Advanced Geothermal Energy Is Widely Available, Clean, and Maybe Cheap Enough to Make a Big Impact

Three advanced geothermal technologies—Enhanced Geothermal Systems (EGS), Advanced Geothermal Systems (AGS), and Superhot Rock Geothermal (SHR)—are poised to transform geothermal from a niche resource into a significant contributor to the U.S. energy mix.

KEY TAKEAWAYS

Key Takeaways

Contents

EGS in Action: Fervo Case Study 11

Government Programs for Geothermal 14

Introduction

The United States faces a growing electricity supply challenge. Data centers, artificial intelligence (AI), manufacturing reshoring, and electrification are driving electricity demand growth not seen in decades, while the retirement of aging baseload plants has left grid operators scrambling for firm, dispatchable power. Coal, nuclear, and, more recently, natural gas have historically filled this role, but coal is increasingly untenable for both environmental and cost reasons, nuclear projects take a decade or more to build, and gas exposes utilities to fuel price volatility. Meanwhile, wind and solar—while increasingly cheap—cannot provide the around-the-clock power that data centers and industrial facilities require. Geothermal energy offers a potential solution—a source of 24/7 baseload power with minimal land footprint and near-zero emissions. This technology has long been limited to a handful of volcanic regions, but could now—thanks to technological breakthroughs borrowed from the oil and gas industry—be on the verge of becoming deployable almost anywhere.

A rare alignment of technological readiness, market demand, and political support makes this moment particularly significant.

This paper examines the potential for accelerated rollout for three advanced geothermal technologies—Enhanced Geothermal Systems (EGS), Advanced Geothermal Systems (AGS), and Superhot Rock Geothermal (SHR)—that are poised to transform geothermal from a niche resource into a significant contributor to the U.S. energy mix. EGS creates artificial reservoirs by fracturing hot dry rock, and has already achieved early commercial rollout: Fervo Energy is constructing a 400 megawatt (MW) project in Utah with power purchase agreements (PPAs) from major utilities, and drilling times have dropped 70 percent in just two years.[1] AGS, using closed-loop systems that eliminate seismic risk, delivered its first commercial power in late 2025. SHR, still in research and development (R&D), promises 5–10 times the energy output per well by tapping supercritical fluids at extreme depths. The Geothermal Technologies Office (GTO) indicates the potential for at least 90 gigawatts (GW) of geothermal electricity-generating capacity by 2050, including in states east of the Mississippi where no geothermal power generation currently exists.[2] Recent flow tests in Utah suggest that these wells can produce commercial-grade heat for many years, and that water losses from circulation are minimal.

A rare alignment of technological readiness, market demand, and political support makes this moment particularly significant. Geothermal enjoys bipartisan backing in Congress and explicit support from the Trump administration, which included it alongside fossil fuels and nuclear in its “energy emergency” declaration (while excluding wind and solar). Tech giants including Google, Meta, Amazon, and Microsoft have signed agreements with geothermal developers for power to feed their data centers. The workforce and equipment needed to scale geothermal already exist in the oil and gas sector. The key question now is how to prove and then scale new geothermal technologies—and what policy levers could accelerate that trajectory.

Box 1: Price/Performance Parity

As countries seek to reduce emissions, they face the need to ensure that, in the long term, zero-emission technologies can reach price-performance parity (P3) with existing energy sources. And because climate change is global, solutions must meet the needs of low-income countries where demand for energy is rising fastest, and where ability and willingness to pay a green premium are low to nonexistent. There is no evidence that forcing change with regulation, subsidies, or exhortation will work. Low-income countries will not adopt clean energy at the expense of growth. Neither will richer countries.

The market is the only lever powerful enough to drive the transition at the scale needed—and it will only work when clean energy technologies can outcompete dirty ones without subsidies or regulations. They must reach P3.

Geothermal has an enormous advantage in that it is both clean and firm—and it doesn’t require backup power for when it fails, as solar and wind do. But it must nonetheless reach P3 for it to become a serious option, especially for developing countries. The very rapid improvement in costs demonstrated by Fervo is therefore immensely encouraging. As costs decline, the United States should be focused on helping Fervo and companies like it scale this technology as fast as possible to drive costs down as quickly as possible, provided that there is a clear pathway to reaching P3. It appears that such a pathway may exist.

Geothermal Modalities

Today, geothermal provides about 3.7 GW of operating geothermal capacity in the United States (16 GW globally), almost all conventional hydrothermal geothermal (HG), which must meet three conditions to be viable:[3]

▪ Heat. Hot rock must be relatively close to the surface.

▪ Fluid. Water or brine must already be present underground.

▪ Permeability. Natural fractures/porosity must allow fluid to circulate effectively.

These conditions occur naturally in volcanic regions marked by hot springs and geothermal vents. Relatively shallow wells can bring hot water, steam, or both to the surface to generate power, without any engineering of the underground reservoir.

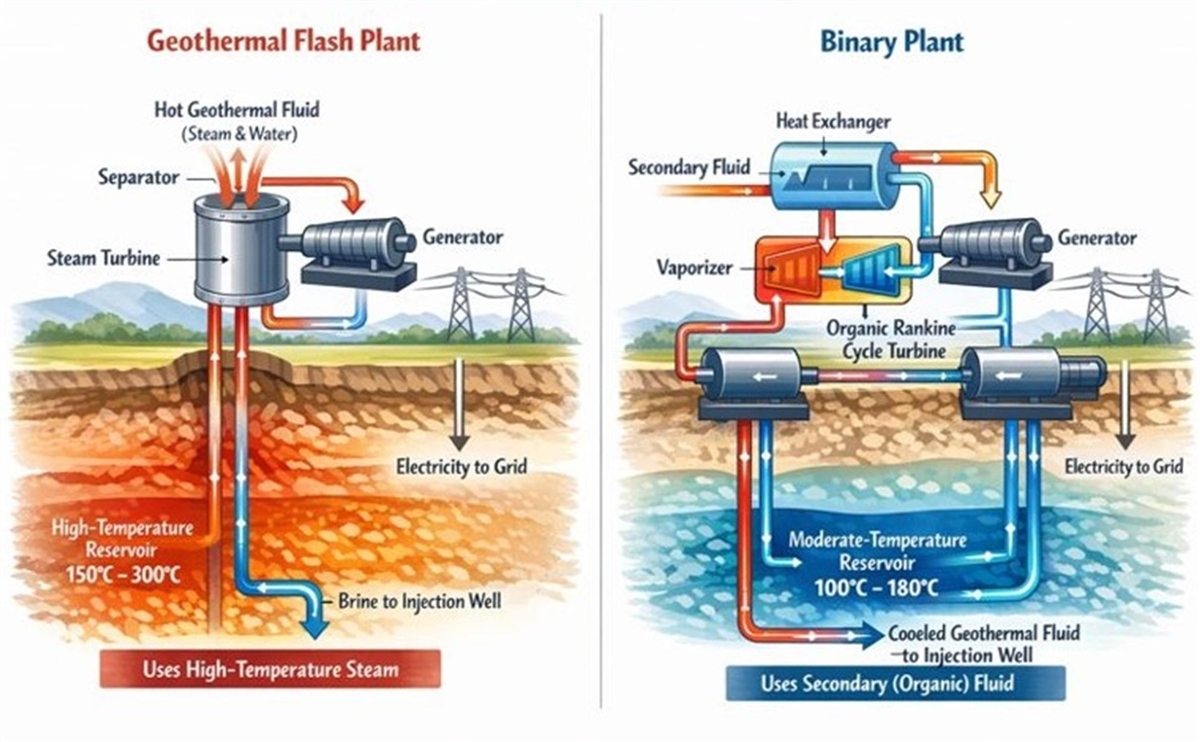

There are two main types of HG plants. (See figure 1.) “Flash plants” are simpler and cheaper, but require hotter resources. They operate with temperatures above 200°C where hot, pressurized water “flashes” to steam when pressure drops at the surface, and that steam drives the turbines directly. “Binary plants” are more expensive but operate at lower temperatures, between 110°C and 200°C. The hot water passes through a heat exchanger and boils a secondary working fluid (with a lower boiling point than water), and that fluid drives the turbine.

Figure 1: Conventional geothermal systems[4]

Both flash and binary plants rely on the convergence of heat, fluid, and permeability, which is difficult to determine beforehand, so wells can come up empty, which is expensive. Wells not finding the necessary hot fluids at working pressures (dry wells) are a frequent outcome.

Three new technological approaches to geothermal offer different solutions to the limited geography, high cost, and significant uncertainty of conventional geothermal.

Enhanced Geothermal Systems

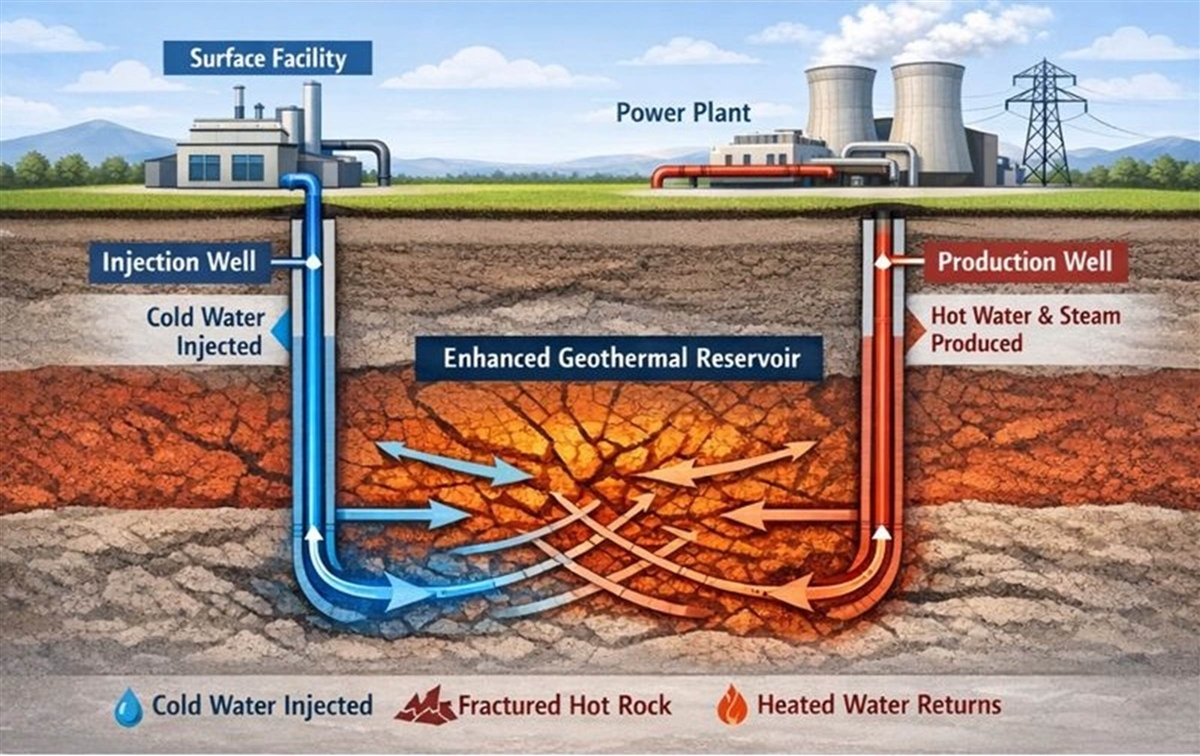

EGS is designed to extract heat from areas that lack natural hydrothermal resources. Reservoirs deep underground are created by injecting fluid into hot, dry rock deep underground to induce fractures. Wells are drilled 3–10 km down into hot, dry, crystalline rock where temperatures are above 150°C and there is limited or no natural permeability. Hydraulic stimulation (hydro-shearing)—a technique from the fracking industry—opens or creates fractures, allowing injected water to circulate through the rock, absorb heat, and return to the surface for power generation (see figure 2).

For EGS to work, operators need a clear understanding of the magnitude and orientation of stresses within a proposed well area. Imagine a cube of rock deep underground. It is being squeezed from all directions but not equally, which creates directional bias in the stress field. The vertical stress is intuitive (at 3 km depth, you have roughly 3 km of rock sitting on top of the cube), but the rock is also being squeezed from the sides, and those side pressures typically differ. These stresses are primarily caused by tectonic forces, but topography and erosion, glacial rebound, local geological structures, and residual stresses “locked in” from ancient tectonic events can all play a part.

Figure 2: Enhanced geothermal systems[5]

Fractures take the path of least resistance. When fluid is injected, it increases pressure; the rock cracks open perpendicular to the minimum stress, because that’s the direction of least resistance. So fractures propagate parallel to the maximum squeeze, and open perpendicular to the minimum squeeze. It’s like when you tear a piece of paper: the tear propagates in one direction (along the line of tear), but it also opens up/widens perpendicular to that line.

Unlike oil/gas fracking, EGS works primarily by reopening and shearing pre-existing fractures in the rock rather than creating entirely new ones. The rock already has natural fracture networks—the fluid pressure causes these fractures to slip slightly (shear), which permanently increases their aperture (width) and permeability.

EGS has already begun the transition from R&D to active deployment. Horizontal drilling and hydraulic stimulation techniques from the shale oil/gas industry have been transformative, dramatically reducing costs and drilling times. Fervo achieved a 70 percent year-over-year reduction in drilling times between its pilot (Project Red in Nevada) and its production wells at Cape Station in Utah while simultaneously reaching reservoir temperatures exceeding 220°C. Since drilling has historically totaled more than 50 percent of geothermal capital costs, that reduction transforms project economics. EGS is now considered bankable, with major utility PPAs signed and construction financing secured from mainstream energy investors. (See Fervo case study.)

Advanced Geothermal Systems

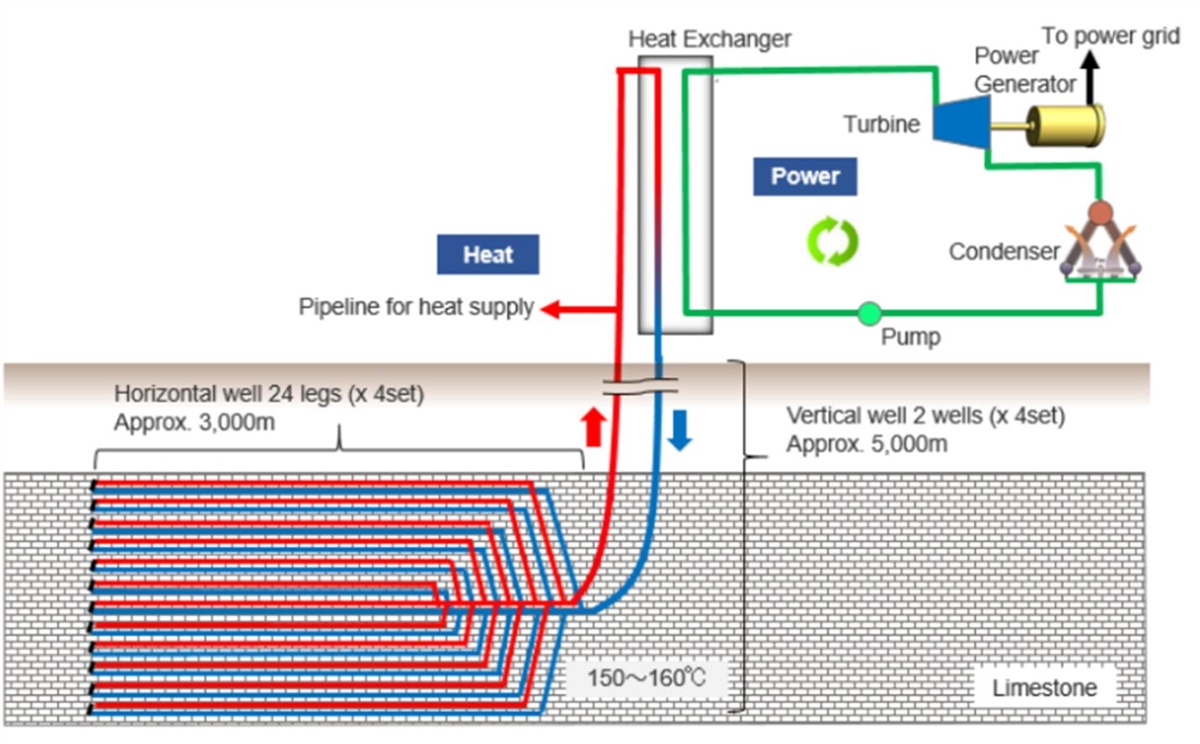

AGS are closed-loop systems that circulate fluid through sealed wellbores and horizontal pipes. These systems operate at depths of 2–7 km and at temperatures above 100°C, but unlike EGS, they require no natural permeability or EGS-type stimulation because fluid remains sealed within closed-loop pipes. Heat is transferred conductively from the rock through the wellbore wall. That eliminates seismicity risk, but also limits power output compared with EGS.

There are two main wellbore configurations for AGS:

▪ Coaxial (pipe-in-pipe) systems operate with a single borehole. An inner pipe sits inside an outer pipe, cold fluid travels down through the space between the pipes and absorbs heat from the surrounding rocks. Hot fluid returns up through the inner pipe, which is insulated to prevent losing heat back to the cooler shallow rock on the way up. This offers a simple design, but it offers only a limited surface area for conduction and hence limited heat recovery.

▪ U-loop systems (such as Eavor’s) use two vertical wells connected at depth by one or more laterals. Cold fluid goes down one vertical well, travels through the hot horizontal section(s), and returns up the other vertical well. The horizontal laterals provide most of the heat absorption, and multiple laterals can be drilled to increase the system’s total length of contact with hot rocks. Eavor’s Geretsried project in Germany uses multiple laterals radiating from the vertical wells to maximize heat capture.

Figure 3: AGS systems[6]

Because AGS conducts heat transfer through the pipe wall, three factors constrain the amount of heat that can be extracted:

▪ Surface area. Heat is only captured wherever pipe contacts rock. Even with long horizontal laterals, AGS provides far less surface area than a fractured EGS reservoir does.

▪ Thermal conductivity of rock. Rock is not a great conductor. Heat from rock further away from the pipe takes time to conduct inward. As heat is extracted, the rock immediately around the pipe cools, and further use must wait for the area to become hot again as heat is conducted in from further away.

▪ Flow rate trade-off. When fluid is pumped too quickly, it doesn’t have time to absorb heat; pumped too slowly, and it doesn’t generate enough power. An optimal flow rate is constrained by local conductive limits.

One clever feature of U-loop AGS (and Eavor’s innovation) is the thermosiphon effect: natural circulation without pumps. Because hot fluid is less dense than cold fluid, in the U-loop system, the hot column of fluid in the “up” leg is lighter than the cold column in the “down” leg, creating natural circulation which means reduced use of pumping power.

AGS produces less power per well than EGS does because it is fundamentally limited by the speed with which heat can conduct through rock and steel, rather than directly mining heat from water flowing through fractures. AGS offers lower power output in exchange for no seismicity risk and no water losses. In practice, therefore, AGS is better suited for district heating than it is for power generation.

AGS reached a major inflection point in late 2025 when Eavor moved from demonstration to first commercial power delivery, becoming the first company to deliver electricity to a commercial power grid using a fully closed-loop geothermal system. Eavor’s Geretsried (Bavaria, Germany) project will ultimately deliver 8.2 MW of electricity and 64 MW of district heating.[7] Eavor’s pilot demonstration facility in Alberta, Canada, has been in continuous operation since 2019, providing five years of operational data that validated the closed-loop concept before construction of the Geretsried plant, which is notably more efficient.[8] Eavor’s October 2025 white paper documents a 50 percent reduction in drilling time per lateral and a 3x improvement in bit run lengths at Geretsried.[9]

Overall, AGS appears best suited for applications such as European district heating, where heat (not electricity) is the main product, feed-in tariffs and clean tech subsidies support higher costs, and competing sources of power are either more expensive or not clean enough to meet EU standards.

Superhot Rock Geothermal

The third technology is SHR, which aims to tap geothermal resources at extreme depths where temperatures exceed 400°C and pressures exceed 22 megapascals (Mpa). That causes water to reach a “supercritical” state in which it no longer behaves as a distinct liquid or gas and instead takes on some unique properties:

▪ Much lower viscosity than liquid water—flows more easily through fractures

▪ Higher enthalpy (energy content)—carries far more thermal energy per kilogram (kg)

▪ Different density behavior—intermediate between liquid and steam

These characteristics mean that SHR offers 5–10 times the energy density per well of conventional geothermal. However, supercritical conditions typically require drill depths of 5–20 km (compared with 3–7 km for EGS). The deeper the well, the more the temperature increases (normally ~25–30°C per km of depth, higher in volcanic areas) and the pressure increases (normally ~10 MPa per km of depth from hydrostatic pressure).[10],[11] In some favorable geologies (volcanic regions such as Iceland), supercritical conditions can be found at 4–5 km, but in typical continental crusts, wells might need to reach 10–20 km—depths that push the limits of current drilling technology.

Higher energy density is very attractive, but SHR is still in its R&D phase because drilling that deep underground takes an enormous and expensive toll on equipment. Conventional drill bits, casings, cement, and electronics are rated for ~200–250°C. At 400°C or more, steel loses strength, elastomers fail, electronics fry, and casings undergo severe thermal expansion/contraction cycles that cause joints to fail. Supercritical water is also highly corrosive: dissolved minerals become more aggressive at high temperatures, and silica scaling and acid attack accelerate dramatically.[12]

Rock itself behaves differently at these temperatures as well. At temperatures above ~350–400°C, rock becomes “ductile”—it deforms plastically rather than fracturing brittlely which makes hydraulic fracturing less effective (rock squeezes closed rather than cracking open).

So far, the economics of drilling that deep have made SHR financially unfeasible, largely because drilling costs increase exponentially with heat and depth. Conventional rotary drilling is impractical, so new nonmechanical drilling technologies such as millimeter wave/gyrotron drilling from Quaise will be important for SHR.

Box 2: Quaise

Quaise is attempting to drill far deeper than currently possible—up to 20 km. The system uses a gyrotron—a vacuum tube device originally developed for nuclear fusion research that generates high-frequency electromagnetic radiation (millimeter waves, which sit between microwaves and infrared on the spectrum).[13] The gyrotron beams at a target rock via a waveguide, a hollow metal tube that directs the energy to the right spot. When the rig is drilling, the tip of the waveguide is positioned a foot or so away from the rock. The gyrotron lets out a burst of millimeter waves for about a minute. The rock heats up, cracks, melts, or vaporizes. Then a mechanical scraper removes debris, and pressurized gas flushes it to the surface. The process repeats.

A primary technological challenge is to avoid accidentally making plasma, an ionized, superheated state of matter, as doing so wastes energy and damages key equipment such as the waveguide. It is also more difficult to keep the beam focused as depth increases. Current tests use a 100 kilowatt (kW) gyrotron, producing four-inch-diameter holes. The next step is a 1 MW system that will drill commercial-scale larger holes over eight inches across. Quaise achieved record depths of 100+ meters in 2025, and hopes to hit 1 km in 2026. Commercial SHR will require depths of 10–20 km.[14]

SHR remains in the R&D and demonstration phase with no commercial projects currently operating. The technology’s extraordinary potential is offset by formidable technical challenges. The Iceland Deep Drilling Project’s second well reached 4,659 meters and 427°C, but the casing failed during recovery and the production portion remains inaccessible.[15] In October 2025, Iceland’s government signed a cooperation declaration for a third well with Reykjavik Energy, Landsvirkjun, and HS Orka. IDDP-3 targets temperatures of up to 400°C at a depth of 4–5 km.[16]

Table 1: Advanced geothermal technologies

|

Parameter |

EGS (Enhanced) |

AGS (Advanced) |

SHR (Superhot Rock) |

|

Depth |

3–10 km (typically 3–7 km) |

2–7 km |

5–20 km (typically 7–10 km) |

|

Temperature |

> 150°C (commonly 150–300°C) |

> 100°C (typically 100–250°C) |

> 400°C (supercritical) |

|

Pressure |

Not a primary requirement |

Not a primary requirement |

> 22 MPa (for supercritical water) |

|

Rock Type |

Hot, dry crystalline rock (granite, basement) |

Any hot rock |

Hot, dry crystalline basement rock |

|

Natural Permeability |

Low or absent (must be created) |

Not required |

Low or absent (engineered) |

|

Stimulation Required |

Yes—hydraulic stimulation (hydro-shearing) |

No |

Yes—hydraulic or thermal stimulation |

|

Heat Transfer |

Convection (fluid contacts rock) |

Conduction only (fluid in sealed pipes) |

Convection (supercritical fluid) |

|

Working Fluid |

Water (injected/circulated) |

Water or carbon dioxide (CO₂) (closed loop) |

Supercritical water or CO₂ |

|

Configuration |

Injection + production wells with fracture network |

Sealed U-loop or coaxial wellbores |

Deep injection + production wells |

|

Power Output |

Standard geothermal output |

Lower; best suited to district heating |

5–10× conventional per well |

|

Key Challenge |

Induced seismicity risk; fracture control |

Drilling costs; slow heat transfer |

Extreme drilling conditions; materials |

EGS in Action: Fervo Case Study

Houston-based Fervo Energy is now producing energy from EGS at commercial scale. It has slashed drilling costs by nearly half and cut completion times by 70 percent in six months, positioning the company to deliver the world’s largest EGS project while transforming the economics of the industry.[17] This suggests that next-generation geothermal power will be positioned to compete economically with conventional energy sources far sooner than government projections indicate.

EGS companies orient their horizontal wells specifically to intersect fractures, but Fervo’s horizontal well design is unique. Instead of two vertical wells connected where fractures occur at different depths, experiencing varying stress fields and temperatures, Fervo’s horizontal well design results in geothermal systems wherein injection and production wells are connected under the surface by a set of fractures where all fractures exist in the same stress field and temperature zone.

Figure 4: Fervo’s well design

Think of Fervo’s system as building a ladder underground—two parallel rails connected by rungs (fractures). These fractures act as flow pathways between two wells: the insertion well (through which fluid is pumped into the rock) and the production well (where the heated fluid is recovered and used to drive turbines). The combination of stress analysis, directional drilling, staged stimulation of the fractures, and real-time microseismic monitoring has made EGS reservoir creation remarkably repeatable—which is why Fervo can now drill multiple wells at Cape Station with confidence that they’ll connect. The setup works like this:

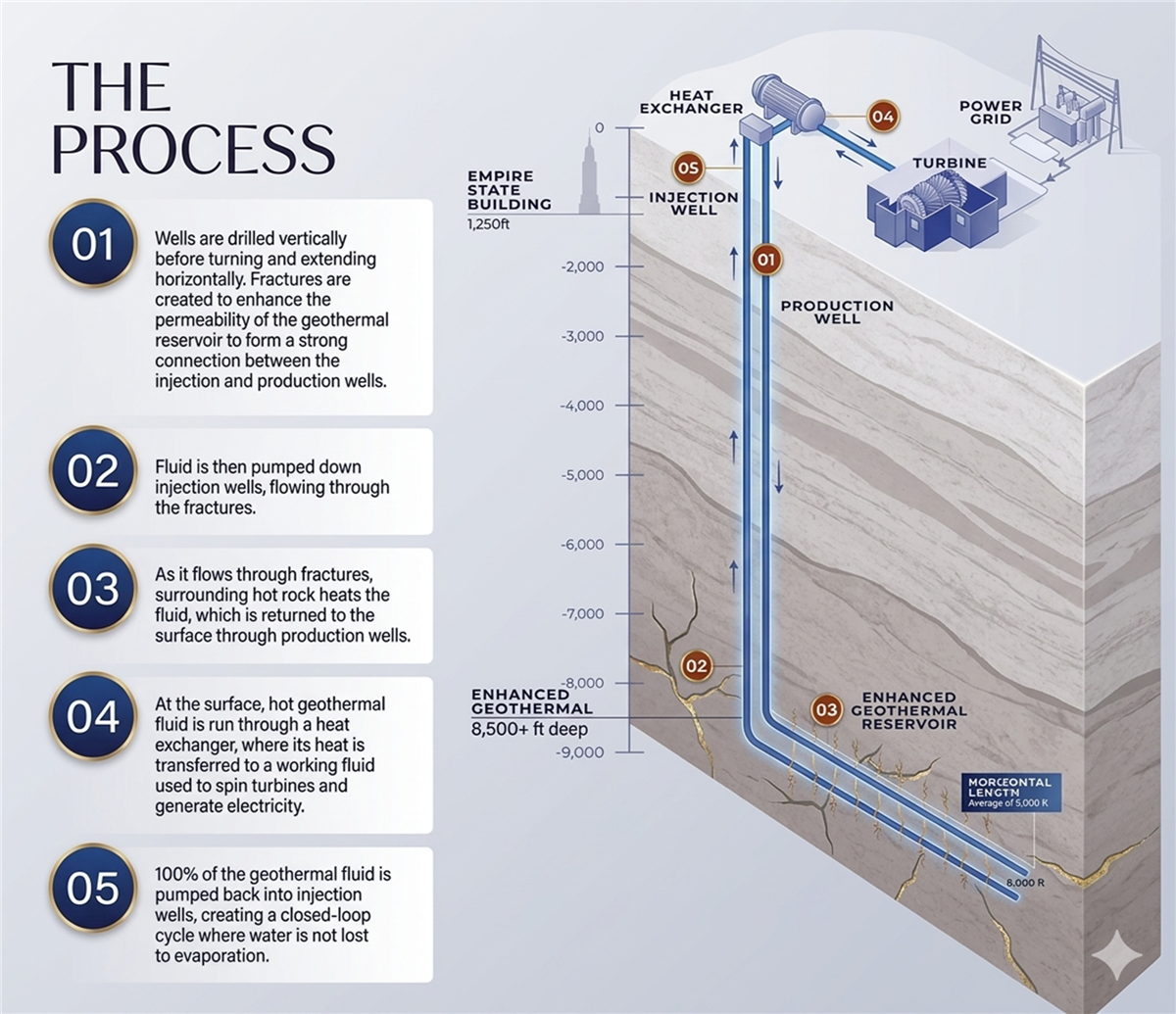

1. Drill the first well. Drill vertically, then curve the well top to become horizontal. The horizontal section will run perpendicular to the natural fracture direction of the rock. If fractures in that geology tend to run east-west, the horizontal section is drilled north-south. This ensures that fractures will cross the wellbore rather than run alongside it.

2. Stimulate the first well using hydraulic pressure. As fractures form, they produce tiny seismic signals. Distributed acoustic sensing installed in the well will detect these micro-earthquakes in real time, creating a 3D map of where fractures are actually forming.

3. Drill the second vertical well into the new fracture zone parallel to the first. Typically, well 2 is drilled a few hundred feet away from well 1—close enough for fractures to connect the wells, but far enough for water to absorb sufficient heat as it travels between them.

4. Connect the ladder. Using plug-and-perf techniques from shale drilling, isolate short sections of each horizontal wellbore and stimulate them one at a time. Doing so creates dozens of controlled fracture pathways connecting the two wells. At Cape Station, Fervo created 100+ fracture flow paths along the paired wells.

5. Confirm and operate. Run flow tests and chemical tracers to verify that the wells are connected through the fractures. Then operate: pump cold water down the injection well, let it flow through the hot fractured rock, and collect it (now heated to ~400°F) from the production well.

Fervo’s drilling costs at Cape Station in Utah have fallen from $9.4 million to $4.8 million per well across the first four horizontal wells, and the company’s goal is to drive its costs down below $3 million per well, to put geothermal on par with North American oil and gas.[18] The company drilled its fastest well in just 21 days—a 70 percent reduction from its first horizontal well drilled in Nevada in 2022. Polycrystalline diamond compact (PDC) drill bits adapted from shale operations have driven these improvements, providing sustained penetration rates averaging 70 feet per hour.[19]

These cost reductions exceed Department of Energy (DOE) expectations. Fervo has achieved a 35 percent learning curve across all projects, nearly double its planned 18 percent target.[20] The company’s penetration rates already comfortably surpass the National Renewable Energy Laboratory’s (NREL’s) 2035 projections for the “most likely scenario” of 50 feet per hour.[21] Fervo’s distributed fiber optic sensing enables real-time monitoring of temperature, flow, and performance, which optimizes reservoir performance and maximizes heat mining efficiency.[22]

In 2024, a 30-day well test at Fervo’s Cape Station project generated over 10 MW of electricity—tripling the output of Fervo’s first commercial pilot at Project Red in Nevada—and recorded peak flow rates of 107 kilograms per second of (kg/s) high-temperature water—comfortably enough to reach commercial production.[23] Fervo has also confirmed zero thermal decline through 12 months of data at Project Red, validating the long-term sustainability of its systems.[24]

Fervo’s technology builds on techniques the management team developed in the oil and gas industry. Devon Energy, a shale pioneer, led Fervo’s $244 million Series D funding round in February 2024. “Fervo’s approach to geothermal development leverages leading-edge subsurface, drilling, and completions expertise and techniques Devon has been honing for decades,” said David Harris, Devon’s chief corporate development officer. [25]

Cape Station in Utah is the world’s largest enhanced geothermal development. Fervo expanded the project from 400 MW to 500 MW based on drilling performance improvements. Phase I will deliver 100 MW beginning in 2026, with full 500 MW capacity operational by 2028.[26] Fervo estimates that Cape Station will generate 6,600 construction jobs and $437 million in local wages, along with 160 full-time operational jobs.[27]

Cape Station is less than a mile from DOE’s Frontier Observatory for Research in Geothermal Energy (FORGE), which helps Fervo leverage the extensive geological data and research findings that FORGE has made publicly available.[28] Bureau of Land Management (BLM) permits will allow Cape Station to expand to 2 GW, and overall, Fervo controls over 16 GW of geothermal leases under direct management. Those leases would be the next stage in commercial development once customer interest converts to contracts.[29] Overall, Fervo claims access to more than 40 GW of EGS across 10 sites, and that its Cape Station wells alone have a potential capacity of 4.3 GW—more than all geothermal currently installed in the United States.[30]

Fervo’s next project at Corsac Station in Nevada will deliver 115 MW of geothermal power and is attracting interest from data center operators seeking firm, clean electricity. The company plans to expand Corsac based on customer demand.[31]

Critically, Fervo has contracted the entire 500 MW capacity of Cape Station through multiple PPAs. Southern California Edison signed two 15-year contracts totaling 320 MW—the world’s largest geothermal PPA.[32] The deals will provide carbon-free electricity sufficient to power 350,000 homes.

Fervo claims that current CAPEX costs are $7,000/kWe. It expects that to fall quickly to $3,000/kWe. That is not far from existing fossil fuel overnight costs. In short, it is a potential energy revolution.

This rapid take-up is partly driven by regulatory mandates. California’s Public Utilities Commission mandated in 2021 that utilities procure 1,000 MW of non-weather-dependent, nonbattery, zero-emission energy to boost grid reliability. The mandate catalyzed demand for geothermal power despite historically higher costs compared with wind and solar.[33]

Fervo has also attracted other customers. Google and NV Energy (a Nevada utility) have structured an innovative Clean Transition Tariff to bring 115 MW of Fervo’s geothermal power to Google’s Nevada data centers.[34] The Nevada Public Utilities Commission approved the first-of-its-kind rate structure in May 2025.[35] Under the tariff, Google pays the difference between geothermal energy costs and lower-cost resources such as solar and natural gas. NV Energy purchases electricity from Fervo’s Corsac Station project and delivers it to Google, which receives credits for energy and capacity on its electric bills. The arrangement enables Google to access firm, clean power without passing costs to other ratepayers.[36]

Additional agreements include 31 MW with Shell Energy for retail customers, and Fervo’s partnership with Google which began in 2021 as the world’s first corporate agreement for next-generation geothermal power.[37] Project Red now delivers 3.5 megawatts to the grid serving Google’s data centers.[38]

On the supply side, Fervo recently announced a long-term supply agreement with Vallourec to scale domestic geothermal infrastructure. Vallourec provides tubing for Fervo’s wells. The deal is worth up to $800 million to Vallourec over 5 years. According to Fervo, “The collaboration directly supports Fervo’s strategy to deploy repeatable GeoBlocks—standardized 50 MW units of geothermal energy.”[39] And Fervo is planning for scaleup: It is focused on driving down the cost of delivering completed 50 MW units.[40]

Because EGS is new and its capabilities are only now being explored, there are no good estimates for the total geothermal capability in the United States, or its distribution. Fervo claims that there are few geographical constraints in deploying its technology, but EGS opportunities east of the Mississippi are especially poorly understood, which is why DOE is seeking to fund an EGS project in the Eastern United States.

Fervo claims that current CAPEX costs are $5,000 per kilowatt-electric (kWe). It expects that to fall quickly to $3,000/kWe.[41] That is not far from existing fossil fuel overnight costs. In short, this is potentially an energy revolution.[42]

Government Programs for Geothermal

Geothermal and nuclear are the Trump administration’s two favored “clean” energy sources. Both were explicitly included in Trump’s Day One “energy emergency” declaration alongside fossil fuels, while wind and solar were excluded. Geothermal is favored perhaps in part because of its overlap with oil and gas technology and workforce. Energy Secretary Chris Wright, formerly CEO of a fracking company that has invested in Fervo Energy, has championed geothermal.[43]

Over the past 15 years, DOE has helped catalyze the emergence of EGS as a viable energy pathway, using three main vehicles to do so: GTO for early-to-mid-stage R&D; the Loan Programs Office (now known as the Office of Energy Dominance Financing (EDF) for large-scale commercialization; and the Advanced Research Projects Agency-Energy (ARPA-E) for high-risk, high-reward technological disruptions. GTO has been merged into the Office of Fossil Energy and Carbon Management (FECM) to create a new Hydrocarbons and Geothermal Office (HGO), where the Office of Geothermal (OG) is a component. Table 2 lists geothermal projects at DOE.

The Bipartisan Infrastructure Law (BIL) and the Inflation Reduction Act (IRA) provided a massive infusion of capital, specifically targeting EGS pilot demonstrations along with the use of geothermal power for critical minerals such as lithium.

Table 2: DOE geothermal projects, 2010–2025

|

Project |

DOE Funding Source |

$M |

Technology |

Size (MW) |

State |

Status |

|

Project ATLiS |

EDF (ATVM) |

1,360 |

Direct Lithium Extraction (DLE) |

N/A |

CA |

Conditional Commitment |

|

Ormat Nevada Portfolio |

EDF (Title XVII) |

350 |

Hydrothermal |

100 |

NV |

Operational |

|

Utah FORGE |

GTO (EERE) |

218 |

EGS |

N/A |

UT |

Successful Reservoir Creation |

|

Blue Mountain |

EDF (Title XVII) |

99 |

Hydrothermal |

50 |

NV |

Operational |

|

USG Oregon |

EDF (Title XVII) |

97 |

Hydrothermal |

22 |

OR |

Operational |

|

Project Red |

GTO (EERE) |

25 |

EGS |

4 |

NV |

Operational |

|

Cape Station Phase I |

GTO (BIL) |

25 |

EGS |

100 |

UT |

Under Construction |

|

Chevron New Energies Pilot |

GTO (BIL) |

20 |

EGS Refurbishment |

N/A |

CA |

Active |

|

Mazama Superhot |

GTO (BIL) |

20 |

Superhot EGS |

N/A |

OR |

Active |

|

Gradient Blackburn |

GTO (WOO) |

2.5 |

Co-production |

1 |

NV |

Pilot Active |

|

Geothermix Austin Chalk |

GTO (WOO) |

2.5 |

Thermoelectric |

N/A |

TX |

Demo Active |

|

ICE Thermal Harvest |

GTO (WOO) |

1.7 |

Waste Heat Recovery |

N/A |

CA |

Active |

|

UT Oklahoma Sedimentary |

GTO (WOO) |

1.7 |

Hydrocarbon Repurposing |

1 |

OK |

Active |

|

Penn State TACS |

ARPA-E (OPEN) |

1.5 |

TACS (Thermal Screens) |

N/A |

PA |

Selected |

|

Ann Arbor GHP |

GTO (EERE) |

0.6 |

GHP (Geothermal Heat Pump) |

N/A |

MI |

Design Phase |

R&D programs Within DOE’s Office of Geothermal (OG)

OG has managed the bulk of the federal geothermal portfolio, structured around five core sub-programs: exploration and characterization; subsurface accessibility; resource maximization; subsurface enhancement and sustainability; and data, modeling, and analysis.[44]

The centerpiece of OG’s efforts is FORGE. Located in Milford, Utah, it is a dedicated field laboratory in which scientists and engineers develop and test EGS technologies in a controlled environment (see box 3).

OG has also supported projects to reduce drilling costs through the “Efficient Drilling for Geothermal Energy” (EDGE) and “Geothermal Drilling Technology Demonstration” programs, focused on the use of PDC drill bits. The Wells of Opportunity (WOO) program supports repurposing idle or marginal oil and gas wells for geothermal production, demonstrating a path for coproduction and industry transition.[45]

DOE also funds the Geothermal Energy from Oil and Gas Demonstrated Engineering Consortium (GEODE) initiative designed to leverage the expertise, technology, and workforce of the oil and gas industry. Led by Project InnerSpace and the Society of Petroleum Engineers, this five-year, $165 million initiative aims to transfer oil and gas drilling and subsurface engineering capabilities to the geothermal sector.[46]

Finally, it’s worth noting that the United States is a leader in advanced geothermal. Rapid scale-up could lead to substantial opportunities elsewhere, bringing U.S. capabilities to partner with local companies and countries.

Box 3: FORGE: A Model R&D Program

FORGE is the federal government’s most ambitious effort to transform EGS from experimental technology to commercial reality.

Origins. The initiative began in 2014 when DOE started exploring how oil and gas drilling advances could unlock geothermal energy in regions lacking natural hydrothermal resources.[47] DOE selected Milford, Utah, in 2018 as the final site for full-scale operations.[48] The University of Utah’s Energy and Geoscience Institute manages the facility, which spans 15 square miles of fractured granite approximately 175 miles southwest of Salt Lake City.[49]

Funding. DOE has committed $298 million to FORGE operations since inception. The initial budget of $218 million, announced in 2018, supported the project through mid-2024.[50] In October 2024, FORGE received an additional $80 million through 2028, reflecting confidence in the program’s progress.[51]

Beyond core operating funds, DOE awarded competitive research grants in geothermal totaling $90 million between 2020 and 2023. In 2021, 17 projects developing technologies such as zonal isolation devices, high-temperature sensors, and advanced drilling systems received $46 million, while a further $44 million was awarded in 2023 focused on reproducible solutions and data dissemination.[52]

Model. FORGE operates as an open-access research facility in which industry, academia, and National Labs test equipment and refine techniques for creating engineered geothermal reservoirs. The site targets extreme conditions—temperatures exceeding 200°C (392°F) and depths reaching 8,559 feet of true vertical depth.[53] FORGE has a dual mission: build field-scale testing infrastructure while enabling external partners to develop novel technologies, and offer a sophisticated testbed for downhole technologies via distributed acoustic sensing (DAS), distributed temperature sensing (DTS), and microseismic arrays that deliver fracture propagation diagnostics with approximately one-meter spatial resolution.[54] As one industry expert noted, “Who else offers you an 8,000-foot hole to put your tool down?”[55]

Critically, and somewhat unusually for DOE, all data collected at FORGE becomes publicly available through FORGE’s Geothermal Data Repository and an online Wiki dashboard, accelerating industry-wide learning.[56] This open-source approach allows companies to bypass costly exploratory research and directly apply proven techniques. FORGE operates with just eight full-time equivalent staff.[57]

Impacts. FORGE has delivered dramatic improvements in drilling performance that address key barriers to commercial deployment. The facility has pioneered horizontal drilling techniques for geothermal wells, adapting methods from shale gas production. Between October 2020 and February 2021, FORGE drilled its first injection well 62 days ahead of schedule—completing it in 74 days rather than the planned 136 days.[58]

DOE reports that FORGE has achieved a sevenfold decrease in on-bottom drilling time, from 440 hours to 60 hours at equivalent depths of 6,000 feet.[59] By 2022, average drilling rates exceeded 71 feet per hour in crystalline granite—a remarkable improvement—and drilling speeds increased fivefold between 2017 and 2022, driving cost reductions of up to 50 percent.[60]

In May 2024, FORGE achieved a critical milestone with successful commercial-scale stimulation connecting injection and production wells.[61] The circulation tests, conducted in April and continued through September 2024, demonstrated sustained flow with more than two-thirds of injected water returning from the production well.[62] The production rate exceeded 20 liters per second at injection depths of 2–3 km, with temperatures maintained at approximately 370°F (188°C).[63] Dr. John McLennan, co-principal investigator at FORGE, called the successful nine-hour circulation test “a Eureka moment” that validated 60 years of EGS research.[64]

Seismic management represents another significant achievement. FORGE has implemented a “traffic-light” protocol wherein operations pause whenever an earthquake that exceeds magnitude 2.0 is caused. During stimulation tests that generated thousands of micro-seismic events, the largest measured just magnitude 1.9—well below levels that cause felt seismicity.[65] Most events ranged between magnitude -2.0 and 0.6, demonstrating that EGS reservoirs can be created without problematic seismic activity.[66]

Private developers have rapidly adopted FORGE innovations. Fervo applied FORGE techniques at its Nevada and Utah projects, achieving flow rates exceeding 95 kg/s—more than triple the previous EGS record of 30 kg/s set at Soultz, France, after 50 years of global effort.[67]

A model for public-private R&D initiatives. FORGE’s open research model and testing environment have lowered barriers to entry for geothermal start-ups while advancing technologies that established players such as Ormat Technologies can also utilize.[68] By providing open-access infrastructure and sharing all research findings publicly, FORGE has accelerated private sector innovation while ensuring that taxpayer investments benefit the entire industry rather than just individual companies. This approach may provide a blueprint for advancing other clean energy technologies from laboratory concepts to commercial deployment.

Precommercial Pilot Projects

In February 2024, DOE announced the first round of EGS pilot demonstration projects funded under the Infrastructure Investment and Jobs Act (IIJA), providing up to $60 million across diverse geographic locations and geologic formations. The IIJA provides for four specific topic areas. Projects in the first three topics are under way; the fourth is expected to be awarded shortly:[69]

1. EGS Proximal. Increase power production in the near term by targeting areas near existing geothermal fields. Awarded to Chevron in Sonoma County, California.

2. Green field. Regions where subsurface heat is present, but no geothermal energy production currently exists. Awarded to Fervo, for three 8 megawatt-electric wells in Utah.

3. SHR EGS. Deep EGS at existing geothermal sites. Awarded to Mazama Energy to demonstrate super-hot EGS (temperatures exceeding 375°C) on the western flank of the Newberry Volcano in Oregon. Completed.

4. Eastern U.S. EGS. Demonstrates EGS specifically in the Eastern United States. Funding opportunity announcement issued July 2024.[70]

These commitments are important, as they demonstrate that GTO may have the capacity to fill the gap left by the elimination of Organization for Economic Cooperation and Development (OCED) funding, providing critical funds for the precommercial demonstration of new technologies. It remains to be seen whether the new OG remains committed to projects such as these.

The Loan Programs Office and ARPA-E

While GTO handles the technical foundation, EDF has focused on the “commercial liftoff” of mature technologies. EDF’s Title XVII program provided critical debt financing and loan guarantees for some of the largest geothermal plants in the country, including the Blue Mountain and Ormat Nevada portfolios, until 2025, when EDF’s focus shifted toward the Advanced Technology Vehicles Manufacturing (ATVM) program to support projects that integrate geothermal power with lithium extraction, such as $1.3 billion loan for Project ATLiS in the Salton Sea in California (see box 4 on Project AtlIs).[71]

Simultaneously, ARPA-E has explored the “superhot” frontier. DOE’s SUPERHOT (Stimulate Utilization of Plentiful Energy in Rocks through High-temperature Original Technologies) program aims to unlock geothermal production from reservoirs at temperatures exceeding 375°C and pressures greater than 22 Mpa. These superhot resources could provide 10–20 GW of energy at a competitive cost. ARPA-E’s Vision OPEN 2024 and IGNIITE 2025 programs have further funded disruptive concepts, such as thermally activated cellular screens and bio-based recovery of rare earth elements from geothermal brines.[72]

Box 4: Project AtLis—Transforming Geothermal Economics?

Geothermal exploration led to the discovery of significant lithium concentrations in the brines of the Salton Sea Known Geothermal Resource Area (KGRA). DOE has estimated that the Salton Sea in Southern California could contain over $4 million metric tons of lithium, enough to produce 10,000 gigawatt-hours of battery capacity.[73]

Project ATLiS is a joint venture between BHE Renewables and Oxy (TerraLithium) using DLE technology, which offers a 95–97 percent lithium recovery rate. DLE may therefore transform geothermal plants from simple electricity generators into critical mineral refineries, fundamentally altering the economics of the sector and aligning it with the national priority of onshoring the battery supply chain.[74] Project ATLiS has an offtake agreement with Ford to deliver ~20,000 tons of lithium annually, quadrupling U.S. domestic supply.[75] Of course, the Salton Sea location taps an existing an hydrothermal plant and a unique geography, but the concept of developing multiple revenue streams from geothermal is encouraging.

Workforce Development and Cross-Industry Spillovers

Certain clean energy construction—such as nuclear—faces significant workforce challenges, as scale-up will require advanced training for tens of thousands of workers. In contrast, geothermal uses technologies originally developed for oil and gas, so workers can shift into geothermal with minimal additional training.

As a result, federal dollars for training drillers, developing drilling technology, and building oilfield supply chains represent fungible infrastructure that can be applied to geothermal; the same rigs drill for oil or gas and for geothermal energy, and the same workers operate them. Major oil companies are already pivoting. Chevron, for example, has a DOE-funded EGS pilot in Sonoma County, California. When the Trump administration supports “energy dominance” through fossil fuel development, it is also sustaining the workforce, equipment base, and R&D ecosystem that geothermal will inherit. Major drilling services companies (e.g., Nabors, Halliburton, SLB) are actively investing in geothermal ventures precisely because they see the transferability.[76] In effect, oil and gas support today can become geothermal workforce development and technology incubation for tomorrow. The International Energy Agency (IEA) estimates that around two-thirds of the technical skills and equipment used in conventional geothermal overlaps with oil and gas; for next-generation geothermal, that overlap is more than 75 percent.[77] Fervo’s success is this transfer in action.

Congressional Activity and the Administration Budget Request

Support for geothermal is growing in Congress. The Geothermal Energy Opportunity Act (GEO Act) requires the Department of the Interior to process each application for a geothermal drilling permit or other authorization under a valid existing geothermal lease within 60 days after completing all requirements under applicable federal laws and regulations (including the National Environmental Policy Act of 1969 (NEPA), the Endangered Species Act of 1973, and the National Historic Preservation Act) unless a U.S. federal court vacates or provides injunctive relief for the underlying lease.[78]

The Geothermal Tax Parity Act would allow geothermal projects to qualify for the same passive loss treatment long available to oil and gas investments, enabling investors to deduct project losses against other income. The bill would also extend existing tax treatment for geological and geophysical exploration costs to geothermal development, reducing upfront risk and encouraging private sector investment.[79]

The House Natural Resources Subcommittee on Energy and Mineral Resources held a hearing on December 16, 2025, reviewing several geothermal bills to expedite development, but no votes are currently scheduled.

The administration’s FY 2026 budget request provides useful insights into ongoing OG priorities for geothermal. It prioritizes Early Career Awards in STEM (science, technology, engineering, and math) but calls for fewer EGS Greenfield Demonstrations, and defers funding for a potential future extension of the FORGE project until FY 2027, anticipating that long-term circulation tests at the site will be completed to provide clarity on the scientific value of future operations at FORGE to EGS commercialization. It also prioritizes the GEODE project (connecting geothermal with oil and gas expertise), R&D to increase sustainability and reduce costs associated with well construction, and subsurface accessibility aspects of EGS Greenfield Demonstrations.[80]

Key Challenges

EGS is already entering a period of rapid technological change and growth. Demand is growing, but the pathway remains uncertain. To fully support rapid development and deployment, DOE’s geothermal program must address significant challenges:

R&D

Beyond FORGE, federal R&D funding for geothermal is under significant pressure. The regular annual appropriation for (now Office of Geothermal [OG]) increased from $125 million to $150 million for FY 2026.[81] Meanwhile, ARPA-E, which has funded potentially important early stage technologies such as microwave drilling, saw its budget cut by roughly 24 percent, from $460 million to approximately $350 million.[82] OG has announced $171.5 million for next-generation geothermal field tests in February 2026, but alignment between ARPA-E and OG remains unclear, and the pathway for technologies after ARPA-E funding is uncertain.[83]

The elimination of OCED funding compounds this problem. OCED funding for early commercial deployment of new technologies has in theory shifted to line offices such as OG. However, OCED’s funding originated through the IIJA, and it is unclear where or when new funding will become available to close the gap between successful R&D and commercial deployment.[84]

Risk and Financing

Existing tax credits were preserved in the 2025 One Big Beautiful Bill (OBBB) through 2033 (vs. 2026–2027 for wind/solar). They may extend as far as 2036, although even that timeframe may still be too short for full EGS scale-up, and will likely need to be revisited. These tax credits may also be insufficient to address financing challenges.[85]

Exploration risk is a major concern. A single well costs $5 million to $10 million to drill, and success is uncertain—developers may drill and find insufficient heat or permeability. At FORGE, well development costs have fallen from $13 million to $5 million per well as drilling rates have improved, but initial wells in new geologic settings remain expensive and uncertain.[86]

This problem is being addressed from multiple angles.

Innovative new technical tools can provide better underground prospecting before commercial-sized operations begin. Zanskar, for example, is using machine learning to predict subsurface temperatures before drilling.[87] Its models integrate geological surveys, existing well data, and geochemical analyses to identify overlooked geothermal resources. New Zealand-based GeoFlow Imaging (GFI) is exploring precision targeting within a known geothermal area. While Zanskar focuses on finding hidden geothermal systems at a regional scale, GFI uses passive seismic imaging (adapted from oil and gas shale monitoring) to focus on precisely locating drilling targets within systems that are already known to exist. Currently, GFI’s technology is still awaiting commercial validation, while Zanskar has demonstrated repeatable successes.[88]

Innovations in the financial sector offer a different approach. Some governments are exploring ways to mitigate risk through insurance against drilling failure. Germany’s Exploration Risk Insurance developed by Munich Re in cooperation with the German Federal Ministry for Economic Affairs and Energy and the German government-owned development bank KfW reduces the financial risk for investors such as municipalities and local authorities. Test drilling is carried out before every new geothermal project. If a discovery is made, the project continues as planned. If no discovery is made, Munich Re pays out the full sum insured and the project is terminated. Partial successes are more complex.[89]

In the United States, the largest potential source of government funding for commercial projects is EDF, as demonstrated by its $1.3 billion lithium/geothermal project in the Salton Sea area. However, priorities here have shifted significantly over time and currently appear focused on the battery supply chain for automobiles, so alignment between OG and EDF is at best unclear. In addition, the authorizing legislation for EDF does not explicitly prioritize the scale-up of new technologies, so funding for scale-up remains challenging.

High upfront capital costs pose another problem: geothermal projects are front loaded, with most spending happening before any revenue is earned.

Regulation and Permitting

Permitting delays have been a significant challenge for geothermal projects. Over 90 percent of identified U.S. geothermal resources are on federally managed lands, making NEPA reviews unavoidable for virtually all utility-scale development. A single geothermal project location can trigger the NEPA process six separate times—for land use planning, leasing, exploration, drilling, power plant construction, and transmission—with individual reviews ranging from under a month to over two years depending on the type of analysis required.[90] Meanwhile, the oil and gas industry has long benefited from categorical exclusions that allow routine activities to be approved without full environmental review.

Further, BLM field offices lack the staffing and geothermal-specific expertise to process applications efficiently, and geothermal permits often fall to the bottom of the priority list behind oil and gas work.[91] Transmission interconnection compounds the problem, as new interstate transmission lines take an average of more than four years to install. Overall, it can take more than 10 years to acquire all the necessary permits.[92]

Recent reforms are beginning to address these barriers. In late 2024 and early 2025, BLM finalized a new categorical exclusion for operations to confirm the existence of a geothermal resource on public lands and proposed an additional categorical exclusion for activities related to the search for indirect evidence of geothermal resources.[93] Several bills now before Congress would further streamline the process: the GEO Act would require BLM to process geothermal permits within 60 days after NEPA requirements are completed, while the Geothermal Gold Book Development Act would standardize procedures across BLM field offices.[94] These are potentially major boosts for geothermal, as federal lands in the West encompass a considerable amount of promising geographies.

Workforce Development

As of 2025, only a handful of universities offer dedicated geothermal engineering programs, so companies often compete fiercely for the same small pool of graduates. This intersects with a broader geoscience crisis: according to the most recent workforce projections from the American Geosciences Institute (AGI), roughly 27 percent of the existing geoscience workforce is expected to retire by 2029, and there aren’t enough geologists to take their place.[95] A 2022 AGI analysis finds that geoscience enrollments and degrees also have continued to decline across all levels, compounding the shortage. By the end of the decade, the country will be facing a labor gap of 130,000 full-time geoscientists.[96]

Today, geothermal companies fill their rosters by poaching workers with directly transferable skills from the fossil fuel and water-well-drilling industries. The 21st Century Energy Workforce Advisory Board (a federal advisory committee) recommended that DOE “establish geothermal centers of excellence to train oil and gas workers for geothermal jobs,” and that the current scattered system of DOE grants and industry certifications be transitioned to a more systematic approach.[97] There is no evidence yet whether these recommendations are being considered.

Grid Connections and Limited Transmission Infrastructure

Given that hydraulic fracturing creates some seismic risk, projects are often located far from population centers and hence from existing grid infrastructure. NREL’s Annual Technology Baseline includes a baseline grid connection cost of $100/kW for geothermal.[98] Costs for transmission operations are significant as well: for a 20 MW geothermal plant, operators can pay between $700,000 and $2 million annually in transmission costs (e.g., transmission lines, maintenance, and grid connection services).[99]

Delays surrounding connection requests for commercial operations have also increased from less than two years for projects built between 2000 and 2007 to over four years for those built between 2018 and 2024, with a median of five years for projects built in 2023.[100] While grid connection and power transmission costs are significant, they are a just small part of total plant costs. More importantly, plants find it hard to acquire funding prior to grid connection approval, so long wait times for transmission can push projects back by years.

One approach to transmission and grid delays is to co-locate data centers with geothermal plants. Google, Meta, and Microsoft have all signed PPAs with geothermal companies to provide energy for new data centers. Some are “behind-the-meter” with no grid connection, and the “energy park” concept is gaining traction—integrating multiple electricity generation sources, storage solutions, and co-located data centers behind one point of interconnection as a form of large-scale microgrid.

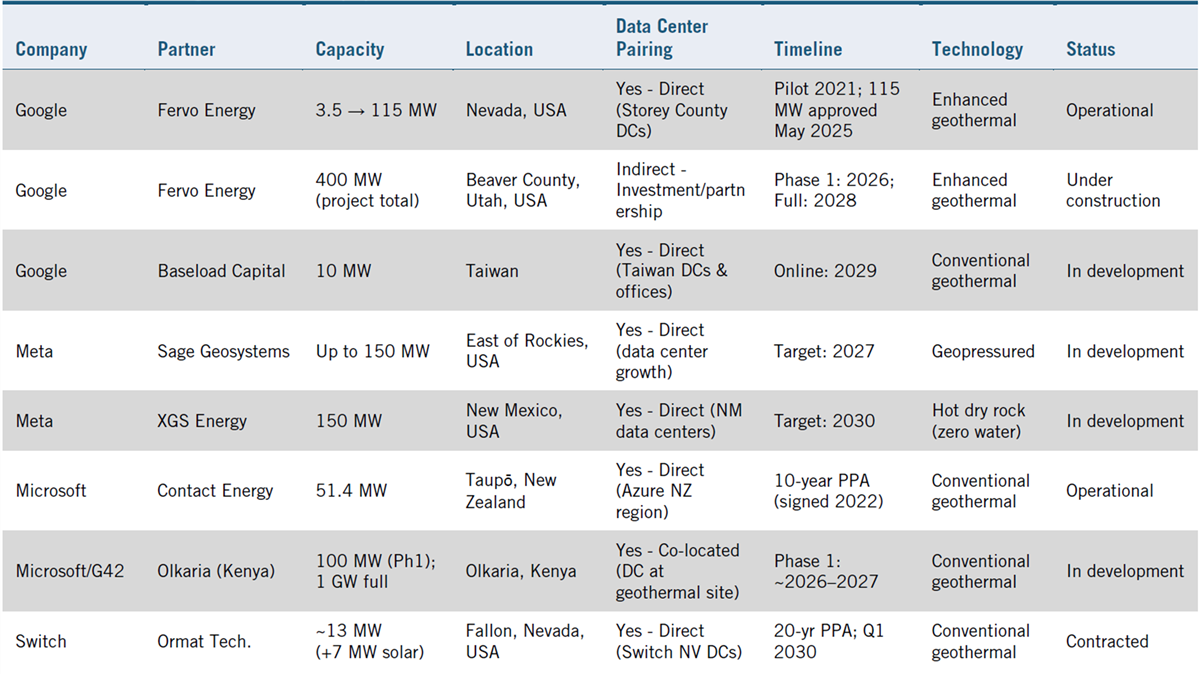

Table 3: Data centers and geothermal, current projects

Recommendations

R&D

The FORGE project has been remarkably successful at relatively low cost in a very short span of time. It also offers a model through its open-access approach to data and its successful partnerships with both the private sector and universities.

As such, it must be a high priority for DOE to support further developments at FORGE, and it is encouraging that additional funding has been provided. However, perhaps a more proactive approach to geothermal R&D should be supported as a high-priority project within DOE. A big success should be followed by rapid efforts to take full advantage of the related opportunities, including expanding the core project.

Congress and DOE should review FORGE from two perspectives: 1) look for opportunities to grow its activities both in Utah and elsewhere as EGS footprints grow, perhaps in particular to a location east of the Mississippi, and 2) exploring use of FORGE open-source data dissemination as a model for other precompetitive DOE investments, such as the MARVEL project for nuclear microreactors. Open dissemination should be the default option, not the exception.

Financing

The current federal support structure is poorly designed and insufficient. It offers grants for R&D, access to testing and validation via FORGE, tax credits through the Investment Tax Credit (ITC) and Production Tax Credit (PTC), and possibly loans (which may or may not be subsidized) via EDF. This leaves plenty of gaps, lots of uncertainty, and limited instruments.

DOE should develop other options, all of which could be designed to spur scale-up. EDF is the logical location, but as currently authorized, it is far too limited in both scope and capabilities to handle these new approaches. Congress must act to turn EDF from a modest loan facility into an office tasked with managing all dimensions of scale-up for new technologies (a forthcoming paper will address these issues). Doing so would allow systematic exploration of options for accelerating rollout, which include the following:

▪ Dry-well insurance. Essentially, drilling insurance offers the mutualization of risk, if the exploration company choses to use it. Under the German model, for example, risk insurance is provided by the private sector but is supported by the government. Companies choose whether to participate, and are reimbursed for dry wells.

▪ Government funded exploration. Government could directly fund exploration on federal land, and then recoup costs by licensing successful wells to developers or auctioning off licenses. Doing so could substantially expand exploration—and could lead to the emergence of specialist exploration companies.

▪ Government supported exploration. Countries with nascent geothermal programs have also used cost-shared exploratory drilling wherein government pays a portion and, if commercially successful, the developer refunds the government’s share.

▪ U.S. co-investment. The current administration is clearly interested in expanding government equity stakes in strategic sectors. Government co-funding acts to mitigate risks for other investors, as the German model suggests.[101]

▪ Scale-up loans. EDF needs to refocus on scale-up. Tactical wins in selected sectors are helpful but largely irrelevant in the long term. If geothermal shows that it is on a path to meeting the challenge of P3 (see box 1), it should be a strategic imperative for EDF to provide loan funding to accelerate deployment and scale-up.

All these funding options are worth systematic exploration, as are further solutions being developed in other countries. Relying only on existing U.S. tools and legislation would likely leave a lot of innovation (and cheap energy) on the table.

Permitting

Four pending bills form an interlocking package that would address the structural bottlenecks constraining geothermal development on federal lands. The STEAM Act eliminates the core permitting asymmetry by extending categorical exclusions to geothermal, reducing the number of NEPA reviews required for activities that are functionally identical to oil and gas drilling.[102] The CLEAN Act ensures a steady pipeline of leasable land by requiring annual geothermal lease sales and mandating replacement sales when BLM misses scheduled auctions.[103] The Geothermal Ombudsman Act addresses BLM’s uneven institutional capacity by creating a task force to share best practices across field offices and allow qualified staff to support geothermal reviews outside their home areas.[104] And the Geothermal Cost-Recovery Authority Act funds the entire apparatus by authorizing BLM to charge developers permitting fees—the same mechanism already available for oil and gas, wind, and solar, but from which geothermal is currently excluded.[105]

These four reforms are mutually dependent. Categorical exclusions are only as fast as the staff available to process them; staff capacity is unsustainable without dedicated funding; funding is meaningless without regular lease sales to generate a pipeline of projects; and all of it is slower than necessary without streamlined environmental review. Enacted together, they are designed to create a self-sustaining system in which industry fees fund the permitting infrastructure that enables the accelerated reviews that make geothermal development viable on federal lands.

The new categorical exclusion for certain geothermal operations on public lands announced by BLM in January 2025, and efforts to expand those explosions, are welcome and should be supported. Beyond public lands, under Section 390 of the Energy Policy Act of 2005, oil and gas receive categorical exclusions for activities requiring fewer than five acres of surface disturbance and for drilling on previously drilled and approved locations.[106] The GEO Act currently active within Congress calls for that broad exclusion to be applied to geothermal as well.

Congress should approve pending legislation to promote permitting parity between geothermal and oil and gas on federal lands. That’s a good start, but it will not be sufficient, and must be revisited soon: geothermal plants use between one and eight acres per MW (including cooling towers and the power plant), so commercial-size plants won’t fit on a five-acre plot. Congress must find a more permanent solution.

Accelerated permitting on non-federal lands should be a further step. While federal lands are likely sufficient west of the Mississippi, that’s not the case in the much more populated Eastern United States. Faster permitting there will be needed once EGS or SHR fully proves out.

Geothermal also faces staff shortages at BLM, where field offices vary significantly in staffing capacity, technical understanding, and interpretation of rules—resulting in what a recent report calls a “piecemeal approach that sends mixed messages to industry.”[107]

We strongly recommend that Congress and the administration ensure that BLM has sufficient staff to accelerate geothermal permit approvals, particularly given the recent and proposed changes to BLM permitting (see “Workforce” ahead). Perhaps a more centralized approach would help eventually with scale-up.

Interconnection

Geothermal plants also often sit far from end users and need a grid connection. Today, that means joining an interconnection queue in which the typical wait has stretched to five years. Federal Energy Regulatory Commission (FERC) Order 2023 helped by replacing the old first-come-first-served system with a first-ready-first-served approach, but geothermal needs more.[108] A geothermal project that has drilled confirmation wells and signed a PPA is not the same as a speculative solar application that may never break ground—yet they may be treated identically.

Regulators should create a “geothermal readiness tier” that gives projects with proven resources and committed buyers a higher priority. Only 14 percent of projects that enter interconnection queues get built; prioritizing those most likely to be completed would speed up the queue for everyone.

Network upgrade costs have also risen sharply. When a new power plant connects to the grid, the developer often pays to upgrade nearby transmission lines, transformers, and substations. Geothermal plants, often built far from existing grid infrastructure, are especially exposed. Yet, geothermal runs around the clock at over 90 percent capacity—a reliability benefit the current rules ignore when assigning costs.

FERC and state regulators should credit geothermal’s steady output against upgrade charges. Regulators should also prioritize behind-the-meter projects co-located with data centers that minimize interconnection needs and skip the queue altogether—and should prioritize projects with firm production funding and offtake agreements.

Workforce

DOE’s Geothermal Liftoff Report identifies “Scale and Train Workforce” as the first of five major imperatives for achieving commercial liftoff for geothermal heating and cooling.[109] This will require action, especially as an upcoming wave of worker retirements is anticipated. It is not enough to simply hope that the market will solve the need to create a new geothermal workforce; an active initiative from DOE and the Department of Labor will clearly be needed.

The 2025 Energy Workforce Advisory Board report offers some solid suggestions, including encouraging apprenticeships and education, highlighting energy careers, and providing options for DOE to drive workforce development. The report notes that more than 25 percent of oil, gas, and geothermal workers are over 55 years old, and calls for retaining aging workers as mentors and trainers “to support this critical juncture of knowledge transfer.” Possibly most important of all, they mention the need to promote “policy certainty.” Particularly now, with the rapidly shifting landscape created by AI, career uncertainty due to political instability for a specific energy source can be discouraging enough to prevent people from investing the training time to joining the workforce.[110]

DOE needs to work extensively with industry to smooth the pathway into the geothermal workforce while expanding funding for higher education training of both technicians and geoscientists.

Conclusion

Geothermal is at an inflection point. Fervo’s rapid development from an interesting technology to a commercial supplier of energy at scale is remarkable, and strongly suggests that there is a substantial future for EGS in the United States and elsewhere. Deeper wells and the avoidance of existing reservoirs make it more likely that the conditions underground will support successful geothermal, while Fervo’s rapid improvement in drilling efficiency is substantially reducing costs at a rapid rate. However, while getting to commercial scale is a remarkable achievement, its offtake agreements currently rest at least in large part on California’s clean energy mandates and on federal ITC\PTC subsidies. Its recent IPO filing strongly suggests that Fervo is moving rapidly along the path to P3, but it is not there yet.

EGS can therefore play an important role in the U.S. energy landscape (and indeed the global landscape), but there is still a lot of work to be done. It is absolutely in the U.S. interest to help drive down costs both by further technology development and through support for scale-up as needed.

Acknowledgments

The author thanks to Daniel Gaster for his extensive work as a researcher on this paper. Any errors or omissions are the author’s responsibility alone.

About the Author

Dr. Robin Gaster is research director at ITIF’s Center for Clean Energy Innovation, and president of Incumetrics Inc. His primary interests lie in climate, economic innovation policy, metrics, and innovation assessment. He has worked extensively on climate, innovation and small business, and regional economic development.

About ITIF

The Information Technology and Innovation Foundation (ITIF) is an independent 501(c)(3) nonprofit, nonpartisan research and educational institute that has been recognized repeatedly as the world’s leading think tank for science and technology policy. Its mission is to formulate, evaluate, and promote policy solutions that accelerate innovation and boost productivity to spur growth, opportunity, and progress. For more information, visit itif.org/about.

Endnotes

[1]. “Fervo Energy Drilling Results Show Rapid Advancement of Geothermal Performance - Fervo Energy,” Fervo, accessed March 3, 2026, https://fervoenergy.com/fervo-energy-drilling-results-show-rapid-advancement-of-geothermal-performance/.

[2]. Chad Augustine et al., Enhanced Geothermal Shot Analysis for the Geothermal Technologies Office, NREL/TP-5700-84822, 1922621, MainId:85595 (2023), NREL/TP-5700-84822, 1922621, MainId:85595, https://doi.org/10.2172/1922621.

[3]. Think GeoEnergy and Carlo Cariaga, ThinkGeoEnergy’s Top 10 Geothermal Countries 2024 – Power, January 20, 2025, https://www.thinkgeoenergy.com/thinkgeoenergys-top-10-geothermal-countries-2024-power/.

[4]. Original diagram using AI from text prompt.

[5]. Original diagram using AI from text prompt.

[6]. Original diagram created with AI

[7]. “Project Geretsried,” Eavor Deutschland, accessed March 3, 2026, https://eavor.de/en/projekt-geretsried/.

[8]. Think GeoEnergy and Carlo Cariaga, Eavor Publishes 4-Year Update on Eavor-Lite Demonstration Project in Canada, January 10, 2024, https://www.thinkgeoenergy.com/eavor-publishes-4-year-update-on-eavor-lite-demonstration-project-in-canada/.

[9]. Admin, “Eavor Announces Significant Drilling Performance Gains at Geretsried Geothermal Project,” Eavor, October 28, 2025, https://eavor.com/press-releases/eavor-announces-significant-drilling-performance-gains-at-geretsried-geothermal-project/.

[10]. Energy glossary, “Geothermal gradient,” accessed March 3, 2026, https://glossary.slb.com/en/terms/g/geothermal_gradient.

[11]. Energy glossary, “Pressure gradient,” accessed March 3, 2026, https://glossary.slb.com/en/terms/p/pressure_gradient.

[12]. Michal Kruszewski and Volker Wittig, “Review of Failure Modes in Supercritical Geothermal Drilling Projects,” Geothermal Energy 6, no. 1 (2018): 28, https://doi.org/10.1186/s40517-018-0113-4

[13]. Casey Crownhart, “This Startup Wants to Use Beams of Energy to Drill Geothermal Wells,” MIT Technology Review, accessed March 3, 2026, https://www.technologyreview.com/2025/07/22/1120545/geothermal-drilling-quaise/.

[14]. “Quaise Energy Achieves Drilling Milestone with Millimeter Wave…” Quaise Energy, July 22, 2025, https://www.quaise.com/news/quaise-energy-achieves-drilling-milestone-with-millimeter-wave-technology.

[15]. Gunnar Gunnarsson et al., “The Iceland Deep Drilling Project (IDDP): 2022 Geothermal Rising Conference: Using the Earth to Save the Earth, GRC 2022,” Using the Earth to Save the Earth - 2022 Geothermal Rising Conference, Transactions - Geothermal Resources Council, 2022, 134–44.

[16]. Carlo Cariaga, “Orkuveitan to Lead Deep Geothermal Drilling Project in Iceland Targeting 400 °C Temperatures,” Think GeoEnergy, October 21, 2025, https://www.thinkgeoenergy.com/orkuveitan-to-lead-deep-geothermal-drilling-project-in-iceland-targeting-400-c-temperatures/.

[17]. “Fervo Energy Announces 320 MW Power Purchase Agreements with Southern California Edison,” Fervo Energy press release, June 25, 2024 https://fervoenergy.com/fervo-energy-announces-320-mw-power-purchase-agreements-with-southern-california-edison/.

[18]. Claire Hao, “Houston geothermal startup Fervo to receive up to $25 million from Department of Energy,” Houston Chronicle, February 14, 2024 https://www.houstonchronicle.com/business/energy/article/houston-geothermal-fervo-funding-18665551.php.

[19]. Sonal Patel, “Delving Deeper: New Optimism for Enhanced Geothermal Systems,” POWER Magazine, April 2, 2024, https://www.powermag.com/delving-deeper-new-optimism-for-enhanced-geothermal-systems/.

[20]. “Fervo Energy Drilling Results Show Rapid Advancement of Geothermal Performance,” Fervo Energy Press Release, February 12, 2024, https://fervoenergy.com/fervo-energy-drilling-results-show-rapid-advancement-of-geothermal-performance/.

[21]. Patel, “Delving Deeper.”

[22]. “Technology,” Fervo Energy, August 9, 2022, https://fervoenergy.com/technology/.

[23]. Trent Jacobs, “Fervo and FORGE Report Breakthrough Test Results, Signaling More Progress for Enhanced Geothermal,” Journal of Petroleum Technology, September 16, 2024 https://jpt.spe.org/fervo-and-forge-report-breakthrough-test-results-signaling-more-progress-for-enhanced-geothermal.

[24]. “2024 Year in Review: Leading the Charge in Geothermal Innovation,” Fervo Energy, February 4, 2025 https://fervoenergy.com/2024-year-in-review/.

[25]. “Fervo Energy Raises $244 Million to Accelerate Deployment of Next-Generation Geothermal,” Fervo Energy press release, February 29, 2024 https://fervoenergy.com/fervo-energy-raises-244-million-to-accelerate-deployment-of-next-generation-geothermal/.

[26]. Ibid.

[27]. “Fervo Energy Breaks Ground on the World’s Largest Next-gen Geothermal Project,” Fervo Energy press release, September 25, 2023 https://fervoenergy.com/fervo-energy-breaks-ground-on-the-worlds-largest-next-gen-geothermal-project/; Tim Fitzpatrick, “Fracking for Heat: Utah Could Become Home to World’s Largest Enhanced Geothermal Plant,” The Salt Lake Tribune, March 9, 2024, https://www.sltrib.com/news/2024/03/09/fracking-heat-utah-could-become/.

[28]. Ibid.

[29]. Lisa Martine Jenkins, “The ‘clean transition tariff’ won approval in Nevada. What’s next for Fervo?” Latitude Media, May 15, 2025 https://www.latitudemedia.com/news/the-clean-transition-tariff-won-approval-in-nevada-whats-next-for-fervo/.

[30]. Fervo Energy Company, Security and Exchange Commission Form S-1, April 17, 2026, https://www.sec.gov/Archives/edgar/data/1853868/000162828026025821/fervoenergy-sx1.htm.

[31]. Jenkins, op. cit.

[32]. Fervo Energy, “Fervo Energy announces 320mw power purchase agreements with Southern California Edison,” Fervo press release, https://fervoenergy.com/fervo-energy-announces-320-mw-power-purchase-agreements-with-southern-california-edison/.

[33]. Diana Digangi, “Fervo, Southern California Edison ink record-setting 320-MW geothermal deal,” Utility Dive, June 28, 2024 https://www.utilitydive.com/news/fervo-geothermal-deal-california-edison-energy/720128/.

[34]. Amanda Peterson Corio and Briana Kabor, “How Google is helping create a new model for clean energy,” Google blog, June 13, 2024 https://blog.google/outreach-initiatives/sustainability/google-clean-energy-partnership/.

[35]. Briana Kabor, “Google’s new model for clean energy approved in Nevada,” Google blog, May 16, 2025 https://blog.google/feed/nevada-clean-energy/.

[36]. Emma Penrod, “NV Energy seeks new tariff to supply Google with 24/7 power from Fervo geothermal plant,” Utility Dive, June 21, 2024 https://www.utilitydive.com/news/google-fervo-nv-energy-nevada-puc-clean-energy-tariff/719472/.

[37]. Fervo Energy, “Fervo Energy Announces 31 MW Power Purchase Agreement with Shell Energy,” Fervo Press Releases, April 15, 2025, https://fervoenergy.com/fervo-energy-announces-31-mw-power-purchase-agreement-with-shell-energy/.

[38]. Maria Galluci, “America’s First ‘enhanced’ Geothermal Plant Just Got up and Running,” Canary Media, November 28, 2023, https://www.canarymedia.com/articles/geothermal/americas-first-enhanced-geothermal-plant-just-got-up-and-running.

[39]. Fervo Energy, “Fervo Energy and Vallourec Announce Long-Term Supply Agreement to Scale Domestic Geothermal Infrastructure,” April 9 2026. https://fervoenergy.com/fervo-energy-and-vallourec-announce-long-term-supply-agreement-to-scale-domestic-geothermal-infrastructure/

[40]. Fervo, SEC Form S-1, April 17, 2026, https://www.sec.gov/Archives/edgar/data/1853868/000162828026025821/fervoenergy-sx1.htm.

[41]. Mark McClure, “Digesting the Bonkers, Incredible, Off-the-Charts, Spectacular Results from the Fervo and FORGE Enhanced Geothermal Projects,” ResFrac, September 12, 2024, https://www.resfrac.com/blog/digesting-the-bonkers-incredible-off-the-charts-spectacular-results-from-the-fervo-and-forge-enhanced-geothermal-projects.

[42]. “Thermal Power Plants More Competitive than Clean Energy When Considering Reliability: Vistra CEO | Utility Dive,” Utility Dive, accessed March 12, 2026, https://www.utilitydive.com/news/vistra-gas-nuclear-coal-plants-clean-energy-tulane/759990/.

[43]. Saul Elbein, “Energy Secretary Chris Wright Throws Support behind Geothermal Boom,” Text, The Hill, March 6, 2025, https://thehill.com/policy/equilibrium-sustainability/5178802-energy-secretary-chris-wright-throws-support-behind-geothermal-boom/.

[44]. Where activities described in this paper took place before GTO became HGEO, we have retained the previous name for clarity.

[45]. “Department of Energy Announces $14.5 Million to Advance Geothermal Drilling Technologies,” DOE, April 23, 2018, https://www.energy.gov/articles/department-energy-announces-145-million-advance-geothermal-drilling-technologies.

[46]. “DOE to Invest Up to $165 Million to Advance Domestic Geothermal Energy Deployment,” DOE, July 28, 2022, https://www.energy.gov/articles/doe-invest-165-million-advance-domestic-geothermal-energy-deployment.

[47]. “FORGE Phases and Sites,” DOE, https://www.energy.gov/eere/geothermal/forge-phases-and-sites.

[48]. Utah FORGE Latest News, DOE, https://utahforge.com/news_archive/.

[49]. “FORGE Phases and Sites,” DOE.

[50]. Brian Maffly, “Utah FORGE achieves crucial geothermal milestone,” University of Utah, May 30 2024 https://attheu.utah.edu/science-technology/supported-with-200-million-from-doe-university-of-utah-research-peo/.