No, Monopoly Has Not Grown

Alarmists say the economy is experiencing a crisis of market concentration, with dominant players stifling competition in industry after industry. That is the pretext for a push to radically restructure antitrust policy—but newly released Census data largely contradict the claim.

KEY TAKEAWAYS

Key Takeaways

Contents

The New Truism: Monopoly Is Rampant 3

Census Bureau Concentration Data. 4

Changes in Concentration: 2002–2017. 7

Highly Concentrated Industries 10

Advanced Technology Industries 12

Concentration and Profitability 15

Why the Divergence of Views? 16

Introduction

Over the past several years, many scholars, activists, pundits, and policymakers have asserted that market concentration has risen across the U.S. economy, leading to a decline in competition. The culprit, they claim, is poorly crafted antitrust laws and lax enforcement, which have allowed firms to grow excessively through mergers. Increased concentration in turn is blamed for several economic and social ills, including slow productivity growth, excess profits, stagnant wages, and business political power. These claims have underpinned calls for a radical restructuring of antitrust policy, including imposing much stricter limits on mergers and breaking up leading companies.[1]

Newly released data on concentration ratios from the U.S. Census Bureau’s 2017 Economic Census provides a way to assess claims about increasing concentration by comparing it to 2002 data. The U.S. Census Bureau released the concentration of largest firms for 2017 on December 3, 2020.[2] The data largely rebuts these claims:

▪ Just 35 of 851 industries (4 percent) were highly concentrated, with the top-4 firms (the C4 concentration ratio) holding more than 80 percent of the market.

▪ In 2017, 80 percent of U.S. business output was from industries with low levels of concentration, with that share increasing from 62 percent in 2002.

▪ Fifty-five percent of industries increased concentration between 2002 and 2017; 45 percent decreased.

▪ The average C4 ratio increased by just 1 percentage point between 2002 and 2017, from 34.3 percent to 35.3 percent, while the average C8 ratio increased even less, from 44.1 percent to 44.7 percent.

▪ There was a slight negative correlation between the C4 level in 2002 and the percentage point change in C4 between 2002 and 2017.

▪ Among the industries with increases in concentration, only one-third increased by greater than 10 percentage points.

▪ Of the 20 industries showing the greatest increase in the C4 ratio from 2002 to 2017, only 30 percent had C4 ratios above 80 percent in 2017.

▪ Of the 115 industries with a C4 ratio of 60 percent or more in 2002, the majority got less concentrated, with the average C4 declining 4 percentage points.

▪ For every advanced technology industry with a C4 ratio over 80 percent, there were 10 with a C4 ratio below 50 percent.

▪ Producer prices rose less from 2002 to 2017 in industries with higher levels of concentration than overall prices.

In short, to paraphrase Mark Twain, the reports of the death of competition are greatly exaggerated.

The New Truism: Monopoly Is Rampant

The “fact” of rising concentration, and even monopoly, has been picked up and commented on by a larger number of pundits and commentators. Brookings’ analyst David Wessel wrote, “There’s no question that most industries are becoming more concentrated. Big firms account for higher shares of industry revenue and are reaping historically large profits relative to their investment.”[3]The Economist concluded that two-thirds of the economy’s roughly 900 industries had become more concentrated between 1997 and 2012.[4] Former chairman of the Council of Economic Advisors Jason Furman testified that market concentration has increased since 1997.[5]

Paul Krugman wrote that “growing monopoly power is a big problem for the U.S. economy.”[6] New York Times columnist Eduardo Porter stated, “There is plenty of evidence that corporate concentration is on the rise.”[7] Economist Joe Stiglitz wrote that a “deeper and more fundamental problem is the growing concentration of market power.”[8] The neo-Brandeisian advocacy group Open Markets has referred to “America’s concentration crisis.”[9] And the Center for American Progress has written about “America’s monopoly problem.”[10]

These claims have motivated hearings and potential legislation to reform antitrust. Senator Amy Klobuchar (D-MN), chairwoman of the Senate Subcommittee on Competition Policy, Antitrust, and Consumer Rights, wrote, “We are seeing higher levels of market concentration across our economy, partially driven by waves of corporate consolidation.”[11] Congressman David Cicilline (D-RI), chairman of the House Antitrust Subcommittee, has warned that America has a “monopoly problem.”[12] Lina Khan, who has been nominated by the Biden Administration to serve as an FTC commissioner, has alleged that the United States faces a “sweeping market power problem” as a result of relaxing antitrust law.[13]

It has become an article of faith that concentration has increased to problematic levels and that this supports wholesale and even radical changes in U.S. antitrust policy.

The Biden-Sanders unity task force released a list of recommendations in August 2020. They proposed a “Tackling Runaway Corporate Concentration,” which emphasized,

Democrats are concerned about the increase in mega-mergers and corporate concentration across a wide range of industries, from hospitals and pharmaceutical companies to agribusiness and retail chains. We will direct federal regulators to review a subset of the mergers and acquisitions that have taken place since President Trump took office, prioritizing the pharmaceutical, health care, and agricultural industries, to assess whether any have increased market concentration, raised consumer prices, demonstrably harmed workers, increased racial inequality, or reduced competition, and assign appropriate remedies. Democrats will direct regulators to consider potential effects of future mergers on the labor market, on low-income and racially marginalized communities, and on racial equity. And as a last resort, regulators should consider breaking up corporations if they find they are using their market power to engage in anti-competitive activities.[14]

In other words, it has become an article of faith that concentration has increased to problematic levels and that this supports wholesale and even radical changes in U.S. antitrust policy. Former member of the Council of Economic Advisors under President Obama, Carl Shapiro, summed up this view in 2017:

Somehow, over the past two years, the notion that there has been a substantial and widespread decline in competition throughout the American economy has taken root in the popular press. In some circles, this is now the conventional wisdom, the starting point for policy analysis rather than a bold hypothesis that needs to be tested.[15]

This report tests that hypothesis with Census Bureau data.

Census Bureau Concentration Data

One way to test this hypothesis is with data. Some scholars have tried to evaluate whether concentration has risen.[16] However, antitrust experts question the basics from many of these analyses, because definitions of the relevant market are debatable.[17] To be fair, it is difficult to measure market power. Competition can differ at national and local levels.[18] Imports have to be considered, which will lower measured concentration in many traded sectors. Potential entry, including from disruptive technologies, also needs to be factored in. And firms can compete with each other even if they are in different industries as defined by the federal government. As such, antitrust law has stressed for the last 40 years that concentration ratios (the share of sales in a particular industry accounted for by a certain number of firms) can never substitute for the detailed economic analysis of specific markets.[19]

Nonetheless, concentration ratios are a foundational set of data that can be used to look at the overall economy-wide state of and change in concentration and competition. The most common measure is from the U.S. Census Bureau, which as part of its quinquennial economic census releases sales data for the 6-digit NAICS industries (e.g., NAICS code 332913 Residential electric lighting fixture manufacturing) consisting of over 850 industries and details the share of sales of firms accounted for by the top 4, 8, 20, and 50 firms in the industry (known as the C4, C8, C20, etc. ratio).

Our choice of granular industry classification (6-digit NAICS industries) is not random. The more detailed the industry classification for market power analysis, the better. For example, using 3-digit or 4-digit NAICS codes, which many have done, is questionable, as it is difficult to argue that a toaster (NAICS code 335210 Small Electrical Appliance Manufacturing) competes with an oven (NAICS 335220 Major Household Appliance Manufacturing), since both goods are classified in the same 4-digit NAICS code (3352 Household Appliance Manufacturing). Examples of 4-digit versus 6-digit NAICS codes are abundant (e.g., NAICS 333241 Food Product Machinery Manufacturing and 333242 Semiconductor Machinery Manufacturing are both in 3332 Industrial Machinery Manufacturing). Analyzing at the 3-digit level of NAICS code is even more problematic, as it is not imaginable that Animal Food Manufacturing (NAICS code 3111) competes with Dairy Product Manufacturing (NAICS 3115) if the relevant market considered is Food Manufacturing (NAICS 311).

Another challenge to an accurate assessment is what to measure, or absolute share numbers of change. Those that claim that monopoly (a misused term, since it implies one firm controls virtually all of a given market) has become a problem simply measure the number of industries with rising concentration. Take an industry wherein the C4 ratio in the base year is 8 percent (each of the top 4 firms has an average of 2 percent of the market). In the most current year, it rises to 12 percent. Now, while the industry has become more concentrated, the top 4 firms average just 3 percent of the market—far from market power.

Yet, those who want to paint a story of a dangerous growth in monopoly do not bother to mention that increases from a low level to another low level are meaningless from a concentration perspective. For instance, Grullon et al. cited the rise of concentration in Furniture and Home Furnishings retailers (NAICS code 442) within the four largest players as an alarming warning because their share increased 200 percent from 1997 to 2012, yet the concentration went from 6.5 percent to just 19.4 percent.[20] In other words, on average, the top four firms had less than 5 percent of the market each. The real issue is not whether industries are becoming more concentrated; it is whether industries are moving from being unconcentrated to concentrated.

Comparing sectors in one period to the next using Census data requires harmonizing the 6-digit NAICS codes over time, as there is always a change in the classification from one Census to another. Using the concordance available at the U.S. Census Bureau between two immediate Census years, the Information Technology and Information Foundation (ITIF) created a concordance between 2002 and 2017. For example, the industry classification for Internet Publishing and Broadcasting and Web Search Portals (NAICS code 519130) in 2017 included two industries considered in 2002: Internet Publishing and Broadcasting (NAICS code 516110) and Web Search Portals (NAICS code 518112). To combine these two industries in 2002 into one, ITIF used the weighted average of the concentration ratio using total revenue.

An additional challenge is that while Census includes all domestic producers, it does not include imports, which take market share from domestic producers. This overstates concentration ratios in most traded goods and services markets and likely overstates the growth because the share of gross domestic product (GDP) imports grew from 13 percent in 2002 to 15 percent in 2017.[21] For example, Covarrubias et al. found that the weighted average C8 ratio for high-import manufacturing industries rose by 6.7 percentage points from 1997 to 2012. However, adjusting for imports reduces the rise to just 1.6 percentage points.[22]

The issue is not whether industries are becoming more concentrated; it is whether industries are moving from being unconcentrated to concentrated.

ITIF examined C4 concentration ratios for 2002 and 2017 at the most detailed 6-digit NAICS code level. A C4 concentration ratio of 50 percent, for example, would mean that the top four firms hold an average of 12.5 percent of the market each. While there is no hard-and-fast definition, generally C4 ratios above 80 percent are considered high in concentration, ratios of 50 to 80 percent medium, and below 50 percent low.[23]

Census collects and reports data on 851 industries for both years. Some industries, such as Construction and Mining, are not listed in one year but are in the other. Some industries do not have sales data because Census does not want to divulge proprietary information.[24] Nevertheless, industries covered in this report represent more than 90 percent of the total private sector output in the United States.[25]

Concentration in 2017

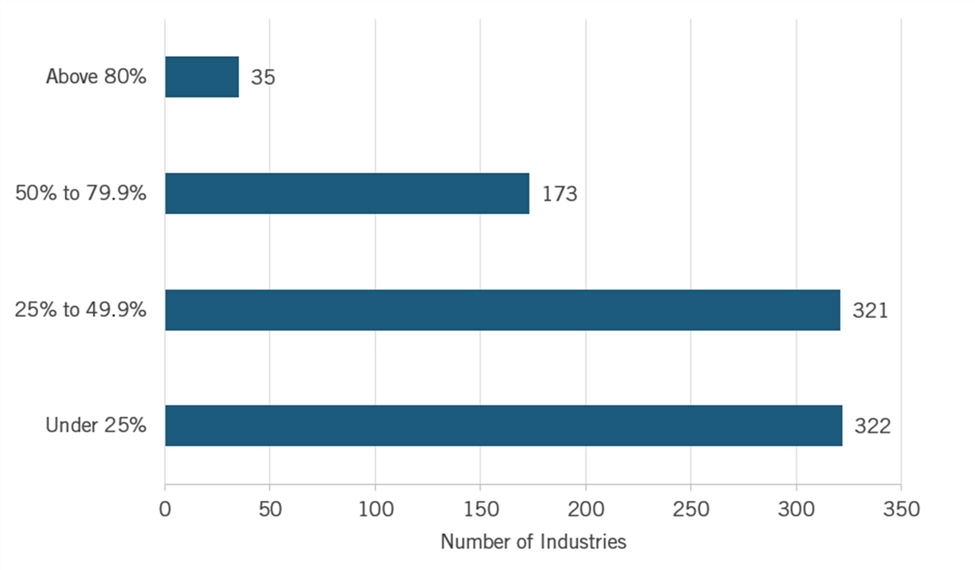

In 2017, 643 industries (76 percent) were unconcentrated with less than a 50 percent C4 ratio (see figure 1). A total of 173 (20 percent) were moderately concentrated with a C4 ratio between 50 percent and 80 percent. And just 35 industries (4 percent) were highly concentrated with a C4 ratio of 80 percent or more. Even at 80 percent, this means the top four firms had only 20 percent of the market share if they split it into equal shares.

Figure 1: Count of C4 concentration in 2017 NAICS codes[26]

Changes in Concentration: 2002–2017

On average, concentration increased only 1 percentage point between 2002 and 2017 after taking the simple average across all industries of the differences between C4 from both years (34.3 percent in C4 from 2002 and 35.3 percent in C4 from 2017). Given that industries with C4 ratios below 50 percent are considered unconcentrated, this is a very low number. The concentration of the eight largest firms (C8) increased even less, from 44.1 to 44.7 percent. Even considering the eight largest firms, the concentration ratio remained lower than 50 percent.

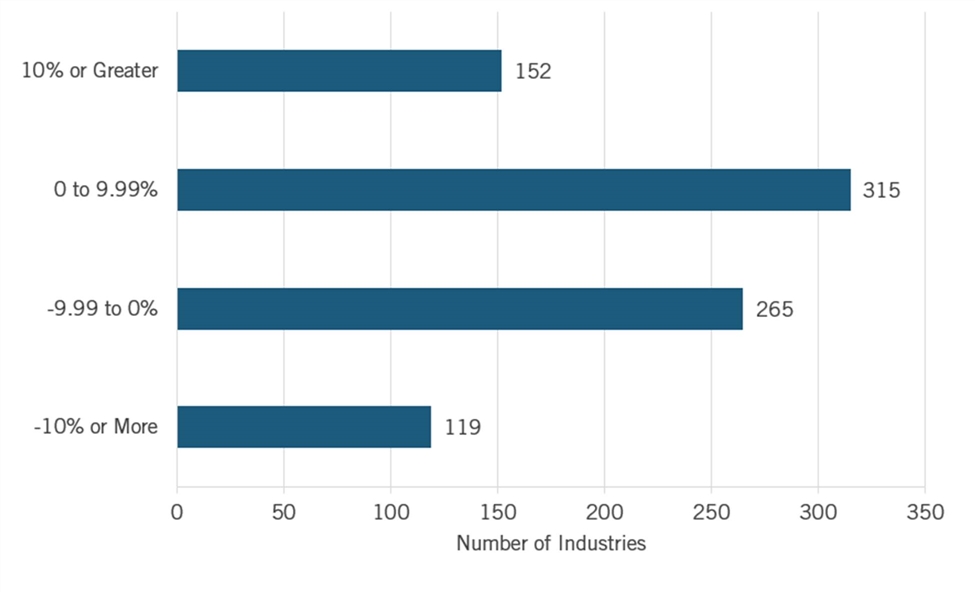

Overall, 467 sectors (55 percent) increased in concentration, while 384 (45 percent) decreased (see figure 2). Again, this is hardly evidence of widespread growth of monopoly. Moreover, among the sectors that saw an increase, only 152 (18 percent of the total) increased by more than 10 percentage points.

Figure 2: Count of percentage-point change in C4 concentration in 6-digit NAICS code industries (2002–2017)[27]

On average more concentrated industries got less concentrated from 2002 to 2017.

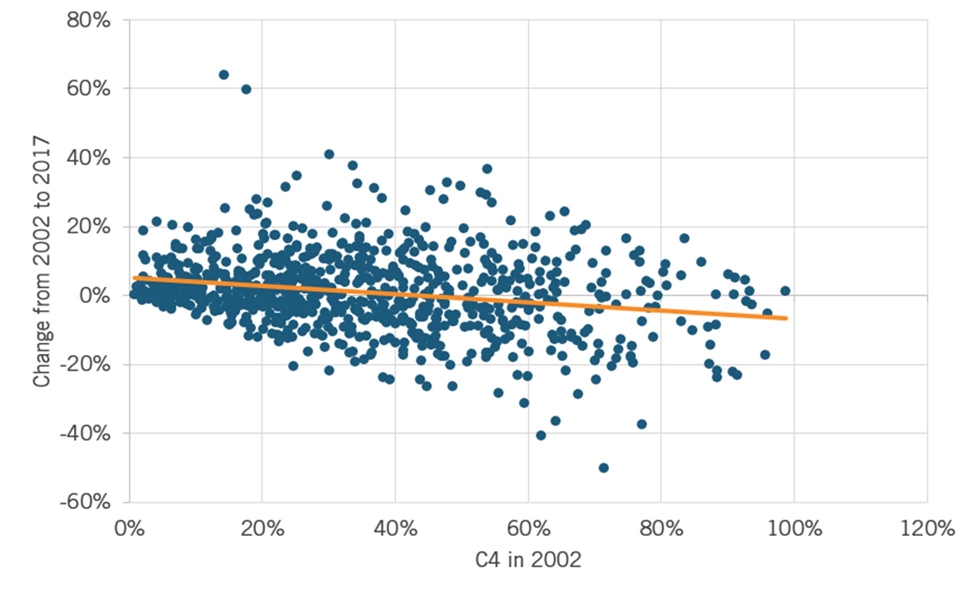

Another way to assess trends in concentration is by looking at whether the increases in C4 ratio were mostly in industries with already high C4 ratios in 2002. In other words, did the concentrated get even more concentrated? Figure 3 presents this relationship, with the y-axis showing the percentage-point change in the C4 from 2002 to 2017, and the x-axis presenting the level of C4 in 2002. The trend line is negative (correlation coefficient of -0.23), indicating that, on average, more concentrated industries got less concentrated from 2002 to 2017. Even the outliers with higher C4 increases were in industries with lower levels of concentration in 2002. With these two outliers removed, the relationship is still negative at the same magnitude (-0.23).

Figure 3: Relationship between C4 ratio in 2002 and percentage-point change in C4 (2002–2017)[28]

If policymakers are concerned about the growth of market power, as opposed to simply the growth in concentration, the key is to examine industries exhibiting higher concentration ratios; in this case, with C4 ratios of 60 percent or higher. Only 94 industries (11 percent) saw an increase in concentration that produced a C4 of 60 percent or more (and even at 60 percent, if each firm held an equal market share, this would mean that each firm had just 15 percent of the market).

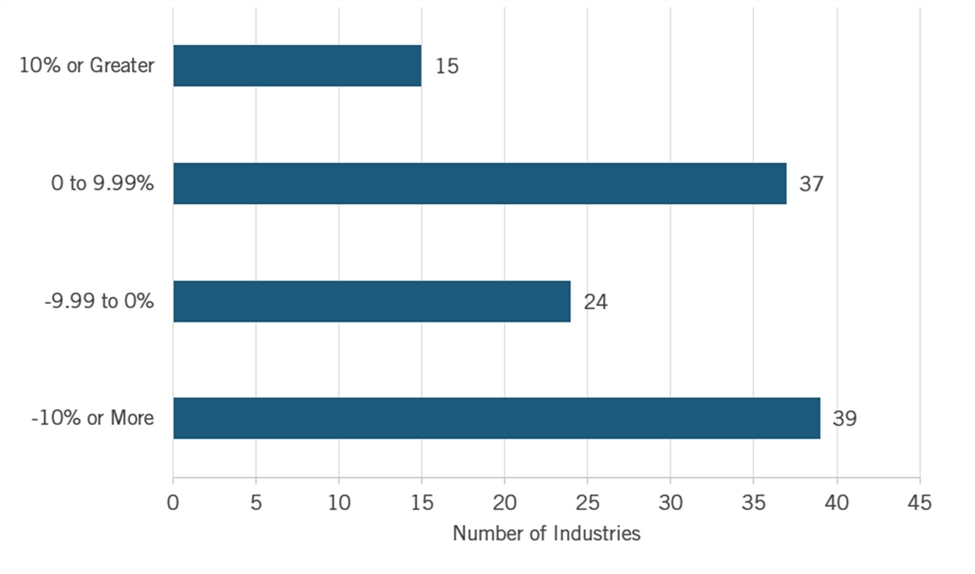

Looking at the 115 industries that had a C4 ratio of at least 60 percent in 2002, 55 percent saw a reduction in concentration ratio (see figure 4). On average, these industries saw a decline of 4 percentage points in their C4 ratio. Thirty-nine industries experienced a reduction of 10 percent or more, and 24 saw a decline of more than 0 percent to 10 percent. In contrast, only 13 percent of the industries showed an increase of more than 10 percentage points. In other words, more sectors with higher C4 ratios in 2002 lost market share than sectors that gained.

Figure 4: Count of percentage-point change in C4 concentration in NAICS codes (2002–2017) for 2002 C4 values greater than 60 percent[29]

Highly Concentrated Industries

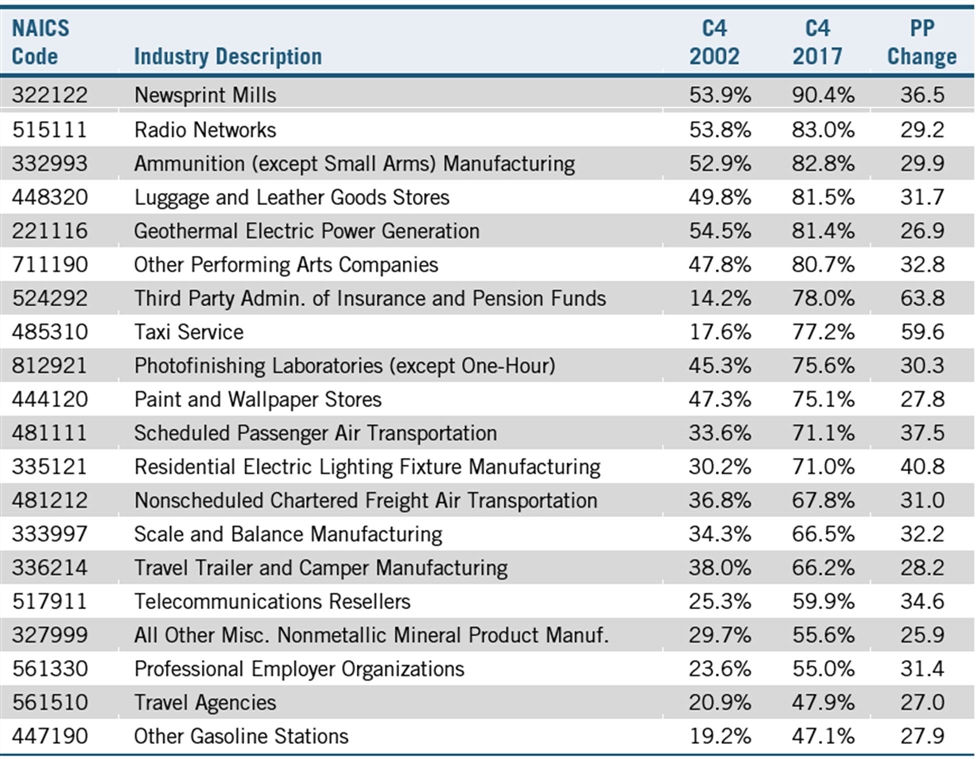

Some industries clearly got less concentrated, while others got more. Table 1 shows the 20 industries with the greatest increases in C4 ratio. Only 30 percent had C4 ratios above 80 percent in 2017. And even for some of them, there was little risk of firms exerting much market power. For example, industries such as other performing arts companies, luggage and leather goods stores, geothermal power generation, and paint and wallpaper stores all face significant competition from firms in other industries such as movie theaters, department stores, and natural gas power generation.

For some other industries, the U.S. trade balance deteriorated, meaning that imports took a larger share and provided more competition.[30] This includes newsprint and electrical lighting manufacturing, in which the United States is the largest importer (importing 20 percent of the total international trade for both industries).[31] For other industries, such as taxi service and travel agencies, the Internet enabled significant economies of scale and cost reductions, such as with the rise of Uber and Lift for taxis and Travelocity and Expedia for travel.

Finally, in a number of industries, technology has created new competitors for these industries. Over-the-air radio stations now compete with satellite radio and smartphones. The dramatic improvement of digital cameras has reduced the market for photofinishing laboratories, likely having caused consolidation as the market shrank.

Table 1: Top 20 industries with the highest percentage-point increase in the C4 ratio from 2002 to 2017[32]

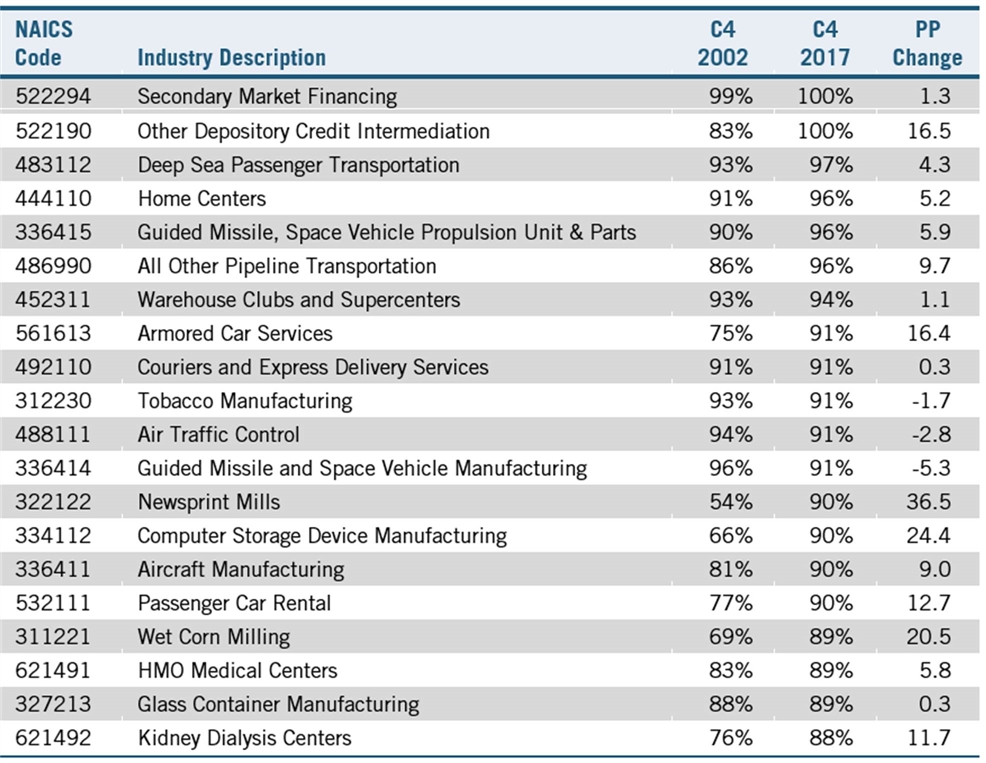

Table 2 lists the 20 industries with the highest concentration ratios in 2017. Fourteen were highly concentrated in 2002, with six joining them by 2017. And of the industries with a C4 ratio above 80 percent, many of them were naturally concentrated. For example, it’s hard to imagine why it would be more optimal for the guided missile and space vehicle industry, computer storage device manufacturing, or aircraft manufacturing to be less concentrated because of the enormous investments needed in research and development (R&D) and production to be successful. Others, such as HMO medical centers and warehouse clubs, and home centers, may be concentrated, but faced competition from other industries (doctors’ offices and other retailers, respectively). Other industries on the list faced technological competition. Passenger car rental faced competition from ride-sharing and also from personal rental companies such as Zip Car.

Table 2: Top 20 industries with the highest C4 ratio in 2017 and their percentage-point change since 2002[33]

There were more unconcentrated tech sectors in 2017 than in 2002.

Advanced Technology Industries

Anti-corporate populists have taken particular aim at technology sectors, claiming that “Big Tech,” particularly the Internet industry, is concentrated. However, the number of advanced technology industries with high levels of concentration is modest (see figure 5). Using the Brookings Institution list of 4-digit NAICS code of advanced technology industries, ITIF constructed a list of advanced technology industries at the 6-digit NAICS code level.[34] Of 135 industries, only 8 have C4 ratios above 80 and 10 times more have C4 ratios below 50. Moreover, there were more unconcentrated tech sectors in 2017 than in 2002. The argument that tech sectors are becoming concentrated does not hold.

Figure 5: Number of 6-digit NAICS code advanced technology industries in C4 concentration ratio groups[35]

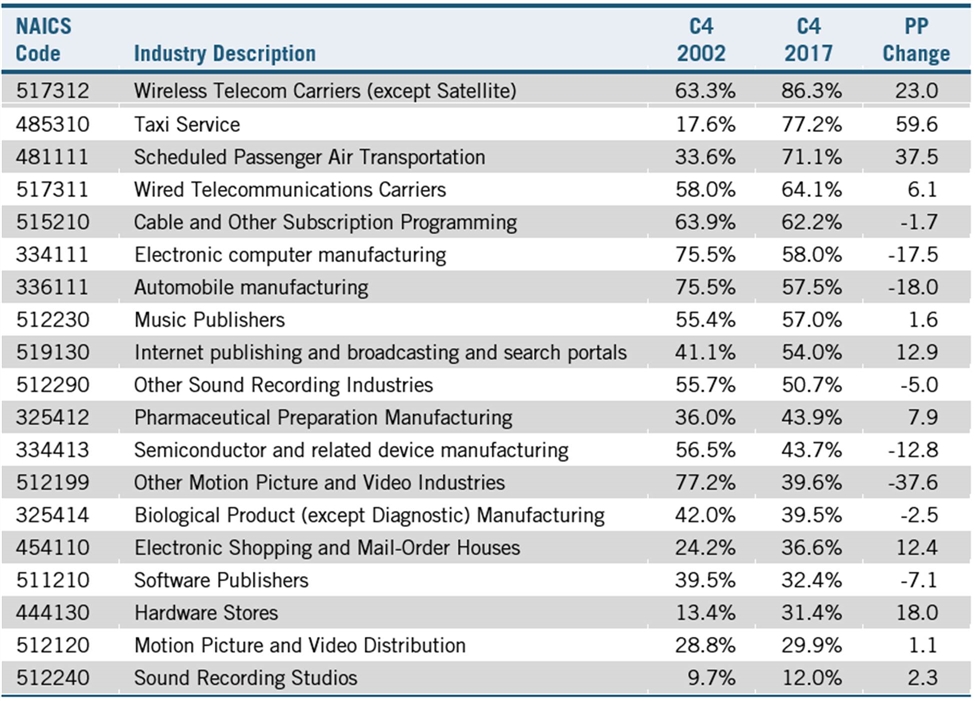

Selected industries, media, and pundits have singled out a number of industries for scrutiny for excess concentration. Table 3 lists some of these industries. In reality, the C4 ratio fell in some, including in automobiles, biotech drugs, computers, and semiconductors in manufacturing; and cable programming, other motion pictures, and software in services.

Some industries, such as motion picture and video distribution and sound recording studios did see increased market share, albeit from low levels to still-low levels. For example, even with the rise of Amazon, the C4 ratio of electronic shopping and mail-order houses increased from 24 percent to just 37 percent.

The C4 ratio for some industries did increase, but by modest amounts, such as for wired telecommunication carriers (58 to 64 percent) and music publishers (55 to 57 percent). Or they increased to modest levels: pharmaceuticals from 36 to 44 percent and hardware stores from 13 percent to 31 percent. The Internet publishing and broadcasting and web search portals industry did increase, but only to 54 percent. Assuming an equal division of the market, the four largest firms would have had just 13.5 percent of the market.

And even in some industries wherein concentration increased and other industries provide little competition, such as scheduled passenger air transportation, the increase in concentration was beneficial. From 1995 to 2016, airline productivity grew four times faster than the overall U.S. economy, and prices rose one-third as fast as the rate of inflation. Investment in capital equipment went up faster than the U.S. average, and profits were below the overall U.S. corporate average.[36]

Likewise, the C4 ratio in the wireless telecommunications industry increased 63 percent to 86 percent. But this has does not appear to have come at the expense of consumer or overall economic welfare. Productivity in the sector grew 84 percent faster than overall non-farm business productivity.[37] The productivity growth rate after the year 2000, when concentration was increasing, was more than three times faster than in the 13 years prior.[38] Moreover, capital investment doubled in inflation-adjusted terms.[39] And according to Bureau of Labor Statistics (BLS) data, nominal prices fell by 31 percent from 2011 to 2020.[40]

Finally, the C4 ratio in the taxi industry increased significantly to relatively high levels, from 18 to 77 percent, but this was presumably because of the entry of car-sharing companies such as Uber and Lyft, where the entry has increased service and held down prices, which led to consumer surplus of $6.8 billion just for all American UberX users in 2015.[41]

Table 3: Selected industries’ percentage-point change in C4 ratio, 2002–2017[42]

Share of Business Output

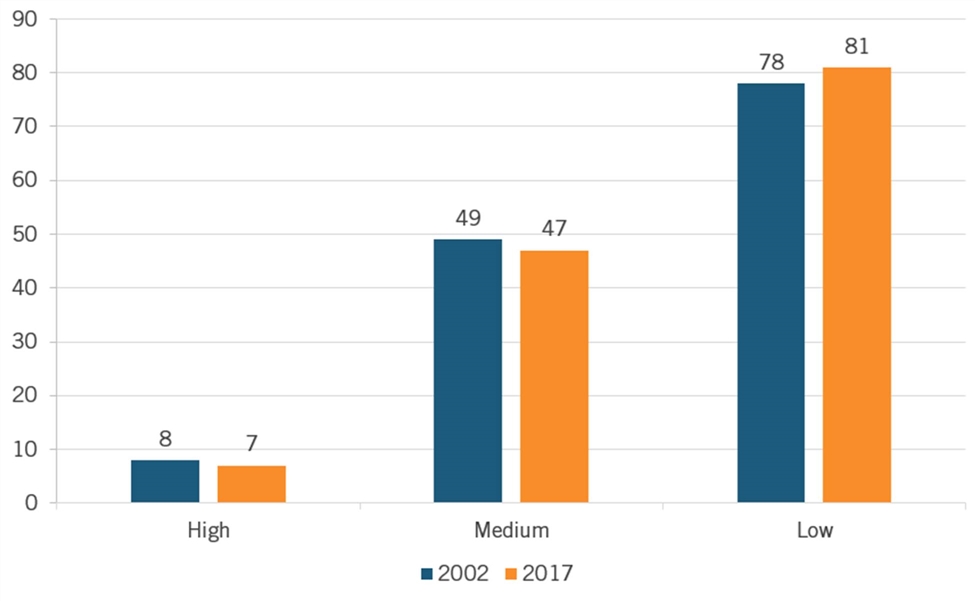

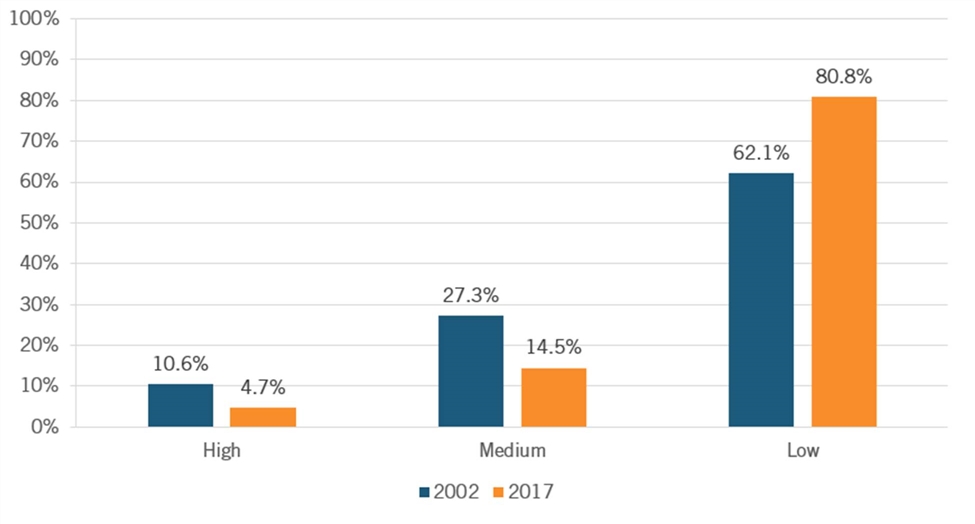

It’s not enough to analyze individual sectors. It is important to also analyze the sectors as a share of the overall economy. To be sure, some sectors are more concentrated. But a key question is what share of the economy these increasing concentration sectors constitute. Figure 6 shows the percentage of sectors with low, medium, and high C4 in business output in 2002 and 2017.[43] Sectors with a low concentration ratio, below 50 percent, had a much higher share in business output than medium (50–80 percent) and high (over 80 percent). Furthermore, low concentration industries became a larger share of the economy. While the low concentration sectors constituted 62 percent of the economy in 2002, by 2017, their share had grown to more than 80 percent. Inverse patterns occurred in medium and high levels of concentration. The share of economic output from highly concentrated industries fell from 10.6 percent in 2002 to 4.7 percent in 2017. In short, the U.S. economy is not becoming monopolistic, filled with giant rapacious firms gobbling up market share. Most of the economy is unconcentrated, and that share has been increasing. But surely the firms in the few concentrated industries must be making rapacious profits. It is to that we now turn.

Figure 6: Percentage change in business output by C4 ratio classification of the U.S. economy[44]

Most of the economy is unconcentrated, and that share has been increasing.

Concentration and Prices

Surely concentration must enable firms to charge higher prices. In fact, of the 36 industries with a C4 ratio of over 70 percent in 2017, and for which there was data available on price changes from the BLS producer price index (PPI), 22 (61 percent) saw price increases from 2002 to 2017 that were lower than the economy-wide PPI. In fact, the correlation between the C4 ratio and the change in PPI was actually negative (-0.31), meaning the more concentrated the industry, the lower the price increase.

Concentration and Profitability

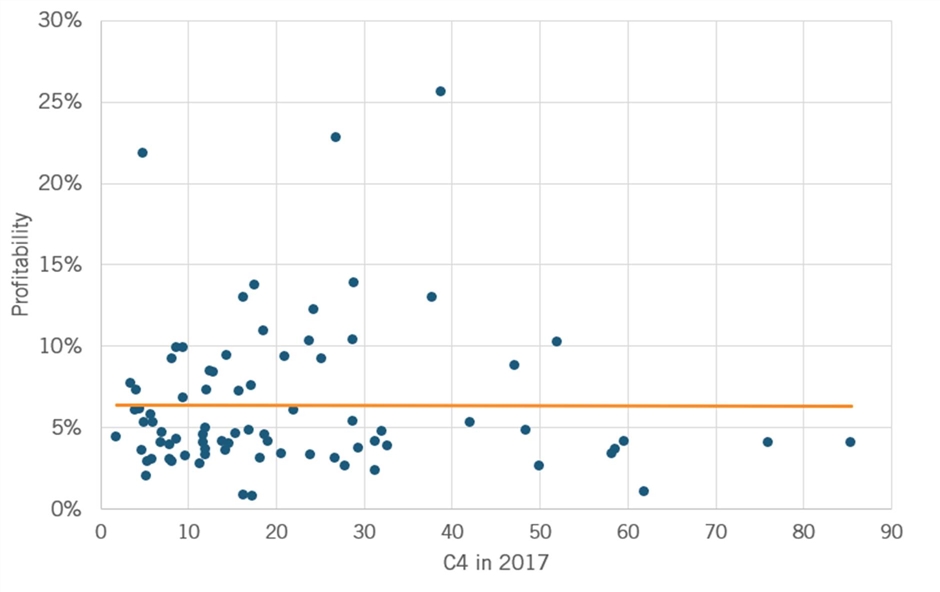

Surely concentration must enable the firms to earn higher profits. To assess this, ITIF combined aggregated profit data from the Corporation Complete Reports from the Internal Revenue Service with the Census C4 data at 3-digit NAICs code, as this was the level of aggregation in the IRS data set.[45] ITIF was able to get data on profits and concentrations for 80 industries.[46] ITIF used the measure of the ratio of net income over total receipts for profits. There is essentially no relationship between industry profitability and the concentration ratio in 2017 (a correlation coefficient of 0.04).

Figure 7: Relationship between the C4 concentration ratio and industry profitability[47]

The more concentrated the industry, the lower the price increase.

Why the Divergence of Views?

As noted, the now widely accepted view is that U.S. industrial concentration has increased significantly in the last two decades—and for many, to dangerously high levels. In fact, as this analysis of Census data has shown, there is virtually no support in the data for this view. So what explains this divergence between conventional wisdom and evidence? There are at least three main reasons.

First, many people, even pundits and analysts, tend to generalize from personal experience. We see this in how so many experts argue, without any real evidence, that the pace of technological innovation is accelerating, just because they see the pace of innovation in smartphones.[48] The same dynamic occurs with regard to views toward changes in concentration. Many Americans use Google, Amazon, and an iPhone, and fly on the four major airlines, and simply assume that concentration must be endemic.

Second, people’s attention is asymmetrical: Whenever a major merger is announced, there is usually a widespread reaction advancing the narrative of galloping concentration. But when companies announce divestitures that often reduce concentration, it is like the proverbial tree falling in the forest: silence. Case in point is recent divestitures, including AT&T’s divestiture of Time Warner, Astra Zeneca’s divestitures, and 3M’s divestitures, have received virtually no attention.[49] Yet, according to Ernst and Young, private equity-backed divestitures have increased 40 percent this year.[50] Likewise, the growth of smaller companies into larger ones that take market share away from the largest companies in a particular industry is rarely noticed. For example, companies such as Salesforce, Netflix, Biogen, and Gilead were much smaller a decade ago but now challenge the leaders.[51]

Finally, and most importantly, the key reason the “monopoly” narrative has become dominant is that neo-Brandeisians (individuals who oppose large corporations) seek a wholesale change in antitrust law to break up large companies, and the narrative of out-of-control monopolization is a critical intellectual tool for their campaign. Over the last 15 years, the neo-Brandeisian view has become the dominant one for most progressives, based on the view that virtually all economic problems stem from one cause: large corporations. This has led to a proliferation of progressive screeds against bigness: Tim Wu’s The Curse of Bigness, Matt Stoller’s Goliath: The 100 Year War Between Monopoly and Democracy, Jonathan Tepper’s The Myth of Capitalism: Monopolies and the Death of Capitalism, Zephyr Teachout’s Break ‘Em Up: Recovering our Freedom From Big Ag, Big Tech and Big Money, Barry Lynn’s Cornered: The New Monopoly Capitalism and the Economics of Destruction, and perhaps the book with the catchiest, if not the most eloquent, title, Sally Hubbard’s Monopolies Suck: 7 Ways Big Corporations Rule Your Life and How to Take Back Control.

The key reason the “monopoly” narrative has become dominant is that neo-Brandeisians seek a wholesale change in antitrust law to break up large companies, and the narrative of out-of-control monopolization is a critical intellectual tool for their campaign.

These books almost all start with a description of an idealized world before the 1980s when corporations were supposedly much smaller and everyone else much better off, and then a host of economic problems since then are all laid at the feet of the rise of so-called monopolies and the rise of a new corrupt school of antitrust, enabled by craven antitrust scholars in the pocket of big companies. And like a three-act play, the finale involves the neo-Brandeisians coming to save us and restoring some long-lost American dream by taking the antitrust hatchet to big, bad corporations. To do that, though, they must first convince voters and pundits that there is a serious problem of monopoly that calls into question the validity of the current antitrust system. The facts, unfortunately for the neo-Brandeisians, completely undercut their case.

Conclusion

As Daniel Patrick Moynihan once famously stated, “Everyone is entitled to his own opinion, not his own facts.” It is time for the debate about monopoly and industry concentration to be grounded in facts.

And the facts (data from the Economic Census) do not support assertions of monopolization. More than 80 percent of business output is in sectors with low concentration ratios, including many advanced technology industries. Moreover, from 2002 to 2017, concentration mostly stayed low and increased very little. In addition, more-concentrated industries did not on average show greater increases in prices or boosted profits than others.

It is unlikely that this data will convince neo-Brandeisian, anti-corporate advocates to modify their Cassandra-like warnings of the monopolization of the U.S. economy. But hopefully it will provide a helpful contribution to the debate over concentration for pragmatic individuals who are guided by facts.

ACKNOWLEDGEMENTS

The authors wish to thank Kevin Gawora for research assistance and Kristin Cotter for editorial assistance. All errors remain the authors’ responsibility.

ABOUT THE AUTHORS

Robert D. Atkinson (@RobAtkinsonITIF) is the founder and president of ITIF. Atkinson’s books include Big Is Beautiful: Debunking the Myth of Small Business (MIT, 2018), Innovation Economics: The Race for Global Advantage (Yale, 2012), and The Past and Future of America’s Economy: Long Waves of Innovation That Power Cycles of Growth (Edward Elgar, 2005). He holds a Ph.D. in city and regional planning from the University of North Carolina, Chapel Hill, and a master’s degree in urban and regional planning from the University of Oregon.

Filipe Lage de Sousa (@FilipeLageITIF) is senior economic policy analyst at ITIF. He is also a lecturer of economics at the master’s program in applied economics of John Hopkins University. He holds a Ph.D. from the London School of Economics. His expertise focuses on private sector development, including productivity, innovation, and trade, topics on which he has published extensively.

ABOUT ITIF

The Information Technology and Innovation Foundation (ITIF) is a nonprofit, nonpartisan research and educational institute focusing on the intersection of technological innovation and public policy. Recognized as the world’s leading science and technology think tank, ITIF’s mission is to formulate and promote policy solutions that accelerate innovation and boost productivity to spur growth, opportunity, and progress.

For more information, visit us at www.itif.org.

Endnotes

[1]Matt Stoller, Goliath: The 100-Year War Between Monopoly Power and Democracy (Simon and Schuster, 2019); Tim Wu, The Curse of Bigness: Antitrust in the New Gilded Age (Columbia Global Reports, 2018).

[2]Information on the released data was accessed on May 24, 2021, https://www.census.gov/content/dam/Census/programs-surveys/economic-census/05-20-21_whats-been-released.xlsx.

[3]David Wessel, “Is Lack of Competition Strangling the U.S. Economy?” Harvard Business Review (March–April 2018), https://hbr.org/2018/03/is-lack-of-competition-strangling-the-u-s-economy#.

[4]“Too Much of a Good Thing,” The Economist, March 26, 2016, https://www.economist.com/briefing/2016/03/26/too-much-of-a-good-thing.

[5]Jason Furman, “Prepared Testimony to the Hearing on ‘Market Concentration,’” OECD, May 27, 2018, DAF/COMP/WD(2018)67, https://www.oecd.org/daf/competition/market-concentration.htm.

[6]Paul Krugman, “Robber Baron Recessions,” The New York Times, April 18, 2016, https://www.nytimes.com/2016/04/18/opinion/robber-baron-recessions.html.

[7]Eduardo Porter, “With Competition in Tatters, the Rip of Inequality Widens,” The New York Times, July 12, 2016, https://www.nytimes.com/2016/07/13/business/economy/antitrust-competition-inequality.html.

[8]Joseph E. Stiglitz, “Market Concentration is Threatening the U.S. Economy,” Columbia Business School blog, March 12, 2019, https://www8.gsb.columbia.edu/articles/chazen-global-insights/market-concentration-threatening-us-economy.

[9]“America’s Concentration Crisis: An Open Markets Institute Report,” Open Markets Institute website, June 2019 (accessed June 5, 2020), https://concentrationcrisis.openmarketsinstitute.org/.

[10]“America’s Monopoly Problem: How the Growing Concentration of Economic Power Affects the Economy, Innovation, and Democracy,” Center for American Progress Action Fund, March 5, 2019 (accessed June 1, 2020), https://www.americanprogressaction.org/events/2019/02/27/173322/americas-monopoly-problem/.

[11]Klobuchar Presses Heads of DOJ Antitrust Division and FTC on Critical Issues of Competition in the U.S. Economy, Events, Speeches and Floor Statements on September, 2019, U.S. Senator Amy Klobuchar, accessed on April 14, 2021, https://www.klobuchar.senate.gov/public/index.cfm/2019/9/klobuchar-presses-heads-of-doj-antitrust-division-and-ftc-on-critical-issues-of-competition-in-the-u-s-economy.

[12]“Congress tries to get the FTC in fighting shape,” The Verge, March 18, 2021, accessed on April 14, 2021, https://www.theverge.com/2021/3/18/22338763/facebook-google-antitrust-cicilline-ftc-slaughter-monopoly.

[13]Lina M. Khan, “The Ideological Roots of America’s Market Power Problem,” The Yale Law Journal, June 4, 2018, accessed on May 24, 2021, https://www.yalelawjournal.org/forum/the-ideological-roots-of-americas-market-power-problem.

[14]“Biden-Sanders Unity Task Force Recommendations: Combating the Climate Crisis and Pursuing Environmental Justice,” Joe Biden campaign website, accessed April 15, 2021, https://joebiden.com/wp-content/uploads/2020/08/UNITY-TASK-FORCE-RECOMMENDATIONS.pdf.

[15]Carl Shapiro, “Antitrust in a Time of Populism,” International Journal of Industrial Organization, 61: 714–748, (2018), https://dx.doi.org/10.2139/ssrn.3058345.

[16]Gustavo Grullon, Yelena Larkin, and Roni Michaely, “Are US Industries Becoming More Concentrated?” Review of Finance, 23, no. 4, (July 2019): 697–743, https://doi.org/10.1093/rof/rfz007.

[17]“Economists: ’Totality of Evidence’ Underscores Concentration Problem in the U.S.,” ProMarket, accessed May 18, 2021, https://promarket.org/2017/03/31/economists-totality-evidence-underscores-concentration-problem-u-s/.

[18]As an example of evaluating concentration and competition at a local market, see C. Lanier Benkard, Ali Yurukoglu, and Anthony Lee Zhang, “Concentration in Product Markets” (working paper, National Bureau of Economic Research, No. w28745, 2021). This work’s findings suggest a higher concentration rate evaluated at the consumer side, yet a reduction of concentration in the U.S. markets from 1994 to 2019.

[19]Shapiro, “Antitrust in a Time of Populism.”

[20]Grullon, Larkin, and Michaely, “Are US Industries Becoming More Concentrated?” 706.

[21]U.S. Bureau of Economic Analysis, National Data (Shares of gross domestic product: Imports of goods and services, [B021RE1A156NBEA], retrieved from FRED, Federal Reserve Bank of St. Louis, May 26, 2021), https://fred.stlouisfed.org/series/B021RE1Q156NBEA.

[22]Matias Covarrubias, Germán Gutiérrez, and Thomas Philippon, “From Good to Bad Concentration? U.S. Industries Over the Past 30 Years,” NBER Macroeconomics Annual 34.1 (2020): 1–46, https://www.journals.uchicago.edu/doi/abs/10.1086/707169.

[23]“AmosWEB is Economics: Encyclonomic WEB*pedia,” accessed March 26, 2021, http://www.amosweb.com/cgi-bin/awb_nav.pl?s=wpd.

[24]The main sectors not covered by the U.S. Census in either or both of these two years are Agriculture (NAICS 11), Mining (NAICS 21), Construction (NAICS 23), Management of Companies and Enterprises (NAICS 55), and Education Services (NAICS 61). We did not count Public Administration (NAICS 91) because it is not a private sector.

[25]Bureau of Economic Analysis from the U.S. Department of Commerce (Gross Domestic Product from 2020 by Industry Group - Table 14 - on March 25, 2021), accessed on April 15, 2021, https://www.bea.gov/sites/default/files/2021-03/gdp4q20_3rd.xlsx.

[26]U.S. Census Bureau, Industry Data (concentration of 4 largest firms, concentration of 8 largest firms, total sales, ITIF internal calculations), accessed on March 5, 2021, https://www.census.gov/programs-surveys/economic-census/data/tables.html.

[27]Ibid.

[28]Ibid.

[29]Ibid.

[30]Xavier Jaravel and Erick Sager, “What are the Price Effects of Trade? Evidence from the U.S. and Implications for Quantitative Trade Models" (working paper, Finance and Economics Discussion Series 2019-068, Washington: Board of Governors of the Federal Reserve System, 2019), https://doi.org/10.17016/FEDS.2019.068.

[31]“The Observatory of Economic Complexity in 2019,” accessed on May 21, 2021; For Newsprint: https://oec.world/en/profile/hs92/newsprint-10480100; For Electric Lighting and Signaling Equipment: https://oec.world/en/profile/hs92/electrical-lighting-and-signalling-equipment.

[32]U.S. Census Bureau, Industry Data (concentration of 4 largest firms, concentration of 8 largest firms, total sales, ITIF internal calculations.

[33]Ibid.

[34]ITIF considered the Brookings classification of advanced industries at 4-digit NAICS code available. ITIF discarded and added some 6-digit NAICS code following the methodology proposed by Brookings Institute. Examples of discarded industries are Clay Building Material and Refractories Manufacturing (NAICS code 327120) and Broom Brush, and Mob Manufacturing (NAICS code 339994), and examples of added industries are Small Arms Ammunition Manufacturing (NAICS code 332992 & 332993). Brookings’s classification, accessed on May 19, 2021, https://www.brookings.edu/research/americas-advanced-industries-what-they-are-where-they-are-and-why-they-matter/.

[35]U.S. Census Bureau, Industry Data (concentration of 4 largest firms, concentration of 8 largest firms, total sales, ITIF internal calculations.

[36]Robert D. Atkinson, “Airline Monopoly Fears Are Bunk” (ITIF, February 14, 2019), https://itif.org/publications/2019/02/14/airline-monopoly-fears-are-bunk.

[37]Nathan F. Modica and Brian Chansky, “Productivity trends in the wired and wireless telecommunications industries,” Beyond the Numbers, 8, no. 8, May 30, 2019, https://www.bls.gov/opub/btn/volume-8/productivity-trends-in-the-wired-and-wireless-telecommunications-industries.htm.

[38]Ibid, Chart 1.

[39]Ibid.

[40]U.S. Bureau of Labor Statistics, Industry Data (Producer Price Index – PPI), accessed March 20, 2021, https://www.bls.gov/ppi/#data.

[41]Peter Cohen et al., “Using big data to estimate consumer surplus: The case of Uber” (working paper, National Bureau of Economic Research, No. w22627, September 2016).

[42]U.S. Census Bureau, Industry Data (concentration of 4 largest firms, concentration of 8 largest firms, total sales, ITIF internal calculations.

[43]ITIF considered the sum of total sales in all investigated 6-digit NAICS codes as the business output.

[44]U.S. Census Bureau op, Industry Data (concentration of 4 largest firms, concentration of 8 largest firms, total sales, ITIF internal calculations.

[45]Internal Revenue Services, Industry Data (Total Receipt, Net Income; Table 1 from the Corporation Complete Reports information; 2013), accessed on May 19, 2021, https://www.irs.gov/statistics/soi-tax-stats-returns-of-active-corporations-table-1.

[46]The 2017 U.S. Economic Census does not report concentration ratios for the NAICS codes 482 (Rail Transportation), 491 (Postal Service), 525 (Funds, Trusts, and Other Financial Vehicles), 551 (Management of Companies and Enterprises), and 814 (Private Households). And IRS does not provide information on profitability for NAICS code 521 (Monetary Authorities-Central Bank). In summary, ITIF analysis consists of all feasible information from the non-agricultural private sector industries in the U.S. economy, which comprises 80 industries of the total of 86 industries of 3-digit NAICS codes (93% of them). The U.S. Economic Census does not cover either Agriculture, Forestry, Fishing and Hunting (NAICS code 11), or Public Administration (NAICS code 92).

[47]U.S. Census Bureau, Industry Data (concentration of 4 largest firms, concentration of 8 largest firms, total sales, ITIF internal calculations. and IRS, Industry Data (Total Receipt, Net Income; Table 1 from the Corporation Complete Reports information; 2013).

[48]Robert D. Atkinson, “The Nonsense of Techno-Exponentialism” (ITIF, May 2014), https://itif.org/publications/2014/05/10/nonsense-techno-exponentialism.

[49]Amber Tong, “After a brief break, AstraZeneca is back at divesting — handing off hypertension meds for $350M,” Endpoints News, January 27, 2020, https://endpts.com/after-a-brief-break-astrazeneca-is-back-at-divesting-handing-off-hypertension-meds-for-350m/; Norbert Sparrow, “3M divests most of its drug-delivery business in $650-million deal,” Plastics Today, December 13, 2019, https://www.plasticstoday.com/medical/3m-divests-most-its-drug-delivery-business-650-million-deal.

[50]Andrew Wollaston et al., “How private equity is refining exit strategies for stronger valuations: 2021 Global Private Equity Divestment Study,” EY, May 19, 2021, https://www.ey.com/en_us/divestment-study/private-equity.

[51]Thomas C. Frohlich and Evan Comen, “America’s fastest growing companies,” USA TODAY, October 8, 2016, https://www.usatoday.com/story/money/business/2016/10/08/americas-fastest-growing-companies/91728104/.

Editors’ Recommendations

May 18, 2020