Energizing Innovation: Raising the Ambition for Federal Energy RD&D in Fiscal Year 2022

The United States should launch a “moon shot” in clean energy that mobilizes its unmatched innovative capabilities to combat climate change and capture global markets. The fiscal year 2022 budget is a critical opportunity for Congress to advance U.S. energy innovation.

CONTENTS

ARPA-E Renewables Transportation Energy Efficiency Electricity Grid Nuclear Fossil Energy Office of Science |

Please note that we have updated this report with data from the president’s full FY2022 budget request. All of the program summaries have been updated. A June update of the main report appears below the original summary in the full report pdf and can also be downloaded separately from the right-side menu on the main report page.

The fiscal year (FY) 2022 budget is a critical opportunity for Congress and the administration to rapidly scale up U.S. investment in energy innovation. In December, Congress provided a sweeping bipartisan overhaul of federal energy innovation programs in the Energy Act of 2020, paving the way for a major expansion in federal research, development, and demonstration (RD&D) to combat climate change and strengthen U.S. competitiveness. And members of Congress on both sides of the aisle have called for reinvigorating the national energy innovation system in order to reverse decades of declining investments and position the United States to thrive in a global clean energy transition. The Biden administration has followed suit, proposing a 27 percent boost in energy RD&D at the Department of Energy (DOE) in FY 2022 and a quadrupling of government-wide clean energy RD&D over the next four years.

But other nations such as Japan, China, and those within the European Union are investing more in energy RD&D to develop carbon-free technologies and capture growing global clean energy markets. China has doubled its energy RD&D in just the last five years, and now invests more than the United States does in key technologies, including solar energy, lithium-ion batteries, advanced nuclear, carbon capture, and electric vehicles (EVs). Europe is outstripping the United States in offshore wind, and has set aggressive targets in hydrogen and low-carbon steel. Meanwhile, U.S. investment in RD&D has declined to its lowest level since pre-Sputnik. And U.S. companies account for a declining share of new cleantech patents, indicating the United States is falling behind in innovation.

The United States should launch a “moon shot” in clean energy that mobilizes the nation’s unmatched innovative capabilities to meet the climate challenge and capture global markets. Congress and the administration should seize on the momentum created by the passage of the Energy Act of 2020, and provide a multi-billion-dollar increase in energy innovation programs at DOE in its FY 2022 budget.

Last year, the Information Technology and Information Foundation (ITIF) partnered with Columbia University’s Center on Global Energy Policy (CGEP) to produce Energizing America: A Roadmap to Launch a National Energy Innovation Mission. This landmark volume calls on policymakers to triple investment in energy RD&D over five years, develops strategic principles for balancing the portfolio, and provides targeted recommendations for accelerating innovation across key decarbonization challenges.

This report builds on Energizing America and consolidates ITIF analysis of federal energy innovation programs and its recommendations to accelerate critical energy technologies. The summary herein provides an overview of federal energy innovation programs, including the key role of DOE in advancing energy technologies and the department’s impact on national energy systems. It assesses the significant updates to DOE’s program authorizations made in the Energy Act and the prospects for greater investment in the FY 2022 budget and appropriations cycle.

Companion to the summary herein are 21 short policy briefs that span DOE’s RD&D programs in renewable energy, transportation, energy efficiency, grid modernization, nuclear energy, fossil energy and carbon management, and basic sciences. Each brief includes a description of the DOE’s program and technology goals; what’s at stake and potential impacts of the program; historic and authorized funding levels; and targeted recommendations for Congress and DOE to accelerate innovation.

This report also includes a living interactive data visualization that will be updated throughout the FY 2022 budget cycle. The administration is expected to release the full congressional budget justification in late Spring 2021, and House and Senate proposals will soon follow. The interactive data visualization will provide a resource for policymakers, researchers, and the public to track federal investments in energy innovation.

Innovation Is Essential to Address Climate Change and Boost U.S. Competitiveness

The transition from an energy system dominated by unabated fossil fuels to one with net-zero emissions is critical for mitigating climate change, protecting human health, and revitalizing the U.S. economy. However, clean energy alternatives have not yet been commercialized for some of the sectors that produce large amounts of greenhouse emissions, including aviation, shipping, steel, cement, and chemicals manufacturing. Meanwhile, many of the clean technologies that already have been commercialized—such as EVs—are still more expensive than the emitting technologies they would replace, and also face other barriers to scaling up. These costs and barriers must continue to fall for these clean technologies to cut emissions drastically.

The transition also brings with it risks and opportunities for U.S. industry. Investment in key clean technologies—from hydrogen to EVs to batteries to carbon capture and storage (CCS)—is rapidly increasing around the world. Even during the COVID-19 pandemic, when many traditional energy industries have suffered from delayed or declining investment, global investment in clean energy has increased. A key question for policymakers is whether that investment will occur in the United States or elsewhere. The risk lies in being left behind as other nations capture growing global sectors.

The solution to both of these challenges is to boost U.S. investment in innovation. But accelerating innovation requires assertive federal policy that involves more than basic research funding. Innovation requires both proactive public investment in RD&D and the creation of markets to hasten early adoption and ignite private sector innovation and competition.

Innovation to Drive Economic Growth and Capture Growing Global Markets

Innovation is fundamental to both long-term job creation in the U.S. economy and the resilience of the economy to disruptions. Technology discovery and development create opportunities for new jobs, and innovation in established technologies drives long-term cost reductions and improvements in quality. Innovation is also an important engine for entrepreneurship, especially in tech-heavy sectors. Finally, innovation is a necessary condition, albeit an insufficient one, for U.S. competitiveness in the rapidly growing global clean energy industry.

Global annual investment in energy was $1.5 trillion in 2020, a decline of 20 percent from 2019 levels due to the COVID-19 pandemic. But the share going to clean energy has been increasing in spite of those headwinds. Investment in renewable energy grew 2 percent in 2020 to $304 billion. Investment in EVs surged to $139 billion in 2020, beating the previous year by 28 percent despite the pandemic. Significant economic opportunities await countries that can supply new and growing clean energy markets.

The United States has long been the world’s leading technological innovator, but it has not always effectively used this advantage to sustain domestic manufacturing. For example, scientists at Bell Labs in New Jersey created the first solar cell in 1957, and strong and steady procurement from the Navy and NASA allowed American solar companies to serve the market in that technology’s early days. Since the turn of the century, however, the United States has ceded much of its original leadership. Only one of the top 10 solar photovoltaic (PV) manufacturers, First Solar, is an American firm (eight are Chinese, one is South Korean), and U.S. companies’ share of the global solar market has dropped below 10 percent.

As countries around the world seek to stimulate their economies and recover from the COVID-19 crisis, the United States could fall further behind in a range of technology areas. The European Union announced more than $200 billion in climate-friendly economic recovery investments, such as clean hydrogen infrastructure. The Chinese government has announced a “new infrastructure” package worth $1.4 trillion that will include investments in advanced energy industries and infrastructure. Japan, the European Union, and 11 other nations have launched national hydrogen strategies and are investing heavily in electrolyzers, fuel cells, and other hydrogen technologies.

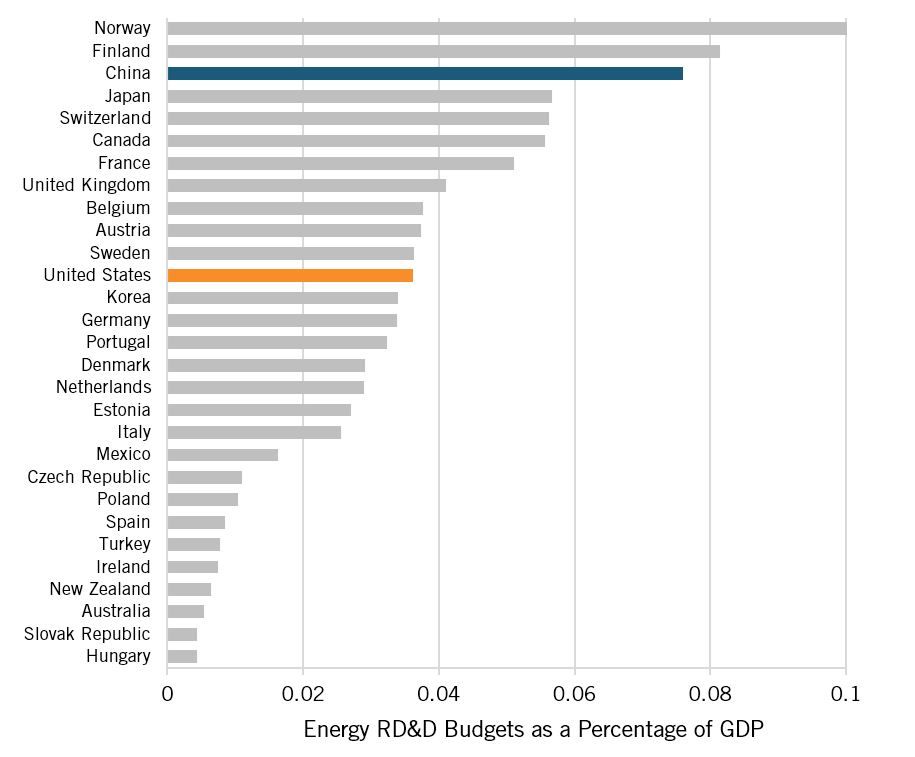

Figure 1: Government energy RD&D investment as a percentage of gross domestic product (GDP), 2019

Even in public funding for energy RD&D, an area wherein the United States has long been the top investor, U.S. leadership is now being challenged by China and Europe. China doubled its investment in clean energy RD&D between 2015 and 2020 to $8 billion annually, putting it ahead of the United States in absolute spending for the first time. And 11 other countries invest more in energy RD&D as a share of their economies than does the United States

(figure 1). As other countries have stepped up their investments in clean energy, the share of cleantech patents granted to U.S. companies by the U.S. Patent and Trade Office—from roughly 50 percent in 2001 to less than 40 percent in 2016—has declined, indicating that U.S. leadership in innovation truly is waning.

These trends are disturbing. The decline of the U.S. manufacturing sector has cost the economy high-quality jobs, increased income inequality, and contributed to public dissatisfaction. The National Academies’ report Accelerating Decarbonization of the U.S. Energy System argues that “the United States should attempt to claw these industrial sectors and markets back, so that it leads the world both in innovation and in the manufacturing and marketing of advanced clean energy technologies.”

But the Academies find cause for optimism. The United States has rich natural resources that give it a competitive advantage in the clean energy transition: It has abundant solar and wind resources (both onshore and offshore), 40 million acres already devoted to producing biofuels, plentiful natural gas, and enormous geologic and terrestrial reservoirs for carbon dioxide (CO2) sequestration. The challenge will be to combine these natural assets with the nation’s culture of innovation to regain global leadership and competitiveness in clean energy technology, modernize and transform the U.S. manufacturing base, and create a new generation of clean energy jobs.

Innovation to Combat Climate Change

Decarbonizing the U.S. economy by 2050 is technically feasible, provided that adequate investments are made over the next decade to advance critical clean energy technologies and solutions. But current funding levels are not sufficient to generate the pace of innovation needed to address climate change. According to the International Energy Agency (IEA), only 6 out of 46 critical energy technologies are “on track” to achieve a net-zero emissions energy system.

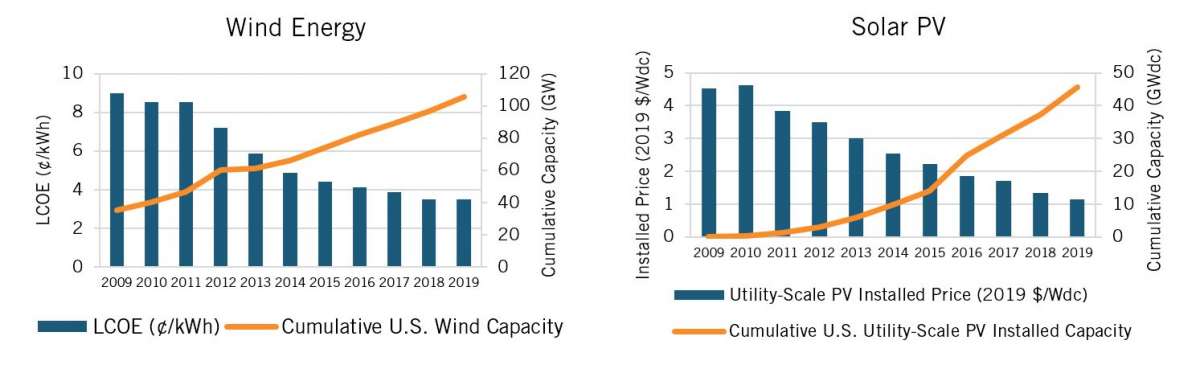

The energy innovation agenda of the last 10 years focused, with considerable success, on reducing the cost and expanding the use of wind and solar resources for electricity generation (figure 2). Rapid cost declines in solar PV, wind turbines, and grid-scale batteries are enabling decarbonization of the power sector on a much faster timeframe than was imagined a decade ago. As of 2018, wind or solar power was the cheapest source of new electricity in 34 percent of U.S. counties, and costs have continued to decline since then. This success is beginning to bear fruit: U.S. power sector emissions have declined 33 percent from 2005 levels, and wind and solar power are poised for rapid build-out in the 2020s.

Figure 2: Cost reductions and capacity build-outs in wind energy and solar PV

The challenge is to replicate the success of wind and solar power with other clean technologies and across all sources of emissions. In the power sector, new affordable, carbon-free firm generation that is available 24/7 and can be dispatched on-demand will be needed to achieve a carbon-free electricity system. In the transportation sector, EVs are projected to reach cost parity with gas-powered cars in the 2023–2025 time range, but significant hurdles related to charging times, driving range, availability of charging infrastructure, and impacts to the grid must be addressed. In buildings, high-efficiency heat pumps and low-global-warming-potential refrigerants can reduce emissions from heating and cooling, but costs must come down to enable wider deployment.

Innovation challenges are even more acute for harder-to-abate sectors. Aviation, marine shipping, and long-distance trucking are more challenging to electrify than light-duty cars and trucks, and will likely require carbon-neutral fuels that are as energy dense as the petroleum-based fuels they would replace. Heavy industries such as steel, cement, and chemicals are especially challenging to decarbonize due to process emissions from chemical transformations and emissions from high-temperature heat. Many promising solutions are being developed but must be validated and demonstrated at commercial scale before they will make a dent in emissions.

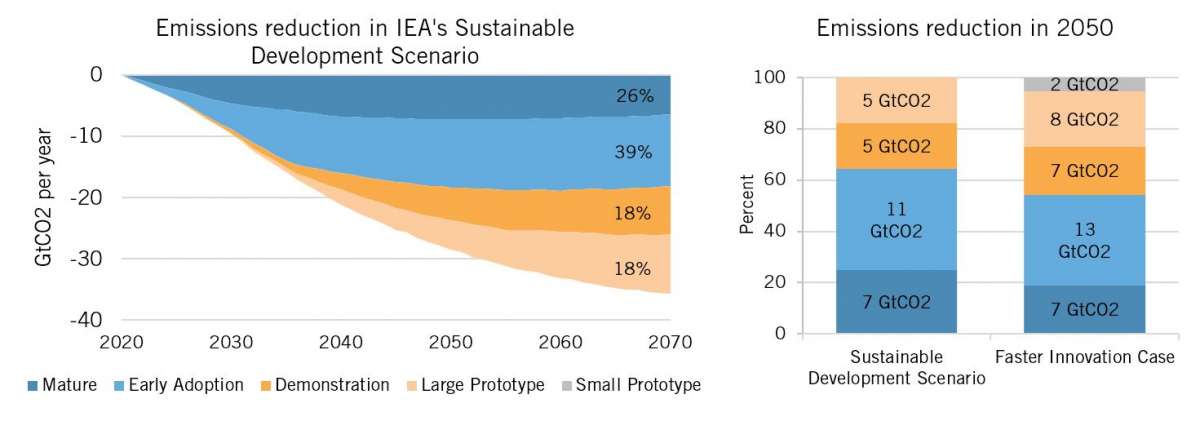

IEA’s Energy Technology Perspectives 2020 reportfinds that large shares of the global annual emissions reductions necessary to achieve net-zero emissions in the coming decades will likely come from technologies that are at the demonstration or prototype stage of development and are not yet commercially available today (figure 3). In IEA’s Sustainable Development Scenario, which reaches global net-zero emissions in 2070, 36 percent of annual emissions reductions in 2070 will come from technologies in these stages. In the Faster Innovation Case, which achieves net-zero global emissions by 2050, nearly half of annual emissions reductions come from technologies in the demonstration, large prototype, or small prototype stage of development (figure 3).

In the past, new energy technologies—even recent successful consumer products such as LEDs and batteries—have taken 20 to 70 years to go from the first prototype to 1 percent market share. The world will not achieve its climate aspirations if innovation moves that slowly in the future. Assertive RD&D and market creation efforts are needed in the 2020s to develop, improve, and scale up nascent, low-carbon energy technologies so they are available as near-term decarbonization opportunities reach their limits.

Figure 3: Global energy sector CO2 emissions reductions by current technology maturity category

The Key Role of the Federal Government in the U.S. Energy System

Many technologies that now make major contributions to both the U.S. and global energy systems were created through federal investments and public-private cooperation. Federally funded nuclear power RD&D, for instance, led to large-scale private investment in commercial power plants that now account for 20 percent of U.S. electricity generation and 54 percent of zero-carbon power generation. Federal support for shale gas resource characterization and directional drilling—in tandem with industry-matched applied research and a federal production tax credit—led to the dramatic rise of shale gas production from less than 1 percent of domestic gas production in 2000 to nearly 80 percent in 2020 (see box 1). Decades of investment and policy-driven market development have led to precipitous declines in the cost of new solar PV (89 percent cheaper since 2009) and new wind facilities (70 percent cheaper since 2009) (see box 2).

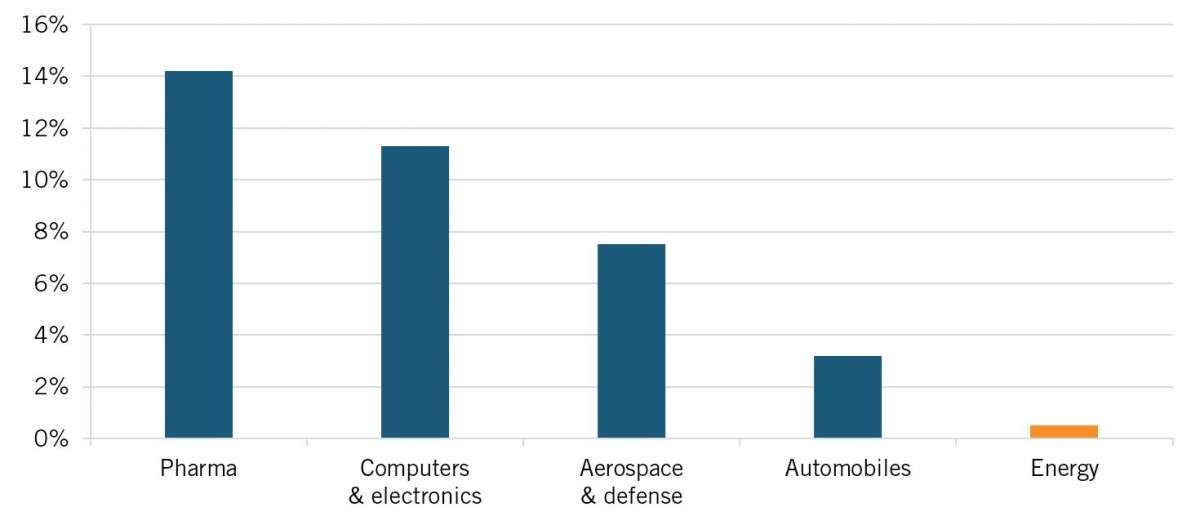

But unlike software and biotech, which attract significant private investment, clean energy faces substantial scale-up and commercialization challenges. Technology development lifecycles are long, and projects are often capital intensive and bear a significant amount of technical and financial risk. For these reasons, the energy industry invests a very small share of its revenues, just 0.5 percent, in research and development (R&D). That is far less than the 14.2 percent R&D-to-revenue ratio found in pharmaceuticals, 11.3 percent in computers and electronics, 7.5 percent in aerospace and defense, and even 3.2 percent in autos (figure 4). Even venture capital funding, which tends to be less risk averse than other sources of private capital, favors payback times and returns on investments that make it a poor match for the cleantech industry.

Figure 4: R&D spending as a percentage of revenue across major global industries, 2018

In addition, because energy is valued as a commodity (i.e., there is no tangible difference in the electricity that comes from a coal plant versus a wind farm) emerging energy technologies frequently cannot distinguish themselves from incumbent technologies on performance and must therefore compete on price from the moment they enter the market. Electric utilities are often legally mandated to keep prices low, and may be prohibited from investing in new technologies.

Box 1: Federal Role in the Shale Gas Revolution

The shale gas revolution example illustrates the synergies of “technology push” and “market pull” policies working in concert to shepherd a new technology to market. Beginning in the late 1970s, the federal government funded fundamental research in directional drilling and shale resource characterization, countenanced and funded industry-wide collaboration in applied RD&D that might otherwise have drawn antitrust scrutiny, and subsidized industry-led demonstrations of the first horizontal wells in West Virginia and Texas. This technology push overlapped with a time-limited market-pull production tax credit for wells drilled between 1980 and 1992, with production eligible for the credit through 2002. By 2002, when federal support tapered off, shale gas had grown to account for 2 percent of domestic gas production and was able to compete in the market on its own. Since then, hydraulic fracturing technologies, combined with vast domestic shale resources, have enabled shale gas to grow to 70 percent of domestic production.

The federal government is uniquely suited to address these barriers by making high-risk, long-term investments the private sector is simply unwilling to fund. For technologies that are far from commercialized, basic and applied research and technology development are necessary to improve the performance and drive down the cost of emerging technologies to the point entrepreneurs and corporate R&D units jump in. As technologies mature, successful demonstration at commercial scale is required to establish cost, reliability, and performance characteristics, and provide confidence to more risk-averse investors and the public that the technology works as intended at a manageable cost. Additional tools such as loan guarantees for first-of-a-kind commercial projects and market pull policies such as tax incentives and clean energy standards bring technologies further down the cost curve. Public investment as a share of the total spent on each technology generally declines as it matures, from full public support for basic research to significant levels of private-sector cost sharing in the development and demonstration stages.

DOE’s key role in bringing shale-gas technology to maturity is just one example in an impressive list of accomplishments. DOE helped develop low-cost flue-gas desulfurization scrubbers for power plants, which made the United States into a global leader in pollution control technologies, while also lowering energy costs and improving air quality for all Americans (see box 3). New methods for producing quantum dots—which have applications in high-efficiency TV screens, solid-state lighting, and quantum computing—were first developed in DOE laboratories. Basic research in subsurface fluid flow and high-strength materials by DOE in the early 1980s resulted in advancements in drilling that could soon enable expansion of enhanced geothermal energy to large parts of the country. In each of these cases, the road from discovery to deployment took decades, required government investment to develop and “de-risk” the inventions, and entailed public and private partners working together to bring them to market.

Box 2: DOE Loan Guarantees Launched Utility-Scale Solar PV

The evolution of solar PV technologies similarly exemplifies the role of smart public policy in accelerating innovation and the synergistic interactions between public and private investment. In the 1970s and 1980s, government and university R&D was responsible for most of the performance improvements and cost reductions in solar PV modules. During that time, the nascent solar industry was supported by the emergence in the public sector of niche applications—primarily for use in satellites—at NASA and the Defense Department that were relatively insensitive to cost. As the technology matured and the solar industry expanded, pull policies such as tax incentives, net-metering, feed-in tariffs, and state portfolio standards helped expand the market for solar and also incentivized greater private sector investment, which enabled the industry to take advantage of economies of scale. In 2011, the DOE Loan Programs Office provided loan guarantees to the first five utility-scale solar PV facilities larger than 100 megawatts (MW). Thanks in large part to these policies working together in the United States and globally, the cost of solar PV panels has declined by 99 percent over the last four decades.

The Department of Energy… And Lots of Other Stuff

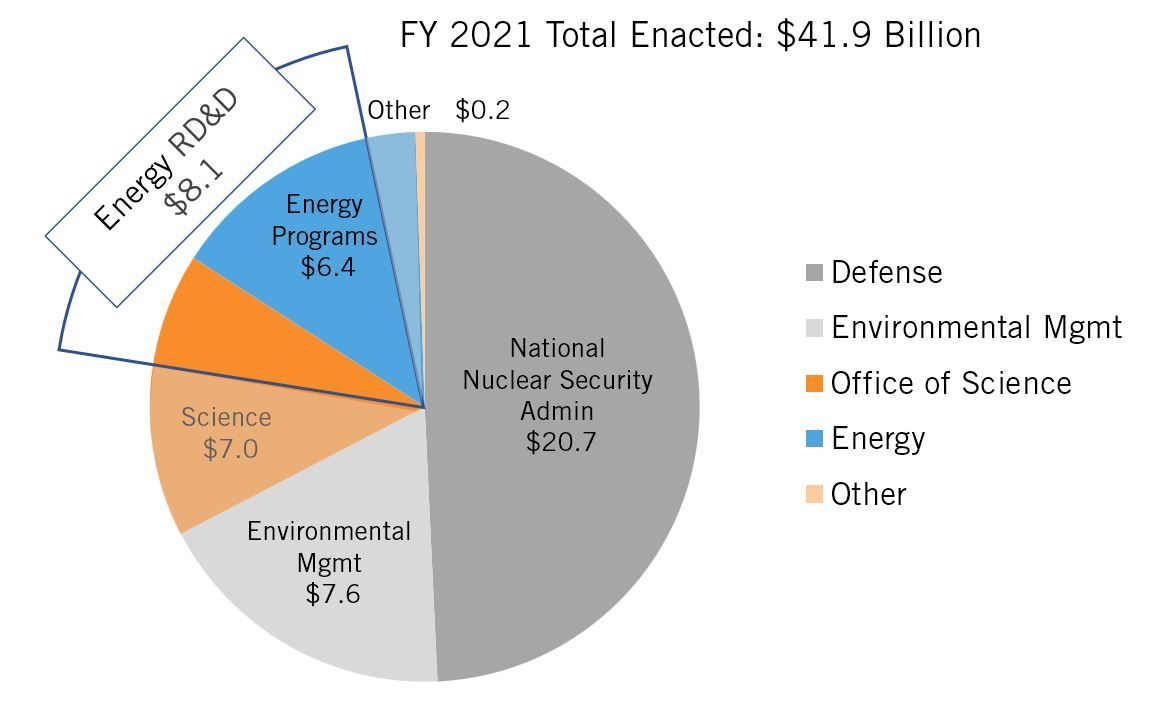

The name “Department of Energy” may leave the mistaken perception that DOE’s primary function is overseeing and improving the nation’s energy system. In reality, when other activities of DOE—defense, environmental cleanup, and non-energy-focused basic science—are taken into account, only a small portion of its budget supports energy innovation. Figure 5 shows DOE’s budget by organization. The department’s $8.1 billion energy RD&D portfolio includes portions of the Office of Science and the energy programs.

Figure 5: DOE budget by major function, FY 2021 (in billions)

DOE was assembled in 1977 from previously scattered federal agencies, the largest of which was the Atomic Energy Commission, which had managed the military’s nuclear weapons program since just after World War II. DOE’s National Nuclear Security Administration (NNSA) carries out such defense responsibilities today. NNSA and other defense programs housed within DOE comprise more than 49 percent of the agency’s nearly $42 billion budget. In addition, DOE’s Office of Environmental Management (EM) is tasked with cleaning up the massive pollution left behind by the weapons program. EM’s budget is more than $7.5 billion, comprising 18 percent of DOE’s budget. Together, these two slices make up more than two-thirds of the department’s budget.

DOE’s $7 billion Office of Science (SC) is one of the government’s largest funders of basic science research, providing critical research infrastructure through its support for 10 of DOE’s 17 national laboratories. SC research is spread across six program areas: Advanced Scientific Computing Research, Basic Energy Sciences (BES), Biological and Environmental Research (BER), Fusion Energy Sciences (FES), High Energy Physics, and Nuclear Physics. While SC is an important component of the nation’s discovery science ecosystem, less than half of its budget is specifically devoted to advancing energy research. (ITIF includes only BES, FES, and the portion of BER that supports bioenergy research centers in its definition of energy-related research.)

DOE’s energy programs include both RD&D and non-RD&D functions. Most of the energy RD&D budget is distributed across DOE’s applied energy offices: Energy Efficiency and Renewable Energy, which houses programs in renewable energy, sustainable transportation, and energy efficiency; Electricity, which supports grid modernization; Cybersecurity, Energy Security, and Emergency Response (CESER); Fossil Energy and Carbon Management; and Nuclear Energy. The Advanced Research Projects Agency for Energy (ARPA-E) is a stand-alone, semiautonomous agency that advances cross-cutting research in high-potential, high-impact energy technologies that are too early for private-sector investment.

Portions of DOE’s energy programs support other critical functions. The Energy Information Administration provides data and analysis to identify energy demand and supply and model the U.S. energy system to project future trends. The Weatherization Assistance Program supports deployment of energy-conserving technologies for low- and moderate-income households. The Office of Indian Energy supports financing of energy infrastructure projects on tribal lands (analogous to the Rural Utility Service at the U.S. Department of Agriculture). DOE’s State Energy Program provides technical assistance and support to states, primarily to support state-level energy offices. The Strategic Petroleum Reserve and other fuel reserves maintained by DOE provide critical insurance against potential interruptions in U.S. fuel supplies. These additional functions, though important, are not part of the energy innovation budget.

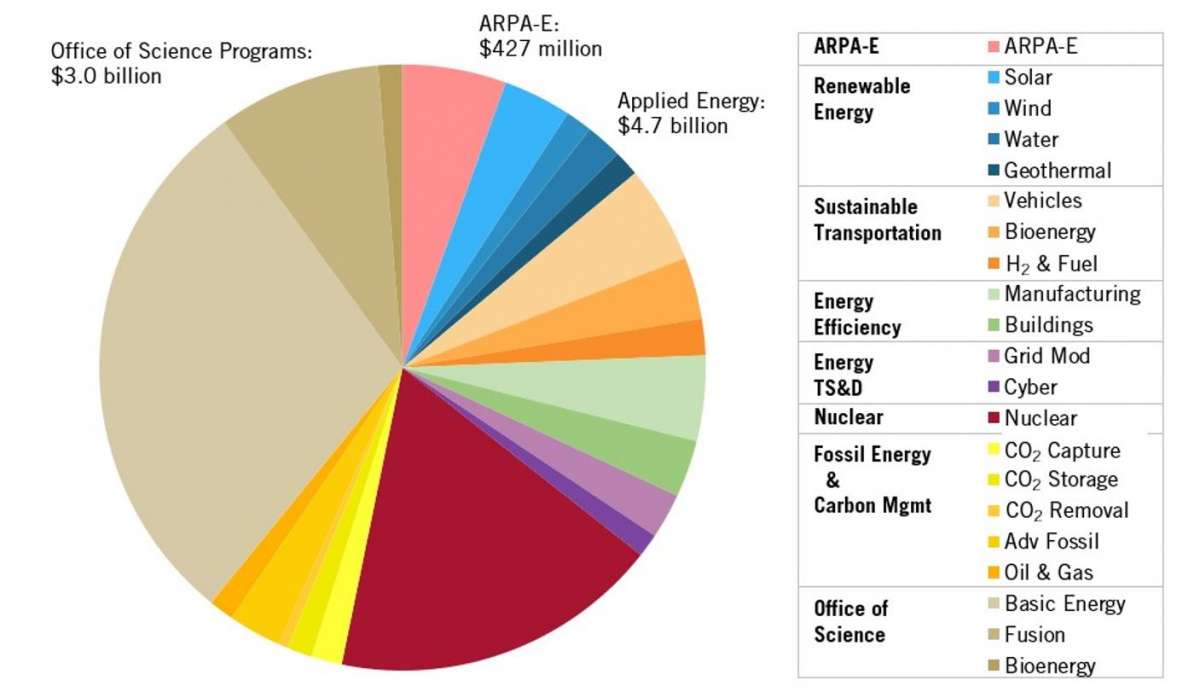

DOE’s entire energy RD&D portfolio—including the applied energy programs, portions of the DOE SC, and ARPA-E—totals $8.1 billion, or about 19 percent of DOE’s budget (figure 5). The portfolio spans 21 science and technology program areas across 7 technology categories, shown in figure 6: renewable energy; transportation; energy efficiency; energy transmission, storage, and distribution (TS&D); nuclear energy; fossil energy and carbon management; and basic energy-related research.

Figure 6: DOE’s energy RD&D funding by program area, FY 2021

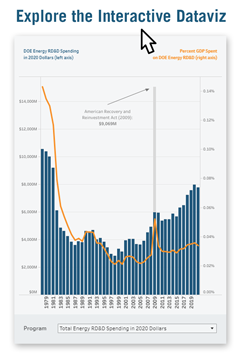

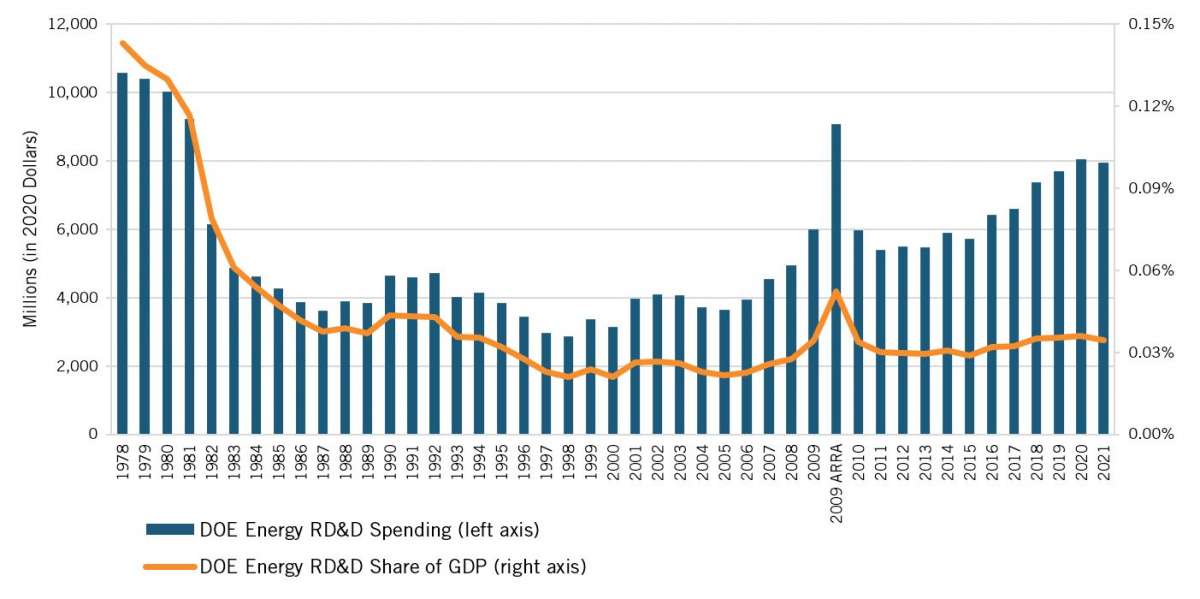

The federal government has not always been so stingy. At the time of DOE’s creation in the late 1970s, energy demand was increasing rapidly, energy prices were high and rising, and the Arab oil embargo and formation of OPEC (Organization of the Petroleum Exporting Countries) sparked fears of rising energy insecurity and dependence. Energy innovation and the development of domestic clean energy resources were viewed as matters of economic and national security. In 1978, Congress invested more than $10.5 billion (in 2020 dollars) in energy RD&D, or 0.14 percent of GDP. Had federal investment kept pace with growth in the economy, DOE’s RD&D budget today would be $32 billion, on par with other national priorities such as health research.

The threat posed by climate change is more severe than the energy shortage crises of the late 1970s, but the government is investing far less in energy innovation to meet this challenge. As energy prices fell in the 1980s, energy innovation receded as a national priority, with funding levels hovering below $4 billion for most of the mid-1980s through the early 2000s. During the George W. Bush administration, Congress began increasing funding in response to higher energy prices and reports that the United States risked falling behind other nations in clean energy. And as part of Mission Innovation—an international agreement launched in tandem with the Paris Climate Agreement to accelerate clean energy innovation—the United States committed to doubling clean energy RD&D by 2021, providing additional impetus for congressional appropriators. Congress has increased budgets for DOE’s energy programs for 11 of the last 15 years, but annual appropriations have consistently fallen short of doubling targets, and funding has not yet returned to its 1978 level (see figure 7).

Figure 7: U.S. DOE Energy RD&D spending, FY 1978 through FY 2021

DOE RD&D: Generating Huge Returns on a Modest Budget

Despite a relatively small investment, federal energy RD&D has delivered big returns for the American public. DOE’s investments have led to commercialization of new products, lower costs and speedier deployment of clean technologies, energy savings for consumers and businesses, less pollution from dirty energy, and greenhouse gas emissions reductions. DOE research has won more than a third of the top 100 R&D awards given out annually by R&D World magazine for each of the last four years. An external review of energy efficiency and renewable energy RD&D at DOE found that a total taxpayer investment of $12 billion between 1975 and 2015 yielded more than $388 billion in net economic benefits, a remarkable return of over $32 for every federal dollar invested (see box 4 for DOE’s buildings and appliances return on investment).

DOE research has also helped reduce the environmental impacts of fossil fuel consumption and made the United States a world leader in pollution control technologies. DOE partnerships with major engine manufacturers to develop more-efficient diesel engines saved the U.S. trucking industry 17.6 billion gallons of diesel fuel over the 12 years between 1995 and 2007, which translated into $34.5 billion in reduced fuel expenditures and $35.7 billion in health and environmental benefits from lower pollution. DOE leadership in carbon capture technologies led to successful first-of-a-kind demonstrations of carbon capture at a fertilizer production facility (Port Arthur, in 2013), a corn ethanol refinery (ADM, in 2017), and a coal power plant (Petra Nova, in 2017) (see box 5). And DOE has issued a conditional loan guarantee of up to $2 billion to build the world’s first clean methanol facility with carbon capture in Lake Charles, Louisiana, with construction slated to begin in mid-2020.

Box 3: Launching the Pollution Control Industry

Federal investments in pollution control technologies provide an example of the multiple benefits of energy RD&D. Prior to DOE’s coal RD&D programs, flue gas desulfurization (FGD) systems (aka “scrubbers”) were costly to build and maintain, incurred substantial energy costs to run, and produced a sludge waste requiring considerable land use for proper disposal. Advancements in pollution control helped drive capital and operating costs down by nearly 50 percent, kept energy costs low, and turned the waste from FGD scrubbers into valuable byproducts such as wallboard-grade gypsum. DOE investments in FGD scrubbers resulted in over $50 billion in savings from lower FGD costs and public health benefits, and also helped turn America into a global leader in environmental technologies. Environmental technologies and services contribute to a trade surplus, yielding net exports of nearly $27 billion annually.

Energy and Climate Benefits of DOE Programs

For each of its applied energy programs, DOE sets technology cost/performance targets based on the RD&D activities possible at a given budget level. As part of its goal-setting process, DOE and laboratory experts assess the ability of its program activities to improve a technology’s characteristics (e.g., capital cost) and move it closer to commercialization. In conducting this analysis, DOE assumes that funding levels will remain constant over time.

Perhaps the best-known target was set by DOE’s SunShot Initiative. Launched in 2011 to make solar energy cost competitive with conventional generation, the initiative aimed to reduce the cost of utility-scale solar PV by 75 percent by 2020, to a nationwide average of 6 cents per kilowatt-hour ($0.06/kWh). That would be within the range of the levelized cost of electricity from a natural gas combined cycle power plant, which was $0.044–0.073/kWh in the United States in 2020. The cost target was achieved three years early, in 2017, prompting DOE to launch new SunShot 2030 goals: $0.03/kWh for utility-scale PV, $0.04/kWh for commercial-scale PV, and $0.05/kWh for residential PV. Achieving these price reductions could result in solar energy meeting 14 percent of U.S. electricity needs by 2030 (up from 2 percent in 2020), support 290,000 new solar jobs, and translate into $30 billion in annual energy cost savings by 2030.

Box 4: Buildings and Appliances

Investments in DOE’s Building Technologies Office (BTO) between 2010 and 2015 culminated in the successful commercialization of 27 products across a range of energy-related technologies, including energy-efficient water heaters, solid-state lighting, and energy-saving windows. For example, the advanced dual evaporator technology for refrigerators—which performs up to 50 percent better than conventional single-cycle refrigeration systems—was developed with assistance from BTO and successfully commercialized by Whirlpool Corporation in 2013. A retrospective assessment of BTO investments between 1976 and 2015 across three technology areas—HVAC, water heating, and appliances—found that BTO investments yielded between $6 billion and $22 billion in economic benefits, with a benefit-to-cost ratio of between 20:1 and 66:1. BTO’s current goal is to reduce the average energy use per square foot of all U.S. buildings by 30 percent by 2030, which would decrease total energy use by 5 quadrillion BTUs and save consumers over $100 billion in energy costs annually.

Recent rapid cost declines have enabled even greater ambition. In March 2021, DOE announced that it is moving up its SunShot goal by five years, targeting $0.03/kWh by 2025. And it announced a new target of $0.02/kWh by 2030.

Other notable DOE technology targets include:

- Reducing average building energy use per square foot by 30 percent from 2010 levels by 2030, saving consumers up to $100 billion annually in energy costs, and cutting carbon emissions by 450 million metric tons;

- Reducing the cost of batteries for EVs to $100/kWh, increasing their range to 300 miles, and decreasing charging time to 15 minutes by 2028, bringing the total cost of ownership of EVs in line with that of conventional cars and trucks;

- Reducing the cost of hydrogen production (to $2 per kilogram) and hydrogen storage (to $1 per kilogram), which could open up new applications for clean hydrogen in key transportation and industrial sectors;

- Reducing the cost of carbon capture to under $30 per metric ton, which could result in up to 30 gigawatts of carbon capture technologies and more than 150 million metric tons of CO2 sequestered by 2030; and

- Reducing fugitive emissions from natural gas systems by 40–45 percent, which would improve public safety, reduce greenhouse gas emissions, and ensure that more natural gas makes its way from the producer to the end customer.

If DOE meets its targets, the nation would gain significant benefits, including lower consumer energy bills and better health and environmental outcomes. A 2017 DOE analysis concluded that if its current RD&D programs were to meet their targets for reducing the costs and improving the performance of clean energy technologies, U.S. carbon emissions could fall 23 percent by 2040 and lower residential energy bills by 25 percent. And if DOE doubled its RD&D budget, better technologies could reduce U.S. emissions by an additional 15 percent. These projections may be conservative, as between 2012 and 2017, DOE met or exceeded 75 out of 76 technology targets. Clearly, RD&D is an important part of the decarbonization tool kit.

Because of its ability both to reduce carbon emissions and lower energy bills, expanding public investment in RD&D may be more palatable to policymakers than carbon pricing as they consider policy options to address climate change. But as DOE’s analysis finds, RD&D can also “soften the blow” of carbon pricing and other regulatory options, opening up avenues of climate policies that would otherwise be prohibitively expensive or politically untenable.

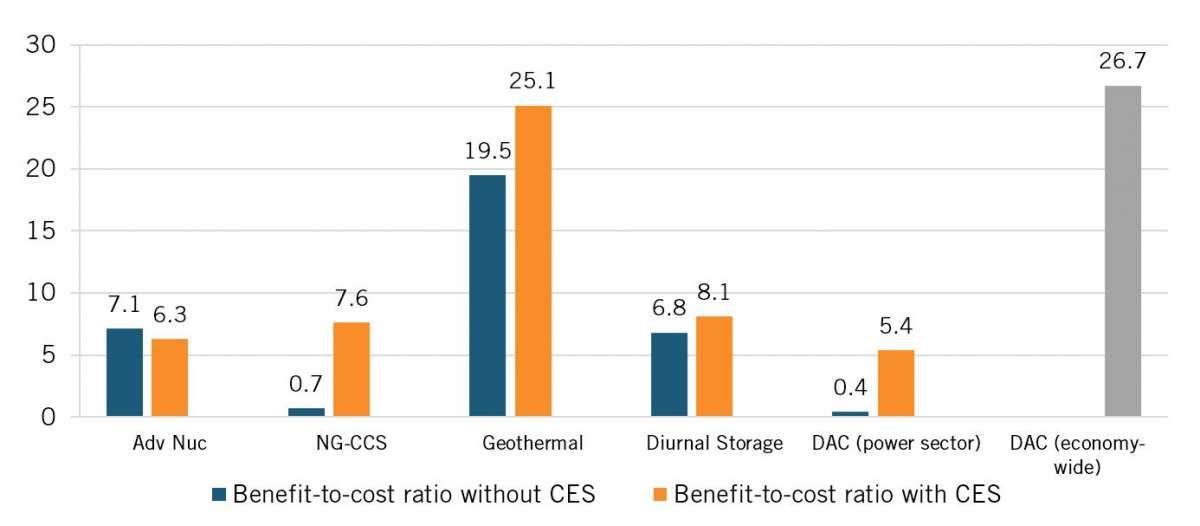

DOE is now preparing to launch new programs across a range of advanced energy technologies in response to the Energy Act of 2020. In April 2021, Resources for the Future (RFF) released a study of the potential impact of additional funding across five of the technologies: advanced nuclear, natural gas with carbon capture and sequestration (NG-CCS), advanced geothermal, diurnal energy storage, and direct air capture of CO2 (DAC). The study projects future cost reductions resulting from the additional RD&D funding and estimates the benefits of these cost reduction under a scenario with and without a national clean electricity standard (CES). Benefits include electricity bill savings, reduced health damages, and reduced climate damages. The study finds average power sector benefits are likely to exceed costs by a factor of 7 without a CES, and by a factor of more than 10 with a CES. Average annual electricity bill savings for each household are about $14 without a CES and $56 with a CES.

Figure 8: Estimated benefit-to-cost ratios from 10 years of higher RD&D funding across 5 technologies

2021: A Critical Opportunity for Energy Innovation

2021 presents a critical opportunity to rapidly scale up U.S. investment in energy innovation. In a polarized political system, energy innovation has long enjoyed bipartisan support. Large majorities of voters across the political spectrum support more funding for research into clean energy. A December 2020 poll found that 82 percent of registered voters support funding more research into clean energy sources such as solar and wind power. And lawmakers from diverse backgrounds have embraced energy innovation as a strategy to combat climate change and promote U.S. competitiveness. From 2011 to 2020, Congress increased federal funding for energy RD&D in every single year except 2015. And support is growing. In Congress, Democrats and Republicans have joined forces to advance legislation around energy storage, advanced renewables, carbon capture, and nuclear.

So far, these efforts have contributed modest, though important, expansions to the federal energy innovation system. Over the past four years, Congress has provided a 40 percent increase in the energy RD&D programs at DOE, reversing decades of neglect and declining investments. However, DOE’s energy RD&D budget for FY 2021 remains more than 20 percent below what it was when the department was established in 1978. And current funding levels are far below what is needed to match the urgency of climate change and advance U.S. competitiveness in clean energy.

But the 2021 budget cycle may be different. In December 2020, Congress came together to pass the Energy Act of 2020, a sweeping overhaul of DOE’s programs, and the first major reauthorization in more than a decade. The Energy Act creates new programs to address technology gaps, expands programs to scale up and commercialize technologies developed in the labs, and authorizes significant boosts in funding for some key technologies. More than 100 members of Congress contributed to portions of the bill. This monumental achievement signifies greater attention and focus on the need for energy innovation, and could be a launchpad for more action in 2021.

Additionally, the number of voices calling for substantially greater investment—not just incremental increases—is growing, as lawmakers and prominent voices on both sides of the aisle have called for doubling, tripling, or even quintupling federal innovation. The debate is no longer over whether to scale up energy innovation—only how much and what to invest in.

Energy Act of 2020: A Significant Step Forward

The Energy Act of 2020 delivers a monumental overhaul of DOE programs—the first significant reauthorization since the Energy Independence and Security Act of 2007, and one of the biggest, wholly bipartisan advancements in clean energy innovation policy in over a decade.

The road to enactment began in the Senate Energy and Natural Resources committee in 2015, when then-Chairman Murkowski (R-AK) and Ranking Member Cantwell (D-WA) launched a bipartisan effort to develop a comprehensive update to national energy policy. Their effort resulted in the Energy Policy Modernization Act of 2015 (EPMA). EPMA easily passed the Senate and was successfully conferenced with the House, but the House ended the 114th Congress early without a chance to vote on the final conference report. In 2019, the process began again, with Chairman Murkowski and (the new) Ranking Member Manchin (D-WV) bringing the bipartisan American Energy Innovation Act to the floor of the Senate in February 2020. The House Science, Space, and Technology Committee—which has jurisdiction over DOE’s RD&D programs—began a parallel process under Chair Johnson (D-TX) and Ranking Member Lucas (R-OK), producing a number of bipartisan bills spanning a range of clean technologies.

This activity culminated in the 530-page Energy Act of 2020, which includes the areas of greatest agreement between the House and Senate energy packages. It was included in the omnibus appropriations act passed by Congress in December 2020.

The Energy Act modernizes and refocuses DOE’s RD&D programs to address critical energy innovation challenges. Technology has evolved rapidly since 2007: New challenges have emerged, and priorities have evolved, highlighting the need to revisit DOE’s authorizations. The Energy Act:

- Revises and updates program authorizations to account for technological advances over the last decade and to address current and emerging challenges;

- Creates new programs in clean manufacturing and carbon removal—sectors that have historically been underrepresented in DOE’s portfolio; and

- Provides the first significant new investment in large-scale demonstration projects—which are essential for scaling up and validating emerging technologies—in more than a decade.

Some gaps remain. Certain technologies received comparatively less attention, and some program reauthorizations did not make it into the final bill. A key challenge facing the current legislature is providing sufficient funding to match innovation challenges, and addressing remaining gaps. But success builds its own momentum. The Energy Act of 2020 showed that Congress can come together in a bipartisan manner to address national challenges. This success makes it more likely that Congress will take the next step.

Box 5: Carbon Capture on the Cusp?

CCS may be on the cusp of significant new build-outs and cost reductions, thanks in part to DOE’s work in developing and demonstrating carbon capture technologies. DOE’s Industrial Carbon Capture and Storage program culminated in the successful launch of CCUS demonstration projects at the Port Arthur fertilizer facility in 2013 and the Archer Daniels Midland ethanol plant in 2017. The Petra Nova coal power plant began capturing its carbon emissions in 2017 at a cost of about $60 per ton. (Although the plant closed due to declining revenues as a result of the COVID-19 pandemic, it was successful in facilitating learning that is projected to lead to 30 percent cost reduction for similar second-of-a-kind projects.) The National Carbon Capture Center in Wilsonville, Alabama, is now installing a natural-gas-fired system to test technologies under natural-gas-fired and coal-fired flue gas conditions. And in February 2018, Congress expanded and extended the 45Q tax credit to incentivize greater utilization and storage of captured CO2.

The Energy Act of 2020 provides a significant expansion of DOE’s programs that could further accelerate carbon capture. It expands R&D activities beyond just power plants to include manufacturing facilities such as cement and steel plants. It also creates a new program to conduct large-scale pilot projects at a scale “beyond laboratory development and bench scale testing, but not yet advanced to the point of being tested under real operational conditions at commercial scale.” And it directs DOE to begin six commercial demonstrations of carbon capture by 2025—two each at coal power plants, natural gas power plants, and industrial facilities.

Taking the Next Step: Time for a Moon Shot in Clean Energy

The successful passage of the Energy Act of 2020 positions Congress to aim for new levels of ambition and launch a moon shot for clean energy. Public support is coalescing around the need for massive scale-up of federal innovation programs. And a growing chorus of science and technology policy experts is calling for substantial scale-ups and new investments in the national innovation ecosystem.

Last year, ITIF partnered with CGEP to produce Energizing America: A Roadmap to Launch a National Energy Innovation Mission. The volume calls on Congress and the president to triple funding for energy RD&D over five years in order to harness the nation’s innovative capabilities and speed the progress of clean energy technologies. Energizing America provides a strategic framework for building a growing RD&D portfolio, with detailed funding proposals across the full spectrum of critical energy technologies.

Other prominent figures have recommended similarly ambitious increases. A pair of recent studies from the National Academies of Sciences, Engineering, and Medicine (NASEM)—Accelerating Decarbonization of the U.S. Energy System and The Future of Electric Power in the U.S.—call on policymakers to triple energy RD&D. The tripling target has also been recommended by the American Energy Innovation Council (AEIC), the Center for Climate and Energy Solutions (C2ES), and the President’s Council of Advisors in Science and Technology. Breakthrough Energy has called for a fivefold increase in funding to $35 billion by 2030, which would bring energy RD&D to roughly 0.1 percent of GDP, in line with historical levels of energy investment, and roughly in line with health spending ($38 billion in 2020).

ITIF joined the Clean Air Task Force, Edison Electric Institute, and other energy utilities and leading energy and climate think tanks to launch the Carbon-Free Technology Initiative, which provides an innovation agenda to develop and commercialize the firm, carbon-free, dispatchable technologies necessary to completely decarbonize the electric power system. The initiative develops detailed policy proposals—building on the policy developments from the Energy Act of 2020—across key technology areas, and recommends tripling investment in power-sector RD&D at DOE. And in May 2021, more than 100 energy and environmental organizations, industry groups, and research institutions jointly signed a letter calling on congressional leadership to provide an FY22 appropriations allocation that enables a multi-billion-dollar increase in the research, development, demonstration, and commercial deployment activities at DOE.

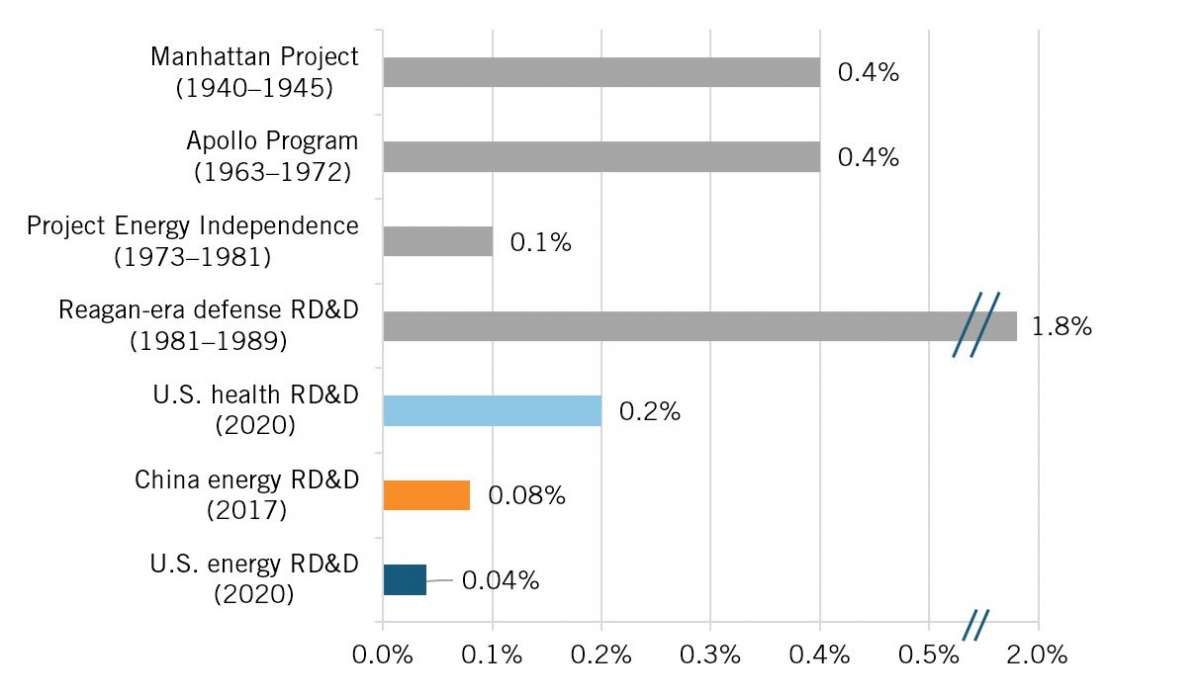

These targets are both ambitious and measured. Other national innovation missions in space, health, and defense show that the United States can marshal its innovative capacity on a much larger scale than it currently does for energy (figure 9). Federal investment in RD&D has accelerated the development of life-saving drugs, modernized the military’s arsenal, and put a man on the moon. By comparison, the federal government has neglected energy innovation.

Figure 9: Federal RD&D funding as a percentage of GDP for selected national innovation missions

The American Jobs Plan and President Biden’s Budget Request for FY 2022

The American Jobs Plan

The American Jobs Plan proposes dramatically increased federal investments—around $2 trillion over the next decade—in the infrastructure and innovation underpinnings of America’s economy, including investments in RD&D and manufacturing. The plan would reverse a decades-long decline in innovation funding, with Federal RD&D investment across all sectors falling to pre-Sputnik levels, and the United States slipping to 10th place among Organization for Economic Cooperation and Development (OECD) countries in national RD&D intensity.

The plan includes proposals to advance clean energy innovation, including both RD&D and early deployment and market expansion policies. Key climate and energy innovation provisions include:

- $40 billion investment to upgrade the research infrastructure in laboratories across the country, including DOE’s 17 national labs;

- $35 billion investment in climate science, innovation, and R&D, with a $5 billion increase in funding for climate-focused research and $15 billion in demonstration projects in utility-scale energy storage, CCS, hydrogen, advanced nuclear, rare earth separations, floating offshore wind, biofuels and bioproducts, quantum computing, and EVs;

- $20 billion in regional innovation hubs to fuel technology development, link urban and rural economies, and create new businesses in regions beyond the current high-growth centers;

- $10 billion R&D investment at historically black colleges and universities (HBCUs) and other minority-serving institutions (MSIs), and $15 billion to create up to 200 centers of excellence that serve as research incubators at HBCUs and other MSIs;

- $10 billion investment in a new green jobs training program—a Civilian Climate Corps—to support the skilled workforce needed to produce advanced technology goods;

- 10 pioneer projects that demonstrate carbon capture retrofits for large steel, cement, and chemical production facilities;

- 15 clean hydrogen demonstration projects; and

- A new Advanced Research Projects Agency-Climate (ARPA-C) to develop new methods for reducing emissions and building climate resilience.

In addition, the proposal includes investments in EV chargers, transmission incentives, government procurement, and other policies to expand markets for clean energy. The plan is currently being developed into congressional legislation, with more details about how the proposal would impact DOE’s energy RD&D budget likely to emerge in the late-Spring to early-Summer 2021.

The Biden Administration’s Budget Request for FY 2022

In April 2021, the Office of Management and Budget released the outline of President Biden’s budget request for FY 2022. The request calls for quadrupling government-wide investment in clean energy innovation over the next four years, providing a much-needed boost in federal innovation programs. Highlights include:

- $46.1 billion for DOE, a $4.3 billion (10 percent) increase over FY 2021;

- $10 billion for government-wide clean energy innovation programs, of which $8 billion would go to DOE programs;

- $7.4 billion for DOE SC, which conducts basic energy science research, as well as discovery science and advanced computing research;

- $1 billion for a new ARPA-C and the existing ARPA-E, of which $700 million is funded through DOE;

- Refocusing the Office of Fossil Energy and Carbon Management on carbon reduction and mitigation, and expanding to include industrial carbon capture, hydrogen, and direct air capture;

- $1.9 billion for a new Clean Energy Projects and Workforce Initiative, with investments to support infrastructure and grants to state, local, and tribal governments to support clean energy deployment in marginalized communities; and

- Support for economic revitalization for coal and power plant communities.

The initial budget guidance is short on details, and will be supplemented by the full budget justification documents in the coming months.

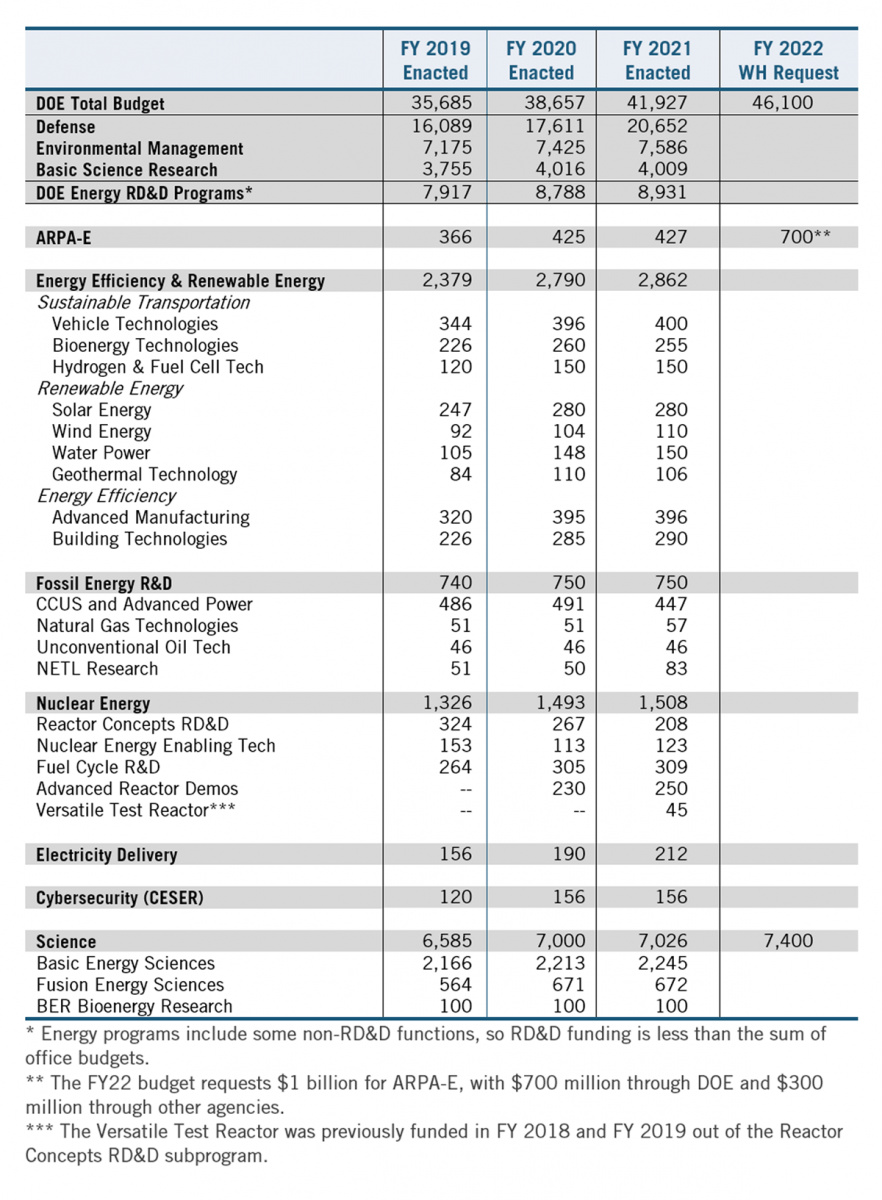

Table 1: DOE budget by program area, FY 2019 enacted through FY 2022 request, in millions of dollars.

What Happens Next

The full budget request and supporting DOE Congressional Budget Justification documents are expected to be released in late Spring 2021. These documents will provide granular funding levels and more details about what the president is requesting and why.

The House and Senate Appropriations committees have already begun holding hearings to solicit testimony and input on their FY 2022 bills. The House Energy & Water Development subcommittee held its first hearing in February on “Strategies for Energy and Climate Innovation,” which focused on DOE’s clean energy innovation programs. The committee has also held hearings on investment and innovation in water resources infrastructure and domestic clean manufacturing. It has scheduled a hearing on the FY 2022 budget request for DOE on May 6.

The next step is for the House and Senate to agree on an overall top-level discretionary budget for FY 2022. The Appropriations committees must then apportion the overall discretionary budget to their subcommittees, setting what are referred to as the “302(b) allocations” for each of the 12 bills that fund the government. DOE, along with the Army Corps of Engineers, Department of Interior, and other related agencies, is funded through the Energy and Water Development (E&W) appropriations bill. Appropriators’ ability to increase funding will be limited by each chamber’s leadership, which will determine how much money will be allocated to the E&W bill and the 11 others that comprise the budget.

Ultimately, an appropriations bill is supposed to pass both chambers of Congress and be signed by the president before the next fiscal year begins on October 1, although continuing resolutions that extend current fiscal-year spending levels into the next fiscal year have frequently been used in recent years.

Concurrent with the appropriations process, the authorizing committees are continuing the process of modernizing and updating DOE’s programs, picking up where the Energy Act of 2020 left off. The House Committee On Science held hearings on building technologies, which were left out of the Energy Act, as well as sustainable aviation, a hard-to-abate source of emissions. House Science has scheduled a hearing on “Climate and Energy Science Research at DOE” on May 4. The U.S. Senate Committee on Energy and Natural Resources has also held hearings on carbon utilization technologies, transportation technologies, and nuclear energy, as well as on the larger role of DOE in energy innovation.

While these hearings are unlikely to impact the budget for FY 2022, they do indicate continuing engagement on emerging innovation challenges and attention to gaps that were not addressed in the Energy Act. These hearings could lead to new legislation to reauthorize and update existing DOE programs, or create new ones.

Conclusion

The United States has a proud history of rising to global challenges by unleashing its potential to innovate. If policymakers decisively invest in the clean energy technologies of the future and sustain that investment, history can repeat itself. Nearing the end of the global coronavirus crisis, the United States should lead the response to climate change and prosper as the world transitions to clean energy. As Congress considers its FY 2022 appropriations, it has a tremendous opportunity to accelerate domestic clean energy industries and shape the U.S. response to climate change. It should build on the foundations paved by the Energy Act of 2020, and continue to elevate energy innovation as a national priority.