Economic Consequences of Section 232 Tariffs on Semiconductor Imports

The Trump administration has imposed tariffs on semiconductor imports on national security grounds under Section 232 of the Trade Expansion Act. These tariffs would raise ICT prices and thereby lower ICT consumption and capital stocks, which would reduce economic growth and lower Americans’ living standards.

KEY TAKEAWAYS

Key Takeaways

Contents

Modeling the Economic Impact of Possible U.S. Semiconductor Tariffs 3

Importance of Semiconductors in American Tech Leadership. 9

Introduction

Semiconductors represent the foundational technology underpinning the modern digital economy. The global semiconductor industry generated approximately $791.7 billion in revenue in 2025 and is projected to surpass $1 trillion by the end of the decade, while enabling an estimated $7 trillion in annual global economic activity through downstream industries and applications.[1] These tiny yet extraordinarily sophisticated components power virtually every modern technology, including smartphones, cloud infrastructure, automobiles, industrial machinery, and defense systems. In other words, semiconductors serve as the computational backbone of the digital age, providing the processing, memory, sensing, and power-management capabilities that support artificial intelligence (AI), advanced manufacturing, telecommunications, and other technology-intensive sectors of the economy.

As such, semiconductors are not merely another traded product; they represent a critical capital good that supports productivity growth, innovation, and competitiveness across the broader U.S. economy. Indeed, American leadership and competitiveness in industries such as AI, quantum computing, cloud services, e-commerce, aerospace, and advanced manufacturing depend heavily on reliable access to advanced semiconductor technologies. In many respects, semiconductors function as the “electricity” of the digital economy: when semiconductor supply chains are disrupted or costs rise significantly, the effects ripple throughout the entire economy. The semiconductor shortages experienced during the COVID-19 pandemic illustrate this reality clearly, as disruptions contributed to production slowdowns in industries ranging from automotive manufacturing to consumer electronics. These disruptions cost the global economy billions of dollars in lost output.

Despite the central importance of semiconductors to U.S. economic growth and technological competitiveness, the Trump administration has once again targeted semiconductor imports with tariffs, this time under Section 232 of the Trade Expansion Act, citing national security concerns. In an executive order issued in January 2026, the administration imposed a 25 percent tariff on a narrow category of advanced semiconductor components while signaling the possibility of significantly broader tariffs during a second phase following trade negotiations.[2] The executive order asserts that “it is necessary and appropriate to impose an immediate 25 percent ad valorem duty rate on the import of certain advanced computing chips and certain derivative products.”[3]

While concerns about national security can be legitimate, applying Section 232 tariffs to semiconductors risks undermining U.S. competitiveness and jeopardizing broader U.S. national security objectives. Indeed, modern national security depends on maintaining technological leadership and economic strength, which semiconductor imports provide by supporting critical U.S. technology industries. But with the implementation of tariffs, these U.S. industries will face higher costs to obtain the most advanced semiconductors from abroad. Indeed, as the International Trade Administration has asserted, “Taiwan Semiconductor Manufacturing Company (TSMC) dominates the market, with U.S. firms such as Apple, NVIDIA, and AMD relying heavily on its advanced manufacturing capabilities.”[4] As such, these U.S. industries may be forced to rely on older chips, posing challenges in developing and deploying the most sophisticated technologies tied to national security.

Because semiconductors represent essential inputs for industries ranging from automobiles to consumer electronics, tariffs that raise chip costs could increase prices, reduce consumer demand, and discourage business investment across the broader economy. Rather than strengthening America’s strategic position, sweeping semiconductor tariffs could slow technological development, reduce business investment, weaken productivity growth, and impair the broader innovation ecosystem that underpins both U.S. economic and military strength. If these effects become widespread, especially during periods of weak growth or high inflation, they could slow economic activity. In this sense, semiconductor tariffs may ultimately weaken national security rather than strengthen it.

This report proceeds by modeling the economic impact of tariffs on U.S. (finished-good) semiconductor imports. It finds that—if blanket 25 percent semiconductor tariffs were applied—these tariffs would decrease U.S. gross domestic product (GDP) growth by 0.19 percent in the initial year and, if sustained, would lead to 0.60 percent less GDP growth in the 10th year post-implementation than would otherwise be the case. Tariffs set at 10 percent would lead to 0.06 percent of GDP growth foregone in the initial year and 0.17 percent lost in the 10th year. Meanwhile, a 50 percent tariff would result in 0.40 percent of U.S. GDP growth foregone in the initial year and 1.94 percent in year 10. A 25 percent tariff would reduce U.S. GDP per capita by an average of $170 in the first year and a cumulative total of $4,825 by the 10th year if sustained for that duration.

Modeling the Economic Impact of Possible U.S. Semiconductor Tariffs

The following lays out a framework for modeling the economic impact of possible U.S. semiconductor tariffs and then analyzes the economic impact of various tariff scenarios.

Framework

The Information Technology and Innovation Foundation (ITIF) has developed a model to estimate the impact a 10 percent, 25 percent, and 50 percent tariff on U.S. semiconductor imports would each have on the American economy. Since semiconductors underpin virtually all information and communications technology (ICT) products, an increase in tariffs would effectively amount to a price hike on the majority of ICT goods. As such, businesses and consumers alike that rely on ICT products and services—such as computers, smartphones, and AI tools—would face higher prices and accordingly reduce demand for these products.

Consumption of ICT goods is highly price elastic. For instance, a study by Cette et al. finds that ICT goods have a price elasticity of 1.3, suggesting that a 1 percent increase in ICT prices induces a 1.3 percent decline in ICT consumption. (However, for this report, ITIF used a more conservative elasticity of 1.15, since ICT inputs for businesses tend to be slightly less price elastic than for consumer consumption.) The elasticity of demand for ICT products can therefore be used to estimate the decline in semiconductor imports associated with reduced ICT consumption under tariff rates of 10, 25, and 50 percent.

Over time, as the cost of semiconductors rises, the consumption of ICT products falls. That means, for instance, that U.S. manufacturers might purchase fewer productivity-enhancing ICT goods such as robots (China already deploys 12 times as many robots as does the United States on a wage-adjusted basis), or perhaps that they revert from using digital to manual processes.[5] For example, firms may delay investments in productivity-enhancing technologies such as automated inventory systems as ICT costs rise. This reduced ICT consumption will lead to a decline in U.S. ICT capital stock, or the total value of ICT capital in the United States, less depreciated capital.

ICT capital has been shown to positively affect both productivity and economic growth.[6] Given this, a decline in capital stock would have an inverse effect, slowing U.S. economic growth. Using a study by Cardona et al., ITIF applied a multiplier suggesting that a 1 percent decrease in a nation’s net ICT capital stock results in a 0.06 percent decrease in its real GDP. Multiplying the United States’ estimated annual net decline in ICT capital stock (as a result of the tariffs) by this multiplier provides an estimate of the potential negative impact a semiconductor tariff would have on U.S. GDP.

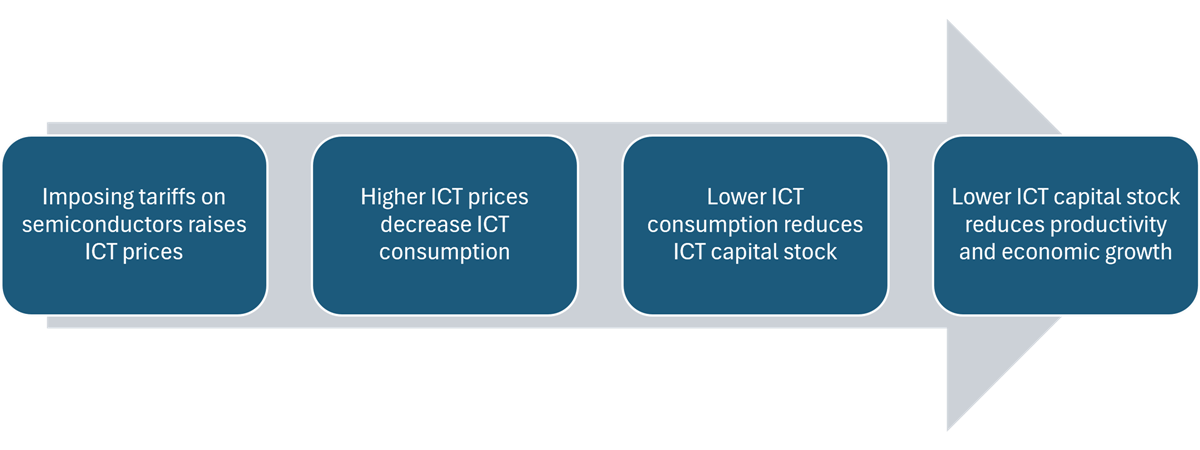

Figure 1 shows the analytical framework ITIF’s model uses to estimate the economic impact of semiconductor tariffs on the U.S. economy.

Figure 1: ITIF’s analytical framework for modeling the deleterious effects of semiconductor tariffs

Economic Analysis

Using data from USA Trade, the International Trade Center, and the Organization for Economic Cooperation and Development (OECD), ITIF calculated that, in 2025, the United States imposes an average tariff rate of 2.42 percent on semiconductor imports.[7] However, this low tariff level has already increased: in January 2026, the Trump administration used Section 232 to impose a 25 percent tariff on a narrow category of semiconductors, with the possibility of imposing broader tariffs on semiconductors at “a rate of duty that is significant” in a second phase.[8]

The United States imported $48.1 billion of semiconductors in 2025, representing about 1.4 percent of all U.S. imports that year.[9] Assuming that the Trump administration implements blanket 25 percent tariffs on all semiconductors, the effective tariff rate would increase 22.6 percentage points above the current average tariff level. Using an ICT price elasticity of 1.15, ITIF estimated that ICT consumption would decline by 26 percent, equivalent to a $12.5 billion decline. The decline in ICT consumption would also mean, in turn, a decline in the nation’s ICT capital stock.

By year 10, semiconductor tariffs set at 25 percent would translate into a cumulative $1.6 trillion decline in GDP, or 3.9 percent of U.S. GDP.

ITIF estimated that the initial U.S. ICT capital stock was 22 percent of U.S. manufacturing net equipment stock in 2022, or $396 billion.[10] Thus, a 25 percent tariff on semiconductors would cause a 3.2 percent decrease in ICT capital stock.

According to M. Cardona et al., ICT has an investment elasticity of 0.06, meaning that a 3.2 percent loss in ICT capital stock would translate into a 0.19 percent loss in economic growth in the initial year such tariffs were imposed. (See table 1.)

Table 1: Economic impact on the United States from imposing a 25 percent tariff on semiconductor imports[11]

|

Indicator |

Economic Impact |

|

ICT price increase |

22.6% |

|

Initial change in ICT consumption and capital stock |

-$12.5 billion |

|

Initial change in GDP growth |

-0.19% |

|

10th-year change in GDP growth |

-0.60% |

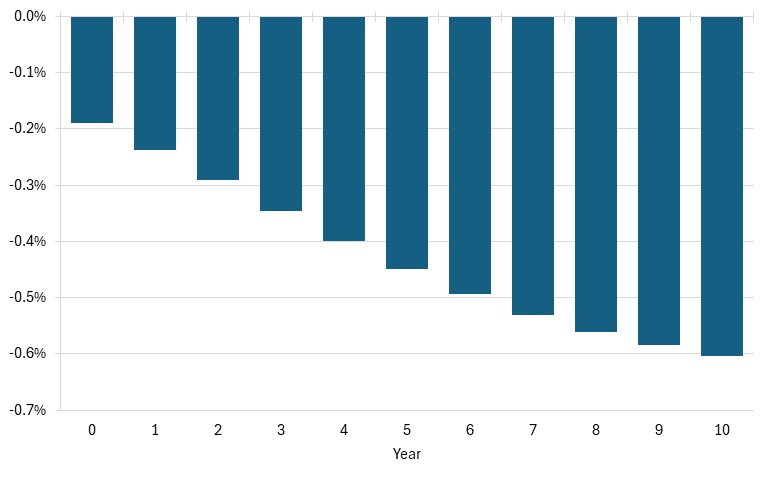

If a 25 percent semiconductor tariff were implemented and sustained over a 10-year period, the United States’ GDP growth would decline by 0.6 percent in the 10th year post-implementation. Although this decline may appear modest, the annual losses would translate into a cumulative $1.6 trillion loss in GDP over 10 years, representing 3.9 percent of projected GDP in the 10th year, absent the tariffs. (See figure 2.)

Figure 2: GDP growth foregone from a 25 percent tariff imposed on semiconductors[12]

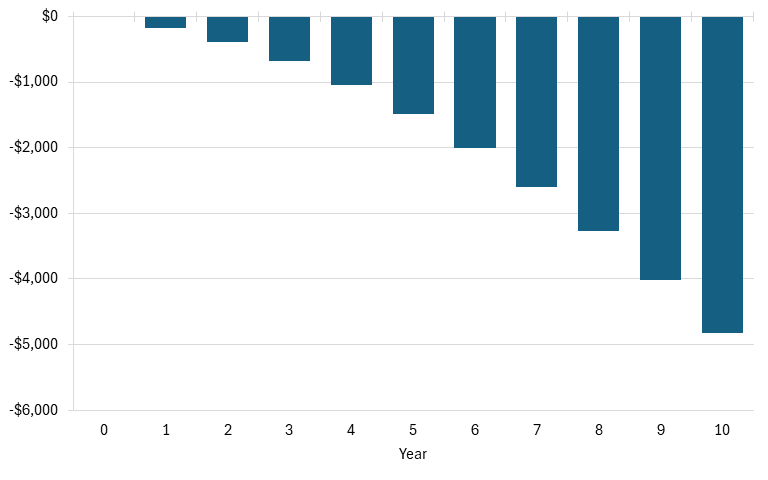

This foregone growth would mean a lower standard of living for Americans. Using the estimated 2025 U.S. population of nearly 342 million from the U.S. Census Bureau, the average American would experience $170 less growth in living standards the first year after a 25 percent tariff were imposed. By the 10th year, the average American would forego a cumulative $4,825 reduction in living standard growth. (See figure 3.)

Figure 3: Cumulative lost GDP per capita from a 25 percent tariff on semiconductor imports (2025 dollars)[13]

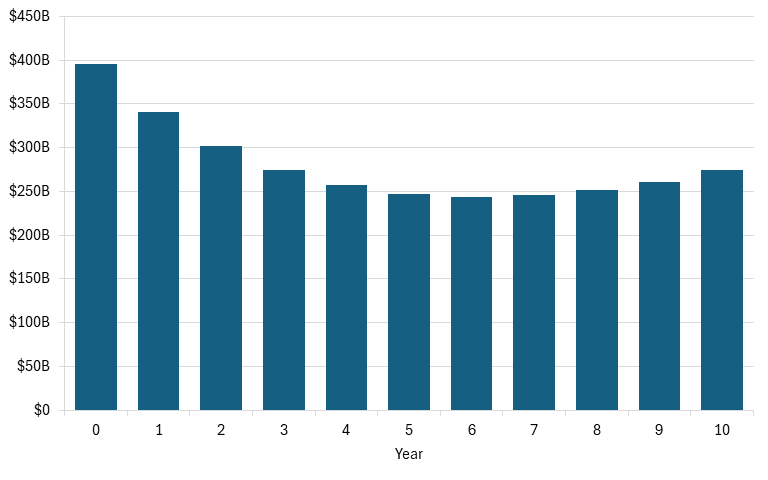

In addition to the GDP loss, the United States would also experience a decline in ICT capital during the first six years. Using data from the Bureau of Economic Analysis, Melina and Villa estimated an ICT capital depreciation rate of 5.7 percent per quarter, or 22.8 percent per year.[14] Considering the depreciation rate of ICT capital and the decline in semiconductor imports, ITIF has concluded that the United States would experience a 13.8 percent decline in ICT capital in the first year after 25 percent tariffs were imposed. The U.S. ICT capital stock would decline by an additional 11.5 percent and 9 percent in the second and third years, respectively, and would continue declining until year 7. By year 7, ICT capital would be only $246 billion, compared with the initial ICT capital stock of $396 billion. America’s ICT capital stock would remain below its initial level for an extended period. (See figure 4.)

Figure 4: U.S. ICT capital stock values after imposing a 25 percent tariff on semiconductor imports[15]

Given that the Trump administration may impose broad tariffs on semiconductors at an unknown level in the second phase of tariffs, ITIF also estimated the impact of a 10 percent and a 50 percent blanket tariff on semiconductors.

A 10 percent tariff on semiconductors would effectively raise ICT prices by 7.6 percent. This would translate into an initial $4.2 billion decline in ICT consumption and a 0.06 percent decline in GDP growth. In year 10, U.S. GDP growth would decline by 0.2 percent. (See table 2.) This would translate into a cumulative loss of $497 billion, or 1.2 percent of GDP, had tariffs not been implemented. For the average American citizen, GDP per capita would be $57 lower in the first year and would see a cumulative loss of $1,454 by the 10th year.

Given the impact of a 25 percent tariff on semiconductors, a higher tariff rate would be even more damaging to the U.S. economy. Indeed, modeling the impact of a 50 percent tariff rate, ITIF found that U.S. GDP growth would decline by 0.4 percent in the first year and by 1.94 percent in the 10th year. For the average American citizen, this would mean living-standard growth would be $358 less in the first year and there would be a cumulative $12,825 decline in living standards by the 10th year. (See table 2).

Table 2: U.S. economic losses from a 10, 25, and 50 percent tariff on semiconductor imports[16]

|

Indicator |

10 Percent Tariff |

25 Percent Tariff |

50 Percent Tariff |

|

ICT price increase |

7.6% |

22.6% |

47.6% |

|

Initial change in ICT consumption and capital stock |

-$4.2 billion |

-$12.5 billion |

-$26.3 billion |

|

Initial change in GDP growth |

-0.06% |

-0.19% |

-0.40% |

|

10th-year change in GDP growth |

-0.17% |

-0.60% |

-1.94% |

Importance of Semiconductors in American Tech Leadership

Even as the U.S. economy has grappled with the negative effects of tariffs, inflation, and, more recently, a global oil shock, it has continued to grow at a steady pace due largely to the country’s investment in AI and data center infrastructure. Top AI firms, such as Microsoft, Alphabet, Amazon, and Meta, have rapidly increased capital investment since 2020 in order to remain at the cutting edge of AI research, design, and infrastructure development. Capital investment in AI accounted for 1.2 percent of GDP in 2025, supporting broader economic growth, while investment by the top five hyperscalers in the United States is on track to reach $1 trillion by 2027.[17]

Data centers have become indispensable to the modern digital economy. Businesses depend on them to operate digital applications, including e-commerce platforms and web services used daily by millions of American firms and consumers. AI developers also rely heavily on data centers, especially to build increasingly advanced large language models (LLMs), since training generative AI systems requires access to vast amounts of data and computing power. At the same time, consumers’ reliance on data centers continues to grow as AI becomes an increasingly important tool for enhancing productivity both at work and in everyday life.

From 2023 to 2030, global demand for data center capacity is expected to increase at an annual rate of 22 percent.[18] Without continued rapid investment in AI infrastructure, data center capacity will be unable to meet the growing demand from businesses and consumers. At the same time, data centers are highly dependent on access to semiconductors. In fact, semiconductors can account for more than 50 percent of the total capital expenditures required to build and operate an AI data center, with some of the largest hyperscale data centers requiring hundreds of thousands of chips.[19] This is largely due to the wide variety of chips used in data centers, from the most cutting-edge central processing units (CPUs) and graphics processing units (GPUs) to the more standard memory chips found in most electronic devices.[20] A new report from the Semiconductor Industry Association and Deloitte finds that, by 2028, annual revenue from semiconductors used in AI data centers will increase tenfold from 2025 levels, reaching $1.2 trillion.[21]

Considering the massive quantity of semiconductors required for data center construction, and the critical role of data center and AI infrastructure investment in driving U.S. economic growth and U.S. leadership in AI, an increase in semiconductor tariffs would be self-defeating. Unlike with other products, firms can’t simply shift their supply chains in order to procure semiconductors domestically, as the United States produces less than one in eight of the semiconductors fabricated globally.[22] U.S. firms will have to continue importing semiconductors, regardless of the tariff, increasing the cost of data center construction and operations—costs that will inevitably be passed down to businesses and consumers. Worse yet, the increased costs could reduce data center construction moving forward, thereby slowing U.S. AI development.

Capital investment in AI accounted for 1.2 percent of GDP in 2025, supporting broader economic growth in the United States.

Slowing data center construction and increasing associated costs would weaken U.S. competitiveness in AI at a critical moment in the global technology race, giving China an opportunity to gain ground. AI development relies on the high-performance computing capacity housed in data centers, and increased hyperscaler costs would also increase costs for AI firms such as OpenAI and Anthropic. These added expenses would slow model training and reduce incentives for continued investment in U.S. AI infrastructure. At the same time, China is continuing to heavily subsidize its AI and semiconductor industries, enabling Chinese firms to expand their AI capabilities without facing the same financial constraints.[23] By misguidedly trying to protect American national security through tariffs, the Trump administration risks weakening the very technological leadership that underpins it.

Policy Recommendations

The Trump administration is justified in seeking to revive American semiconductor manufacturing capacity, but placing high blanket tariffs on semiconductors would introduce adverse consequences. Though tariffs may spur a resurgence in American chip manufacturing, the effects will be muted as firms grapple with the high costs of capital they impose. There are more effective and less harmful ways than tariffs to increase domestic semiconductor production. And that’s especially true in the midst of an ongoing memory semiconductor shortage, which already risks driving up prices for goods such as automobiles.[24]

Rather than raising tariffs on semiconductors and providing offsets to firms that invest in the United States, the Trump administration should remove all existing tariffs on semiconductors and focus on protecting and extending incentive programs for firms investing in domestic semiconductor production. The most important of these programs in the 2022 CHIPS and Science Act was the investment tax credit (ITC), which provided a 25 percent credit (since increased to 35 percent) to companies that begin construction of semiconductor-related manufacturing in the United States.[25] This program is currently set to expire at the end of 2026. Congress should extend the 35 percent ITC through 2030, and extend the credit beyond just chip manufacturing and apply it to firms investing in semiconductor research and design.

Should the administration continue with its semiconductor tariff regime, Congress should require that future tariffs enacted under Section 232 include annual reviews and automatic expiration after a specified date. This would ensure that tariffs on key products, such as semiconductors, are maintained only if they are effective at improving national security and do not unduly harm economic competitiveness.

The administration should also ensure that the offsets implemented under phase 2 of the Section 232 investigation are applied not only to semiconductor manufacturers but also to firms engaged in semiconductor research and design, as well as firms advancing U.S. competitiveness in AI. Investment in AI infrastructure, including data centers, has become a major driver of economic growth in the United States. Capital investment in AI alone accounted for about 1.2 percent of GDP in 2025. Given the importance of AI investment to the U.S. economy and the sheer volume of semiconductors that must be imported to build data centers, these firms should also be eligible for tariff offsets.

Conclusion

Ultimately, while the goal of strengthening U.S. national security is both valid and necessary, broad semiconductor tariffs imposed under Section 232 risk weakening the very economic and technological foundations that underpin America’s national security. Broad semiconductor tariffs are not the way to bolster U.S. national security. Semiconductors represent essential inputs that enable innovation, productivity growth, and leadership across nearly every advanced industry critical to both economic competitiveness and national defense. Tariffs on semiconductor imports would impose significant long-term costs on the U.S. economy through slower GDP growth, reduced household incomes, weakened industrial competitiveness, and potential loss of AI leadership.

In an industry defined by deeply integrated global supply chains and rapid technological advancement, policies that raise costs and restrict access to the world’s most advanced chips may ultimately undermine U.S. innovation capacity rather than strengthen it. A more effective strategy for enhancing national security would focus on expanding domestic innovation, strengthening alliances, and increasing U.S. semiconductor capabilities without imposing broad economic costs that could weaken America’s long-term technological and strategic leadership.

Acknowledgments

The authors would like to thank Stephen Ezell for his assistance with and feedback on this report. Any errors or omissions are the authors’ own.

About the Authors

Trelysa Long is a policy analyst at ITIF. She was previously an economic policy intern with the U.S. Chamber of Commerce. She earned her bachelor’s degree in economics and political science from the University of California, Irvine.

Meghan Ostertag is a policy analyst for economic policy at ITIF. She was previously an intern with the Federal Deposit Insurance Corporation. She holds a bachelor’s degree in economics from American University.

About ITIF

The Information Technology and Innovation Foundation (ITIF) is an independent 501(c)(3) nonprofit, nonpartisan research and educational institute that has been recognized repeatedly as the world’s leading think tank for science and technology policy. Its mission is to formulate, evaluate, and promote policy solutions that accelerate innovation and boost productivity to spur growth, opportunity, and progress. For more information, visit itif.org/about.

Endnotes

[1]. Semiconductor Industry Association, “Global Semiconductor Sales Increase 19.1% in 2024; Double-Digit Growth Projected in 2025,” news release, February 7, 2025, https://www.semiconductors.org/global-semiconductor-sales-increase-19-1-in-2024-double-digit-growth-projected-in-2025/; Oxford Economics, “Enabling the Hyperconnected Age: The role of semiconductors,” Semis Matter, 2013, 20, http://www.semismatter.com/enabling-the-hyperconnected-age-the-role-of-semiconductors/; “Global Annual Semiconductor Sales Increase 25.6% to $791.7 Billion in 2025,” Semiconductor Industry Association, February 6, 2026, https://www.semiconductors.org/global-annual-semiconductor-sales-increase-25-6-to-791-7-billion-in-2025/.

[2]. The White House, “Adjusting imports of semiconductors, semiconductor manufacturing equipment, and their derivative products into the United States,” executive order, January 14, 2026, https://www.whitehouse.gov/presidential-actions/2026/01/adjusting-imports-of-semiconductors-semiconductor-manufacturing-equipment-and-their-derivative-products-into-the-united-states/.

[3]. Ibid.

[4]. “Semiconductors including chip design for AI,” International Trade Administration, December 1, 2025, https://www.trade.gov/country-commercial-guides/taiwan-semiconductors-including-chip-design-ai.

[5]. Robert D. Atkinson, Meghan Ostertag, and Trelysa Long, “A Time to Act: Policies to Strengthen the US Robotics Industry” (ITIF, July 2025), https://itif.org/publications/2025/07/18/time-to-act-policies-to-strengthen-us-robotics-industry/.

[6]. Federico Biagi, ICT and Productivity: A Review of the Literature, working paper, Institute for Prospective Technological Studies, European Commission, September 2013, https://publications.jrc.ec.europa.eu/repository/bitstream/JRC84470/jrc84470%20final%20111113.pdf.

[7]. United States Census Bureau, “USA Trade (US imports for 8541 and 8542 in 2025),” accessed May 12, 2025), https://usatrade.census.gov/index.php?do=login; International Trade Center, “List of importers for the selected products (imported value for total all products),” accessed May 2026, https://www.trademap.org/Country_SelProduct_TS.aspx?nvpm=1%7c%7c%7c%7c%7cTOTAL%7c%7c%7c2%7c1%7c1%7c1%7c2%7c1%7c2%7c1%7c1%7c1; OECD, “Global Revenue Statistics Database tax revenue; taxes on income profits, and capital gains; general taxes on goods and services; and customs and import duties),” accessed February 2025, https://data-explorer.oecd.org/vis?fs[0]=Topic%2C1%7CTaxation%23TAX%23%7CGlobal%20tax%20revenues%23TAX_GTR%23&pg=0&fc=Topic&bp=true&snb=150&df[ds]=dsDisseminateFinalDMZ&df[id]=DSD_REV_COMP_GLOBAL%40DF_RSGLOBAL&df[ag]=OECD.CTP.TPS&dq=..S13._T..PT_B1GQ.A&lom=LASTNPERIODS&lo=10&to[TIME_PERIOD]=false.

[8]. The White House, “Adjusting imports of semiconductors, semiconductor manufacturing equipment, and their derivative products into the United States.”

[9]. United States Census Bureau, USA Trade (US imports for 8541 and 8542 in 2025), accessed May 12, 2026; UN Comtrade, Trade Data (total U.S. imports for 2025), accessed May 2026, https://comtradeplus.un.org/TradeFlow?Frequency=A&Flows=X&CommodityCodes=TOTAL&Partners=0&Reporters=all&period=2025&AggregateBy=none&BreakdownMode=plus.

[10]. National Institute for Science and Technology, “U.S. Manufacturing Economy,” https://www.nist.gov/el/applied-economics-office/manufacturing/manufacturing-economy/total-us-manufacturing.

[11]. United States Census Bureau, USA Trade (US imports for 8541 and 8542 in 2025); OECD, “Global Revenue Statistics Database”; U.S. Bureau of Economic Analysis, National Income and Product Accounts (Table 1.1.6. Real Gross Domestic Product, Chained Dollars), accessed May 2026, https://apps.bea.gov/iTable/?reqid=19&step=2&isuri=1&categories=survey&_gl=1*14am8sj*_ga*ODQ5MjY3MDUwLjE3NDA0MTI5NzA.*_ga_J4698JNNFT*czE3NDcwNTY3MDUkbzkkZzEkdDE3NDcwNTcwNTgkajYwJGwwJGgw#eyJhcHBpZCI6MTksInN0ZXBzIjpbMSwyLDMsM10sImRhdGEiOltbImNhdGVnb3JpZXMiLCJTdXJ2ZXkiXSxbIk5JUEFfVGFibGVfTGlzdCIsIjYiXSxbIkZpcnN0X1llYXIiLCIyMDEzIl0sWyJMYXN0X1llYXIiLCIyMDI1Il0sWyJTY2FsZSIsIi05Il0sWyJTZXJpZXMiLCJBIl1dfQ==.

[12]. Ibid.

[13]. United States Census Bureau, USA Trade (US imports for 8541 and 8542 in 2025); OECD, “Global Revenue Statistics Database”; U.S. Bureau of Economic Analysis, National Income and Product Accounts (real GDP for the United States).

[14]. Giovanni Melina and Stefania Villa, “From Servers to Rates: AI, ICT Capital, and the Natural Rate,” International Monetary Fund, October 31, 2025, https://www.imf.org/en/publications/wp/issues/2025/10/31/from-servers-to-rates-ai-ict-capital-and-the-natural-rate-571484.

[15]. United States Census Bureau, USA Trade (US imports for 8541 and 8542 in 2025); OECD, “Global Revenue Statistics Database”; U.S. Bureau of Economic Analysis, National Income and Product Accounts (real GDP for the United States).

[16]. Ibid.

[17]. Rebecca Patterson and Ishaan Thakker, “Will Artificial Intelligence Do More Ham Than Good for U.S. Growth,” Council on Foreign Relations, September 3, 2025, https://www.cfr.org/articles/will-artificial-intelligence-do-more-harm-good-us-growth; “AI Investment Accelerates Across U.S. Tech While Cost Pressures Intensify Broadly; Ratings Impact Mostly Positive,” S&P Global, May 7, 2026, https://www.spglobal.com/ratings/en/regulatory/article/ai-investment-accelerates-across-us-tech-while-cost-pressures-intensify-broadly-ratings-impact-mostly-positive-s101684007.

[18]. Bhargs Srivathsan et al., “AI Power: Expanding Data Center Capacity to Meet Growing Demand” (McKinsey & Company, October 29, 2024), https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/ai-power-expanding-data-center-capacity-to-meet-growing-demand.

[19]. “Powering AI: The Semiconductor Ecosystem at the Foundation of Data Centers,” Semiconductor Industry Association (SIA) and Deloitte, June 2026, https://www.semiconductors.org/powering-ai-the-semiconductor-ecosystem-at-the-foundation-of-data-centers/; Stephen Ezell, Trelysa Long, and Meghan Ostertag, “Short-Circuited: How Semiconductor Tariffs Would Harm the U.S. Economy and Digital Industry Leadership” (ITIF, May 21, 2025), https://itif.org/publications/2025/05/21/short-circuited-how-semiconductor-tariffs-would-harm-the-us-economy/.

[20]. Ibid.

[21]. Ibid.

[22]. Antonio Varas et al., “Government Incentives and US Competitiveness in Semiconductor Manufacturing,” SIA and Boston Consulting Group (BCG), September 2020, https://www.semiconductors.org/turning-the-tide-for-semiconductor-manufacturing-in-the-u-s/.

[23]. Stephen Ezell, “How Innovative Is China in Semiconductors?” (ITIF, August 2024), https://itif.org/publications/2024/08/19/how-innovative-is-china-in-semiconductors/; Hodan Omaar, “How Innovative Is China in AI?” (ITIF, August 2024), https://itif.org/publications/2024/08/26/how-innovative-is-china-in-ai/.

[24]. David Shepardson, “Automakers, retailers warn US memory-chip shortage is impacting prices,” Reuters, June 3, 2026, https://www.reuters.com/business/autos-transportation/automakers-retailers-warn-memory-chip-shortage-impacting-prices-2026-06-03/.

[25]. Semiconductor Industry Association, “Chip Incentives & Investments,” accessed May 29, 2026, https://www.semiconductors.org/chips/.

Editors’ Recommendations

Related

May 21, 2025