Is the United States Immune to Dutch Disease?

Venezuela has a problem, and you can tell what it is simply by looking at the architecture in Caracas, its capital. The city is full of buildings with heavy concrete facades, the brutalist style briefly in vogue when global oil prices went through the roof in the 1970s and took Venezuela’s economy with them. The problem is that oil income turned out to be a double-edged sword. As Venezuela became more dependent on oil, other industries were crowded out, unable to compete due to the appreciation of the Bolívar, Venezuela’s currency. However, oil production did not provide jobs to average Venezuelans. When oil prices came down, the economic miracle crumbled like a house of cards. Today, amid political turmoil, high unemployment and hyperinflation, it’s worth asking whether the oil wealth did more harm than good.

Venezuela suffers from what economists call Dutch Disease or the Resource Curse—negative consequences derived from reliance on natural resource exports. Mineral exports drive up the value of the country’s currency, making it harder for other industries in the nation to compete globally. The result is a hollowing out of a country’s other traded sectors, particularly manufacturing.

American economists have for years doled out advice to Dutch Disease-stricken nations, extolling the virtues of balanced economic growth, with the tacit assumption that the United States is advanced, diversified, and large enough to avoid the pitfalls of reliance on wealth from minerals. But now, as the United States celebrates an oil boom of its own, the question must be asked: Is the United States immune to Dutch Disease?

To start, let’s examine the symptoms of the disease.

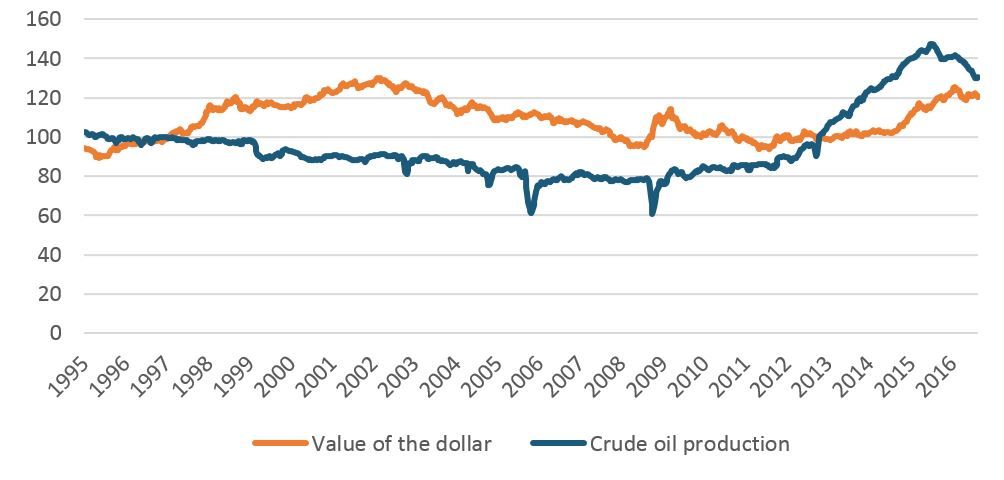

Thanks to fracking technology, which has enabled a shale revolution, the United States has become one of the world’s largest producers of oil. The oil boom has dramatically reduced the United States’ reliance on imported oil. Indeed, in December 2015, Congress reversed a 40-year ban on exporting oil, and the United States is poised to run a trade surplus in the energy sector. Because oil imports are down, the value of the U.S. dollar is up, making it harder for businesses in the United States to compete with foreign competition in traded sectors.

Figure 1: Value of the U.S. Dollar and U.S. Crude Oil Production (Index 1997=100), U.S. Energy Information Administration and St. Louis Federal Reserve

Of course, a currency’s value is supposed to act as a sort of pressure gauge on the economy’s competitiveness—if an economy is doing very well and outcompeting others, the value of its currency goes up, allowing consumers at home to buy more goods from abroad. On the other hand, if an economy is struggling to keep up, the value of its currency drops, making goods cheaper abroad. In the long term, currency valuation is the primary regulator of balanced trade deficits. Even with the jump in petroleum production, the United States is now running a trade deficit that is larger than ever, despite not having run a surplus since 1975. From 2012 to 2015, while the dollar appreciated by over 20 percent, the U.S. trade deficit in non-petroleum goods rose by 44 percent, or $245 billion. Clearly, the mechanism by which currency valuation helps modulate the trade deficit is not functioning as an arbiter of global competitiveness. Meanwhile, labor productivity growth stagnated, signaling rough waters ahead for U.S. manufacturing industries.

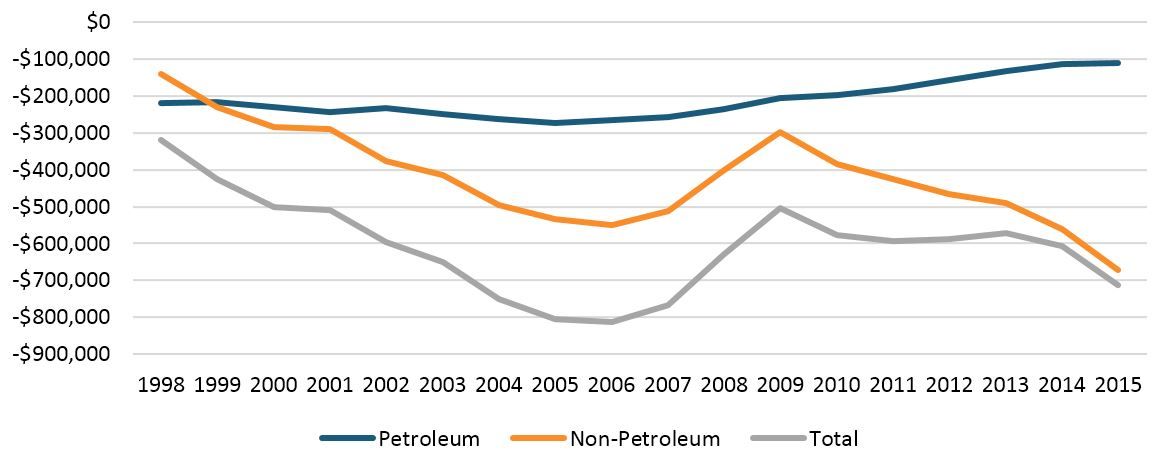

The United States’ large trade deficit is even more significant when you consider that the U.S. deficit in petroleum, traditionally as substantial percentage of the overall trade imbalance, has been significantly reduced. However, Americans simply replaced this foreign consumption with consumption of other products. In 2014, Robert Lawrence correctly predicted that the end of U.S. reliance on foreign oil would have almost no effect on the trade deficit. Goaded along by the strong dollar, Americans poured nearly the entire surplus created by the shale oil boom into elevated consumption of foreign goods, which actually damaged the prospects for U.S. producers.

Figure 2: U.S. Trade Deficit, by Petroleum and Non-Petroleum, Census Bureau, 1998-2015, Millions of Chained (2009) U.S Dollars

The growth of oil money in the United States adds one more barrier to the idea that the United States can survive without a well-articulated and robust innovation strategy. If a manufacturing renaissance based on U.S. cost-competitiveness seemed far-fetched before, it certainly is now. The appreciated dollar, and the expectation that the dollar will remain strong, hurts companies who export with thin margins. From a competitiveness standpoint, an appreciated dollar is functionally no different than widespread currency manipulation by foreign competitors like China. Indeed, Harry Moser of the Reshoring Institute posits that recent appreciation resulted in a 12 percent drop in value of the renminbi against the dollar, eliminating years of slow appreciation by the Chinese currency to correct for artificial depreciation designed to give China an edge in manufacturing industries.

That’s not to say that oil wealth is strictly bad for the U.S. economy, but it does imply that we should follow our own advice regarding a national response to Dutch Disease. What do we do with a pile of money and reduced ability to compete at the margins in the current global economy? Invest in the future. Specifically, the United States should invest in basic public research that can help it retain a competitive edge in advanced industries, where currency valuation is less likely to impact global competitiveness. A national strategy to promote innovation and competitiveness in these industries should also be a priority.

Resource-dependent countries around the world are following this advice to avoid the negative repercussions of Dutch Disease. Saudi Arabia, perhaps the most oil-rich country in the world, is in the middle of making an ambitious bet on innovation. After only spending around 0.25 percent of GDP on public R&D in 2000, the Kingdom seeks to invest 2 percent of GDP by 2017. By contrast, the United States spends less than 0.8 percent of GDP on public R&D, the lowest investment levels since the U.S. reaction to Sputnik in 1957. Unable to compete at the margin due to a highly appreciated currency, Saudi Arabia is looking to compete in winner-takes-all innovation where being first to a specific technology ensures a country’s competitiveness regardless of the value of their currency. And yes, Saudi Arabia is pouring substantial resources into clean energy solutions, trying to disrupt the industry that has made them rich. The United States should use its oil boom to double down on public research areas like clean energy, advanced manufacturing tools and process, and biopharmaceuticals instead of allowing oil wealth to be a hindrance to competitiveness.

Editors’ Recommendations

December 16, 2016

Trumpism and the New Economy

November 16, 2016

Transition Memo to President Trump: How to Spur Innovation, Productivity, and Competitiveness

November 9, 2016