AI Is Not Going to Reduce Labor’s Share of Income or Destroy the Tax Base

As AI capabilities continue to advance, some people have begun raising concerns about the long-term implications for the tax base. A popular line of argument holds that widespread automation could reduce labor income, shift economic activity toward capital, and ultimately erode payroll tax revenues that fund major government programs. Some have even suggested policymakers should begin “modernizing” the tax system in anticipation of these changes.

But this concern is likely overstated.

The tax base would erode only if labor’s share of income fell dramatically and persistently over many years. That scenario is highly unlikely because workers displaced by AI are unlikely to permanently disappear from the labor market. Instead, most will transition into new occupations and industries, just as workers have during previous waves of technological change. As such, policymakers should refrain from changing the tax base on the assumption that labor income will decline while corporate capital gains increase. Instead, they should focus on diffusing AI across the economy to ensure U.S. businesses remain globally competitive and on supporting worker training and adjustment policies that help Americans transition successfully to new jobs.

Using data on labor’s share of income, GDP growth, and labor income tax rates, the Information Technology and Innovation Foundation (ITIF) developed a simple model to estimate how much the labor share would need to decline before tax revenue actually falls. The model compares a baseline year of tax revenue with the following year, in which the economy continues to grow but labor’s share of income declines.

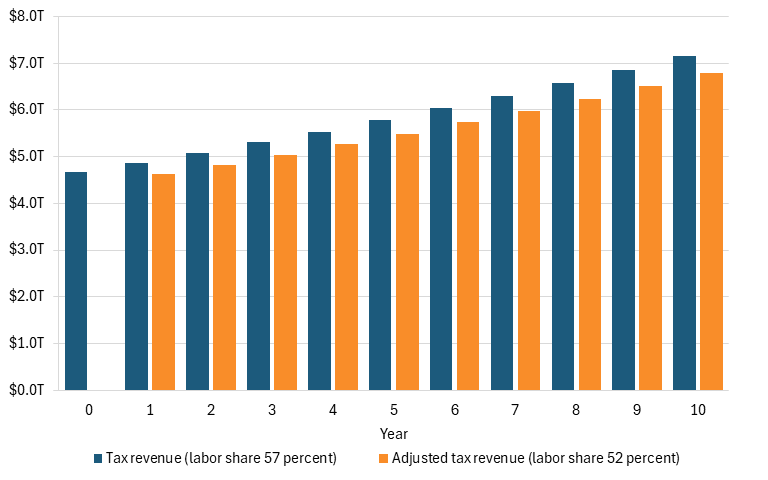

The results suggest that labor’s share of income would have to fall sharply just to reduce current tax revenue. For example, with labor share at 57 percent in the baseline year (Year 0), tax revenue would total roughly $4.7 trillion. Assuming GDP growth in the following year (Year 1), tax revenue would naturally rise to about $4.9 trillion if the labor share remained stable. To reduce tax revenue below the Year 0 level, labor share would need to fall from 57 percent to roughly 52 percent in a single year, a dramatic five-percentage-point decline. By comparison, labor’s share of income has dropped by an average of just 0.1 percent annually over the last 73 years. Yet even then, the erosion would likely be temporary. Indeed, by Year 2, GDP growth alone would bring tax revenue back above the Year 0 level, recovering the tax base. (See figure 1.)

Figure 1: U.S. tax revenue from Year 0 to Year 10, by labor share of income

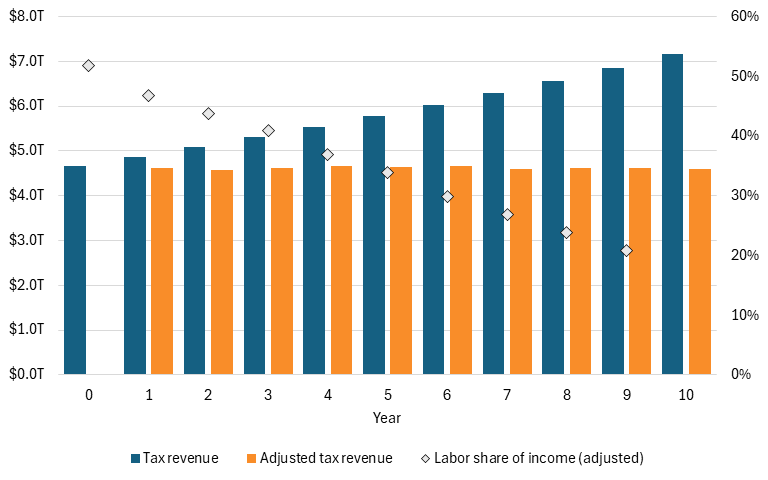

Because economic growth increases the overall size of the economy, tax revenue would recover unless the labor share continued to fall each subsequent year. In the model, labor share would need to decline to approximately 47 percent in Year 2, then continue falling year after year to keep reducing the tax base below the Year 0 level. By Year 10, labor’s share of income would have to collapse to roughly 21 percent to keep tax revenue below its original level.

Figure 2: U.S. tax revenue from Year 0 to Year 10 and labor share of income needed to reduce tax revenue to below Year 0

That scenario borders on implausible. Historically, the U.S. economy has repeatedly adapted to major technological disruptions without experiencing catastrophic declines in labor income. From the spread of industrial machinery to the rise of computers and the Internet, new technologies have consistently reshaped work rather than eliminated it altogether. Between the 1950s and 2023, the U.S. labor share of income remained relatively stable, fluctuating largely between 57 and 64 percent despite enormous technological change.

Moreover, research on automation also suggests that technological disruption tends to reallocate labor rather than permanently eliminate it. Workers displaced by automation frequently move into new occupations, including ones created by emerging technologies themselves. AI will almost certainly disrupt labor markets, but disruption does not necessarily imply a collapse in labor income.

This matters because the proposed solution of shifting more taxation toward capital-based revenue could create serious unintended consequences.

First, higher taxes on capital income reduce the return on investment, weakening firms’ incentives to invest in AI infrastructure, advanced equipment, and productivity-enhancing technologies. In a global environment where countries such as China are aggressively investing in AI and advanced industries, discouraging domestic investment could undermine U.S. competitiveness.

Second, the proposal could also reduce business investment in research and development (R&D), weakening U.S. competitiveness. Many advanced industry firms rely heavily on retained earnings and capital returns to finance innovation. Semiconductor companies in the United States, for example, spend roughly 17.7 percent of revenue on R&D. Pharmaceutical firms similarly tie R&D expenditures closely to revenue streams. Moreover, a study by Mulligan et al. found that lower corporate tax burdens can increase innovation productivity within U.S. borders.

As a result, shifting the tax base away from labor and toward capital could unintentionally slow AI adoption, weaken innovation, and reduce U.S. competitiveness, which are the very outcomes policymakers should be trying to avoid.

As such, rather than redesigning the tax system around the assumption that AI will permanently destroy labor income, policymakers should focus on ensuring broad AI diffusion throughout the economy. The goal should be to help workers use AI to become more productive, transition into new occupations, and complement emerging technologies. Policies that encourage workforce adaptation, skills development, and technological adoption are far more likely to strengthen the economy than policies built around fears of a collapsing labor market.

Humans have adapted to major technological transformations before, and there is little reason to believe AI will be fundamentally different.

Methodology

To calculate the labor share of income needed to erode the tax base (that is, reduce tax revenue to the Year 0 level), ITIF first obtained the compound average annual growth rate of GDP from 2004 to 2024, the average labor income tax rate from 2016 to 2025, the average tax revenue share of GDP from 2015 to 2024, and the labor share of income in 2023.

To calculate the tax revenue in Year 0, the average tax revenue share of GDP was multiplied by the GDP in 2023. This assumes that this is the tax revenue when labor’s share of income is 57 percent, which was the share in 2023, and the tax rate on labor was 17 percent.

To calculate how much the labor share needs to decline in subsequent years (Years 1 through 10) to fall below that of Year 0, we first calculated the GDP by multiplying the previous year’s GDP by (1 + the average annual growth rate of GDP). Then, ITIF multiplied the new GDP by the average tax revenue share of GDP to obtain tax revenue when labor share remains unchanged (or remains at 57 percent). Next, the new GDP was multiplied by the unchanged labor share of income to obtain the amount of labor income in the economy if the labor share had remained unchanged. This labor income amount was then multiplied by the average labor income tax rate to obtain the labor tax revenue when labor share remains unchanged from Year 0.

Then, to obtain the new tax revenue, we selected a new labor share of income, which was multiplied by the new GDP to obtain labor income at that level. Next, labor income at the new labor share level was multiplied by the labor income tax rate to determine the labor income tax revenue.

To obtain the tax revenue losses from a change in labor income, the labor tax revenue after adjusting labor income share was subtracted from the labor tax revenue when the labor share remained unchanged (from Year 0). Then, this tax revenue loss is subtracted from the overall tax revenue when labor share was unchanged to obtain the new overall U.S. tax revenue after labor share had changed. The new overall U.S. tax revenue after a decline in labor share was then compared to the overall U.S. tax revenue in Year 0 to determine whether the decline in labor share was sufficient to erode the tax base. If not, the labor share of income continued to decline incrementally (by 1 percentage point each time) until the overall tax revenue fell below that of Year 0.

Editors’ Recommendations

July 27, 2022

US AI Policy Report Card

September 18, 2025

Hey, AI Job Doomers: Wanna Bet?

November 4, 2025

An AI Job Apocalypse? Watch This Chart

Related

June 19, 2026

Bad Taxes Would Slow AI Innovation

June 8, 2026

Taxing AI Compute Would Be a Mistake

April 8, 2019