The United States Needs Data Centers, and Data Centers Need Energy, but That Is Not Necessarily a Problem

Electricity demand is growing rapidly and starting to strain the grid. Instead of slowing the growth of data centers, the United States should deploy new technologies and strategies to efficiently increase grid capacity while accelerating new generation and transmission.

KEY TAKEAWAYS

Key Takeaways

Contents

Peak Demand and the Electricity Grid. 4

Demand Side Solutions: Demand Management, Data Centers, and More. 10

Economics of Supply-Side Innovation. 17

Appendix A: A Roadmap for FERC. 27

Appendix B: Comparing costs 28

Introduction

The explosive growth of artificial intelligence (AI) also implies rapid growth of electricity demand, for the first time in several decades. Previously, growing electrification had been roughly matched by growing efficiency, leaving demand flat. That is now changing, quite rapidly. OpenAI and the other AI companies are seeking out sources that can provide multiple gigawatts of energy, so they certainly believe demand is growing. Beyond data centers, more electric vehicles (EVs) and the electrification of homes and industries add to demand as well.

Supply is another matter. It takes time to add generating capacity to the grid, and more time to develop the transmission lines to move electricity to where it’s needed. That in part is why huge new AI campuses are being designed: AI companies can then control their own energy generation (“behind the meter”) and don’t have to worry as much about transmission.

But all that new capacity is some years away. Manufacturers have a five-year backlog for gas turbines. Solar is quicker to build but harder to permit, and locations are usually not that close to demand so transmission is needed. New-build nuclear is at least a decade away. And while we strongly support data centers bringing their own energy supplies “behind the meter,” even that will take considerable time.

Data centers therefore seek electricity from the existing grid. And the grid has a fundamental dilemma. In the early 20th century, the U.S. grid emerged from a period of competition into geographically separated monopolies. It made no sense to build separate competing wires everywhere, and electricity companies quickly became vertically integrated, managing electricity generation, transmission, and distribution. Those monopolies were closely regulated and not just for price (“rates”); the utilities needed permission to add capacity because that meant adding cost, for example.

The fundamental social contract for these regulated monopolies was that they would have to provide service to everyone who wanted it (“universal service”). These monopoly utilities were regulated in such a way that they were able to make a steady return on their assets. But deregulation over the past few decades has chipped away at those monopolies. Much of the vertical integration has been unwound. More third-party owners of generation and transmission have emerged. Competitive wholesale markets have spread. These changes have made the system more competitive and efficient.

Data centers need energy quickly, but new capacity takes time, and regulators won’t price out or abandon existing customers. So, bridging solutions to future capacity are needed.

When change was slow, regulators and utilities could cope quite easily. But now change needs to be very fast. Utilities want to serve the new demand but are cautious about building out large new facilities without guarantees that demand will in fact be there when they come onstream in 5–10 years. After all, Google just announced that the energy cost per text query fell by 93 percent in 2024 alone; maybe all that demand will just never happen. And regulators are wary of adding huge new costs to the existing rate base, especially as costs come before the revenues do, thereby adding risk. Electricity prices are driven by multiple factors on both the supply and demand sides, and data center demand is only one variable among many; the drivers of electricity demand are in fact incredibly complex. But without new capacity, adding huge new demand to the grid will have inevitable consequences when supply is constrained in the short term (next 5–10 years): either prices go up, energy allocations move from existing consumers to new ones, or both.

Simply opening the door to new demand would be normal for most markets. Prices would go up for a bit, new supply would come online, a new competitive equilibrium would emerge. And in theory, that would work for electricity as well. Perhaps it should—but it doesn’t. Regulators are not prepared to let new entrants disrupt existing supply, as they are responsible for keeping prices stable as best they can, and are generally risk averse. The price of electricity has already been a sore point for politicians, and while AI companies have plenty of high-level friends, public perspectives are less positive. At the same time, environmentalists and other long-term foes of AI and innovation more broadly see this as an opportunity, and have pressured regulators to deny data center requests.[1]

But strangling AI by accident via electricity shortages is not smart, and won’t work—it simply hands advantages to other countries and encourages U.S.-based companies to go offshore where their energy needs will be met.

That’s not necessary though. True, data centers and the grid face a period of transition. As massive new electricity demand hits the grid, new capacity will lag behind, and in the meantime regulators will not abandon existing customers or allow huge capital investments to raise prices for all users. But there are solutions to this problem. This report is about how best to fill the gap without blocking the growth of data centers or putting utilities and the grid under unnecessary strain. To get to those solutions, we have to understand how the grid operates today.

Peak Demand and the Electricity Grid

After nearly two decades of flat consumption, demand for electricity is climbing again from sources that include data centers and AI, the potential of onshore manufacturing, EVs, and electrification of heating and cooling for buildings. The U.S. Energy Information Administration (EIA) projects that electricity consumption will rise nearly 2 percent annually through 2026, marking the first sustained increase in almost 20 years.[2]

This challenge is magnified by the growth in peak-hour demand, not just average load. Transmission lines must be sized to withstand the few highest-demand hours annually, often during extreme weather or high general-use periods. A handful of those moments can drive 10–20 percent of a region’s annual transmission investment, making them disproportionately expensive benchmarks for grid design.[3]

Figure 1 shows that the percentage of annual hours during which the grid approaches peak load is very small. But the existence of peak demand and a grid sized to meet it also means that spare capacity is available at other times. That’s why combined cycle gas turbine (CCGT) gas generators—a cheap energy source—operate at only 57 percent of annual capacity on average. They are just not needed a lot of the time.[4]

Figure 1: Distribution of load as a percentage of peak, for each hour in 2022

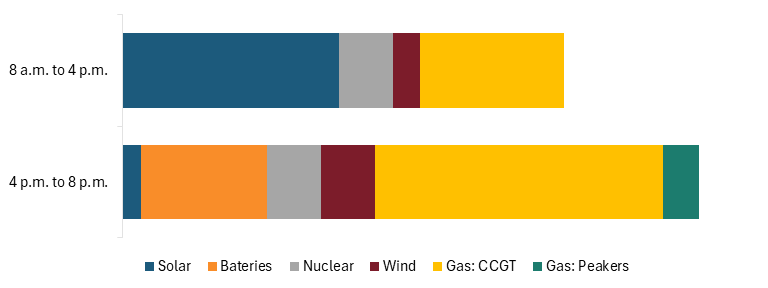

The U.S. electricity grid uses a variety of technologies to meet that demand. That mix changes over time, both daily and seasonally, and more so now because variable energy sources—wind and solar—have become a bigger component. Typically, demand is higher in the evening, which is also when solar and wind produce at much lower levels, and their energy has to be sourced elsewhere.

Figure 2: Hypothetical energy generation mix

Gas-powered generators are “dispatchable”—and can be ramped up or down to meet demand. Solar and wind are not, and nuclear also is not because it takes time to ramp up and down and the economics of nuclear power make this infeasible. Gas peakers are more expensive than CCGTs, so they are only used when CCGTs are maxed out.

The hypothetical stack shown in figure 2 shows just how the grid has excess capacity when demand is below peak. But accessing that demand so data centers and all other customers can have reliable and available energy when they need it is another story.

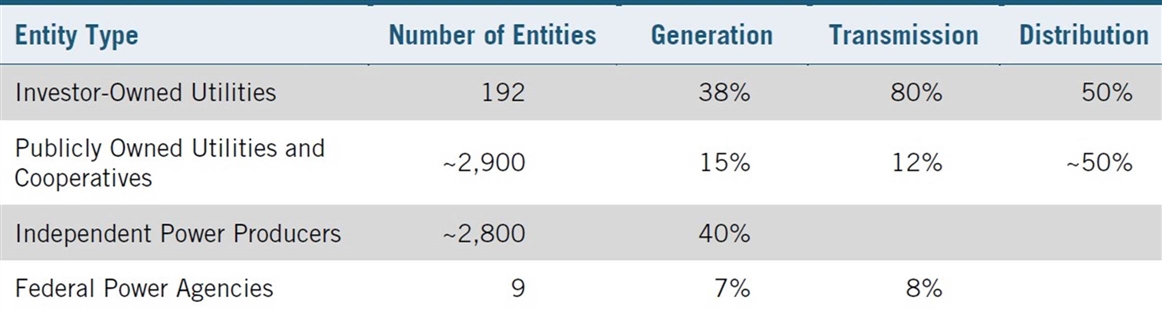

Box 1: Grid Background—U.S. Generation, Transmission, and Distribution

The U.S. electricity grid operates through three interconnected segments: generation, transmission, and distribution.

Generation. Power plants produce electricity at low voltages from either coal, natural gas, oil, nuclear reactors, wind, solar, biomass, or hydroelectric. About 40 percent is generated by independent power producers, with the remainder mostly coming from investor- and publiclyowned utilities (i.e., they are still vertically integrated). Connections to the transmission system are regulated by Federal Energy Regulatory Commission (FERC) and transmission organizations.

Table 1: U.S. electric system ownership by entity type[5]

Notes: Federal power agencies include four Power Marketing Administrations and the Tennessee Valley Authority (TVA)

Transmission networks transport electricity over long distances using high-voltage power to reduce energy loss. Most are owned by private utilities, though some belong to publicly owned utilities, electric cooperatives, or the federal government.[6] There are 10 regional organizations that manage transmission—independent system operators (ISOs) and regional transmission operators (RTOs).

While major sections of the country operate under more traditional market structures, two-thirds of the nation’s electricity load is served in RTO regions.[7] In regions with competitive electricity markets, RTOs and ISOs coordinate, control, and monitor multistate electric grids. They operate wholesale electricity markets and ensure nondiscriminatory access to transmission. Seven ISOs and RTOs manage approximately two-thirds of the electricity supply in the United States, while the rest is managed by individual utilities.[8]

The RTOs, ISOs, and individual utilities are organized into three major interconnected systems: the Eastern Interconnection, which covers areas east of the Rocky Mountains; the Western Interconnection, which serves from the Rockies westward; and the Electric Reliability Council of Texas (ERCOT), which covers most of Texas. All these entities are regulated by FERC, and generators need RTO\ISO\ERCOT permission before connecting to transmission.

Distribution systems deliver electricity to end users via lower-voltage networks. These grids are managed by investor-owned utilities, municipal utilities, and cooperatives, and are regulated by state public utility commissions (PUCs) or local government. Investor-owned utilities served approximately 72 percent of all electricity customers as of 2017.[9]

Wholesale electricity markets. FERC has been encouraging the development of competitive wholesale electricity markets, and RTOs/ISOs operate a range of competitive real-time, day-ahead, ancillary services, and operating reserve markets, in some case with locational pricing as well, alongside nonmarket power purchase agreements between individual utilities and large customers. Longer-term arrangements also exist: New England’s ISO for example operates a three-year-ahead auction every year. Some regions also include transmission-related markets, such as the Transmission Congestion market operated by the Southwest Power Pool.[10]

Demand Growth

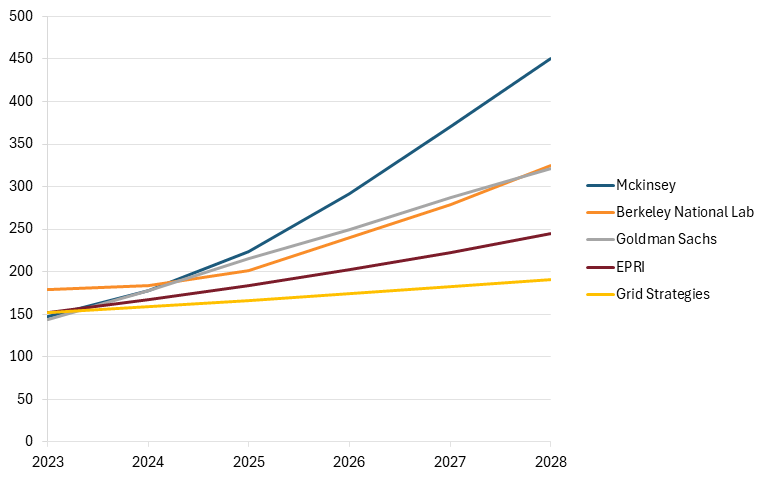

AI data center loads—including peak loads—will grow across the entire demand spectrum. By 2028, data centers are projected to consume up to 6.7–12 percent of national electricity, compared with 4 percent today, even though they are becoming much more efficient—Google claims that the energy used per text query has declined by 93 percent in the last year.[11]

American Electric Power expects that three quarters of its demand growth will come from data centers.

We do not yet know for sure whether AI will meet sometimes inflated estimates of future demand. But utilities are clearly planning for a very substantial surge. For example, American Electric Power (AEP) expects that three quarters of its demand growth will come from data centers.[12] Figure 3 shows a range of expected growth rates.

It’s also worth noting that demand growth is geographically concentrated especially in Virginia, Texas, and selected parts of the West. Those areas face particular challenges.[13]

Figure 3: Estimates for projected growth in electricity demand from data centers (TWh per year, 2023–2028)

Meeting Demand

The grid is sized for peak demand. If peak demand grows by 15 percent, that electricity must come from somewhere. Grids operate with a small margin of unused capacity at peak, because unused capacity is expensive. Utilities cannot simply tap reserves. They can run gas peakers for longer, but that capacity is also limited at peak times, and peakers are expensive to run. Adding new energy resources is expensive, takes time, and may add complications—the fastest way to add capacity is through solar farms (as the queue for gas turbine snow stretches five years or more), but these still take time, and variable energy simply is inherently complicated; peak demand is early evening for example, when solar is often useless.

Without adding new capacity to serve this new demand, increased demand inevitably leads either to price increases, rationing, or both. A sudden increase in demand therefore creates a fundamental conflict between the foundational principle that utilities must serve all comers and the existing regulatory mandate to ensure that electricity is reliable and is provided at the lowest possible cost.

This conflict has led directly to calls for halting data center deployment, fueled partly by suspicions about AI, partly by other largely NIMBY (“not in my backyard”) objections to huge new data centers, and partly by regulators and politicians frightened that they will be blamed for rapid increases in electricity prices or, worse yet, by growing numbers of retail customers unable to pay their bills. In some cases (e.g., Ohio), regulators have introduced new higher prices to discourage data centers. They have also demanded that data centers sign long-term agreements to insure against a late drop in demand from them after expensive new infrastructure is built. In other areas, regulators have responded to public concern by blocking data center deployment altogether. Bluntly, these are incredibly shortsighted responses that break the “serve all comers” foundation without solving the problem; they are the wrong response, and will be ineffective as well.

Politicians and regulators acting like ostriches are not unusual; a head in the sand is often a comfortable (and crowded) place to be. But data isn’t just the new oil; it is at the heart of both modern society and modern economies. Refusing to advance in the United States simply leaves it open to more aggressive competitors, notably China. We cannot afford that. And we don’t have to, because we can drive through the coming grid transition without turning aside, without just hoping to hide in the previous economy.

Serving new electricity demand is the price of entry into the future economy. To do so, we must take the necessary steps on both the supply and the demand side of the electricity market to provide the transitional energy we need while we build the enhanced capacity that the future will demand.

There is substantial spare capacity available on the grid to meet new demand. The problem is how to activate it, and how to ensure that peak demand is still always met.

New demand requires both short- and long-term responses. In the long term, new sources of energy must be added to the grid (or provided locally “behind the meter”), and new transmission capacity must be deployed to deliver that power to where it is needed. But rolling out new energy sources and new transmission lines takes time—sometimes a long time. Utility-scale gas turbine manufacturers now apparently have about a five-year waiting list. Variable resources face growing pushback in many states, while the best and most efficient sites for renewables are increasingly taken. Building new transmission lines is both hugely expensive and absolutely necessary, and we must do a lot better—the 2023 Department of Energy (DOE) Transmission study finds that the grid will need 5,000 new miles of transmission annually through the next decade; last year, we built 888.[14]

We must add new electricity resources, but that will take time. That transition will not be managed simply by auctioning existing electricity supplies to meet data center demand at whatever price they will pay. U.S. electricity markets are fairly tight, as existing spare peak capacity is relatively limited and quite expensive. Simply allowing substantial new demand into the market could lead to significant price increases—perhaps very significant increases—for all electricity users. The energy balance is quite delicate, and substantial new demand has to be met from existing supply.

U.S. regulators at both FERC and in the states will therefore be very reluctant to approve data center deals that take energy from existing customers (FERC regulates the interstate transmission of electricity and wholesale markets, while state PUCs regulate the intrastate distribution and sale of electricity to retail customers. Their job is to provide sufficient reliable electricity supplies to meet the needs of all customers at the lowest price. But rising electricity prices have led to growing concern at both the state and local levels about the potential need to impose higher prices across the existing customer base in order to power up data centers, even though the “serve all comers” requirement would mandate just that, and even though the link between data center demand and electricity prices is difficult to specific precisely. Regulators are trying to skirt a conflict between the mandate to serve everyone and the needs of existing customers. Because utilities are paid as a percentage of their assets, building out expensive new infrastructure (including green energy to replace dirty) will raise rates immediately, as that infrastructure is paid for by the current customer base. This leaves the current grid in a bind. New demand is arriving rapidly, but new supply is lagging behind and will take at least 5 years but perhaps 10 or more to come online.

However, there are pathways through the transition that square this particular circle. Currently, the U.S. grid operates at about 40 percent of capacity.[15] Even CCGTs, the workhorses of the U.S. electricity grid, operate at only 57–66 percent efficiency, according to EIA.[16] So there is substantial spare capacity on the grid to meet new demand. The problem is how to activate it, and to how ensure that peak demand is still always met.

On the demand side, existing efforts to reduce and reshape peak demand need to be expanded and accelerated (in part by using regulatory tweaks to provide better incentives). Data centers themselves can be a key resource, as they can provide critically important demand flexibility by time shifting nonurgent tasks, or in some cases moving them to other geographies that are off-peak at the time. There are limits to what is possible without degrading the product, but significant flexibility can be developed.

On the supply side, the limiting factors are generation in the medium and long term and transmission in the short term—the spare generating capacity exists outside of peak demand periods, but congestion on existing transmission lines means it is hard to deliver. We need to get more capacity out of existing wires, along with expanded use of utility-scale batteries and virtual power plants (VPPs) and networks of distributed energy resources (DERs), such as home solar panels, batteries, and smart thermostats, that are aggregated and managed by software to act like a single, traditional power plant. At the same time, we need to sharply reduce the time before new assets can be put into service. Currently, utilities have minimal incentives to increase efficiency. That must change.

Demand Side Solutions: Demand Management, Data Centers, and More

The current grid will be able to meet the new demand challenges—but that will require new thinking from utilities, regulators, customers, and government.

Data Centers as Grid Assets

DOE’s “2024 Powering AI and Data Center Infrastructure Recommendations” identifies three priorities: 1) improving efficiency in AI workloads, 2) codifying utility-operator flexibility contracts, and 3) accelerating clean generation and storage tailored for data center load growth.[17] The Electric Power Research Institute’s DCFlex project builds on this framework, partnering with more than 40 organizations—including Google, Meta, Microsoft, Duke Energy, and Pennsylvania-New Jersey-Maryland Interconnection (PJM)—to test demand-response, workload shifting, and use of uninterruptible power supplies (UPSs) as grid resources.[18]

Data center energy flexibility can be based partly on the nature of the tasks they run. Real-time tasks—such as search queries, video streaming, financial transactions, and live communications—must be served instantly, with latencies measured in milliseconds. These cannot be curtailed without breaking service-level agreements (SLAs). These originally dominated data center workloads, but they are now rapidly becoming swamped by AI.

But not all tasks must run instantly. Non-real-time tasks (“non-critical tasks”) include model training, batch analytics, content indexing, software updates, and background storage operations. Such tasks can be temporally shifted (moved to lower-demand hours) or geographically shifted (moved to facilities in less-constrained grid regions) without degrading user experience. Google, for example, has shown that AI training jobs can be paused and restarted in different time zones, effectively moving load with the sun and with grid availability.[19] This is one form of demand-response flexibility, moving loads so that peak demand is reduced.

Creating a Flexible Partner for the Grid

Data centers can therefore modulate peak demand through a variety of mechanisms:

▪ Temporal Shifting. Non-critical workloads can be deferred to night hours or to times when output from renewable sources is high. Microsoft reports that it already schedules certain training tasks overnight when wind generation peaks in Texas.[20]

▪ Geographic Shifting. Large data center providers with global networks such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform can route computing tasks to regions with spare grid capacity or abundant renewables. Google pioneered this with its “carbon-intelligent computing” platform, which shifts compute to align with local clean generation supply—and also applies to other reasons for shifting demand as well.[21]

▪ UPS Utilization. Every hyperscale facility contains uninterruptible power supplies via batteries for resilience. Aggregated across a single site, this may provide 50–100 megawatts (MW) of short-term capacity (1–4 hours). Meta and Microsoft have both piloted programs to dispatch UPS fleets into demand-response markets where they can help to blunt demand at peak periods.[22]

▪ Cooling Flexibility. Chiller and HVAC systems can pre-cool facilities in advance of peaks, then coast through short intervals without active cooling. AWS has experimented with this approach at its Virginia campuses.[23]

▪ AI-Aware Scheduling. By integrating grid signals into job schedulers, operators can automatically pause or resume noncritical workloads in response to frequency or price conditions. The Electric Power Research Institute’s (EPRI’s) DCFlex pilots show that 10–40 percent load modulation is feasible without breaching SLAs with customers.[24]

▪ Contracted Demand Response. Through direct partnerships with utilities, data centers can pledge interruptible load during stress events. Google has signed such contracts with the TVA and Indiana Michigan Power, allowing short-term curtailment during peak intervals.[25]

Real-World Examples

▪ Google uses carbon-intelligent workload shifting across its global fleet, aligning compute with renewable generation and curtailing AI training tasks during peak grid demand.[26]

▪ Microsoft pilots hydrogen fuel cells for backup power and time-shifts training workloads in Texas to align with wind output.[27]

▪ AWS tests HVAC pre-cooling in Virginia and participates in regional demand-response markets with UPS systems.[28]

▪ Meta collaborates with PJM in the DCFlex project, demonstrating 10–15 MW of dispatchable UPS and load modulation capacity.[29]

Table 2: Flexibility pathways for hyperscale data centers

|

Flexibility Pathway |

Timescale |

Operator Examples |

System Value |

|

Temporal Load Shifting |

Hours–Days |

Google, Microsoft |

10–40 percent of non-real-time workloads shiftable |

|

Geographic Load Shifting |

Hours–Days |

Google, AWS |

100s of MW globally routable |

|

UPS Utilization |

Seconds–Minutes |

Meta, Microsoft |

50–100 MW per site (short duration) |

|

Cooling Pre-charging |

Hours |

AWS, Meta |

5–10 percent facility load reduction during peaks |

|

AI-Aware Scheduling |

Seconds–Hours |

Google, Meta, Microsoft |

10–40 percent load modulation achievable |

|

Backup Generation |

Minutes–Hours |

Microsoft, AWS |

10–50 MW/site (diesel today, hydrogen emerging) |

|

Contracted Demand Response |

Minutes–Hours |

Google, TVA; AWS, Dominion Energy |

10–100 MW depending on site contracts |

Flexibly reducing peak loads need not impair data center operations. Real-time workloads remain protected, while noncritical tasks and supporting systems can modulate as needed. Collectively, hyperscale facilities could provide tens of gigawatts of demand-response capacity nationwide—comparable to today’s entire U.S. demand-response market.[30]

However, data centers are not charities, and they will require incentives to maximize flexibility. One option is to build flexibility into interconnection agreements. Getting approval to connect to the grid is a big challenge both at FERC and within individual states, where there are often long queues of projects waiting for approval. FERC has a large backlog of projects, and state regulators are cautious (for good reason—see Virginia box). It should, however, be possible to incentivize data centers toward flexibility by cutting the time for approval. Agreements that specifically mandate peak load management by the data center when required by the utility could be placed on a fast track to approval, especially in conjunction with the other demand management tools previously described.

Cost Assignment and Insurance for Data Center Demand: Dominion’s Virginia Rate Case[31]

New grid infrastructure is expensive, and regulators have traditionally been locked in a death struggle with utilities that want to expand their asset base because that generates more revenue and more profits, without perhaps being as necessary as the utilities claim. The rise of data centers adds a further layer to this traditional struggle: the question of who pays for necessary upgrades. Existing users, in theory (and usually in practice), get exactly zero benefit from adding either users or capacity to the grid. On the contrary, they can be on the hook for new transmission (expensive) and new generation (also expensive). This conflict can take years to sort out, and does not align at all with the urgent timeline for data center deployment.

Then there is the problem of demand insurance. Data centers are screaming for more electricity now, but what happens when projected demand is overstated? Maybe AI will become much more energy efficient. Maybe data centers will find it easier to build new facilities elsewhere than upgrade existing ones. Maybe water scarcity will have an impact. New electricity capacity has a long payback period, so utilities are wary of building assets that could be stranded when demand goes elsewhere.

These issues are well illustrated in the Dominion Energy’s Virginia rate case. Dominion is asking for a new rate class that will provide demand guarantees covering generation and transmission, a long term (14-year) contract with large users, and a separate rate for large electricity users (25 MW or higher) targeting data centers (note that Dominion’s original formulation included existing large shopping centers, which are not happy about it).

Data centers have broadly accepted the principle that rates should be transparent and that large new users should, over time, pay for the demand they need, although they have pushed back to negotiate down the specifics of the new rate class in Virginia.

On the other hand, the supply squeeze exists because building more grid infrastructure has not been a priority (indeed, it has been the opposite). Solving for short-term solutions helps, but in the end, we must build more gird infrastructure.

By reframing data centers not as “black holes” sucking in electricity from the grid but as flexible grid partners, regulators and utilities can tap a resource already embedded in the landscape of digital infrastructure. With DOE, EPRI, and the Duke University study now quantifying these opportunities, data centers can become critical partners in balancing the grid and managing periods of peak demand.

Other Demand-Side Options

Efficiency and Grid-Interactive Buildings

Energy efficiency is the original demand-side resource, but the modern grid demands more than insulation and LED lights. DOE’s Grid-Interactive Efficient Buildings (GEB) initiative envisions buildings that actively support grid stability. GEBs use automation to adjust HVAC systems, water heating, refrigeration, and lighting in response to grid signals, often with no perceptible change for occupants.

Lawrence Berkeley National Laboratory’s (LBNL’s) GEB roadmap estimates that widespread deployment could provide tens of gigawatts of flexible capacity across U.S. regional grids.[32] Meanwhile, utility-scale feeder-level Volt/VAR (Volt-Amps Reactive) optimization commonly reduces peak demand by 1–4 percent when deployed broadly.[33] These numbers sound modest, but at the scale of regional systems, they rival the capacity of a large gas plant.

EV Charging

EVs represent both a threat and an opportunity. Left unmanaged, clusters of EV chargers can stress distribution transformers and exacerbate peaks. But with smart controls, they become one of the grid’s largest flexible loads.

A 2024 joint study by DOE, the National Renewable Energy Laboratory (NREL), LBNL, and Kevala examined EV adoption scenarios across multiple states. It finds that managed charging could reduce peak load impacts by 30 percent and avoid 30–50 percent of required distribution upgrades in high-adoption cases.[34] Crucially, direct-control pilots by utilities show that savings are far greater than time-of-use tariffs alone. For example, pilots in California and Minnesota found that when utilities directly paused or staggered charging, transformers avoided overheating events; time-varying prices were not nearly so effective.[35]

In practice, managed charging requires utility–customer partnerships, clear incentives, and interoperable standards. California’s Public Utilities Commission has already authorized utilities to invest in managed charging infrastructure, while Midwest utilities are experimenting with bundled EV and home energy management offerings.

Another concrete example: Faced with the prospect of a $1 billion substation upgrade, ConEd instead invested about $200 million in a portfolio of targeted efficiency, storage, and demand-response projects: the Brooklyn-Queens Demand Management (BQDM) program. The result was 52 MW of peak demand reduction, enough to defer the substation indefinitely.[36]

The lesson has spread, albeit slowly. Utilities in California, Massachusetts, and Oregon now deploy non-wires alternatives (NWAs) routinely, using portfolios of DERs to defer or replace traditional transmission and distribution projects. While not all NWAs succeed, the concept illustrates that demand reduction, when aggregated and verified, is another alternative to steel and concrete.

The grid could reliably integrate 76–126 GW of new demand with no additional need for capacity expansion if those loads accepted modest curtailments.

Rethinking Load Growth: Peak Load Curtailment

Traditional load forecasting often assumes that demand growth is inflexible and must be met hour for hour. The 2025 “Rethinking Load Growth” report from the Nicholas Institute at Duke University challenges that premise. Modeling flexible industrial, transportation, and data center loads, it finds that the grid could reliably integrate 76–126 GW of new demand with no additional need for capacity expansion if those loads accepted modest curtailments—just 0.25 to 1 percent of annual hours. For context, peak July 2024 demand in the United States was about 760 GW.[37]

Put differently, a steel mill or AI data center that tolerates less than 100 hours of curtailment per year could allow utilities to provide many gigawatts of new capacity without proportionate transmission or generation expansion. The report argues that planning should shift from “peak-proofing” every megawatt to designing systems that treat load flexibility as a grid resource.

The implications are profound. If regulators and utilities adopt this framing, then what looks like a grid crisis may instead be a portfolio opportunity: combining efficiency, managed charging, NWAs, and flexible load commitments to create capacity at a fraction of the cost of new transmission.

Supply-Side Solutions

New generation and transmission take a long time to deploy. But there are other ways to address supply in the short and medium term without building new capacity. New technologies can squeeze a lot more capacity out of existing wires.

Dynamic Line Ratings (DLR)

Transmission lines are rated based on the amount of electricity they can safely transmit. “Static line ratings” assume worst-case conditions, such as high ambient heat, low wind, and full sun. But transmission lines often run cooler than those assumptions, especially when wind is higher, which cools conductors, and hence can safely accept higher loads. DLR uses sensors attached to transmission lines to monitor current conductor temperature, sag, and weather in real time. This enables operators to safely run higher current through the same line when conditions allow.

In 2021, FERC required all transmission providers to implement ambient-adjusted ratings (AARs) by July 2025.[38] AARs are a first step: they account for seasonal and daily temperature variations, but do not incorporate localized wind or solar data in real time; full DLR systems offer much larger capacity gains.

DLR uses sensors attached to transmission lines to monitor current conductor temperature, sag, and weather in real time.

DOE pilots in New York, Texas, and the Midwest have demonstrated the impact of DLR. In one New York case study, DLR avoided more than $1.7 million annually in wind curtailments by enabling more generation to move through existing lines. Modeling by PJM and the Brattle Group shows that DLR can increase effective line capacity by 10 to 30 percent under typical conditions, and in strong wind situations, increases can reach 40 percent.[39]

DLR is also relatively quick and cheap to deploy. A DLR retrofit requires months, not years, and costs range from $5,000 to $20,000 per mile, while new transmission construction is typically $3–6 million per mile.[40] But DLR adoption by utilities has been sluggish. Many utilities have filed for extensions to delay compliance with FERC Order 881 until 2027 or 2028.[41] Existing incentives are heavily tilted away from adoption.

Reconductoring With Advanced Conductors

If DLR unlocks hidden capacity, reconductoring replaces the conductor itself to double or even triple carrying capacity. Traditional steel-reinforced aluminum cables sag under heat, which limits the amount of power they can safely carry. New advanced conductors can operate at higher temperatures with minimal sag.

DOE and Idaho National Laboratory estimate that more than 118,000 miles of transmission lines in the Unite States are candidates for reconductoring.[42] A GridLab/UC Berkeley study modeled national deployment, and finds that reconductoring could quadruple interzonal transfer capacity by 2035, compared with a business-as-usual trajectory, and at one-third the cost of building new lines.[43] In the Unted States, Xcel Energy and Southern California Edison have begun pilot programs targeting congested corridors where reconductoring costs are far lower than acquiring new rights-of-way.[44]

International experience also validates these findings. In the European Union, utilities in Spain and Germany have used reconductoring to unlock large amounts of capacity without building new corridors.[45]

The chief barrier is once again not technology but planning and accounting rules. Traditional utility planning often treats reconductoring as an operational expense rather than a capital investment, dramatically reducing incentives for utilities to pursue it.[46] DOE has signaled that correcting these accounting asymmetries is a policy priority.[47]

Power Flow Control and Topology Optimization

Even when DLR and reconductoring raise the ceiling of a given line, congestion often results from uneven use of parallel lines. Grid physics means that power flows along the path of least resistance, which may not align with system needs. Power flow control technologies, such as flexible AC transmission systems (FACTS), modular power flow controllers, and topology optimization software can push electrons onto underused paths.

National Grid in the United Kingdom pioneered this approach, unlocking nearly 2 GW of capacity with modular flow controllers in under two years.[48] In the United States, utilities such as New York Power Authority and American Electric Power are piloting FACTS devices that can reroute flows dynamically during congestion events.[49] Software optimization layered on top of these devices allows operators to reconfigure network topology in real time, redirecting flows away from overloaded lines.[50] It’s likely that AI will have a significant impact here in the medium term.

The economics are striking: Modular flow control has been shown to unlock capacity at costs of under $50 per kilowatt (kW), a fraction of new transmission costs.[51] Deployment timelines are also measured in months, not years, making flow control an essential short-term lever.[52]

Integration and Stacking Benefits

Each of these tools—DLR, reconductoring, and flow control—works independently, but their benefits stack when deployed together. A corridor reconductored with composite conductors and equipped with DLR sensors and flow control devices could support double to triple its prior capacity—without a single new right-of-way.[53] DOE’s 2023 National Transmission Needs Study notes that if fully deployed, grid-enhancing technologies (GETs) could defer the need to build dozens of gigawatts of new long-distance transmission.[54]

In effect, GETs are the grid’s version of “software eating the world”: small, modular, and data-driven interventions that offer disproportionate value compared with steel-in-the-ground expansion.

Batteries

Storage represents a qualitatively different lever for managing grid impacts: time-shifting electricity supply itself. In practice, large-scale storage can—at a price—firm up renewable generation and also replace the need for expensive new energy sources and transmission capabilities by providing electricity to meet peak demand. Batteries are also geographically flexible, so they can be deployed to avoid the need for new transmission lines.

Grid-scale U.S battery storage has grown at breakneck speed, almost doubling from 2023 to 2024, while NREL projects 200GW of installed U.S. battery storage by 2035.[55] DOE’s “Pathways to Commercial Liftoff” report for storage anticipates that this growth will be economically compelling, avoiding $10 billion annually in grid costs.[56] Under DOE’s Grid Resilience and Innovation Partnerships (GRIP) program, utilities in California, Texas, and the Midwest are piloting large-scale storage specifically as a transmission substitute. Early modeling indicates that strategically sited batteries can defer $1 billion to $2 billion in transmission expansion costs per region.[57]

Virtual power plants

VPPs are networks of decentralized energy resources such as solar panels, home batteries, and smart devices that can be aggregated and coordinated to provide electricity and grid services. DOE estimates that scaling VPPs to 80–160 GW by 2030 could provide the equivalent of 100 large thermal power plants, at far lower cost and with far shorter lead times.[58] Companies such as Tesla, Sunrun, and Generac are already enrolling residential customers into VPP programs in California, Vermont, and Texas. However, early enthusiasm for VPPs built around rooftop solar has dissipated, as negative economics for property owners has emerged. EVs could, however, remain an important potential source of time-shifting energy capability, as they are purchased for other reasons, so their VPP capabilities do not have to survive a cost-benefit test on their own.[59]

Despite rapid progress, barriers remain. Market rules in many regions still treat storage primarily as a generation resource, not as transmission or distribution deferral. Cost allocation remains contentious: who pays for a battery that primarily reduces congestion? And long-duration storage technologies are not market proven.

The central policy question is not whether to build new transmission, but how to meet surging demand more quickly and cheaply.

Economics of Supply-Side Innovation

New high-voltage transmission lines typically cost $2.5 million to $6 million per mile.[60] Overnight capital costs (the cost of construction alone, not including interest, profits, and other costs) for new energy generation in the United States run (very roughly) from $1,700 to 2,000/kW for CCGTs to more than $10,000/kW for nuclear, and CCGT costs are growing fast as demand spikes. Transmission lines take 10–20 years to permit and build, while new nuclear deployment will take at least 10 years for large reactors. By contrast, batteries can be deployed in 2–3 years, and their costs are falling. NREL projects a further 52 percent cost decline for lithium-ion batteries by 2035, bringing capital costs to under $500/kW. Grid-enhancing technologies and other non-wires alternatives can be similarly competitive.[61]

The central policy question is not whether to build new transmission—clearly, the United States must do so—but how to meet surging demand more quickly and cheaply. Every year of delay in new transmission increases reliance on expensive peaker plants and curtailment of renewables—and increases the likelihood of fierce conflicts over access to limited energy resources.

Alternative strategies have multiple advantages:

▪ Speed. DLR, power flow controls, and data center flexibility are deployable in under a year—orders of magnitude faster than new transmission.

▪ Cost-effectiveness. DLR and power flow controls unlock capacity at pennies per kilowatt compared with new construction.

▪ Scalability. Reconductoring and storage scale nationally, while NWAs are more localized.

▪ System Value. Transmission remains essential for interregional balancing of renewables, but in the near term, stacked alternatives provide cheaper, faster relief.

Table 3: Comparative cost of grid capacity options

|

Option |

Cost Metric |

Capacity Gain |

Deployment Time |

Example Project/Case |

|

Dynamic Line Ratings |

$5K–$20K per mile |

+10–30 percent |

Months |

NYISO Pilot (2022) |

|

Reconductoring |

~⅓ cost of new lines (per MW-mile) |

2–3x capacity |

1–3 years |

Xcel Energy pilot |

|

Power Flow Controls |

<$50/kW unlocked |

100s of MW to GW |

Months–1 year |

U.K. National Grid |

|

Efficiency/NWAs |

~$3,800/kW (BQDM) |

1–4 percent peak demand reduction |

1–3 years |

Brooklyn-Queens (NY) |

|

Data Center Flexibility |

Near-zero marginal |

10–40 percent workloads shiftable |

Immediate |

Google-TVA pilot |

|

Storage (Li-ion) |

~$1,000/kW now, <$500/kW by 2035 |

Location-specific |

2–3 years |

Moss Landing, CA |

|

New Transmission |

$2.5M–$6M per mile |

Multi-GW regional |

10–20 years |

SunZia (NM-AZ) |

Conclusions

Future demand for electricity is impossible to predict accurately, but seems likely to grow quickly, driven in particular by data centers and AI. We will eventually need a significant upgrade to both generation and transmission. What’s much less clear is when that demand will materialize, where it will land on a continent-sized geography, and, in particular, where it will impact peak loads. This paper argues that there are viable pathways to meet higher demand in the short and medium term before we have to bring new transmission lines and new generation onstream.

However, such a solution will not arrive on its own. Without significant action across multiple fronts and at substantial scale, the existing grid will come under increasing pressure—and we can expect a massive struggle for access. Regulators will be caught between the sudden growth in demand and political pressure to service existing commercial and residential customers first, while keeping a lid on prices.

Yet, action at scale will be challenging. The grid is fragmented; the seven regional transmission organizations (RTOs) each have their own plans and business models, and must themselves confront multiple state regulators. The Texas grid is essentially independent. FERC is becoming more supportive, but is still moving quite slowly. And every utility makes its own decisions within that regional structure.

Much of the technology base for an effective transition is also relatively new. DLR and reconductoring, for instance, are being resisted, at least ostensibly, in part because some utilities think they are unproven. DOE has a substantial role here in testing and validating these technologies, and in supporting further research and development, but full-scale commercial demonstration is not complete.

There are some significant technical challenges. Digitization underpins nearly all the proposed solutions: DLR sensors, power flow controllers, AI-aware data center scheduling, and VPP aggregations. While these add flexibility, they also expand the attack surface for cyberthreats. Utilities already face thousands of intrusion attempts daily, and adding millions of distributed endpoints creates new vulnerabilities. The North American Electric Reliability Corporation (NERC) has warned that poorly secured Internet of Things devices tied to grid functions could become points of failure. Policymakers must invest in cybersecurity as aggressively as in physical infrastructure.[62]

Absent significant action across multiple fronts and at substantial scale, the existing grid will come under increasing pressure, and we can expect a massive struggle for access.

Utilities and contractors also face a looming labor bottleneck. More than half the current U.S. utility workforce is expected to retire within the next decade.[63] Recent natural disasters have placed huge strains on existing workforces—such as in Puerto Rico and North Carolina. Transmission line workers, protection engineers, and cybersecurity experts are already in short supply. Training and apprenticeship programs are expanding, but not nearly at the pace required. Without a new pipeline of skilled labor, projects risk costly delays.

But by far the biggest problem is the misalignment of incentives for utilities. Fundamentally, utilities in the United States are still regulated monopolies whose job is to provide sufficient reliable electricity for their customers at the lowest possible price (including profits). The doctrine of universal service emerged in that environment, while regulators still approve electricity rates because there is little competition near the end user. For utilities, a larger rate base means higher profits, so cheap capacity is less attractive than expensive capacity. Utilities have also historically also been highly risk averse. They offer a safe investment for reliable returns, so speculative investments are simply not part of the model. Utility executives are well aware of this—and people who crave excitement do not typically become senior utility executives.

Thus, from the perspective of utilities, efforts to manage the transition without new transmission lines and new generation have minimal value. Further, existing wholesale markets are not typically structured to pay for services that avoid congestion and curtailments, so utilities are highly incentivized to address the transition by building new assets, and markets have limited mechanisms for paying for alternatives.

By the mid-2030s, the nation will likely require thousands of miles of new interregional transmission, often connecting to new generation and new end users. But the choice is not between new lines or no lines. It is between a brittle, overbuilt system and a layered, resilient grid that uses every tool at its disposal. Flexibility—via data centers, EVs, storage, efficiency, GETs, and demand response—buys the time needed to put steel in the ground. It can, in the meantime, avoid an unnecessary and potentially disastrous conflict between different electricity users.

The projected growth of peak demand is therefore both a blessing and a curse. It is a curse because the grid must be sized and managed to meet peak demand, which implies investments in the hundreds of billions of dollars, many potentially painful moments when existing capacity is not sufficient, and wasted capacity most of the time. But it is also a blessing, because that wasted capacity can be accessed using tools on both the demand and the supply sides of the energy equation, allowing us to build a more efficient grid for much less money and acting as a bridge to a more electrified future. The crisis is real, but so is the opportunity. America has the technologies, the policy tools, and the capital. What remains is the will to treat flexibility not as a niche, but as the backbone of the 21st-century grid.

Recommendations

The capacity of the current electricity grid will need to expand, probably substantially, in the coming years. The administration appears to believe that the federal government should not be directly funding this expansion, and has sought to cut $15 billion previously allocated for that purpose, although it has also claimed that more loans will partly replace the cuts. Regardless of the administration’s plans, if demand materializes as current models suggest, we are heading into a crunch: new generation and new transmission cannot come on stream fast enough to meet projected needs. The following recommendations are focused on addressing that crunch by closing the short- and medium-term gaps between supply and demand.

The crisis is real, but so is the opportunity. America has the technologies, the policy tools, and the capital. What remains is the will to treat flexibility not as a niche, but as the backbone of the 21st-century grid.

Many of these recommendations are regulatory, designed to unleash the options described in this paper. Currently, regulations are not set up to do so. And the need is urgent, so Congress and the administration should be pushing FERC hard to adopt a pro-flexibility mindset and to use all the tools at its disposal to accelerate the transition. But both DOE and the data centers themselves will be important players, and should be taking steps to create and normalize the necessary flexibility.

Further, while the grid will undoubtedly need new generation, plenty of under-utilized capacity is locked away by insufficient transmission capacity. The first short- and medium-term fix is therefore to address that problem. And that will take action from FERC, DOE, and the data centers themselves.

FERC: Actions to Accelerate Adoption of Alternatives to New Transmission Lines

For NWA alternatives to deploy at scale and on time, FERC needs to move into an accelerationist mindset. The default option must be deployment of cost-effective technologies that enhance capacity of the existing grid. FERC can make that happen by taking the following actions:

▪ Correct incentives so that utilities get paid fairly for software, sensors, and modular hardware, and that utility incentives for building new assets vs. increasing efficiency balance appropriately

▪ Require both long-term and near-term planning to include GETs as a standard option

▪ Ensure that markets and operating procedures actually use the extra capacity GETs unlock

▪ Build the data capabilities and standards that will be needed to make flexibility happen at scale

Recent rule makings represent progress. But a lot remains to be done. Today, slack selection standards, misaligned incentives, and ineffective real-time capacity utilization mean that NWAs are just an afterthought in utility planning.[64]

Correcting the Capital Bias

This is the heart of the NWA adoption problem. Traditional cost-of-service regulation favors rate-base steel and wires over software and sensors—the effect described in the well-known Averch-Johnson paper, which shows that regulated companies engage in excessive capital accumulation to expand profits.[65] Grid regulators in the United States typically set the price of electricity to include a profit for utilities as a percentage of their fixed assets; this drives utilities to expand the rate base—the assets under their control. In contrast, making those assets more productive may generate no new revenue, and no additional profit. In some cases, the impact may even reduce revenues. Utilities would much prefer to build expensive new capacity. That’s why FERC has approved over $53 billion in transmission investment across 123 projects since 2006.[66]

Perhaps the most important single reform on the menu for FERC is to adopt a uniform, technology-neutral mechanism for sharing the savings that can be unlocked by non-wires alternatives to transmission. For example, wherever new technology verifiably reduces congestion, the transmission owner should earn a share of measured savings, with the remainder flowing to customers. Federal lawmakers recently reintroduced the Advancing GETs Act in January 2025, specifically requiring FERC to establish shared savings incentives for GETs.[67]

Perhaps the most important single reform on the menu for FERC is to adopt a uniform, technology-neutral mechanism for sharing the savings that can be unlocked by non-wires alternatives to transmission.

Some utilities such as National Grid support revenue sharing. It reports that dynamic line ratings show that available transmission capacity is greater than static ratings 94–97 percent of the time, with an average increase of 47 percent in line capacity. This is concrete evidence of achievable benefits that shared savings mechanisms could unlock.[68]

FERC should also ensure that transmission owners face no systemic incentive bias between GETs and wires. That means ensuring that appropriate GET investments (including software, sensors, and modular power-flow hardware) are capitalized as regulatory assets to provide a return on these investments. FERC has authority to make these changes under §219 of the Federal Power Act (FPA), but it never finalized the March 2020 Notice of Proposed Rulemaking (“2020 NOPR”) that would have provided up to a 1 percent return on equity for transmission technologies that enhanced reliability, efficiency, and capacity. Once those requirements are in place, it will be possible to determine the amount of return that will fully incentivize adoption by utilities.[69]

FERC should also ensure that utilities can make money quickly and effectively on these new grid-expanding technologies, so the cost-recovery process needs to be improved. A fast-track FPA §205 filing template for would help with GETs, and there is a precedent for this: a 2023 FERC order allows utilities to include cybersecurity expenses in the rate base.[70]

Planning Reforms

A key step in grid management is planning for upgrades. Currently, GETs are still largely shut out of that process, but FERC can help. So far, it has taken baby steps.

FERC Order No. 1920 requires regional grid managers to consider alternative transmission technologies—explicitly including GETs—during long-term planning. That’s not enough. FERC should require selection of these alternatives whenever they meet reliability/operational needs at lower cost or a superior “time-to-benefit” than conventional transmission construction does.[71]

The same order requires transmission providers to evaluate cost-effective solutions using seven specific benefit categories over a 20-year planning horizon. However, that also leaves too much discretion; evaluation doesn’t necessarily lead to action, and utilities can easily dismiss GETs in favor of capital-intensive alternatives that provide better returns under traditional rate-of-return regulation.[72]

FERC should require selection of alternatives whenever they meet reliability/operational needs at lower cost or a superior “time-to-benefit” than conventional transmission construction does.

GETs can be rolled out much faster than transmission lines, so FERC should require transmission providers to include a “GETs first” step in near-term reliability planning and in economic/congestion analysis. It could, for example, insist that a GETs package be evaluated for any transmission constraint that occurs more than 250 hours/year, or causes at least $10 million/year in congestion costs, and that it should be adopted when it is the best cost-benefit solution. That aligns with DOE guidance showing that GETs can deliver capacity quickly.[73]

The cluster studies and affected-system analyses that underpin grid upgrades should test GET options before accepting costly, time-consuming network upgrades.[74] Order No. 2023 already requires that transmission providers evaluate alternative transmission technologies in their cluster studies.[75] But FERC could instruct Regional Transmission Organizations (RTOs) and Independent System Operators (ISOs) to make a GET solution the default remedy when it solves the identified constraint for at least the study time horizon with equal or better reliability and time to deployment—with appropriate cost allocation and measurement and verification (M&V).

Operations and Markets

Line ratings are still not measured dynamically, so FERC needs to act now. Order No. 881 mandates AARs and seasonal ratings (i.e., ratings that show the maximum safe capacity of a transmission line must consider seasonal shifts). This is again a positive baby step, but it’s not enough. Dynamic line ratings use sensors to monitor line conditions in real time, and can therefore unlock substantial capacity, but deployment is minimal.[76]

In 2024, FERC opened an advance notice for DLR using sensors and software to monitor wind/solar.[77] FERC should now propose a rule that (i) requires DLR on persistently congested lines above defined thresholds, (ii) mandates day-ahead forecasted line ratings (i.e., line capacity) in market models, and (iii) sets interoperability/data standards for multi-utility coordination. These could unlock the extensive capacity that DLR can generate on congested lines.

This additional capacity needs to be paid for. FERC should direct RTOs/ISOs to file a tariffed product that pays for verified incremental thermal capacity (from DLR, Advanced Power Flow Control, topology optimization, or advanced reconductoring staging) during defined intervals. Payments could be based on measured ratings increases and congestion cost reductions, analogous to how electricity markets compensate reserves and fast-ramping capability today. DOE and National Labs already provide M&V scaffolding for this.[78]

Where DERs, also known as VPPs, can address local reliability problems or congestion, FERC should also require grid operators to use these capabilities to provide targeted relief as an alternative to a near-term wires upgrade (under clear deliverability and telemetry rules). This approach ties GET deployment and distribution-side flexibility together in market operations.[79]

Cross-Cutting Support: Data, M&V, and Compliance

FERC and DOE can collectively provide a critically important technical base for GET rollout by publishing a FERC-approved M&V manual for GETs. This would include ratings telemetry, device performance baselines, topology action logging, and congestion-savings attribution. That manual should be required for cost recovery, shared-savings settlements, and selection in Order No. 1920 portfolios. DOE, Idaho National Laboratory, and the Electricity Systems Integration Group have already provided a head start; FERC can lock in a common template.[80]

FERC and DOE can collectively provide a critically important technical base for GET rollout by publishing a FERC-approved M&V manual for GETs.

Part of the problem with current grid-related decisions is insufficient transparency, which is necessary to promote equitable competition between GETs and new lines, and within these categories as well. Order No. 881 already requires line ratings data to be shared; FERC should extend this with a uniform, machine-readable public feed of historical/forecast line ratings, binding constraints, and operator actions (with appropriate security redactions). Better transparency helps developers and consumer advocates validate that GETs were genuinely assessed and used wherever they are the best solution.[81]

Finally, FERC needs to get a lot more serious about GETs-related enforcement. It should announce in advance that a failure to 1) evaluate GETs against quantitative selection thresholds, 2) integrate forecasted ratings/topology in models, or 3) implement cost-effective GET solutions will trigger a §206 investigation for unjust and unreasonable rates. This would force large rebuilds to show that GETs were evaluated and—wherever they are cheaper/faster—adopted.

Accelerating FERC-driven reform is highly desirable and entirely possible. New demand on the grid will not wait for the often cumbersome and time-consuming procedures that have been standard at FERC. We believe that rollout of GETs across the grid could be transformed by FERC within 36 months. The roadmap in appendix A offers one pathway toward implementation.

The regulatory foundation exists. The technology works. The only piece is regulatory and political urgency to make GETs the default choice for addressing transmission constraints.

NEPA Reform (2024–2025)

Reform of the National Environmental Policy Act (NEPA) has been a top priority in the energy world for at least a decade. In response, DOE and the White House Council on Environmental Quality (CEQ) have issued reforms, setting two-year deadlines for environmental impact statements and one-year deadlines for environmental assessments. The proposals also accelerate categorical exclusions for low-impact projects, including solar storage, EV charging infrastructure, and transmission improvements, and encourages shared information across agencies to reduce repetitive analysis.[82] President Trump has added to Biden’s NEPA deregulation in his “Unleashing American Energy” executive order, which directs the CEQ to remove NEPA regulations from the Code of Federal Regulations. Agencies are still bound to complete environmental reviews under agency rules and legal precedent; however, there is now no overarching federal NEPA framework.[83]

Given that GETS affects only the existing transmission lines, and has no impact on the environment, all GETS deployment should be fully excluded from NEPA review.

DOE

DOE will play a substantial role in grid modernization. It can support development of critically important new technologies, as well as the rollout of comprehensive gird modernization. In general, we support the shift toward loans rather than grants, as doing so will enhance the efficiency of grid modernization programs by bringing market discipline more fully to bear, while still encouraging nationally strategic modernization. We also, however, believe that other important functions will require that the federal budget bear some burden to allow DOE to continue and expand existing work expanding the grid.

▪ Transmission Facilitation Program (TPF). The $2.5 billion in revolving fund loans funded through the Infrastructure Investment and Jobs Act have now been fully allocated. And while the Trump Administration may well seek to redirect priorities for funding, it would be a mistake to end this program. Indeed, more generally, we support the use of government loan authorities for infrastructure development and deployment. The administration should consider expanding the TPF, perhaps substantially, and ensuring that demonstration funding for new transmission technologies is part of the package.

▪ Grid Resilience and Innovation Partnerships (GRIP). As with TFP, while priorities may change with administrations, GRIP is a critically important support for GETs in particular, and should perhaps be refocused to funding GETs before committing large amounts for more expensive forms of grid modernization. The administration should therefore recommit funding for GRIP.

▪ National Transmission Needs Study (NTNS). NTNS provides data and model underpinning for grid management and planning. The last NTNS was completed in 2023 and will be rerun in 2026. Given that needs are now changing more rapidly, it makes sense to accelerate NTNS studies to make them biennial.

▪ Lab Partnerships. The Grid Modernization Lab Consortium (GMLC) plays a key role in testing and validating new technologies and developing shared models for the grid. It effectively allocates tasks across the National Labs, and has developed useful coordination functions. It is, however, indirectly under threat following proposed substantial cuts to some of the key partners: NREL, for example, will lose more than half its funding under the proposed budget. Budget cuts at the Labs are, in general, mistaken, starving a critical resource for long-term economic growth, but at a minimum, cuts need to be sufficiently granular to protect the Labs’ role in building an expanded and more efficient grid.

▪ DOE Offices. The sharp cuts to the Office of Electricity in particular are ill-advised. The savings made will be heavily outweighed by reduced state capacity in a critical area. The Loan Program Office should be strengthened and redirected to ensure that loan funding is available to encourage (not replace) sector investment in grid modernization, and especially GETs.[84]

Overall, ensuring that DOE and the National Labs can do the work that’s needed to accelerate grid modernization should be among the highest priorities of the administration and Congress.

Data Center Activity

Data centers will need to be connected to the grid in most cases, even if they rely primarily on energy sources deployed behind the meter. But data center loads on the grid, especially at peak times, can be flexible enough that most of the apparent conflict between data centers and other users for scarce energy can be avoided. The Nicholas Center report concludes that extremely modest curtailment of demand from data centers during peak periods will be enough to de-stress the grid, potentially generating 75 terawatt hours (TWh) of peak capacity annually. That’s enough to ensure that the grid’s commitment to satisfy peak demand can be met without immediately building new energy sources and new transmission lines, even though these will clearly be needed if demand continues to grow as expected.

Data centers can develop and share a model of best practices, which should become industry standard.

The key then is to normalize this kind of peak load demand management by data centers. Regulators are concerned that their existing customers will be left either with much higher prices or (worst case) without electricity at all if they simply allow huge new sources of demand to come onto the grid. That, of course, conflicts with the universal service mandate of regulated monopolies, but in the current context, it is a rational concern. It is, however, one that the data centers themselves can substantially address.

Data centers can develop and share a model of best practices, which should become industry standard. It would include commitments to unload demand from the grid during peak periods. The data centers themselves should include this in their operational planning, developing the capability to shunt non-real-time demand to off-peak hours or onto other currently off-peak geographies (e.g., from the West Coast at 8 p.m. to the East Coast where it is 11 p.m. and demand is winding down). Poor East-West interconnection means that West Coast utilities cannot draw on East Coast electricity resources, but data centers can reallocate work without needing to reallocate electrons via interconnection. That would allow data centers and utilities to formulate connection agreements that support the grid rather than threatening it, and would even allow backup capacity (e.g., from batteries) at the data centers to be used by the grid in some circumstances.

These arrangements must become industry standard, and that will be driven by the biggest owners of data centers in conjunction with government support. Testing and validation can be provided with help from FERC, DOE, and EPRI. And while it is tempting to keep such operating arrangements private, both the United States and the data center owners in general will benefit as the effectiveness of data centers in managing peak demand is more widely understood. DOE might consider offering some financial incentives to encourage publication of results from demonstration and pilot projects.

Using supply and demand tools to manage peak loads in the coming years offers a bridge across the transition to a much-expanded grid with much more generation and transmission.

Finally, it is hugely in the interests of data centers to take this path and become active partners in managing peak demand on the grid. It’s true that under universal service doctrine, they should simply be permitted to buy whatever electricity they need. But if they try to force an extensive and immediate expansion of peak load demand, they will inevitably face long delays as regulators struggle to balance the needs of old and new customers, and as utilities push for expensive new upgrades that take many years to approve and deploy. Taking the initiative and addressing peak load demand directly by managing their own demand in conjunction with real-time signals from the grid will avoid most of these problems and, more importantly, allow much faster grid connections, as the recent CapFlex program at Dominion Energy shows.[85] Implementing GETs through regulatory reform can do the rest to bridge the period before new energy sources and transmission lines can be deployed.

Using supply and demand tools to manage peak loads in the coming years offers a bridge across the transition to a much-expanded grid with much more generation and transmission. That bridge can support the rapid expansion of data centers quickly and efficiently, without damaging either their interests and customers or the utilities and their existing customer base.

These are necessary and effective short-term solutions. But in the end, the United States must build physical capacity to avoid electricity as a constraint. Today, the United Kingdom has the highest energy prices in the Organization for Economic Cooperation and Development (OECD), in large part because they have failed to build the transmission that connects generation (in the North) to demand (in the South). The United States cannot afford to make the same mistake.

Appendix A: A Roadmap for FERC

The approach outlined herein uses authorities already available to FERC. Order No. 1920 puts GETs on the planning table; Order 2023/2023-A lets planners trade network upgrades for smarter fixes; Order No. 881/881-A upgrades ratings fidelity; Order No. 1977/1977-A ensures new long-distance lines move when they must.[86] But without cost-recovery parity, shared-savings incentives, and model/market rules that value real-time thermal capacity, GETs will remain an afterthought.

Up to 12 months (use live dockets):

▪ In Order No. 1920 compliance cases, require “select-if-cost-effective” language for GETs and reconductoring, with explicit screening thresholds and portfolio M&V.

▪ In Order No. 2023/2023-A compliance cases, require GETs-first remedies for cluster constraints and affected-system upgrades wherever they are cost effective. Insist that utilities show their work in assessing options.

▪ Issue a DLR NOPR that builds on the 2024 NOPR, which would require DLR on persistently congested lines, along with day-ahead forecasts.

▪ Finalize the 2020 Transmission Incentive NOPR to provide the regulatory certainty that utilities require for GETs investments. The proposed 1 percent return on equity incentive should be implemented immediately; and FERC should monitor take-up to ensure that this is enough to promote action.[87]

12–36 months (lock in operations):

▪ Approve RTO/ISO tariff filings that create a thermal-capacity product, and require use of forecasted ratings in dispatch and unit-commitment engines.

▪ Complete a FERC M&V manual and condition incentive recovery in tariff filings on compliance.

▪ Implement Shared Savings Mandates as proposed in the Advancing GETs Act, allowing utilities to share in quantified customer benefits from GET deployment.[88]

36 or more months (normalize the practice):

▪ Revisit incentives to calibrate shared-savings rates and to sunset some initial additional incentives once GETs become business-as-usual.

▪ Create independent transmission technology monitors to ensure that regional operators comply with GET evaluation mandates, and to identify opportunities for deployment.[89]

▪ Use periodic audits of ratings/topology data to verify that operators consistently deploy GETs under stress conditions.

Appendix B: Comparing costs

Dynamic line ratings (DLR)[90]

▪ Cost: $5,000–$20,000 per mile for sensor installation

▪ Capacity gain: 10–30 percent on average, up to 40 percent in windy conditions

▪ Deployment time: Months

▪ Comparison: Equivalent to adding hundreds of MW across congested regions for pennies on the dollar compared to new transmission

Reconductoring with advanced conductors[91]

▪ Cost: About one-third of new transmission lines on a per MW-mile basis

▪ Capacity gain: Doubles or triples line capacity

▪ Deployment time: 1–3 years

▪ Comparison: Best suited for existing congested corridors where rights-of-way already exist

Power flow controls and topology optimization[92]

▪ Cost: Less than $50/kW of unlocked capacity

▪ Capacity gain: Up to gigawatts at the system level

▪ Deployment time: Months to a year

▪ Comparison: One of the fastest-to-market solutions, but requires sophisticated grid management

Efficiency and NWAs[93]

▪ Cost: Highly variable, but BQDM delivered 52 MW for $200 million—about $3,800/kW

▪ Capacity gain: Feeder-level reductions of 1–4 percent typical

▪ Deployment time: 1–3 years

▪ Comparison: Best for urban load pockets where traditional infrastructure is expensive

Data center flexibility[94]

▪ Cost: Near zero marginal cost—software scheduling and contracts drive flexibility

▪ Capacity gain: 10–40 percent of workloads (non-real-time) shiftable; tens of gigawatts nationwide

▪ Deployment time: Immediate once contracts and software are in place

▪ Comparison: A uniquely scalable solution if regulators value flexibility as capacity

Storage as virtual transmission[95]

▪ Cost: ~$1,000/kW for lithium-ion today, falling below $500/kW by 2035

▪ Capacity Gain: Location-specific; can defer billions in transmission upgrades

▪ Deployment time: 2–3 years

▪ Comparison: Ideal for bridging gaps while transmission lags behind

New transmission[96]

▪ Cost: $2.5 million–$6 million per mile

▪ Capacity gain: Gigawatts, scalable inter-regionally

▪ Deployment time: 10–20 years, with major permitting risk

▪ Comparison: Indispensable long term, but not a near-term capacity solution

About the Author

Dr. Robin Gaster is research director at ITIF’s Center for Clean Energy Innovation, and president of Incumetrics Inc.,. Dr. Gaster’s primary interests lie in climate, economic innovation policy, metrics, and innovation assessment. He has worked extensively on climate, innovation and small business, and regional economic development.

About ITIF

The Information Technology and Innovation Foundation (ITIF) is an independent 501(c)(3) nonprofit, nonpartisan research and educational institute that has been recognized repeatedly as the world’s leading think tank for science and technology policy. Its mission is to formulate, evaluate, and promote policy solutions that accelerate innovation and boost productivity to spur growth, opportunity, and progress. For more information, visit itif.org/about.

Endnotes

[1]. Data Center Watch, “$64 billion of data center projects have been blocked or delayed amid local opposition,” accessed October 14, 2025, https://www.datacenterwatch.org/report.

[2]. U.S. Energy Information Administration. “EIA Publishes Its First Energy-Sector Forecasts Through 2026,” press release, January 15, 2025, https://www.eia.gov/pressroom/releases/press564.php.