily available data base assessing the number and extent of innovations from Chinese firms. As such, we use three methods to assess Chinese firm innovation. The first, and least useful, is a review of quantitative innovation indicators, such as R&D personnel, patents, and article citations. These are useful, but not determinative.

The second is an analysis of individual Chinese firms. We use as a population of Chinese-headquartered firms listed on the EU R&D 2,500 list (the list of the world’s top 2,500 R&D spenders). A total of 679 Chinese companies were on the 2023 list, and we selected, mostly at random, although we tried to ensure broad sector coverage, 44 companies to examine more closely. At one level, this is a biased sample in that it only includes leading R&D spenders. But these are the kinds of companies most likely to be innovative, so to the extent that they are not, this tells us a lot about Chinse innovation capabilities. While we selected at least 2 companies to fit with the 11 in-depth industry/technology case studies, for the rest, we chose randomly. Relying on native Chinese language researchers, we reviewed company annual reports and investment analyst reports to qualitatively assess the product innovations these companies have developed and the extent to which these are or close to new to the world. ITIF experts then independently scored each firm on a scale from 1 to 10 (1 being a complete copier to 10 being at the leading edge of innovation in the world).

Third, we examined nine key industries and technologies important to national security and national economic power: EVS, robotics, semiconductors, chemicals, AI, biotechnology, quantum computing, displays, and commercial nuclear power. Some of these technologies are dual use and important to not only U.S. national security but also its economic security.[59] Others are emerging technologies that help shape technology competition.[60] To do that, we relied on interviews and roundtables with experts on Chinese industries. For the most part, we did not interview experts in China, in part because of current CCP restrictions on sharing information with foreigners, but also because we were not certain we would obtain objective information.

A limit of these methodologies is the extent to which firm studies and industry case study results can be generalized. One way we addressed this was to examine a range of companies and industries. But to be sure, both were samples, and it’s possible that the innovation performance of other companies and innovation-based industries is considerably different. Of course, examining even more industries in depth would have been better. But the time cost involved in doing so is extensive. Even with the limitations discussed, the fact that the same general dynamics were found in all 11 industries suggests that the results are likely to be generalizable across virtually all Chinese globally traded industries, especially the ones the Chinese government is targeting.

We also chose not to use some cross-national datasets on firm innovation performance, for two reasons. First, national surveys of firm innovation performance (e.g., asking questions such as what percentage of firm revenue came from new products) do not differentiate between products new to a firm, new to a country, and new to the world. Second, these surveys appear to not be comparable across nations. For example, OECD reports that 80 percent of Canadian firms are innovative, compared with 38 percent of American firms, a lead that most Canadian innovation policy experts would find dubious at best. It also reports that 38 percent of Chinese firms are innovative (from the 2108 Chinese Innovation Survey), equal to the U.S. number, and Chinese manufacturing firms overall are the most innovative in the world. This is likely to be more of a result from survey bias than actual performance, just as it appears that Chinese firms over-report R&D expenditures to the government and seek to inflate their innovation performance.[61] It could also be an indication that the survey only asks the firm if it is innovative compared with what it had been doing.

For the most part, we also chose to focus on product innovations and not on process innovations for several reasons. First, many process innovations are a way for a firm to lower production costs. China can and does that in many ways, including government subsidies, currency manipulation, and others. Second, and more importantly, it is extremely difficult to measure process innovations because, by definition, they are within the firm and not sold in the marketplace. This should not diminish the importance of process innovation. There are innovations that U.S. companies have come up with, but the United States has lacked the processes and skills needed to make them. This broader manufacturing ecosystem, including technical skills and deep supplier networks, is one reason China has been so successful in advanced manufacturing.[62]

One final note on methodology: The goal of this study was not to predict future technological developments. Both private markets, the main determinant, and government policies are themselves highly unpredictable, and the interactions and eventual outcomes among them are even more so. But to use an analogy, if someone observes a sports team with great athletes working out intensely and supported with a massive budget, it’s not unreasonable to predict that this team is likely going to be successful. In other words, while it is not possible to predict the course of technology development (will EVs, or hydrogen vehicles, become dominant?), it is possible to assess current positions and momentum, and that should and can inform likely predictions about the future.

Despite the limitations of raw data, the following section examines an array of empirical data sources and studies to assess both trends and levels in Chinese innovation. The overall finding is that, in some areas and industries, China appears to be ahead of the rest of the world, and in most others, it is rapidly catching up.

Empirical Data

Normally, to assess how innovative a country is compared with others, measures should be examined controlling for the size of the economy. Otherwise, an extremely innovative small country would look less innovative than a very large country that is not very innovative. However, when assessing how innovative Chinese industries are, and the threat that poses to other nations’ industries, total figures are extremely relevant because firms don’t compete against an entire country, but rather against other firms. Therefore, this section examines total figures.

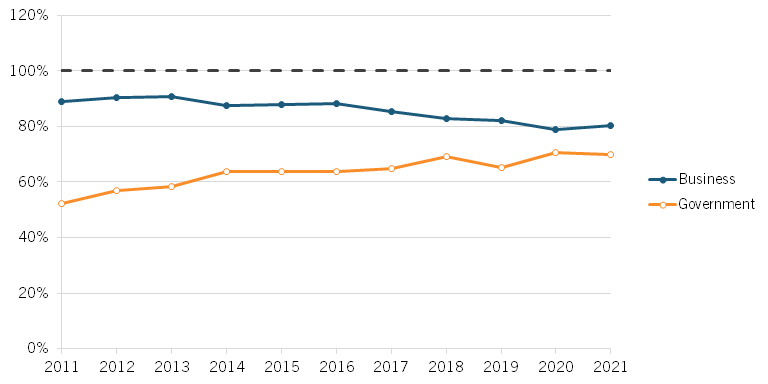

Figure 6 shows the number of total full-time researchers in China relative to the number in the United States. In 2011, China’s total number of researchers exceeded 1.3 million, almost 20 percent more than the 1.1 million researchers in the United States. The dashed line represents the total number of researchers in the United States over this same period. By 2021, the gap between China and the United States had increased substantially. The number of researchers in China increased by over 1 million employees to 2.4 million, almost 50 percent more than the total in the United States, 1.6 million.

Figure 6: Number of researchers in China relative to number in the United States[63]

Figure 7 shows the number of researchers employed by private businesses in China as a percentage of all researchers, relative to the United States. In 2011, 62 percent of full-time researchers in China were employed by private business enterprises compared with 74 percent in the United States. Over the decade, the share of business researchers decreased substantially compared with the United States. In 2021, only 58 percent of researchers were employed by private businesses in China, compared with 83 percent in the United States. This trend reveals an increasing concentration of research conducted in the business sector in the United States, while the opposite occurs in China.

Figure 7: China’s researchers in the business sector as a share of total researchers, relative to the United States[64]

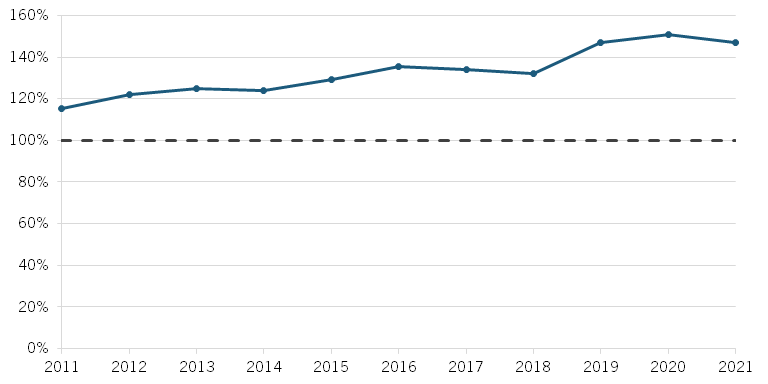

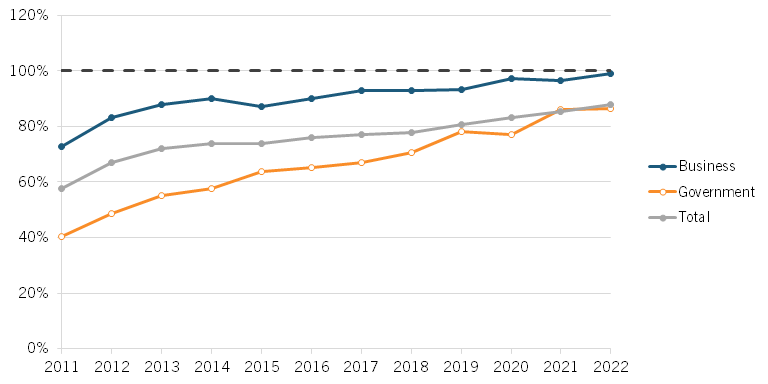

Figure 8 shows gross expenditure on R&D by performing sector in China relative to the spending in the United States from 2011 to 2022. In all sectors and in overall expenditure, China neared the United States in R&D spending. In 2011, China spent $246 billion on research, just 58 percent of the $427 billion spent by the United States that same year. However, 11 years later in 2022, China had crept much closer to the United States, now spending $811 billion, or 88 percent of the $923 billion spent by America. Sectorally, China has also come close to equaling the United States, represented on the graph as the black dotted line. China spent 86 percent of the United States’ expenditure on government research, and in the business sector, China’s expenditure in R&D was virtually equal to that of the United States; in 2022, China spent $641 billion while the United States spent $646 billion.

Figure 8: China’s gross domestic expenditure on R&D by sector, relative to the United States[65]

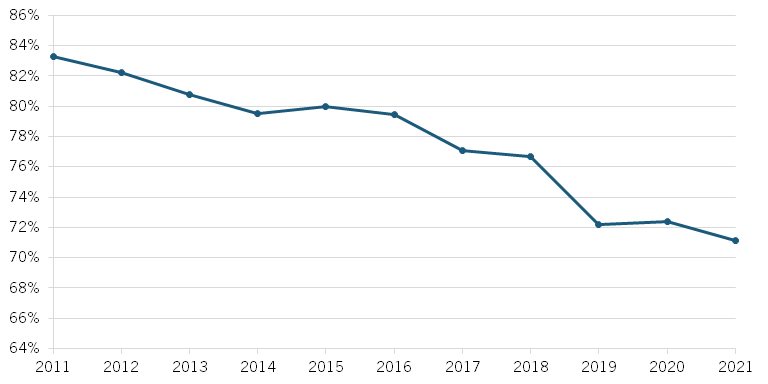

Figure 9 depicts the R&D intensity in China by performing sector, relative to the United States. Between 2012 and 2022, R&D expenditure by private businesses increased in both countries. In 2012, the R&D intensity in China was 1.42 percent or 89 percent of the R&D intensity in the United States. By 2022, the R&D intensity in the business sector in China had declined, while the intensity by government entities increased. Most recent data shows that the R&D intensity in China’s business sector has declined to just 80 percent of the United States, while R&D intensity financed by China’s government has increased to 70 percent of U.S. levels, an increase of 18 percent over the past decade. The dashed line represents the level at which R&D intensity in China would be equal to the United States.

Figure 9: R&D intensity in China by performing sector relative to the United States[66]

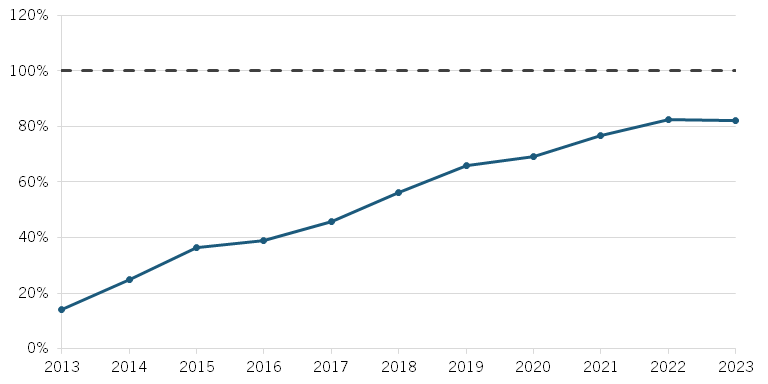

Every year, the European Commission compiles a list of the firms that have invested the greatest amount of money in R&D. Figure 10 shows the number of these firms that were concentrated in the United States and in China. Since 2013, China had made significant gains compared with the United States, represented as the dashed line. In 2013, 658 of the top-R&D-spending firms were located in the United States, almost six times more than the 93 firms located in China. By 2023, the numbers in the United States and China had increased, but not proportionally. China had increased its top R&D firms sevenfold, with 679 firms making the list in 2023. In the United States, 827 firms made the list.

Figure 10: Number of global top R&D investment firms in China relative to the United States[67]

Figure 11 demonstrates the growth in scientific and technical articles published in China relative to the United States from 2010 to 2020. In 2012, about 330,000 articles were published in China, and just 75 percent of the over 430,000 articles were published in the United States that same year. However, by 2016, China had surpassed the United States. The dashed line represents the number of articles the United States publishes annually. Most recent data from 2022 shows that China continues to exceed the United States, publishing almost 900,000 articles, 47 percent more than the 457,000 published in the United States.

Figure 11: Number of science and technical articles published in China relative to the United States

To be sure, some of China’s published papers appear to be fraudulent, based on strong incentives to “publish or perish.”[68] However, one academic study that controlled for a number of independent measures, including type of journal, finds that China is farther ahead in top-level academic journal publications than is generally believed and that China overtook Europe in 2015 and the United States in 2019. Wagner, Zhang, and Leydesdorff wrote:

The top-1% analysis using field normalization may have obscured the fact that China is operating at world-leading levels of scientific output in both volume and quality. The increase of the quality of China’s scientific output challenges a number of assumptions about the ways or conditions within which nations build scientific capacity. China’s science policy has propelled the nation to world-class levels in a very short time period, moving the nation’s profile from rapid imitation to levels challenging nations with a longer history of world-leading science.[69]

Clarivate, a data analytics company, produces an annual list of highly cited researchers, or “influential researchers … around the world who have demonstrated significant and broad influence in their field(s) of research.” Figure 12 shows the share of these highly cited researchers located in China relative to the United States. In 2018, over 43 percent of highly cited researchers were located in the United States, while only 8 percent were found in China. However, over the next several years, the number of these influential researchers in the United States fell, while in China the opposite occurred. By 2023, the number of highly cited researchers more than doubled there, with 18 percent of all highly cited researchers living in China. Meanwhile, the share of these researchers in the United States fell to 38 percent.

Figure 12: Share of highly cited researchers in China relative to the United States[70]

Figure 13 shows the number of top 100 global universities in China relative to the United States from 2013 to 2023. In 2013 through 2015, China had no universities in the top 100 of the Academic Ranking of World Universities, a list published by the Center for World-Class Universities, while the United States had over 50 each year. By 2023, China had increased its number of top universities to 11, 29 percent of the 38 universities the United States had in the top 100.

Figure 13: Number of top 100 universities in China relative to the United States[71]

Figure 14 shows the change in gross VC investment in China relative to the United States from 2015 to 2023. Over this period, VC in both countries saw a relative decrease. In 2015, China saw about $53.2 billion in VC investment, 20 percent more than the $43 billion invested in the United States. The difference in VC investment between China and the United States hit its peak in 2018, when China received $123.5 billion. The United States fundraised just $71 billion that same year. After 2018, China faltered in VC investment, losing a substantial amount of fundraising in the several years following. As of 2023, the two countries each raised about $27 billion in VC fundraising.

Figure 14: Gross VC investment in China relative to the United States[72]

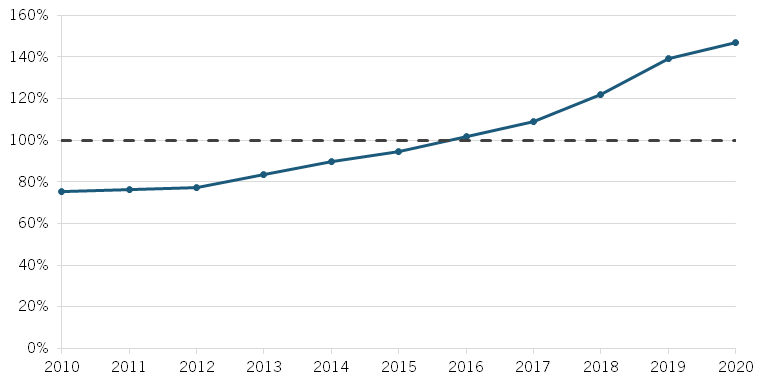

Figure 15 shows the number of Patent Cooperation Treaty (PCT) patent applications for China relative to the number of applications in the United States. From 2011 to 2021, China surpassed the United States, represented by the dashed line, in patent applications. In 2011, Chinese filers applied for just over 17,000 patent applications, only 35 percent of the 49,000 applications from the United States. Over the next decade, both countries increased their patent output; however, China did so faster. In 2019, China officially produced more patents than the United States did for the first time in history, and by 2021, China had produced over 67,000 patent applications per year, 19 percent more than the 56,467 patent applications produced in the United States.

Figure 15: Number of PCT patent applications for China relative to the United States[73]

China has been known to publish a significant number of false or dubious patents, making the number of sheer patent applications misleading. Instead, looking at the number of patents granted by the United States Patent and Trademark Office (USPTO) can provide a more truthful estimate of the number of legitimate patents published by China. Figure 16 shows the share of patent grants awarded by the USPTO to Chinese firms from 2010 to 2020. In 2010, China was granted just 3,303 patents, less than 1 percent of all patents awarded in the United States that year. Yet, by 2020, China’s patent grants in the United States increased to almost 27,000, 7 percent of all grants. China had the third-most patents granted by USPTO in 2020, behind only the United States and Japan—evidence that, despite some questionable patents, China is publishing many quality patents.

Figure 16: Share of patent grants awarded to Chinese firms by USPTO[74]

China had the third-most patents granted by USPTO in 2020, behind only the United States and Japan—evidence that, despite some questionable patents, China is publishing many quality patents.

Another study of patenting by Bergeaud and Verluise finds that China’s contribution to frontier technology had become quantitatively similar to U.S. levels in the late 2010s while overcoming the European and Japanese contributions, respectively. Although in some ways China still exhibits the hallmarks of a catching-up economy, that veneer has quickly faded. The quality of frontier technology patents published at the Chinese Patent Office has leveled up to the quality of patents published at the European and Japanese patent offices. At the same time, frontier technology patenting at the Chinese Patent Office seems to be increasingly supported by domestic patentees, suggesting the buildup of domestic capabilities.[75]

Another study of Chinese patenting finds that, in the last decade, Chinese patents have become less dependent on foreign knowledge and technology, and the importance of Chinese patents relative to USPTO patents has steadily increased over the last two decades. Moreover, Chinese and foreign patenting have become more similar in terms of specialization across technology classes, suggesting that China is now innovating in areas similar to the global leaders.[76]

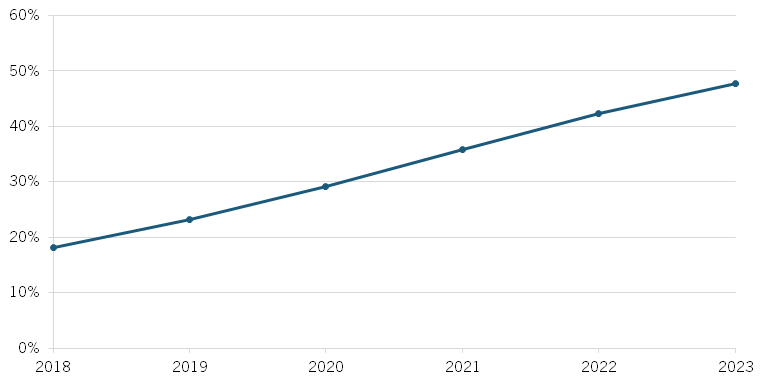

Figure 17 shows the value of IP licensing receipts in China relative to the United States from 2013 to 2023. Over this period, the value of IP licensing receipts in China increased relative to that of the United States. In 2013, IP receipts in China were valued at less than 1 percent of the value in the United States. Yet, by 2023, this value had increased to 9 percent, with a peak of 10 percent in 2022. The United States still maintains a significant lead in the value of IP licensing receipts; however, China has made gains over the past decade.

Figure 17: Value of IP licensing receipts by China relative to the United States[77]

Since 2017, WIPO has produced an annual report ranking the top 100 science and technology clusters, or “local concentrations of world-leading science and technology activity.” These clusters are hubs of innovation, with high rates of patent applications, scientific and technical article publication, and great densities of large firms with high rates of R&D investment. Figure 18 shows the number of these hubs that were located in China relative to the United States between 2017 to 2023. Over this time, China rapidly increased its number of clusters, from just six in 2017 to 23 in 2023. At the same time, the United States, represented by the dashed line, stayed relatively stagnant in its number of clusters, with 22 clusters in 2017 and 21 clusters in 2023. As of 2023, China had two more scientific clusters in the global top 100 than the United States did.

Figure 18: Number of WIPO global innovation clusters in China relative to the United States[78]

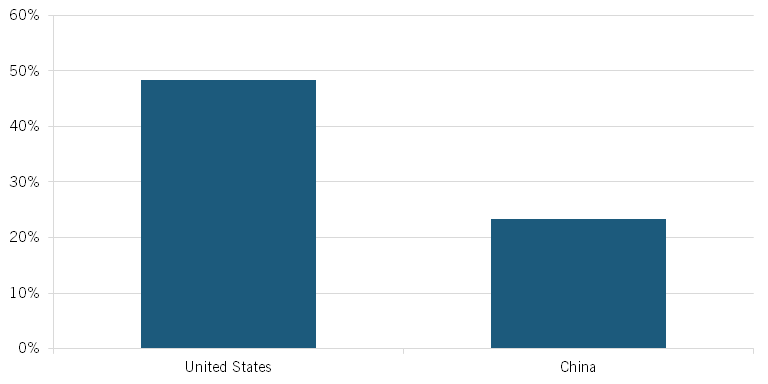

Unicorns are private start-up companies that have a value of over $1 billion. As of April 2024, there were 1,453 unicorn companies, with many concentrated in the science and technology sector. Figure 19 shows the share of unicorns concentrated in the United States and in China. The United States accounts for most of the world’s unicorns at 48 percent, while China holds 23 percent.

Figure 19: Unicorns in the United States and China as a share of total unicorns in 2024[79]

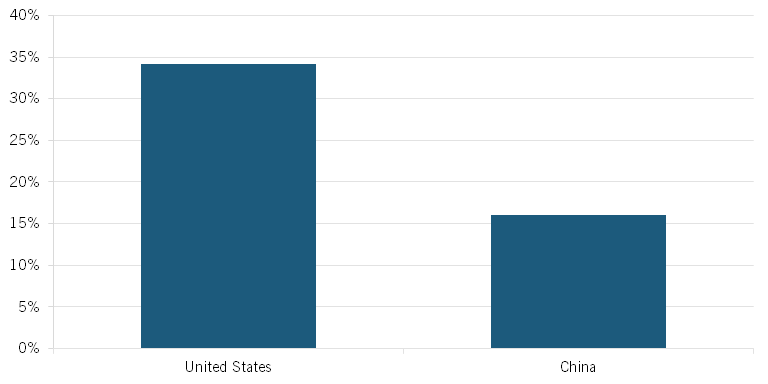

Figure 20 depicts the number of supercomputers located in China and the United States as a share of the top 500 supercomputers in the world. In 2024, the United States housed 171 of the top 500 supercomputers, or 34 percent of the most-powerful supercomputers in the world. China, on the other hand, held just 80 supercomputers, or 16 percent of the top 500 supercomputers in the world.

Figure 20: Share of supercomputers in the top 500 in China and the United States in 2024[80]