Lies, Damned Lies, and KPMG’s Corporate Tax Reform Statistics

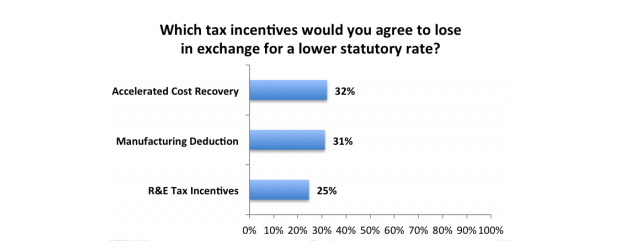

Percentage of business executives willing to give up specific tax incentives (n=682) (source: KPMG)

Last Friday, Reuters reported on a recent KPMG survey of 682 business executives that finds that, (to paraphrase KPMG’s website) in exchange for a lower statutory corporate tax rate, 68 percent of respondents would be willing to give up accelerated depreciation of capital equipment, 66 percent would be willing to give up the domestic production deduction for manufacturing, and a “surprising” 52 percent would be willing to give up the research and experimentation (R&E) tax credit.

This is untrue, and here’s why. The survey question (Question 4a) that asks which tax incentives the executives would be willing to give up is limited to only those executives who answered “yes” on a previous question (Question 4) about whether or not they’d be willing to support reform that repeals tax incentives in exchange for a lower rate. This means that, while the previous question had 682 respondents, the subsequent question on the specific tax incentives they’d be willing to give up had only 322 respondents.

So, while it is indeed true that, for example, 52 percent of the 322 executives who answered Question 4a would be willing to give up the R&E credit in exchange for a lower statutory rate, it is far cry from “52 percent of respondents overall” saying this, as is claimed on KPMG’s website. In fact, this means that only 168 out of the 682 business executives who took the survey—just 25 percent—say they’d be willing to give up the R&E credit. The same reasoning applies to accelerated depreciation and the domestic production deduction: just 219 executives, or 32 percent, want to give up the former; and just 213 executives, or 31 percent, want to give up the latter.

These figures show that, in reality, few corporate executives want to give up tax incentives like the R&E credit in course of corporate tax reform. While this may be reason enough to keep these incentives off the table during tax reform negotiations, there are a couple even more important reasons for policymakers to leave the incentives in place. First, the companies that claim these tax incentives tend to be those that compete in the U.S. economy’s traded sector, and in a world with ever increasing global competition, it is extremely important that policymakers get traded-sector tax policy right. Sacrificing these tax incentives for the sake of lowering the statutory rate would effectively lower taxes on the non-traded sector while raising taxes on the traded sector. But, since the health of the non-traded sector is dependent on the health of the traded sector, this policy makes little sense. Second, much of the benefits of tax incentives such as the R&E credit flow not to the performing businesses themselves but to American society at large. While these “positive externalities” are not the immediate concern of the survey’s business executives, they are certainly the concern of U.S. policymakers, and Congress should keep in mind that by removing these incentives they would be sacrificing much more than just a few corporate tax breaks.