---

title: "Targeted Pressure: How Chinese Manufacturing Competition Impacts US States"

summary: |-

Chinese industrial policy is reshaping global manufacturing and impacting every U.S. state. The result is growing risk to American industry, jobs, and national security.

date: "2026-06-01"

issues: ["Manufacturing", "National Competitiveness"]

authors: ["Trelysa Long", "Meghan Ostertag"]

content_type: "Reports & Briefings"

canonical_url: "https://itif.org/publications/2026/06/01/targeted-pressure-how-chinese-manufacturing-competition-impacts-us-states/"

---

# Targeted Pressure: How Chinese Manufacturing Competition Impacts US States

## Key Takeaways

- Unfair Chinese policies and practices, not market-based competition, are reducing foreign manufacturing capabilities, including America’s.

- Overcapacity and below-cost pricing are central competitive tools. In many sectors, Chinese firms expand output beyond global demand, driving down prices and squeezing more U.S. firms out of both domestic and third-country markets.

- Erosion of U.S. industrial capacity poses national security risks. Many affected industries are critical to defense and infrastructure, increasing U.S. vulnerability to supply chain disruptions and economic coercion.

- Every U.S. state is harmed by unfair Chinese competition, with negative implications for companies, economic output, and well-paying jobs.

- This report examines a leading industry for each U.S. state and the current and potential future negative impact from Chinese unfair competition.

# Introduction

China is engaged in an intensifying techno-economic war to dominate a select group of advanced, globally traded industries that are the bedrock of technological leadership and economic power in the 21st century. The Information Technology and Innovation Foundation (ITIF) calls these industries “national power industries.” China’s gains in national power industries are coming at the expense of U.S. and allied global market share and production capabilities, which puts at risk not just America’s global competitiveness, but also its national security.[1](#_edn1) That’s because becoming dependent on Chinese firms in the “enabling,” “dual-use,” and defense industries that together comprise the larger class of national power industries leaves the United States open and vulnerable to coercion from China—an unacceptable risk amid rising tensions between the two countries.[2](#_edn2)

Importantly, this techno-economic battle is taking place not just in high-tech industries that are clustered in places like Silicon Valley and Harvard Square, but also in many other strategically important industries that are spread across the entire country. Every state relies on these industries, ranging from agricultural machinery to medical instrument manufacturing, to employ hundreds or thousands of workers and contribute to its economy—and most of these industries are facing increasing competition from China.

However, China and its firms are not normal competitors. Unlike American firms, those in China benefit from high levels of government subsidies, artificially inflated demand, tax incentives, favorable financing, reduced energy prices, and many more policy instruments used to strengthen Chinese competitiveness. In this way, U.S. firms can no longer compete on innovativeness and productivity alone, and many have seen declines in sales, employment, and market share as a result. These firms are no longer competing just against other firms, but also against the might of the Chinese government.

> Every state relies on national power industries—and most of these industries are facing increasing competition from China.

Despite the abundance of information on the risks posed by unfair Chinese competition in these industries, there is a significant lack of data to support a causational techno-economic analysis, particularly at the state level, on how Chinese firms may have contributed to the decline of American industries. This data gap limits policymakers’ ability to assess where and how Chinese competition is affecting U.S. industries and regions. To address this, policymakers should consider a dedicated effort to systematically collect and analyze global and state-level market share data across manufacturing industries. Such an initiative would enable a more precise identification of which state industries face the greatest competitive pressures from China, as well as when and how these pressures emerge.

This report draws on the best available industry-wide data on employment, exports, and global market share to assess a single national power industry in each state in the context of the U.S.-China competition in that industry. In doing so, it examines the relationship between U.S. firms in these industries and the potential competitive pressures posed by China.

# State Analyses

All industries analyzed in this report are national power industries, or industries that enable a strong military or give the United States leverage over other nations. The specific industry for each state was selected using a location quotient (LQ), which measures an industry’s specialization relative to a state’s economy. The LQ is calculated as an industry’s share of a state’s economy divided by the national industry’s share of the U.S. economy or as a state’s share of domestic output in an industry divided by the state’s overall share of the national economy. In this report, the industry’s share of output is calculated using the number of employees in that industry. Each selected industry had a high LQ in its state in 2023.

The state analyses use data from the U.S. Census Bureau’s County Business Patterns to measure employment in each industry at the state level, supplemented by anecdotal evidence on investment and major firms, where available. To examine the relationship between these state industries and Chinese competition, the analyses incorporate data on U.S. and Chinese global market shares, where available; when such data is unavailable, U.S. and Chinese exports as a share of global exports are used as proxies. This approach is supported by Saltarelli et al., who found that “export [data] mirrors remarkably well domestic production for manufacturing sectors or sectors related to physical goods.”[3](#_edn3) Additionally, where applicable, export data was used to assess how the United States and China compete in key third-country markets. Industry exports are calculated using the appropriate Harmonized System (HS) codes and Standard International Trade Classification (SITC) codes.

It should be noted that export data depicts the value of exports from the two countries, not necessarily from U.S. or Chinese firms. For instance, a Tesla facility operating in and exporting products from China will be counted as producing Chinese exports even though Tesla is an American company.

## Alabama: Artificial and Synthetic Fibers and Filaments Manufacturing (NAICS 325220)

Alabama is one of the largest producers of artificial and synthetic fibers and filaments in the country, employing 20 percent of the industry’s workforce. However, the United States is no longer as strong in this industry as it once was. China’s emergence as a low-cost producer has significantly increased competition for American manufacturers and at least partially contributed to the decline of this industry in the United States.

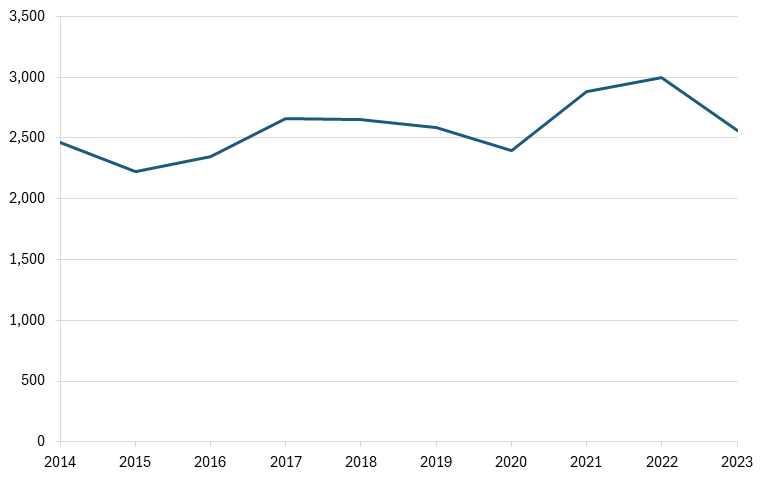

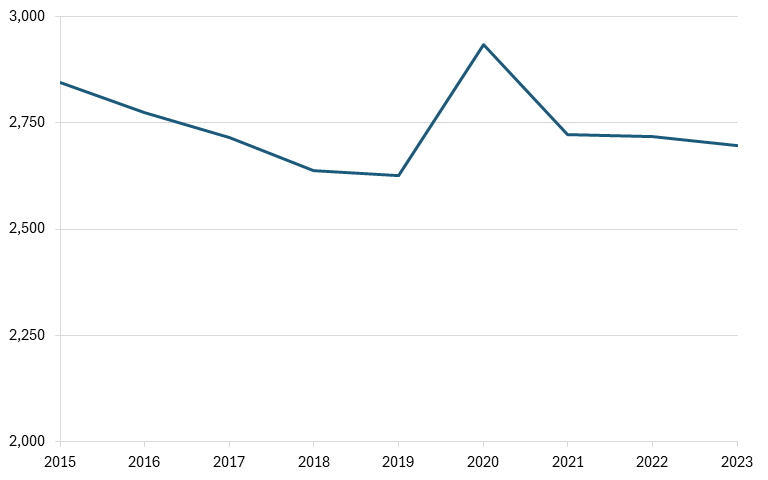

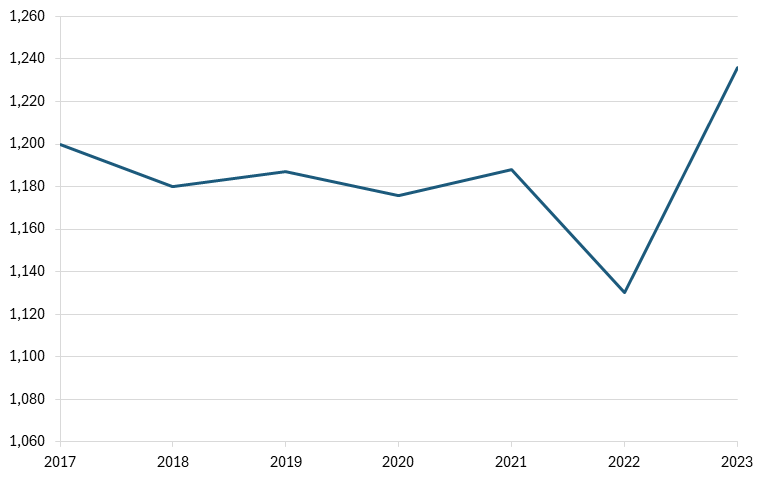

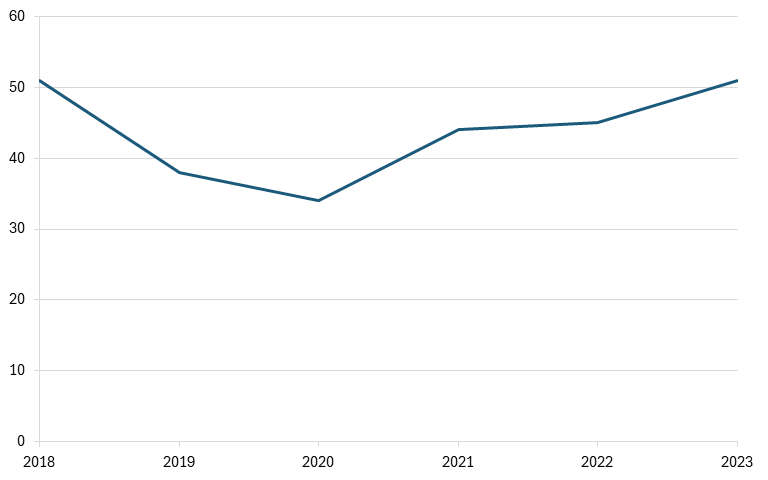

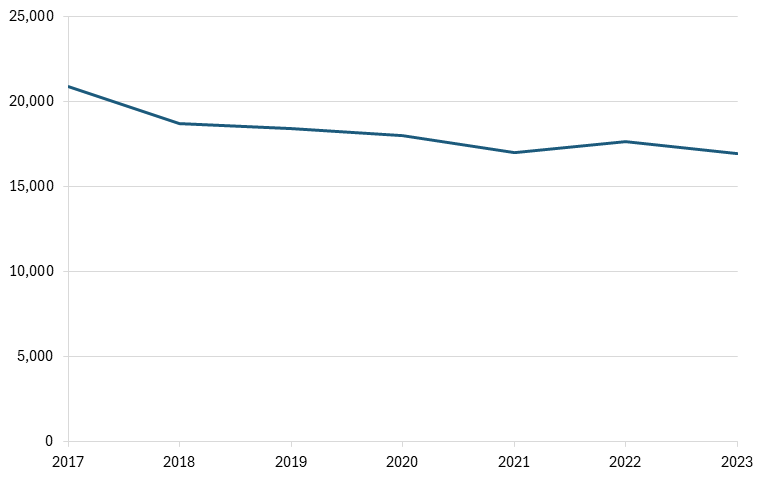

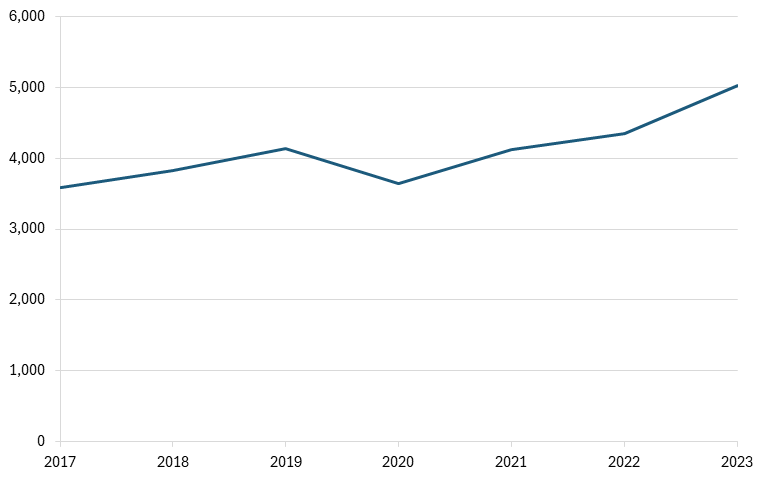

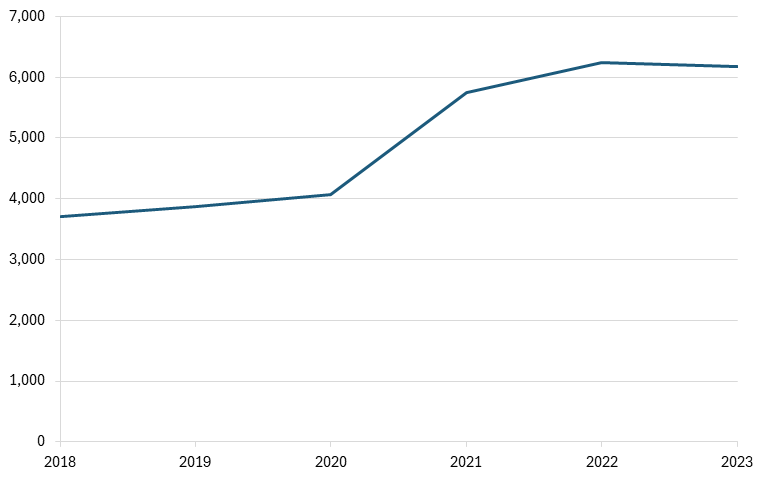

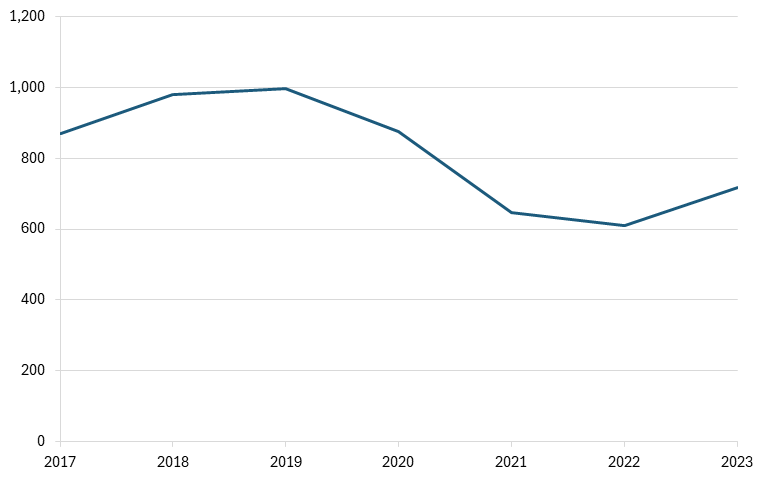

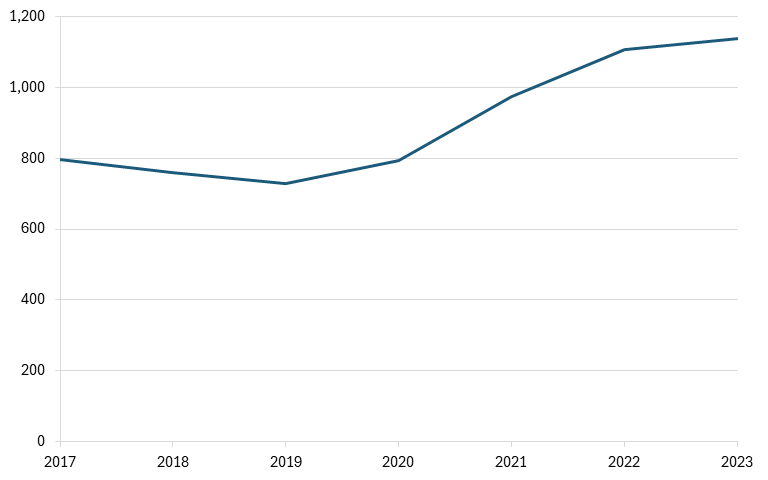

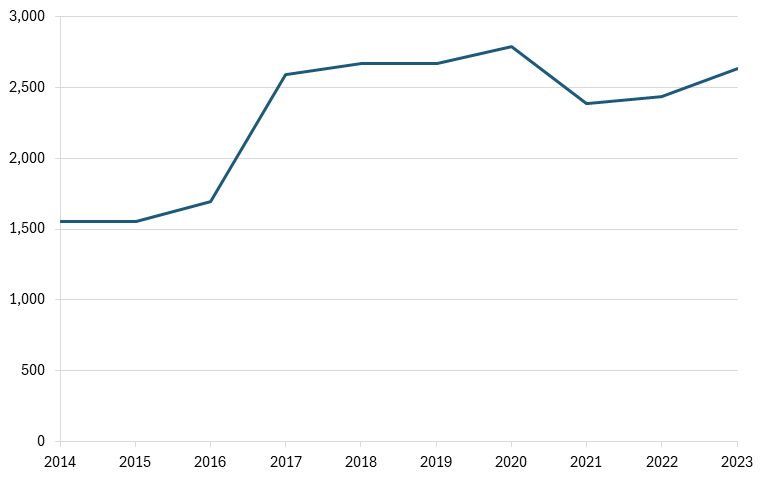

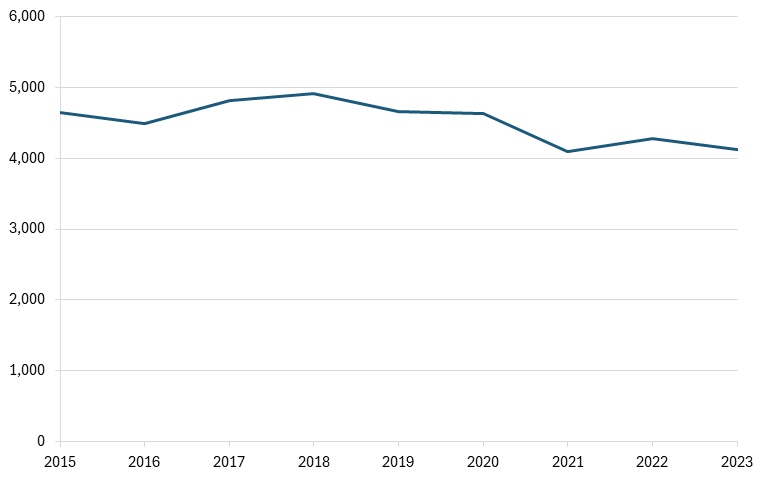

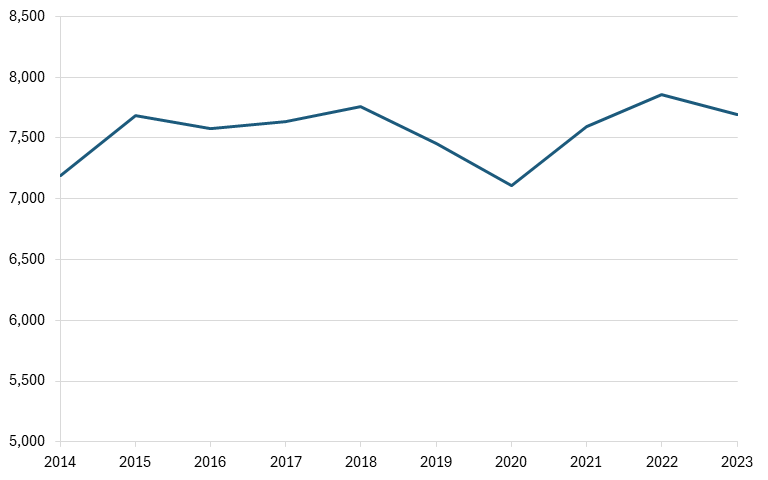

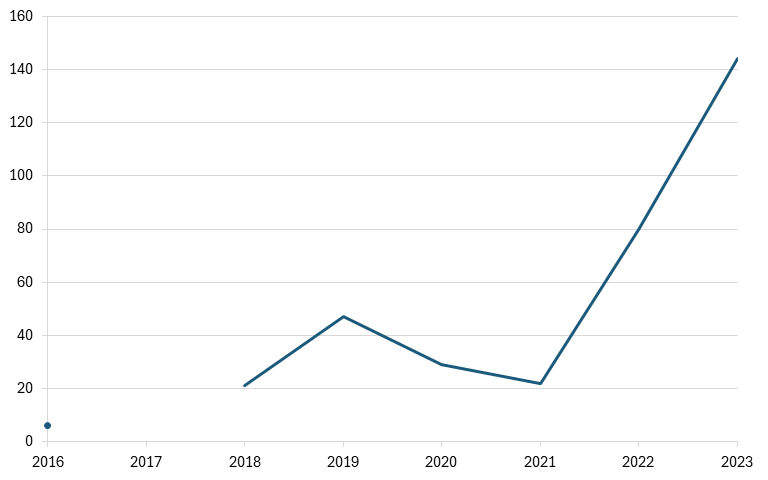

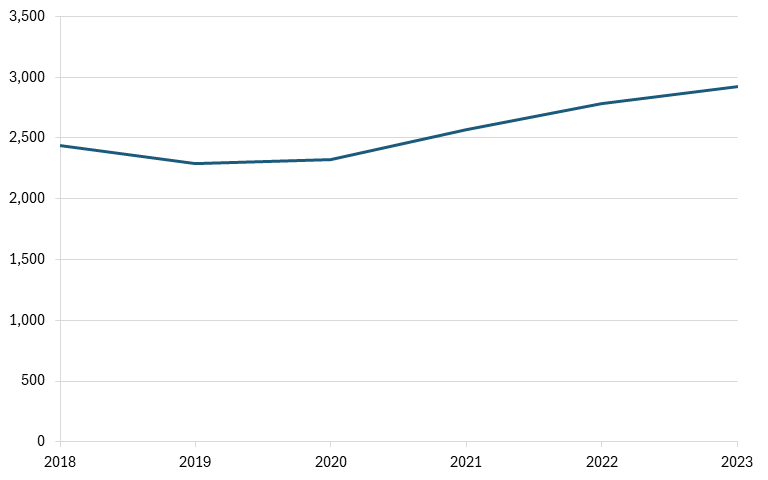

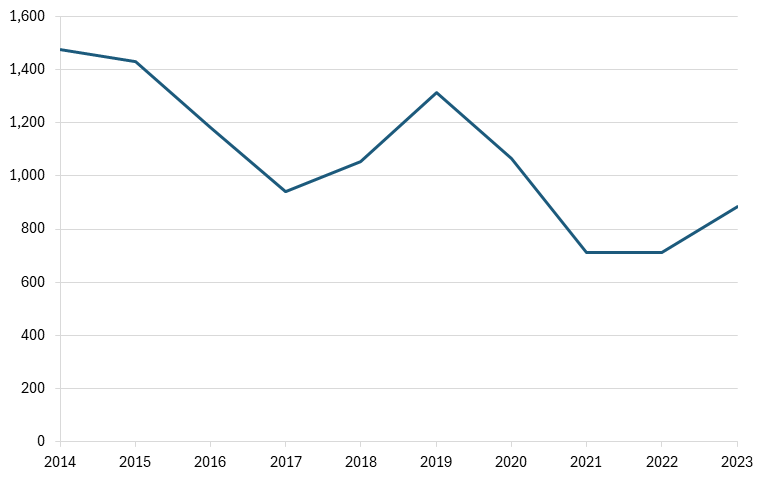

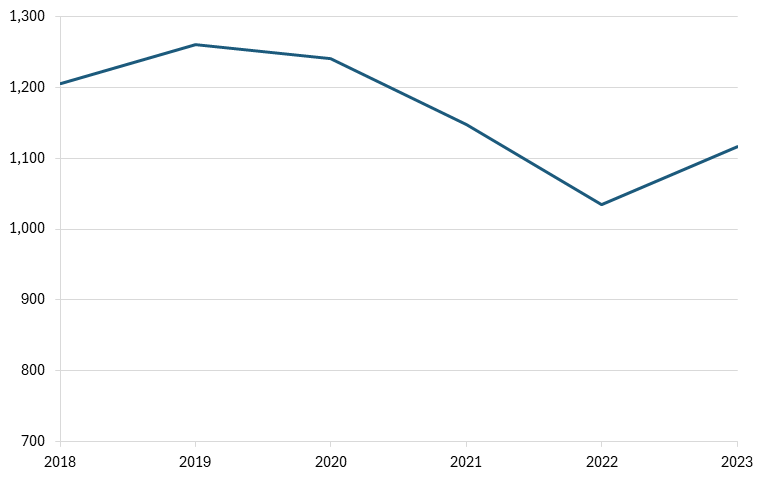

The artificial and synthetic fibers and filaments industry produces several types of man-made fibers, including polyester, nylon, and acrylic, which have industrial uses in addition to their well-known textile uses, such as industrial-strength cables, medical equipment, and personal protective equipment.[4](#_edn4) Alabama is a relatively strong producer of artificial and synthetic fibers in the United States, although employment in the industry has fluctuated over the past decade. From 2013 to 2023, employment fell from 2,500 to as low as 2,200 in the late 2010s, before rising again to a peak of 3,000. As of 2023, Alabama’s artificial and synthetic fibers and filaments industry employed just over 2,500 workers.[5](#_edn5) (See figure 1.)

**Figure 1: Employment in the artificial and synthetic fibers and filaments industry in Alabama**

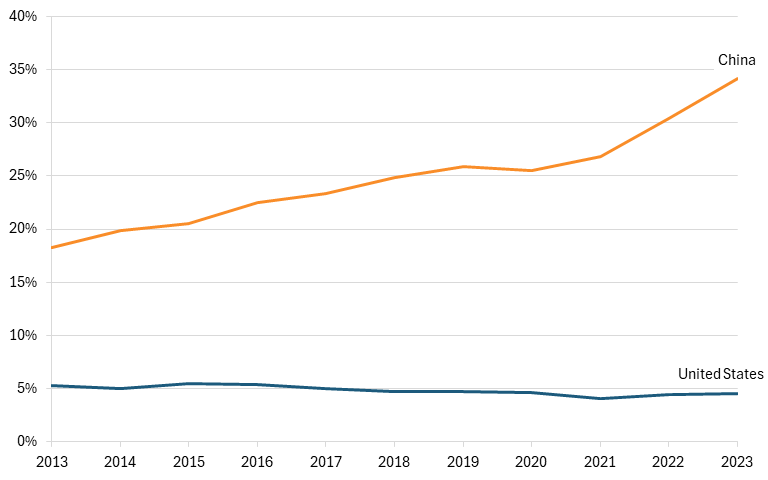

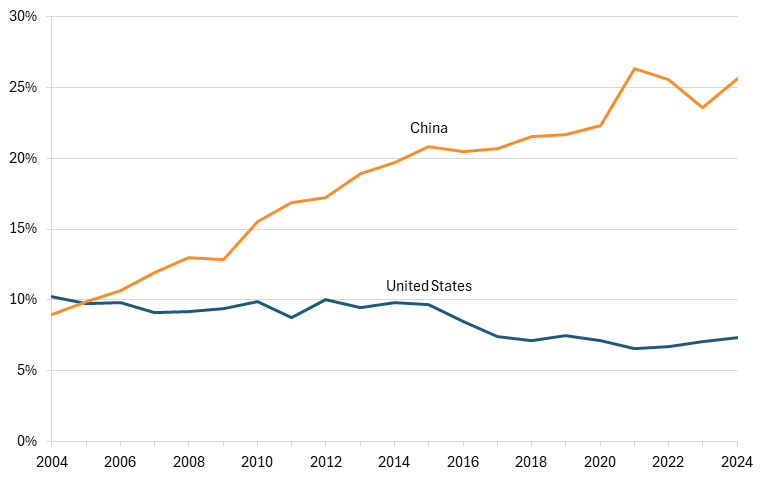

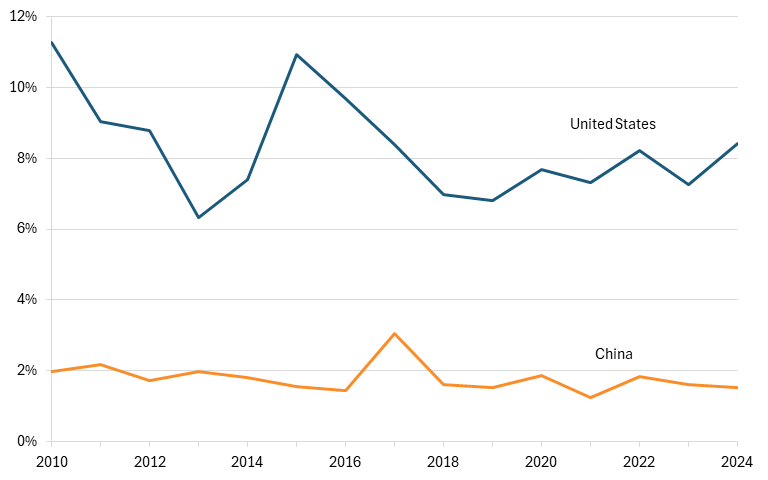

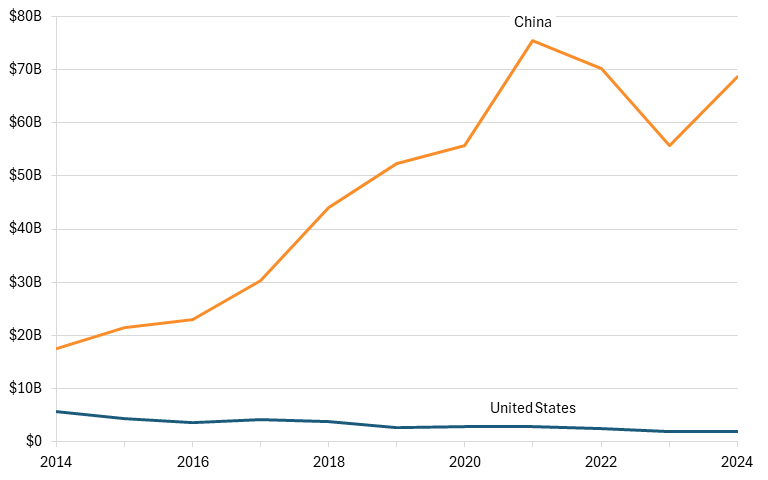

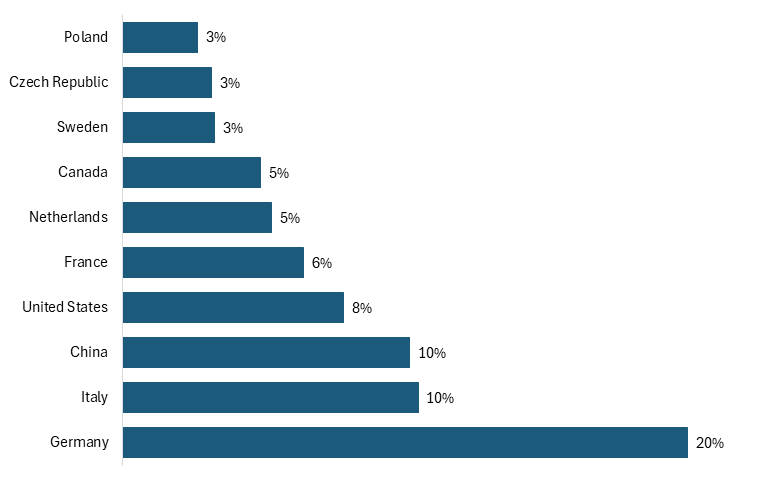

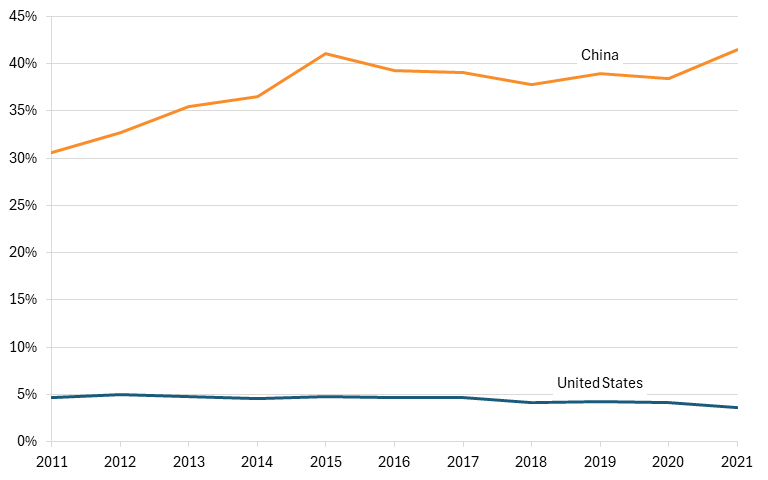

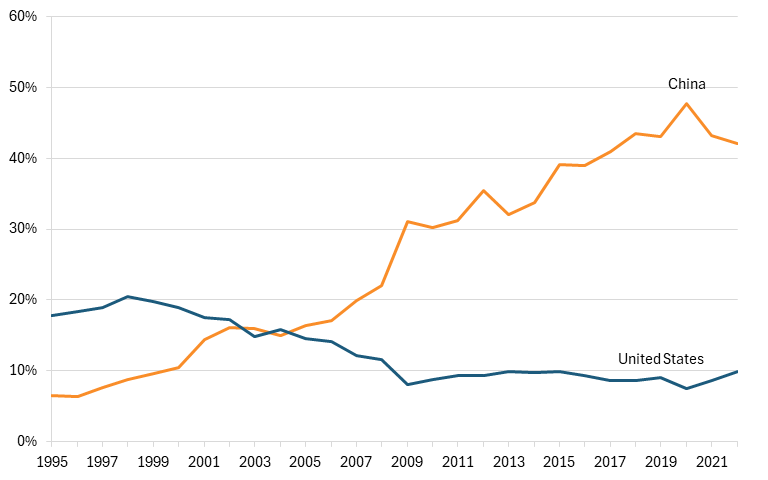

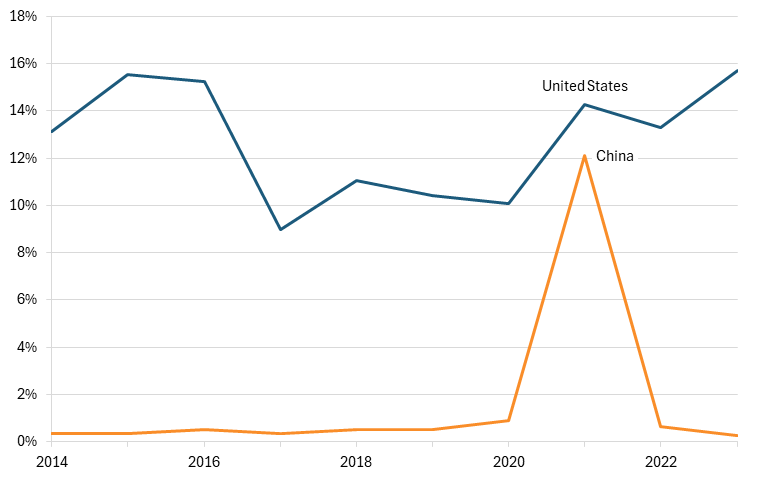

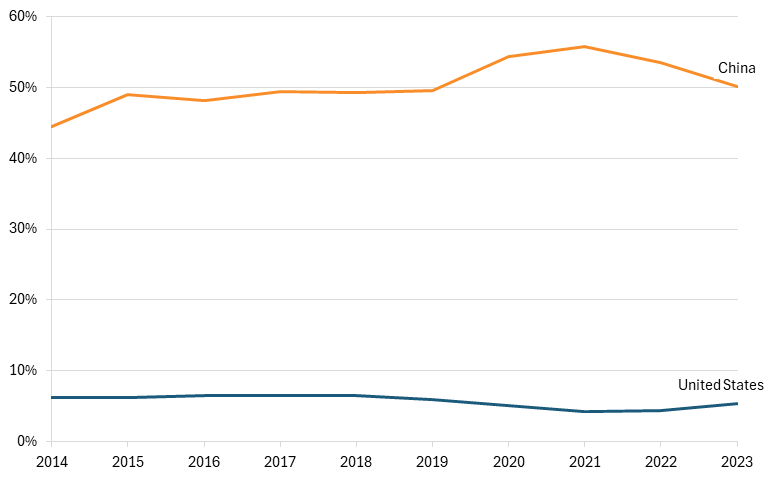

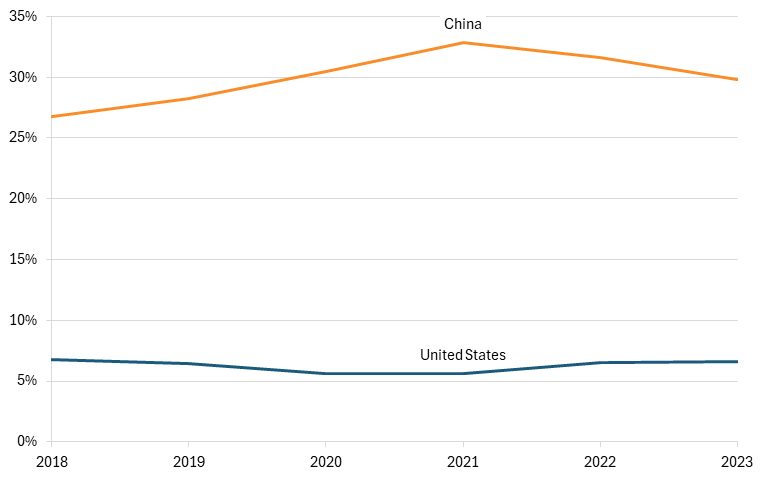

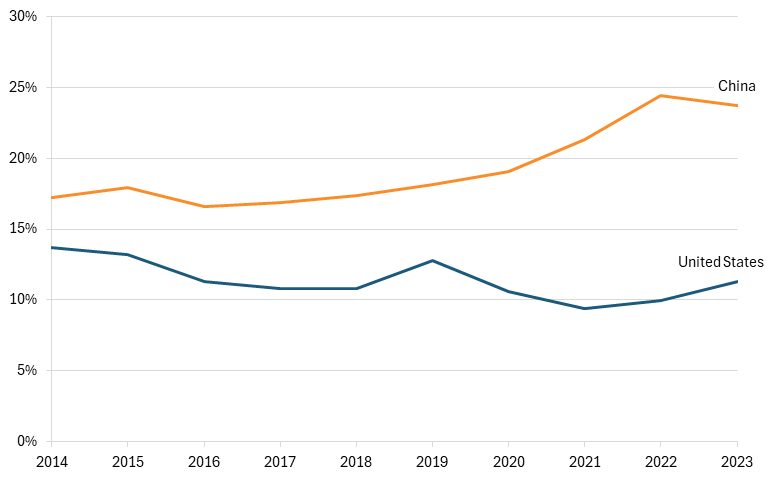

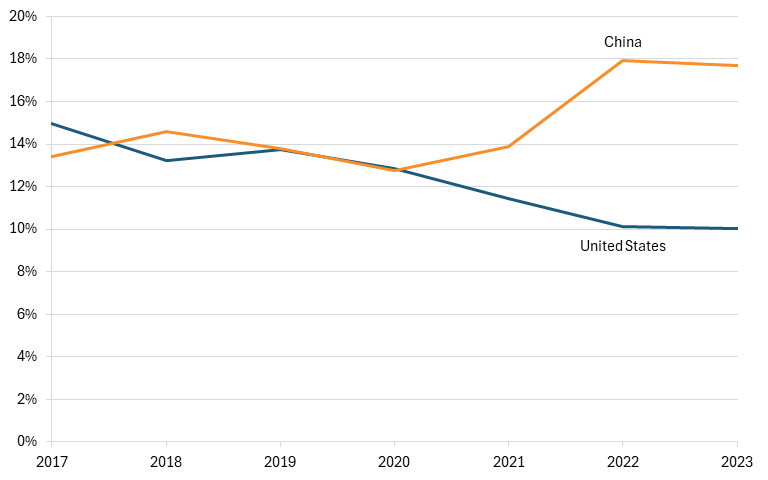

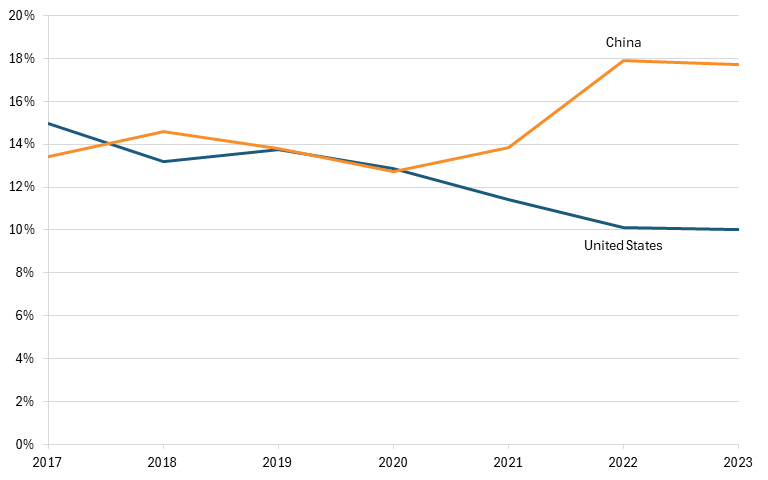

The United States used to be one of the largest producers of man-made fibers. An analysis of HS code 5402, synthetic filament yarn, one of the major exports of firms in these industries, demonstrates that from 1996 to 2000, the United States commanded 11 percent of the global market share in this industry, less than Germany (14 percent) but more than similarly advanced economies such as South Korea and Italy (10 percent each). China maintained less than 1 percent of the global market share. However, China’s accession to the World Trade Organization (WTO) changed this reality. In 2023, China held 48 percent of this growing industry, while U.S. market share more than halved to just 5 percent.[6](#_edn6)

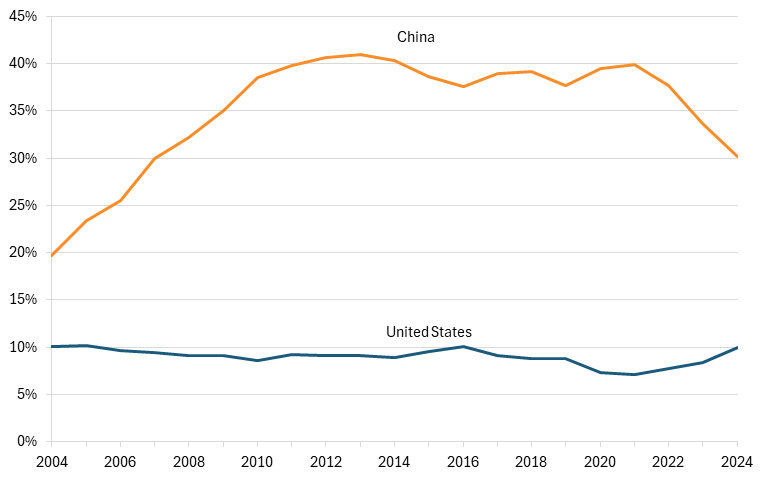

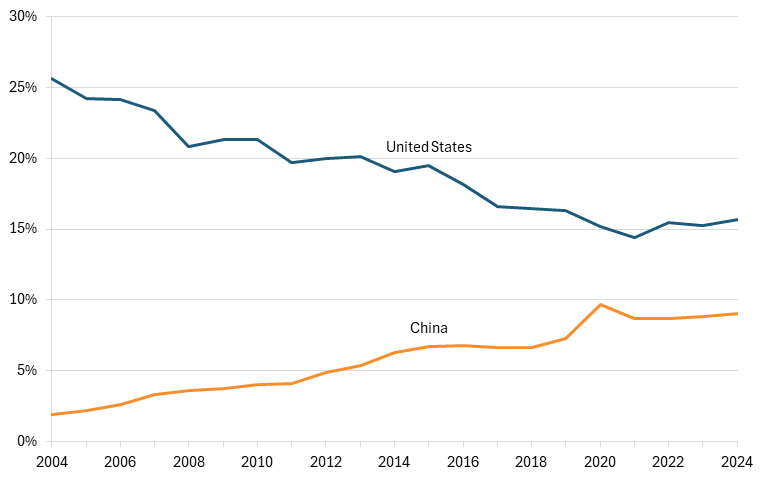

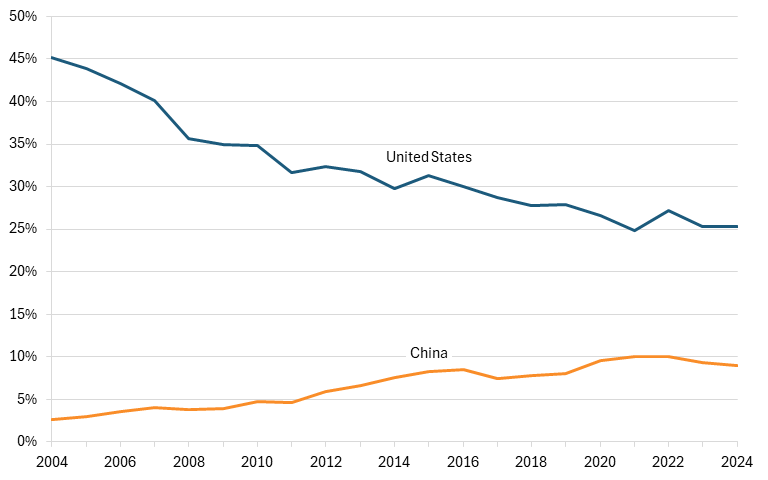

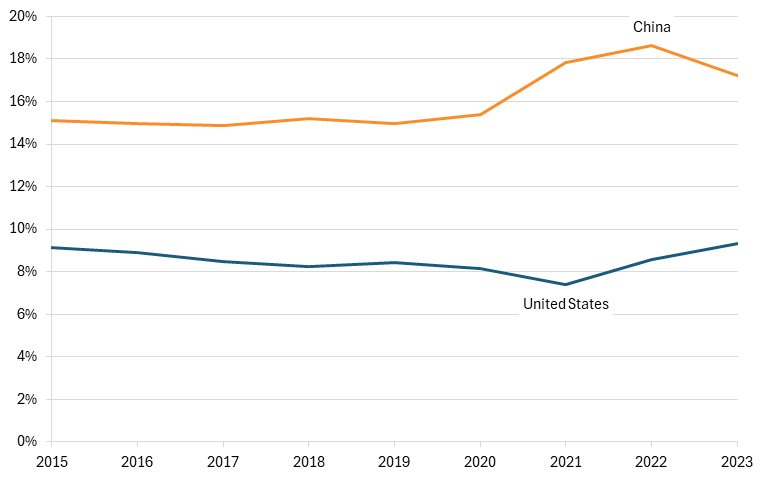

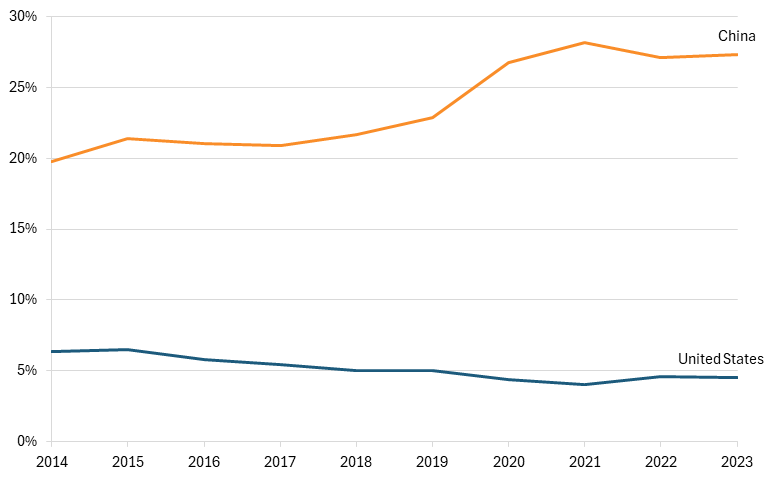

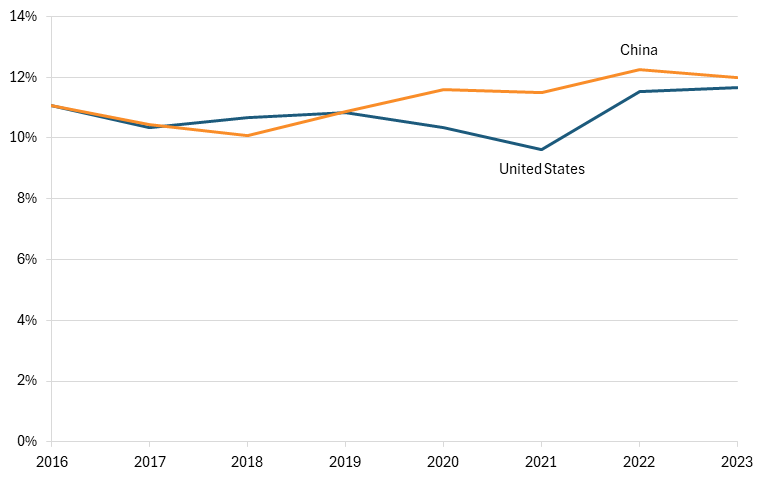

Chinese firms were able to rapidly increase exports and market share through low production pricing and high production levels, both of which reduced the market price of synthetic fibers and squeezed U.S. producers. Today, U.S. production of synthetic fibers has declined by 74 percent since its peak in 1996.[[7]](#_edn7) China holds over one-third of global market share across all goods produced by the synthetic fiber industry (HS 54 and 55), an increase of 86 percent from 2013 to 2023. At the same time, the United States has seen its global market share fall to just 4.6 percent.[8](#_edn8) (See figure 2.)

**Figure 2: Global market share of synthetic fiber exports**

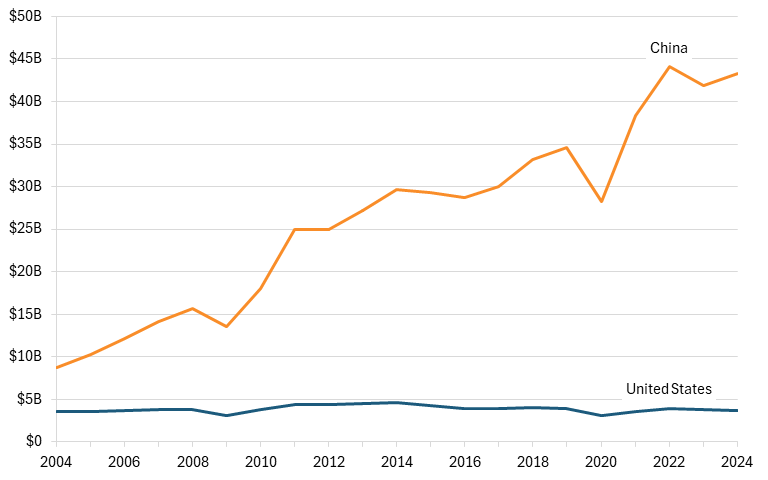

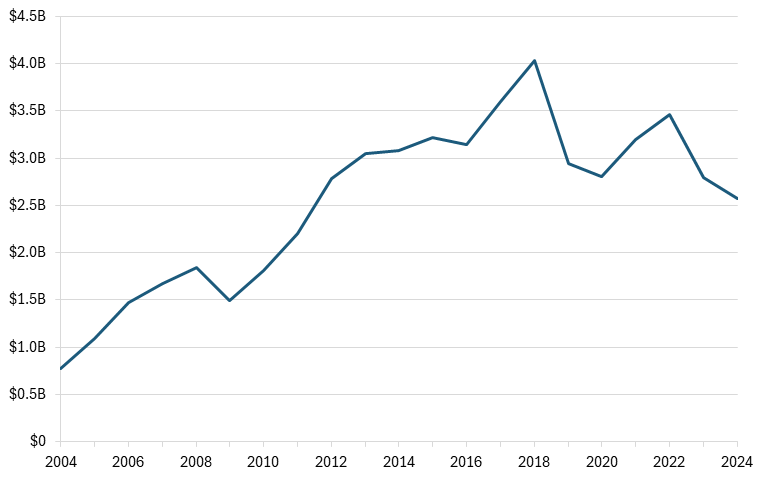

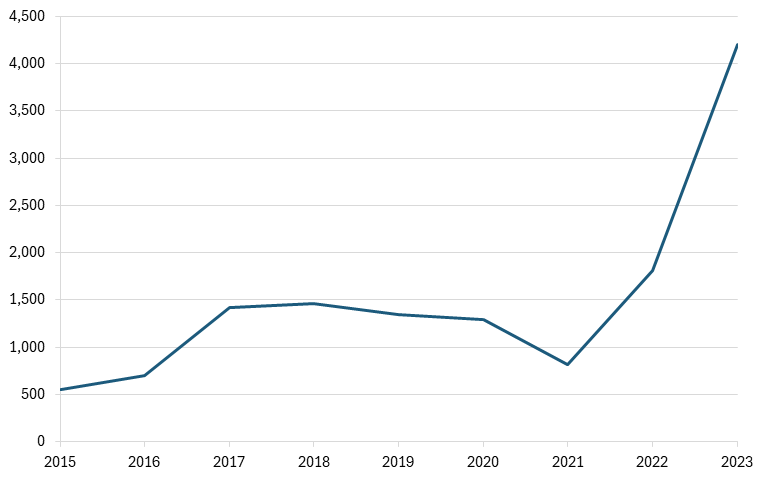

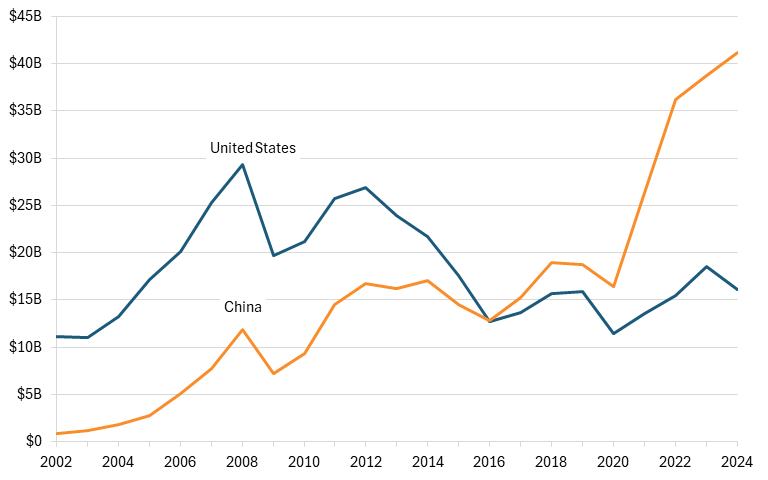

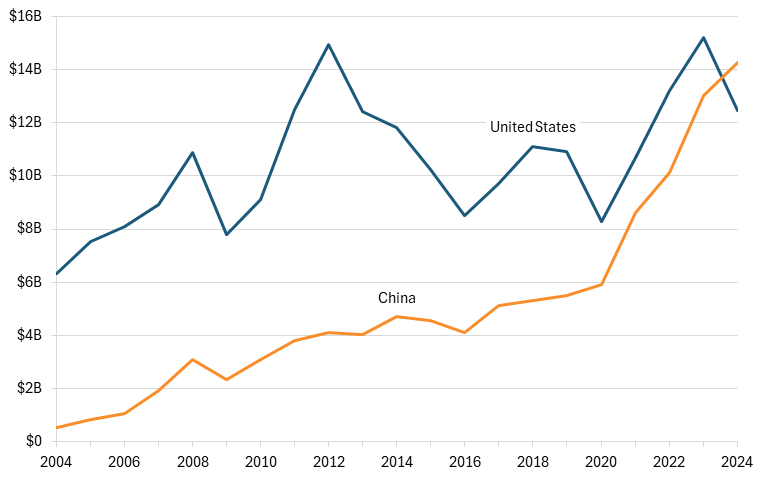

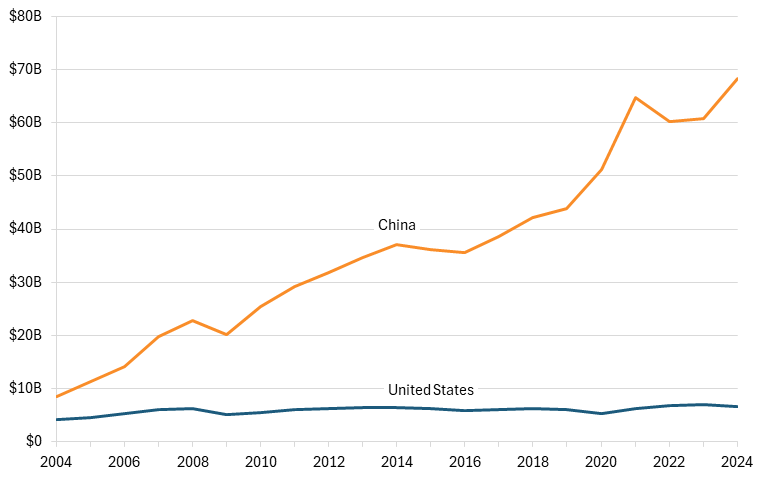

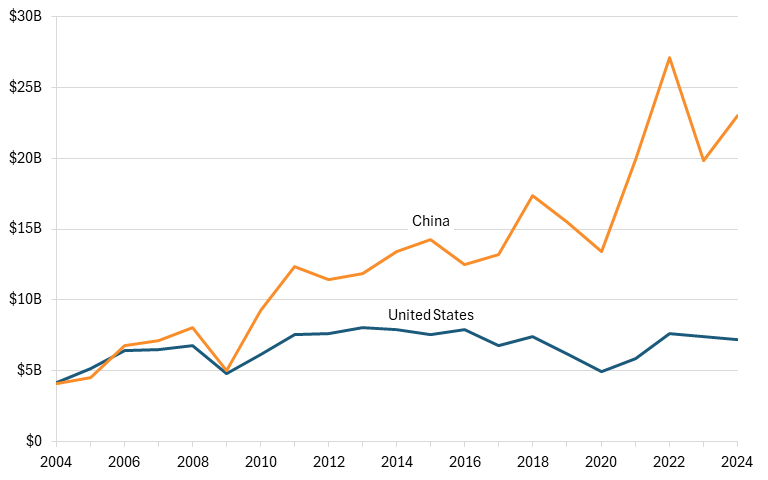

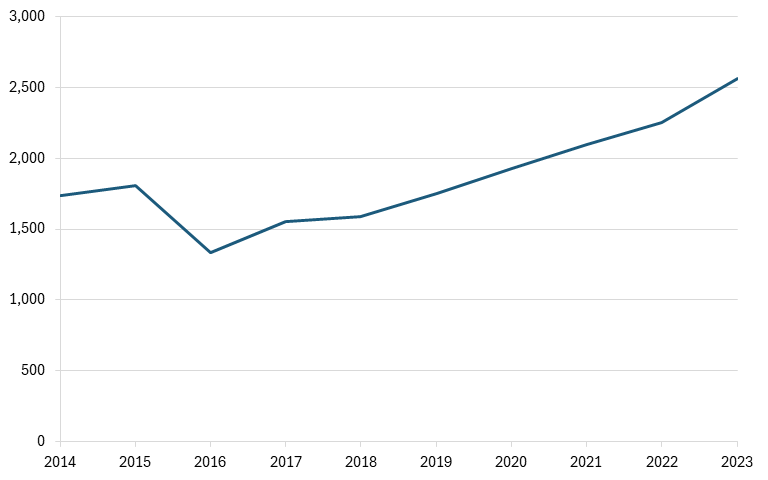

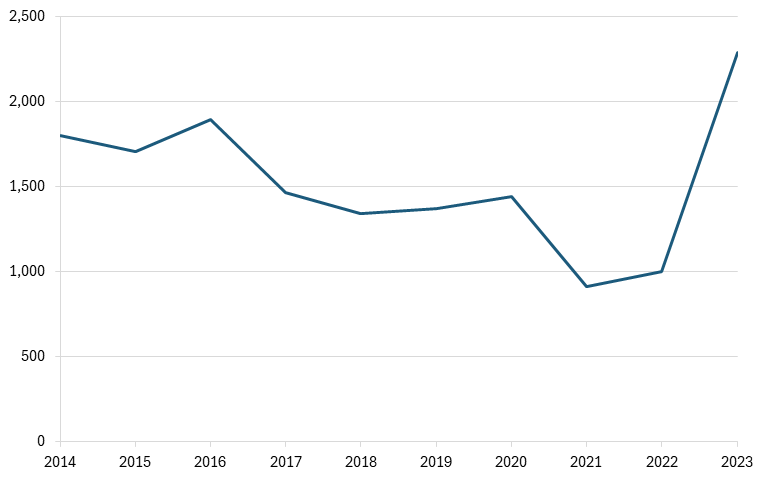

The market for synthetic fibers has grown steadily since the late 1990s, more than doubling since 1996.[9](#_edn9) However, this growth has not been distributed evenly. Chinese exports in the synthetic fiber industry (HS 54 and 55) were only about $4 billion greater than U.S. exports in 2004. By 2024, Chinese exports had surged, with exports increasing by 398 percent to over $40 billion. For the United States, exports have remained stagnant or declined every year since the early 2000s, with exports increasing just 3 percent.[[10]](#_edn10) (See figure 3.)

**Figure 3: Artificial and synthetic fiber (HS 54 and 55) exports**

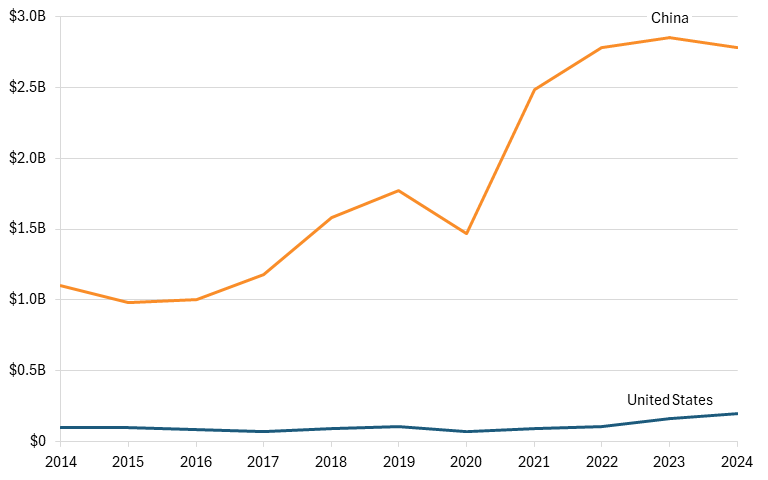

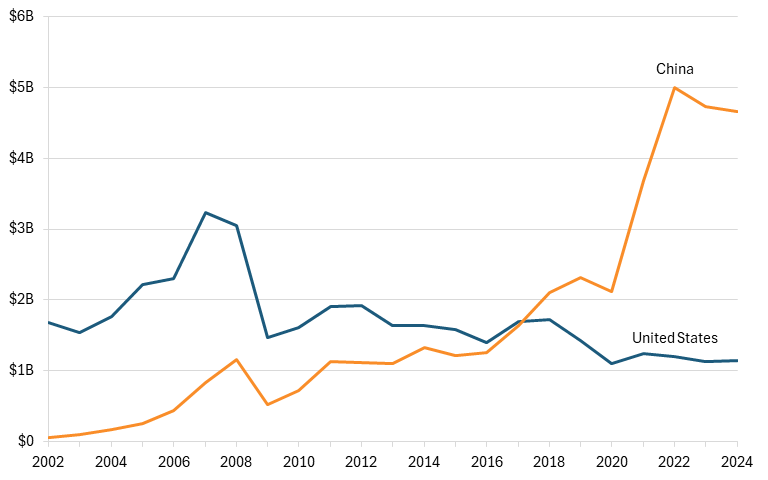

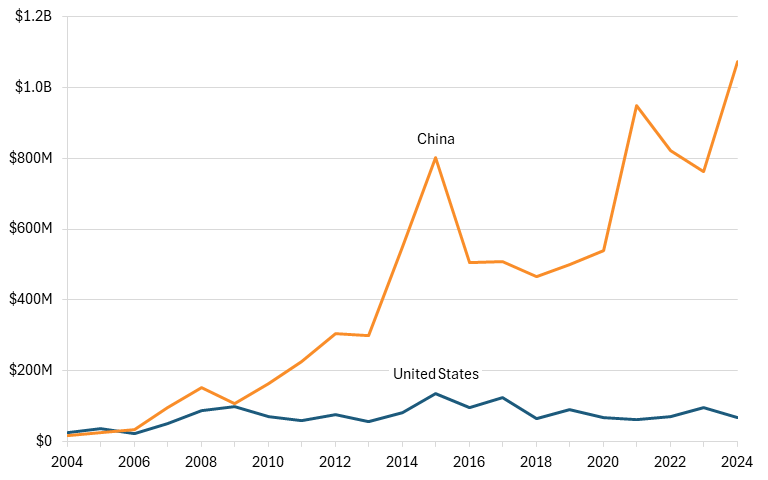

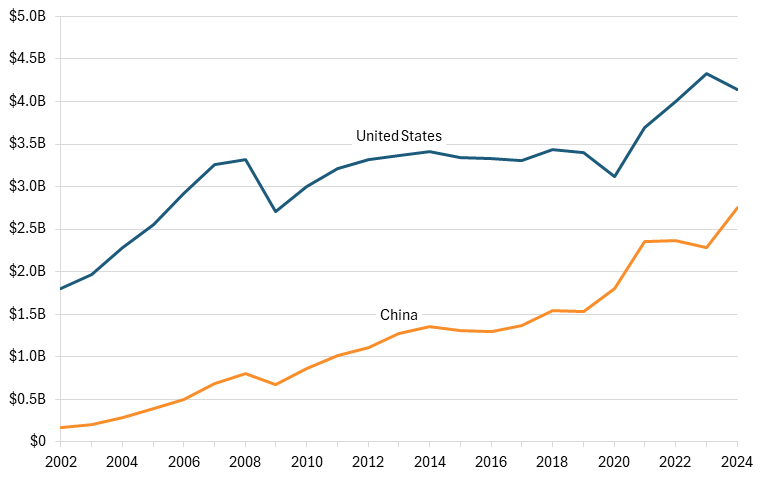

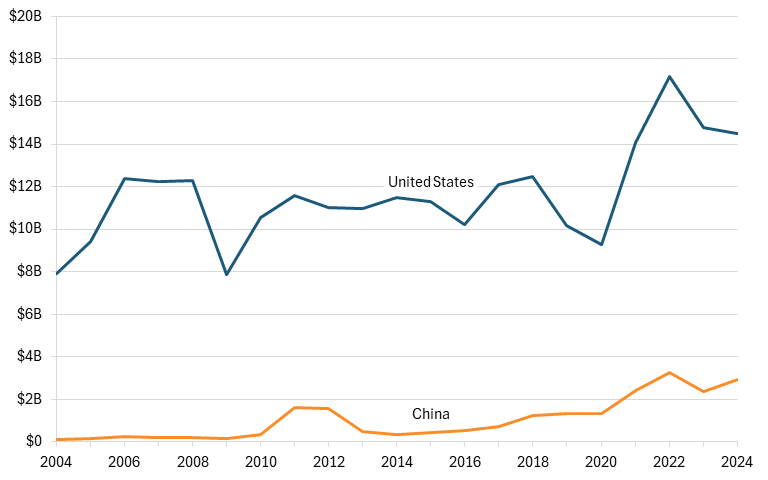

China’s rapid growth in global market share is only possible through the domination of third-party markets. Large textile-exporting countries are importers of synthetic fibers, making them key markets for firms in that industry. Exports to Bangladesh, India, Italy, and Vietnam—four of the five largest exporters of textiles in the world—were dominated by China.[11](#_edn11) China exported $2.8 billion worth of synthetic fibers to these countries in 2024, while U.S. exports totaled just 7 percent of that, or $199 million.[12](#_edn12) (See figure 4.)

China’s rise as one of the top exporters of synthetic fibers in the world correlates with the subsequent decline in the U.S. synthetic fiber industry. The industry in the United States has seen its workforce, which used to be over 17,500 workers, fall by 25 percent and output decline steeply, leaving U.S. firms insignificant in the global market, far overshadowed by Chinese competitors.[[13]](#_edn13) The evidence indicates that China’s accession to the WTO, and the free trade protections that came with it, allowed Chinese firms to overproduce and underprice goods, enabling them to gain global market share at the expense of the United States and making it a contributor to the decline of the synthetic fibers industry in Alabama.

**Figure 4: Synthetic fiber exports to Bangladesh, India, Italy, and Vietnam**

## Alaska: Metal Tank (Heavy Gauge) Manufacturing (NAICS 332420)

Alaska’s metal tank (heavy gauge) manufacturing industry plays a small but important role in supporting the state’s energy, mining, and infrastructure sectors. These tanks—used for storing petroleum, chemicals, and water—are critical inputs for Alaska’s resource-based economy. However, like many U.S. fabricated metal product industries, the sector operates in an increasingly competitive global market wherein China’s rapid expansion, supported by state-backed industrial policies, presents a growing challenge.

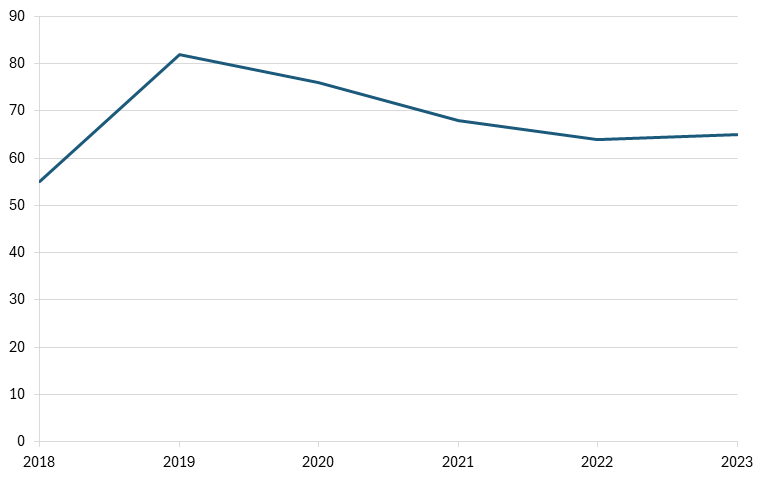

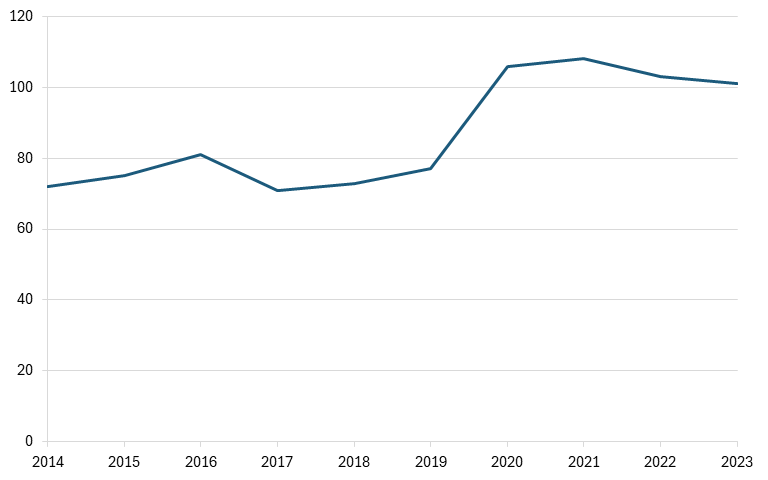

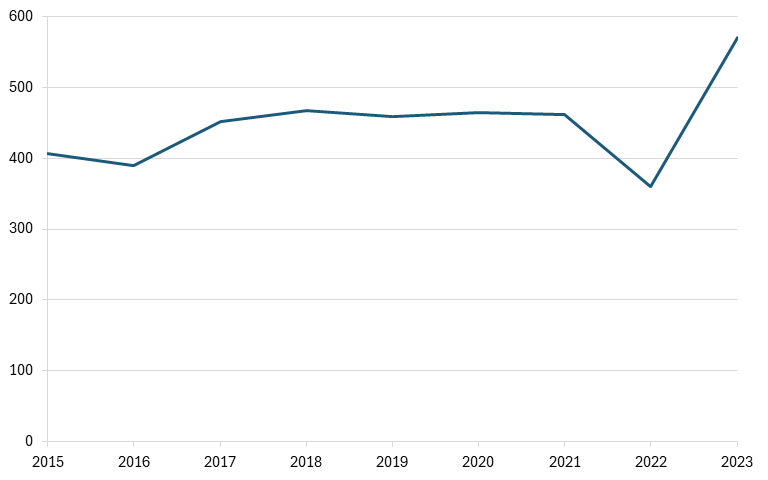

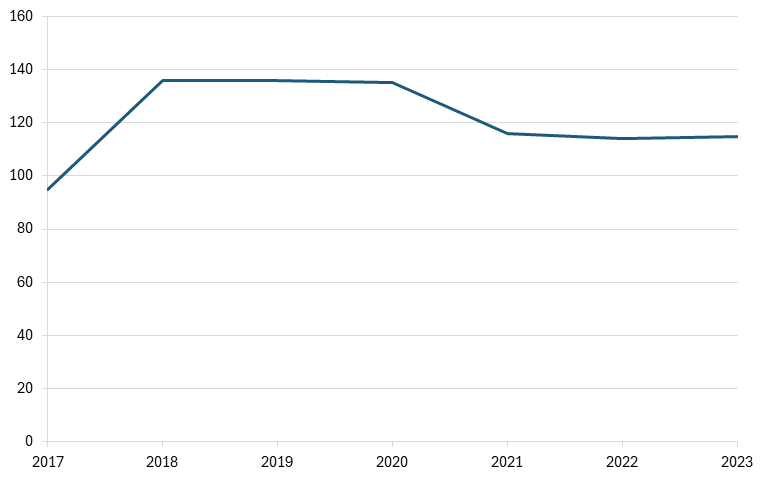

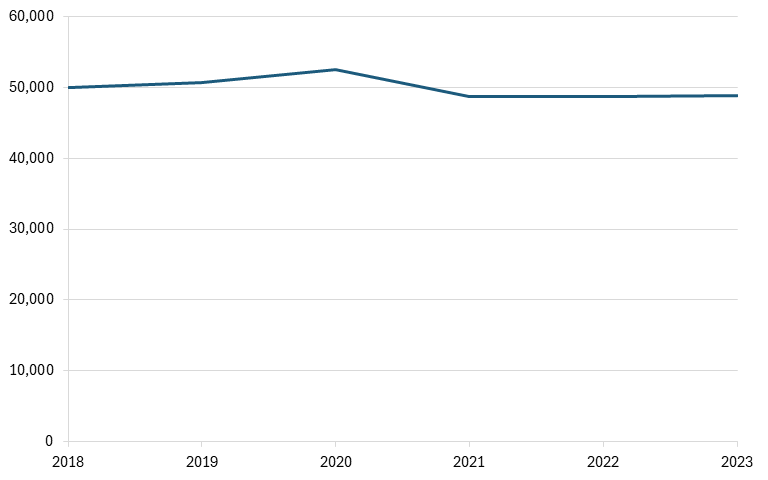

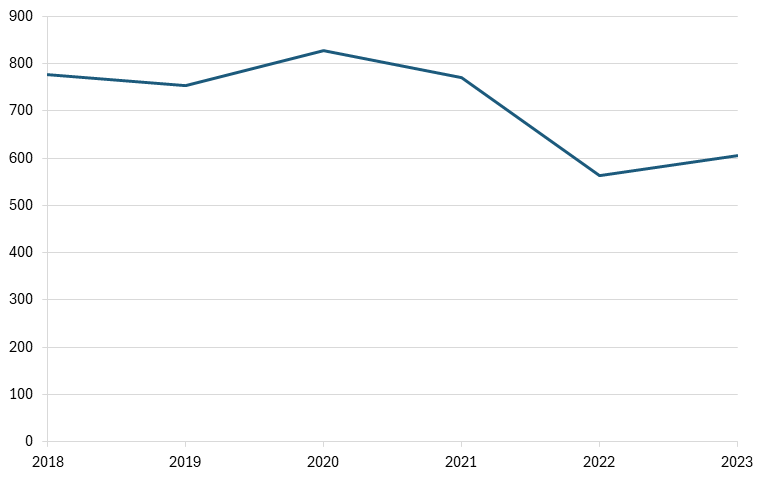

While Alaska is not a large manufacturing state, its metal tank industry is closely tied to oil and gas activity and broader industrial demand. Employment in the industry has fluctuated over the past several years, rising from roughly 55 workers in 2018 to a peak of over 80 in 2019 before declining and stabilizing around the mid-60s by 2023.[14](#_edn14) (See figure 5.)

**Figure 5: Number of jobs in metal tank (heavy gauge) manufacturing in Alaska**

Despite its localized importance, the U.S. metal tank manufacturing industry remains a relatively small player globally compared with China. Fabricated metal products, including storage tanks (HS codes 7309, 7311, 7611, 7613, 8609), have seen China emerge as a dominant exporter over the past two decades. Chinese firms benefit from economies of scale, vertically integrated steel supply chains, and extensive government support, allowing them to produce tanks and related fabricated metal products at lower cost than U.S. competitors.[15](#_edn15)

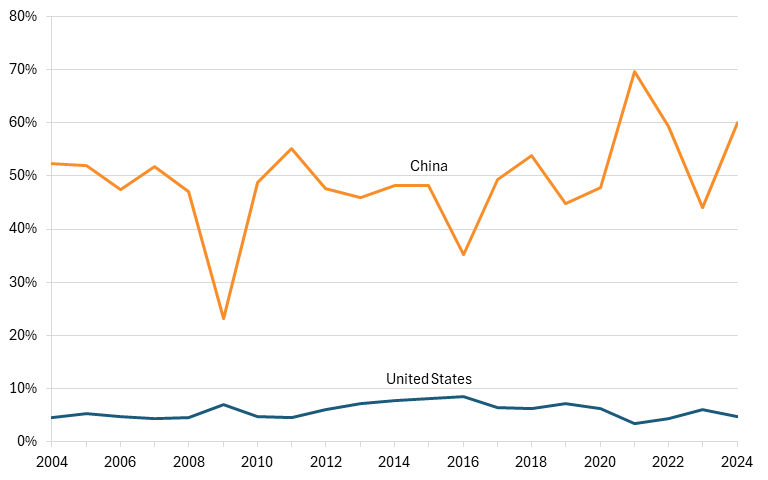

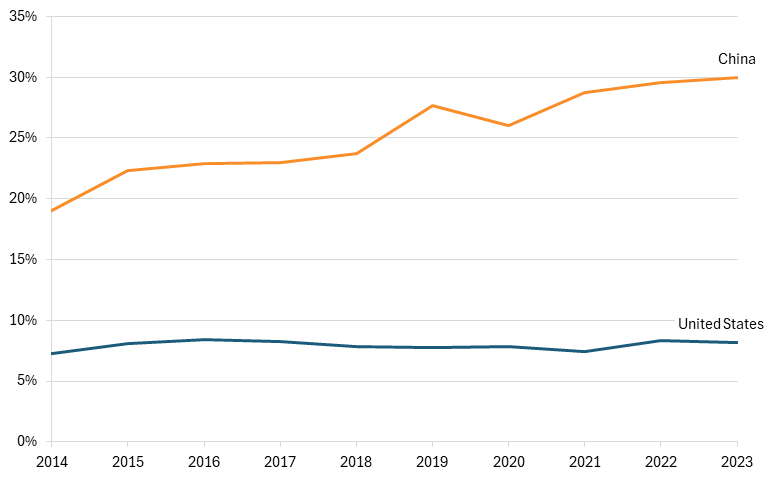

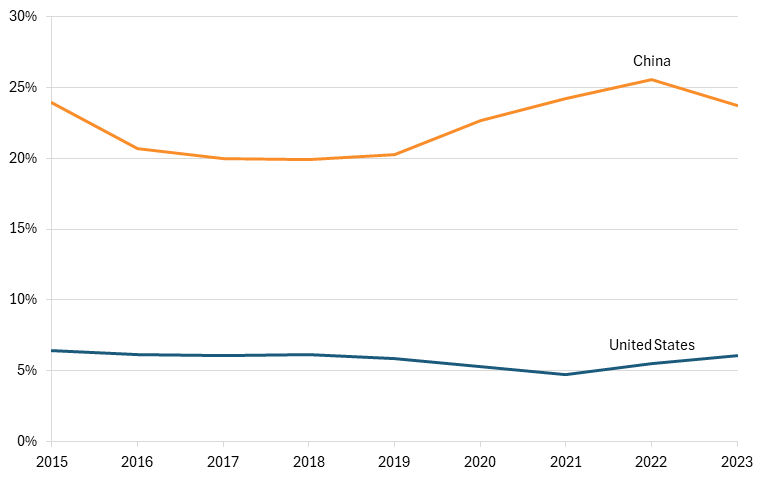

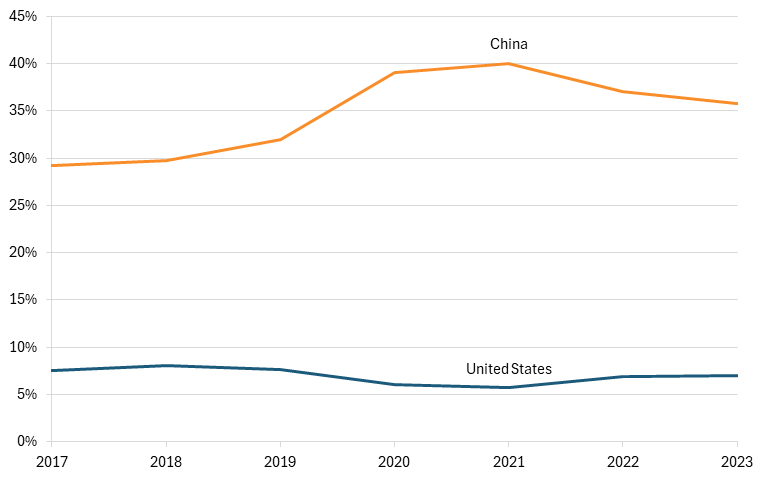

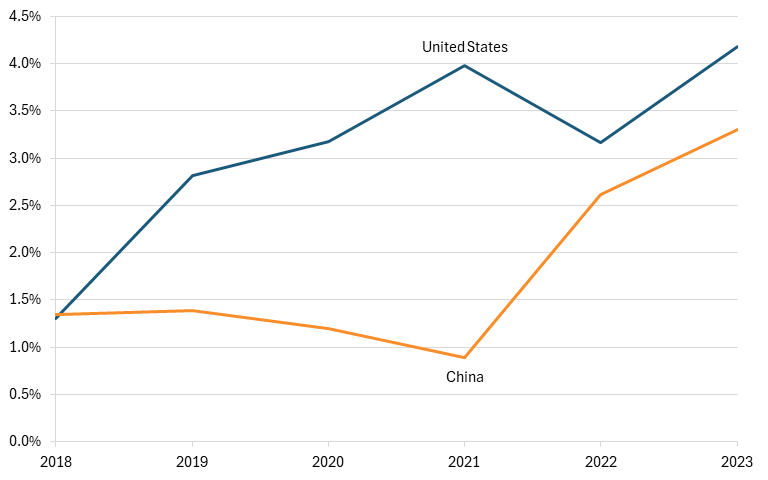

China’s rise is particularly evident in export market share. Since the early 2000s, China has consistently captured a significantly larger share of global exports of metal tanks than the United States has. While China’s export share has fluctuated largely between roughly 40 and 70 percent over the past two decades, the United States has remained in the single digits, typically below 10 percent.[16](#_edn16) (See figure 6.) These trends also largely correspond to Alaska’s employment trends over the past several years, with employment remaining relatively stagnant, similar to U.S. exports.

**Figure 6: United States’ and China’s shares of global exports of heavy-gauge metal tank manufacturing**

China’s global dominance in fabricated metal products is closely tied to state support. Under industrial strategies such as Made in China 2025, the Chinese government has prioritized advanced manufacturing sectors, including metals and industrial equipment. Chinese metal producers benefit from a range of subsidies, including below-market financing from state-owned banks, discounted land and energy, export tax rebates, and direct fiscal support. According to the Organization for Economic Cooperation and Development (OECD), government support for Chinese metal producers is significantly higher than for firms in market economies, contributing to persistent global overcapacity and downward pressure on prices.[[17]](#_edn17) This allows Chinese firms to undercut international competitors, sometimes selling products at or near cost.

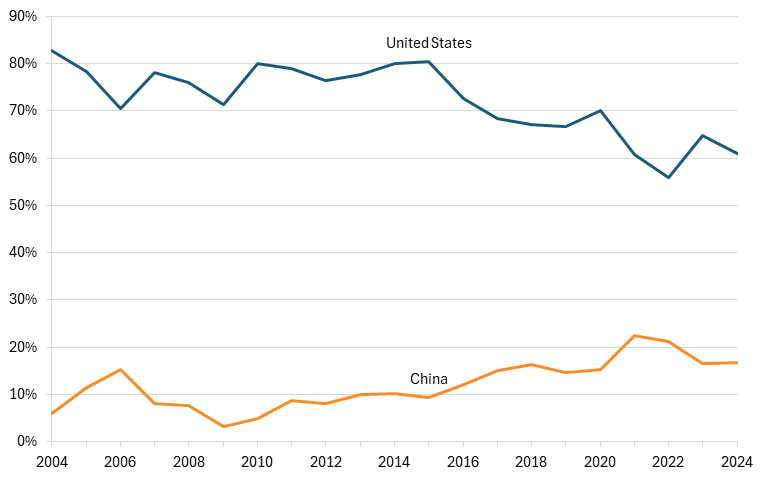

The competitive pressure from China is also visible in key export markets. The United States has traditionally exported metal tanks primarily to neighboring countries, particularly Canada and Mexico. Over the past two decades, however, China has steadily increased its presence in these markets. While the United States still maintains a dominant share—often accounting for 60 to 80 percent of exports to these countries—China’s share has risen from less than 6 percent to the mid-teens and, in some years, above 20 percent, suggesting that U.S. firms are facing growing competition from lower-cost Chinese competitors.[18](#_edn18) (See figure 3.)

**Figure 7: United States’ and China’s shares of heavy-gauge metal tank exports to Mexico and Canada**

Overall, while Alaska’s metal tank manufacturing industry is relatively small, it remains exposed to global competitive pressures. China’s continued expansion in fabricated metal products—fueled by subsidies, overcapacity, and export-oriented industrial policy—poses a long-term risk to U.S. producers. For Alaska, where the industry supports critical energy and infrastructure activities, sustained competition from lower-cost imports could limit growth, reduce margins, and constrain job creation. Ensuring the resilience of this niche-yet-essential manufacturing sector will depend on maintaining domestic industrial capabilities amid intensifying global competition.

## Arizona: Semiconductor and Related Device Manufacturing (NAICS 334413)

Arizona is specialized in and dependent on the semiconductor industry, which operates in a highly competitive global market. China’s extensive subsidies and continued rapid expansion of manufacturing capacity pose a challenge to the sector’s future success.

The semiconductor industry is the second-largest traded industry in Arizona, behind the aerospace sector, contributing over $3.5 billion in exports.[19](#_edn19) Employment in this industry has surged in recent years due to sizeable investments in the greater Phoenix area from some of the largest semiconductor firms in the world, such as Intel and Taiwan Semiconductor Manufacturing Corporation (TSMC). These investments contributed to a 61 percent increase in employment between 2015 and 2023, with the largest jump occurring in 2022, the year the CHIPS and Science Act was passed.[20](#_edn20) (See figure 8.) These investments have also made Arizona one of the largest hubs for semiconductor manufacturing in the United States.

**Figure 8: Employment in semiconductor manufacturing in Arizona**

However, while investment in the Arizona semiconductor industry has been significant, the Chinese government has invested even more, threatening to take global market share from American producers. Through substantial subsidies and overproduction, Chinese firms are suppressing semiconductor prices, gaining global market share, and potentially harming the future success of Arizona fabs. Overall, the Chinese government plans to invest over $150 billion in the industry by 2030, nearly three times the $52 billion invested by the United States in the CHIPS and Science Act in 2022.[[21]](#_edn21) In the first half of 2025 alone, the government invested $63.3 billion in the industry.[22](#_edn22)

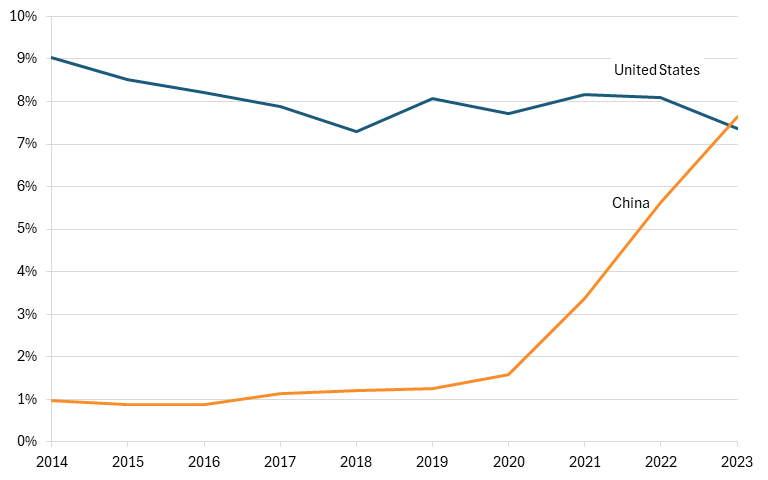

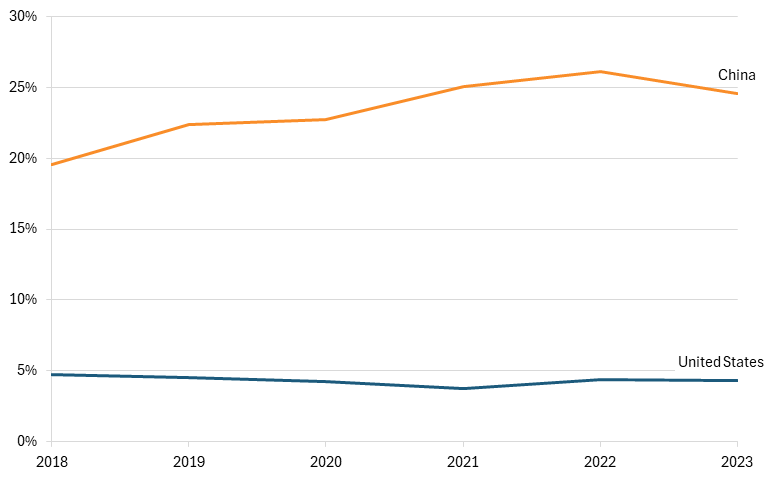

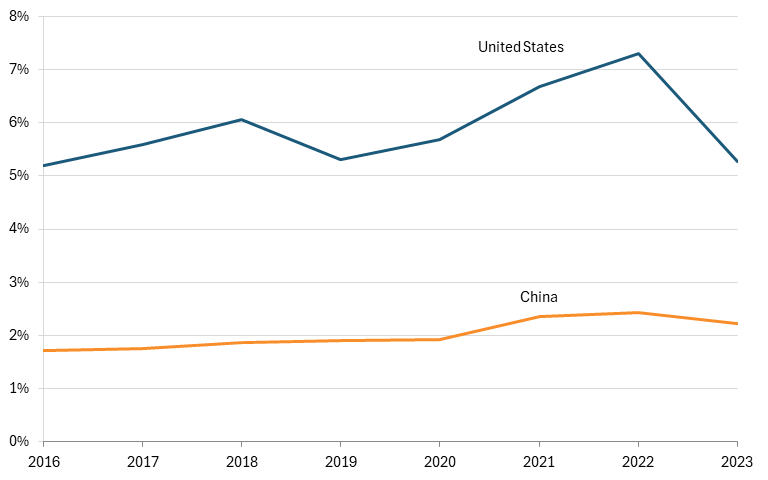

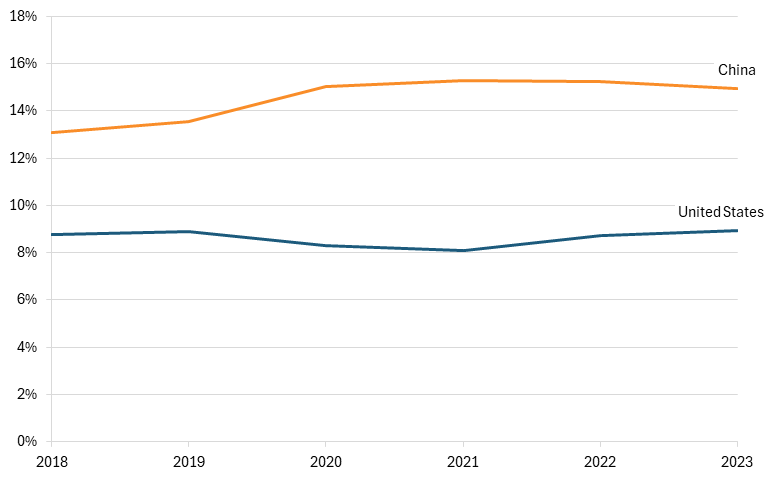

China’s push for dominance in semiconductors is most evident in legacy semiconductor manufacturing, which has benefited from significant industrial subsidies and has grown faster than the rest of the global market. Chinese legacy chip production capacity grew more than four times as fast as global demand between 2015 and 2023.[23](#_edn23) Continually increasing production capacity without corresponding demand growth can result in overcapacity, which reduces prices and revenue for U.S. chip manufacturers. In terms of overall semiconductor production capacity, China’s stock has been rising at the expense of the United States, disproportionately affecting areas highly concentrated in semiconductors, such as Arizona. Between 2000 and 2025, China’s share of global semiconductor manufacturing capacity increased by 20 percentage points, while the United States saw its share decline by 8 percentage points.[[24]](#_edn24) (See figure 9.)

**Figure 9: Share of global semiconductor production capacity, 2000–2032 (projected from 2025)**

For much of the early 2000s, the United States exported far more semiconductors (HS codes 8541 and 8542) than China did. However, from 2009 until the present, China has overtaken the United States, with exports growing exponentially while U.S. exports have remained stagnant. From 2014 to 2024, Chinese semiconductor exports grew by 126 percent, while U.S. exports increased by just 37 percent.[25](#_edn25) (See figure 10.) Indeed, TSMC’s $165 billion investment to support the construction of six fabs in Arizona, most of which are not yet operational, will likely increase U.S. exports as more fabs come online.[26](#_edn26) However, the U.S. Commerce Department has noted that China’s chip industry expansion poses a threat to new chip facilities in the United States, stating that new Chinese chip capacity could result in fabs in the United States and other allied countries being reduced to producing fewer chips than is necessary to remain profitable.[[27]](#_edn27)

**Figure 10: Semiconductor exports**

The high subsidies in the Chinese semiconductor industry allow Chinese firms to sell semiconductors at a lower cost than U.S. competitors can, at times selling chips below production cost. Chinese manufacturers sell chips 30 to 50 percent cheaper than U.S. suppliers do, making their products more attractive in third-party markets.[28](#_edn28) U.S. exports to Malaysia, Singapore, and Vietnam have grown at a fraction of the pace of China’s, with Chinese exports to these countries close to double that of the United States in 2024. (See figure 11.)

**Figure 11: Semiconductor exports to Malaysia, Singapore, and Vietnam[29](#_edn29)**

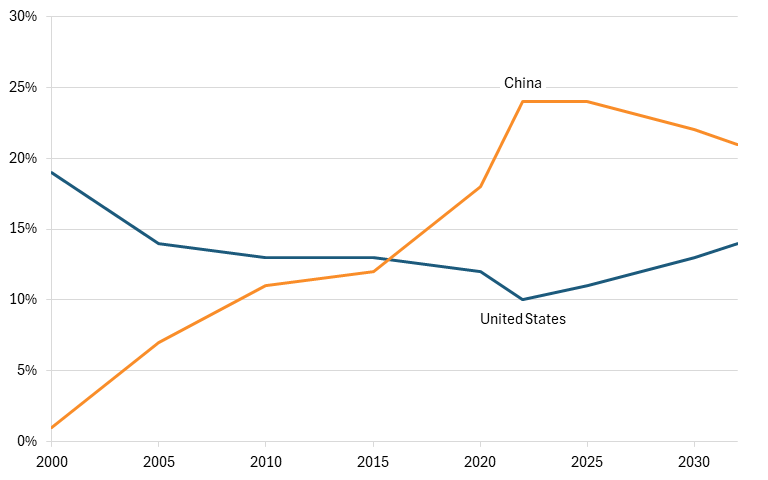

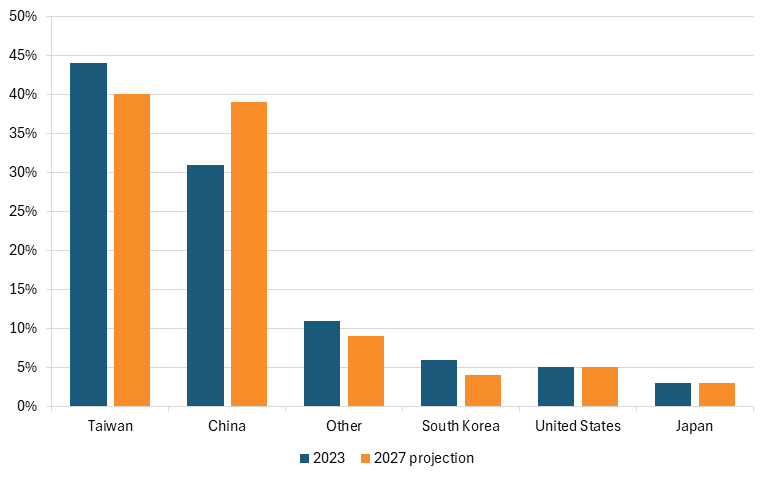

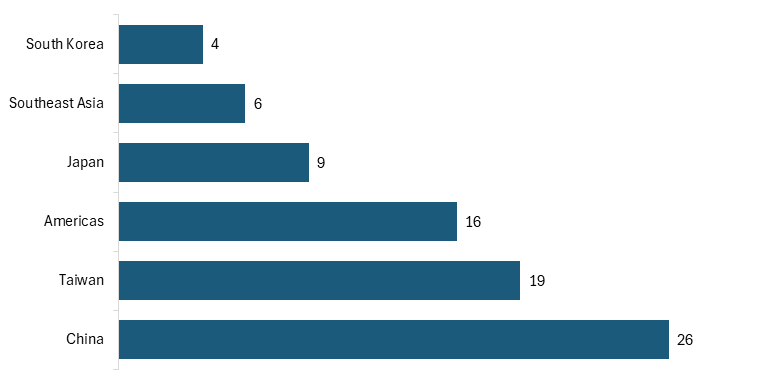

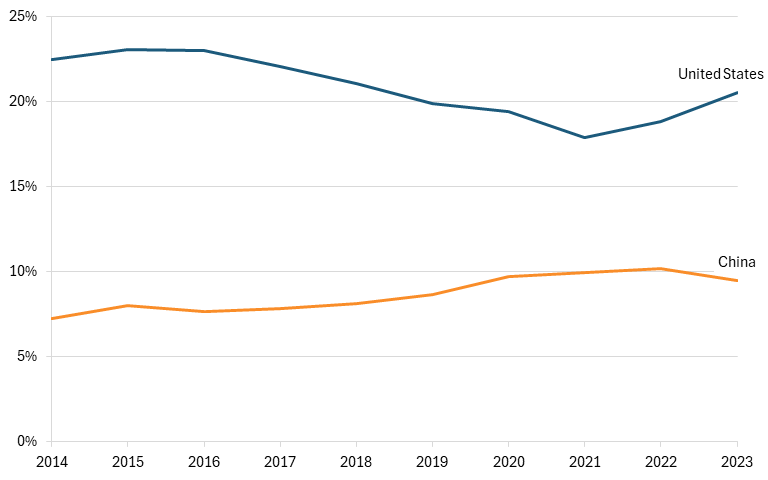

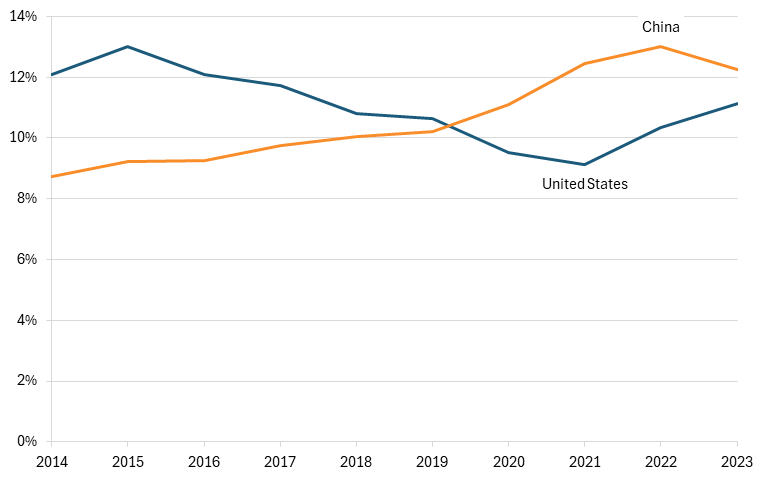

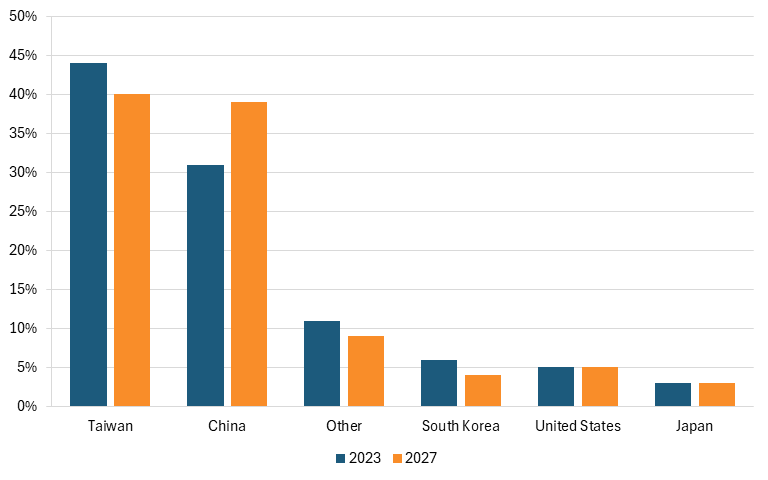

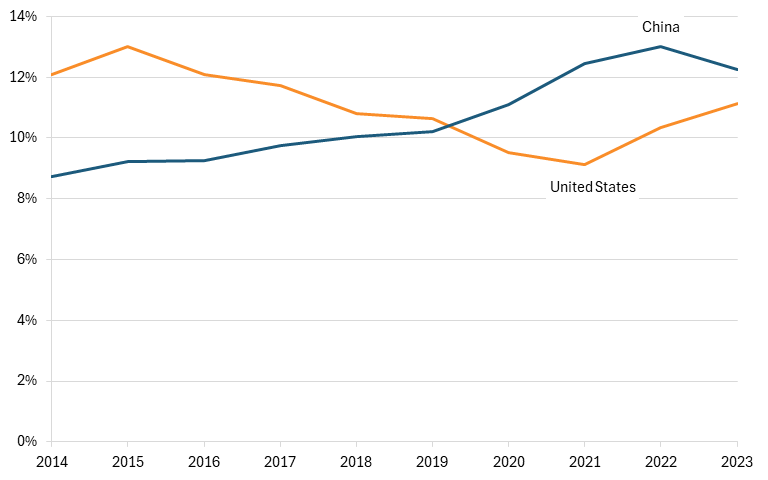

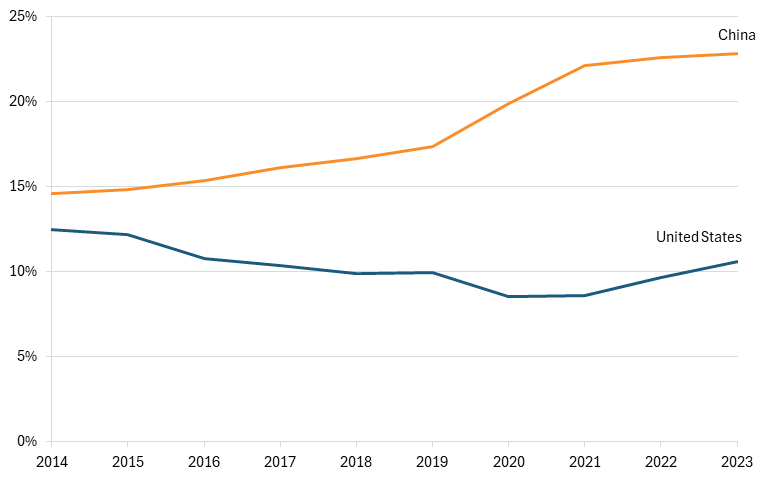

In China’s Made in China 2025strategy, released in 2015, the government explicitly aims to achieve 70 percent self-sufficiency in semiconductor products by 2025 and to become the world leader in semiconductor manufacturing by 2030.[30](#_edn30) Although these goals haven’t yet been reached, China-based firms are expected to continue to grow rapidly, as policy support and investment remain aligned with these objectives. China’s share of legacy chip manufacturing is expected to grow from 31 percent in 2023 to 39 percent in 2027, making it second globally behind Taiwan, whose share is projected to decline from 44 percent to 40 percent.[31](#_edn31) The United States is projected to hold 5 percent of the global market share. (See figure 12.) Moreover, between 2022 and 2026, China is expected to build more new fabs and complete more major expansions than any other region will, bringing 26 facilities online, compared with only 16 in the Americas.[32](#_edn32)

**Figure 12: Global market share in legacy semiconductor manufacturing, 2023 vs. 2027 projection[33](#_edn33)**

China’s push for dominance in the global semiconductor market poses a direct threat to U.S. firms, and its growth is not expected to slow.[[34]](#_edn34) As Chinese producers replace U.S. suppliers domestically and expand aggressively into third-country markets, U.S. semiconductor exports will face sustained erosion in market share, revenue, and profitability. Chinese authorities will continue to aggressively subsidize the semiconductor industry to reach their $150 billion target, thereby contributing to overcapacity and artificially low prices for Chinese firms. For Arizona, where semiconductors are one of the state’s most important export industries and an industry that has seen rapid growth over the past several years, this loss of global demand and reduced revenue would translate into slower industry growth and weaker job creation—a threat to the future of the state’s economy.

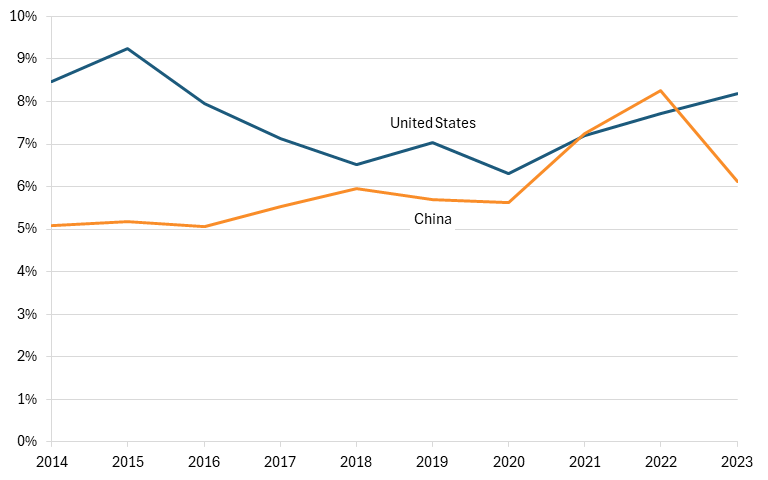

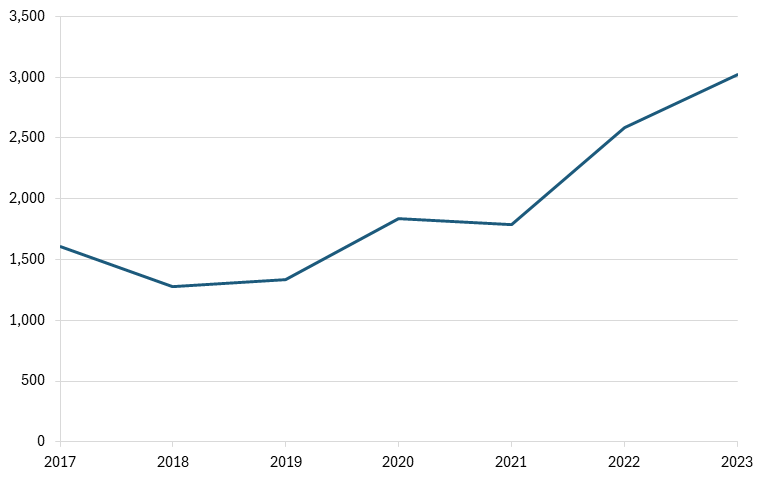

## Arkansas: Motor and Generator Manufacturing (NAICS 335312)

Arkansas has one of the largest motor and generator manufacturing industries in the country, employing over 2,600 workers and competing in a competitive global market.[[35]](#_edn35) This industry is a critical input to U.S. energy and power infrastructure, making it vital for the United States to maintain a secure supply chain and strong domestic manufacturing capabilities. While the United States has historically been a major producer of advanced electrical equipment, including industrial motors and generators, China’s rapid expansion in electrical machinery manufacturing poses a significant threat to the sector’s future success and U.S. national and economic security.[36](#_edn36)

Motor and generator manufacturing produces essential components used in industrial machinery, HVAC systems, power generation equipment, and manufacturing processes. These products are critical inputs across the economy, with generators serving as primary and secondary power sources for factories, hospitals, telecommunications towers, and data centers, making the industry a key part of critical infrastructure.[37](#_edn37) The expansion of data center infrastructure, in particular, has been a powerful catalyst for growth in this sector.

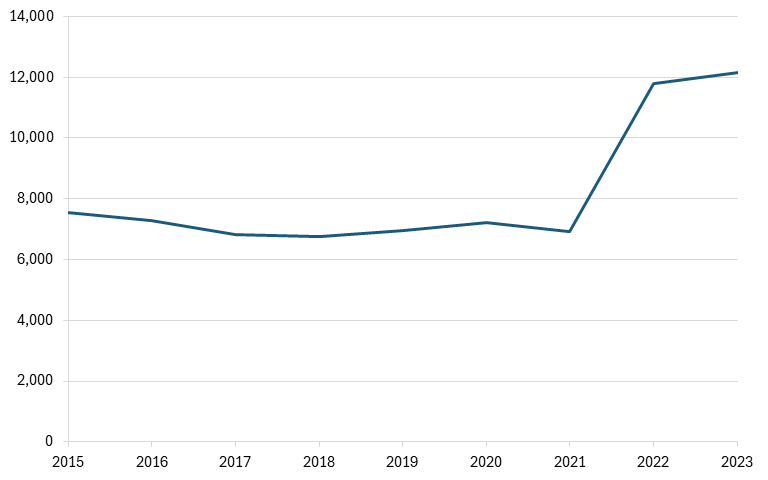

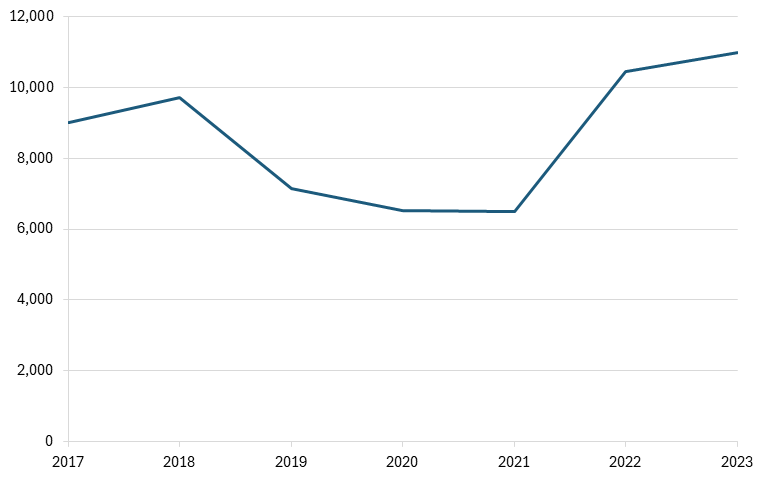

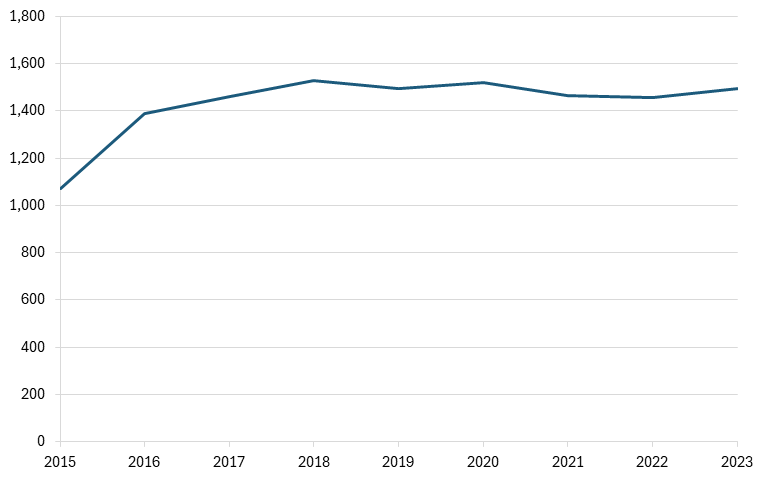

Arkansas plays an important role in this industry, particularly in the state’s western regions. The state is home to major manufacturers, including ABB Motors and Mechanical, headquartered in Fort Smith, and Nidec Motor Corporation in Mena. The concentration of production in a handful of facilities makes the industry particularly important to local economies in Arkansas, where manufacturing jobs provide stable, high-wage employment. Between 2015 and 2023, employment in the motor and generator industry in Arkansas experienced a decline. Despite a surge from 2019 to 2020, employment in this industry fell by about 5 percent, while overall employment in the state increased by 11 percent.[38](#_edn38) (See figure 13).

**Figure 13: Employment in the motor and generator manufacturing industry in Arkansas**

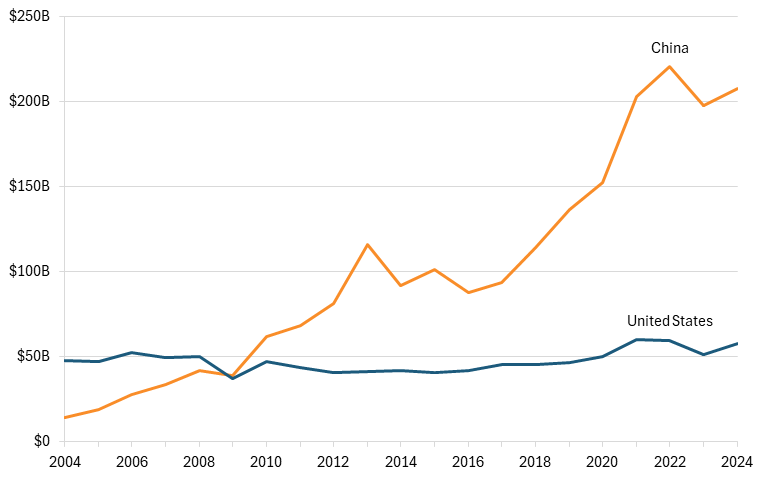

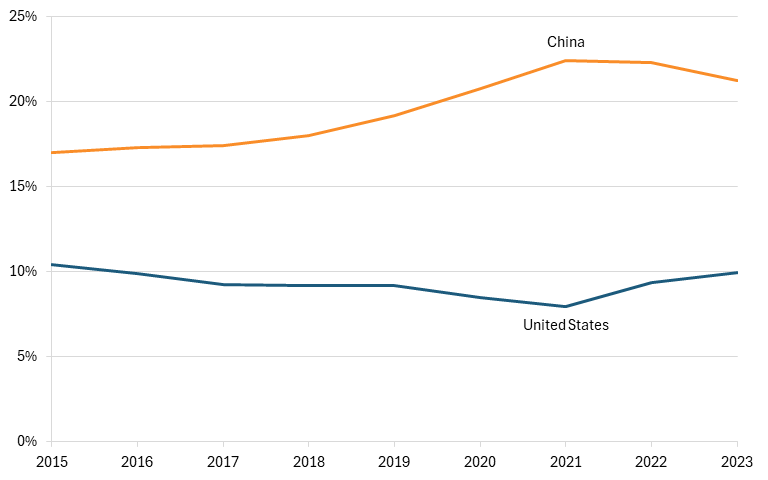

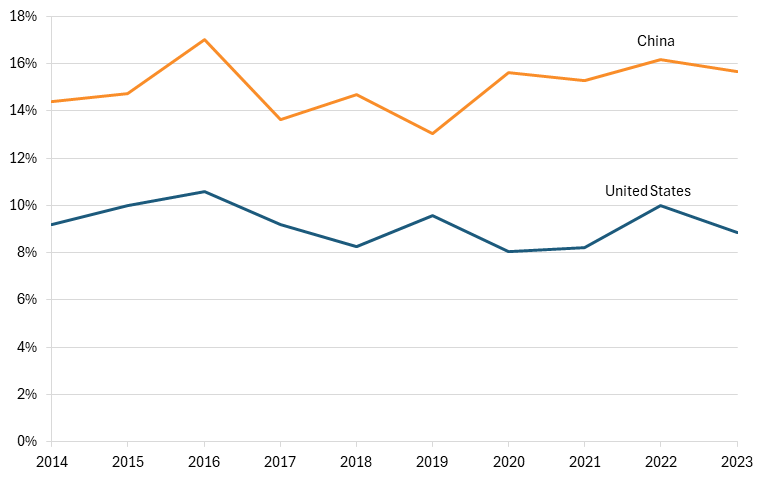

Despite its importance to Arkansas, the U.S. motor and generator industry has lost ground globally. China has rapidly increased its share of global exports, becoming a dominant supplier of electric motors and generators. In the early 2000s, the United States’ share of global exports of motors and generators (HS 8501, 8502, and 8503) exceeded that of China, with the United States holding about 10 percent of the global market while China held 9 percent. However, by 2005, China had surpassed the United States and continued to increase its global export share, rising from 9 percent to over 25 percent by 2024. In comparison, the U.S. share of global exports fell from 10 percent to 7 percent.[39](#_edn39)

**Figure 14: United States’ and China’s shares of global exports of motors and generators**

China’s rise in global market share has been driven in part by its ability to penetrate foreign markets, including the United States. U.S. imports of motors and generators from China increased substantially between 2004 and 2018, peaking at over $4 billion, a 420 percent increase, before declining slightly in recent years. Despite this decline, import levels remain significantly higher than over 20 years ago in 2004, demonstrating the continued presence of China’s producers in the U.S. market. (See figure 15.)

Being a significant input to critical infrastructure, the United States needs to have a strong and secure supply chain for motors and generators. Relying on imports from China in this industry leaves the United States vulnerable to economic coercion and national security risks.

**Figure 15: U.S. imports of motors and generators from China**

China’s rapid expansion in the motor and generator industry has occurred within a broader industrial strategy prioritizing the electrical equipment industry, recognizing it as a strategic manufacturing sector under the Made in China 2025 plan.[40](#_edn40) Made in China 2025 is a cohesive strategy for Chinese industrial dominance, outlining the government’s support for national champions in strategic industries through large-scale subsidization, tax credits, export seller credits, and more. These policies have supported the scaling of the Chinese electrical equipment industries, including motors and generators, and likely reduced costs for Chinese producers, allowing them to quickly gain market share globally.

China’s growing competitiveness is evident not only in its penetration of the U.S. market but also in third-country markets that have traditionally been dominated by U.S. firms. Canada and Mexico, the two largest export destinations for U.S. motor and generator manufacturers, are increasingly importing motor and generator products from China.[41](#_edn41) Over the past decade, the share of exports of motors and generators to Canada and Mexico from the United States has declined from about 75 percent to 50 percent, while China’s export share has grown from 3 percent to 23 percent, nearly a quarter of all imports.[42](#_edn42) (See figure 16.)

**Figure 16: United States’ and China’s shares of motors and generator exports to Canada and Mexico**

China’s continued expansion in motor and generator manufacturing poses a direct threat to U.S. firms and the regional economies that depend on them. As Chinese producers gain market share in both domestic and international markets, U.S. manufacturers may face declining exports, tighter profit margins, and reduced investment. In Arkansas, motor and generator manufacturing employment has already experienced a decline over the past several years, and the growing threat of China could worsen the situation still, translating into slower growth, reduced economic output, and potential jobs losses.

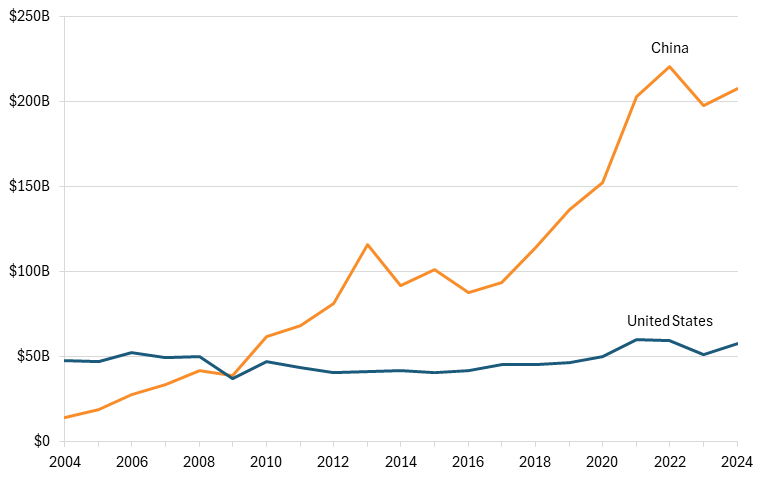

## California: Computer Storage Device Manufacturing (NAICS 334112)

California specializes in the computer and storage device manufacturing industry, which operates in a highly competitive global market. Although California remains home to many of the United States’ most important computer hardware and data storage firms, China’s extensive industrial support for electronics and information technology manufacturing has helped it become the dominant global producer and exporter in this space, posing a significant challenge to California’s future industry success.

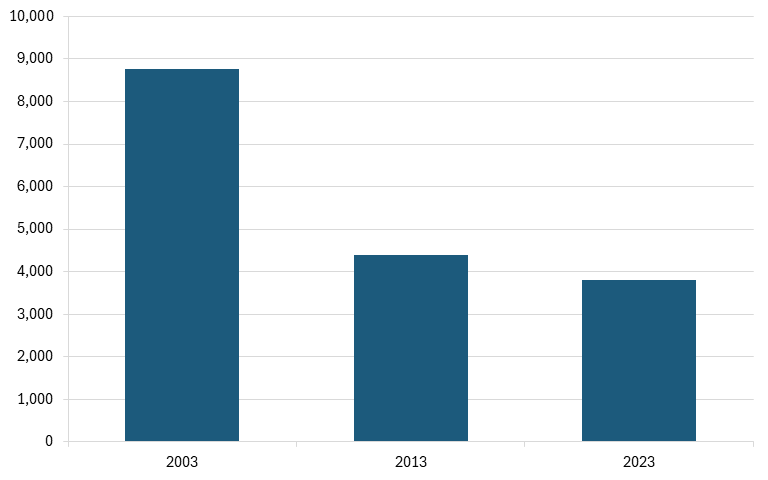

Computer and storage device manufacturing includes products such as servers, enterprise computing systems, and computer storage devices. These products are critical to the digital economy, particularly as the build-out of data centers continues and the demand for data storage supporting artificial intelligence (AI) continues to grow. California is the center of gravity for this industry in the United States, with many of the country’s leading firms in computing hardware, data infrastructure, and storage systems based in the state. California is home to Supermicro in San Jose, Western Digital in San Jose, and Apple in Cupertino. This concentration of firms has made California one of the country’s most important states for advanced computing hardware. At the same time, the industry has shrunk over the long term in employment terms. California’s employment in this industry fell from 8,761 workers in 2003 to 4,381 in 2013 and then to 3,799 in 2023, a decline of roughly 57 percent.[43](#_edn43) (See figure 17.) Still, 84 percent of the country’s workforce in this industry is in California, underscoring California’s importance to this industry.[44](#_edn44)

**Figure 17: Employment in computer storage device manufacturing in California**

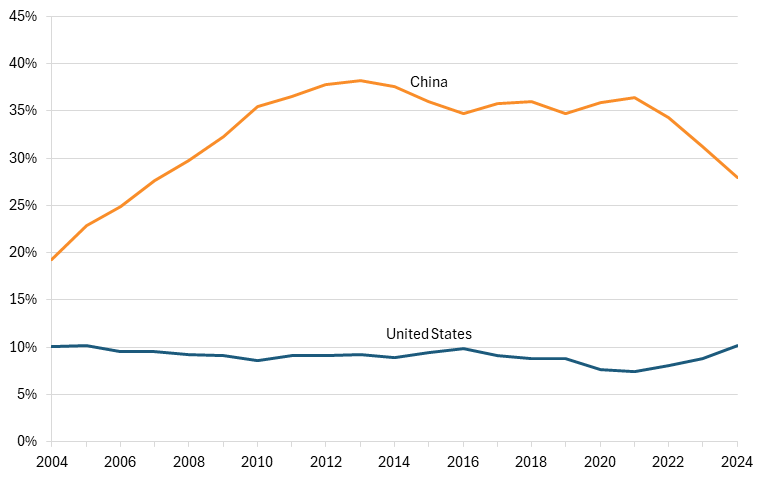

China has consistently held a larger share of the export market for computer storage devices (HS codes 8471, 8473, and 8523) than the United States has over the past two decades. In 2004, China accounted for about 20 percent of all exports in this industry, while the United States accounted for about 10 percent. China’s exports continued to increase relative to the rest of the world over the next decade, controlling about 37 percent of the export market at its peak in 2013, before declining for the next several years. In 2024, China’s exports in this industry accounted for one-quarter of all exports, while U.S. exports still sat at about 10 percent.[45](#_edn45)

**Figure 18: United States’ and China’s shares of global exports of computer storage devices**

In East Asian markets, a critical region for technology exports such as computer storage devices, China’s market share has also surged. In 2024, China exported about 6 percent of all computer storage device products to Indonesia, the Philippines, and Vietnam, while the United States exported about 3 percent. By 2024, however, Chinese exports had surged, reaching 45 percent in 2023 before declining slightly to 43 percent in 2024. The United States’ exports to these markets, on the other hand, stagnated. By 2024, the United States accounted for about 5 percent of all exports to this region, a marginal increase from 20 years prior. The scale of China’s growth underscores its aggressive export expansion strategy and its dominance of third-country markets.[46](#_edn46)

**Figure 19: United States’ and China’s shares computer storage device exports to Indonesia, the Philippines, and Vietnam**

China’s dominance in computer and storage device manufacturing has been driven by a deliberate strategy to build a broader computing hardware stack. Under Made in China 2025, Beijing identified next-generation information technology as a priority sector and pushed implementation through national, provincial, and city-level guidance.[[47]](#_edn47) In practice, that support has enabled Chinese firms to produce high-value computer hardware, including servers, data center equipment, and other digital infrastructure products.[48](#_edn48) China’s vast domestic market for cloud services, enterprise IT, and digital infrastructure has further reinforced this growth, allowing domestic producers to scale rapidly before expanding abroad.

China’s concerted effort to build advanced manufacturing capacity and expand into higher-value products has been highly successful, driving a surge in exports and likely a substantial increase in global market share. While it’s difficult to conclude definitively that China’s rise in computer storage device manufacturing directly caused California’s employment decline or the stagnation of U.S exports, the correlation is clear.

China’s continued growth in this industry could be an even greater threat to California in the future. Should China continue its strategic investment in next-generation IT industries through industrial strategies similar to Made in China 2025, we can expect Chinese exports to continue rising while U.S. producers face growing pressure. For California, that would mean weaker export volume, lower profits, reduced output, and further job losses in the country’s most important computer and electronics manufacturing state.

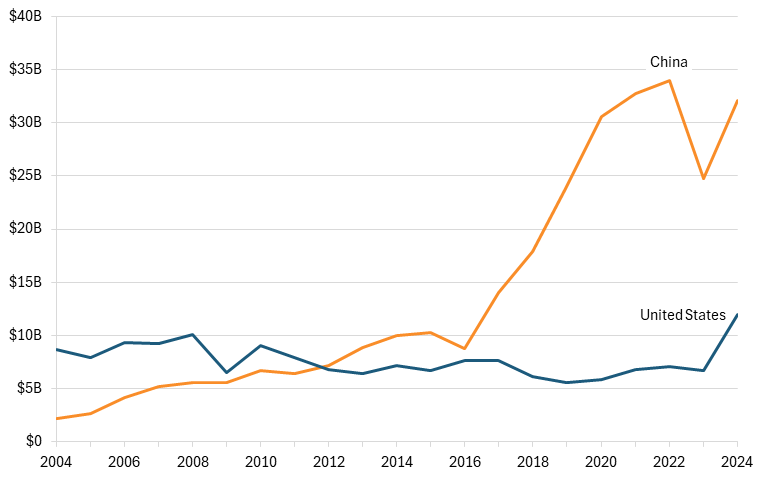

## Colorado: Computer Storage Device Manufacturing (NAICS 334112)

Colorado has the second-largest computer storage device manufacturing industry in the country, operating in a highly competitive global market. Although the state remains home to important data storage and enterprise hardware capabilities, China’s rapid expansion in electronics manufacturing and data-storage supply chains poses a growing challenge to the future competitiveness of Colorado firms.

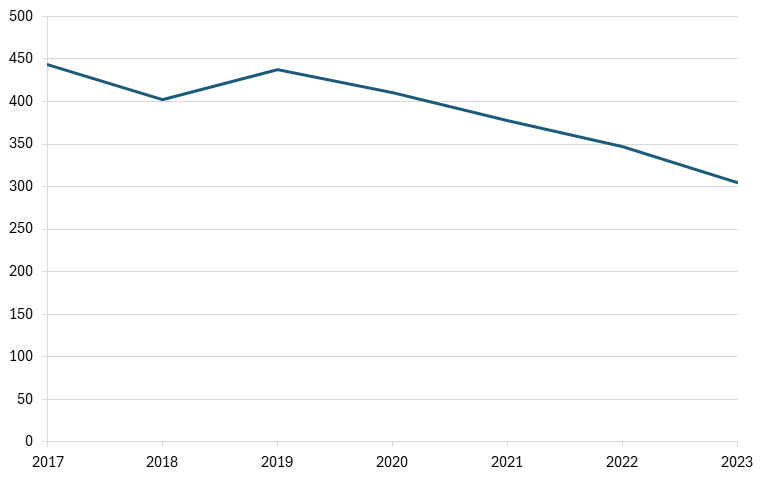

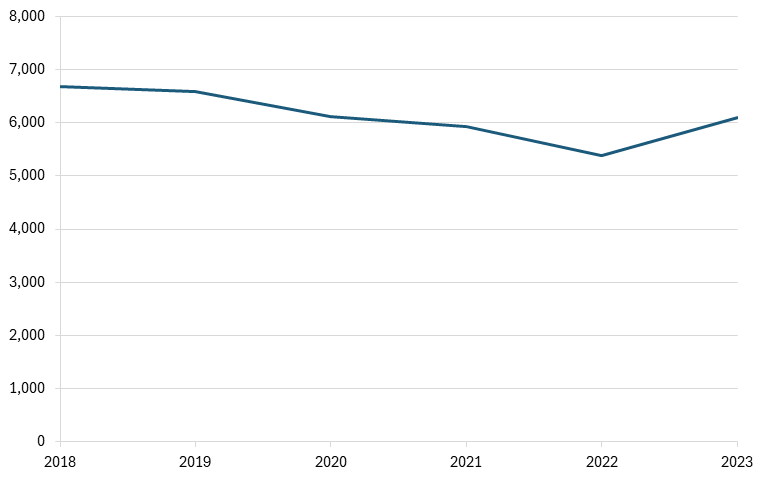

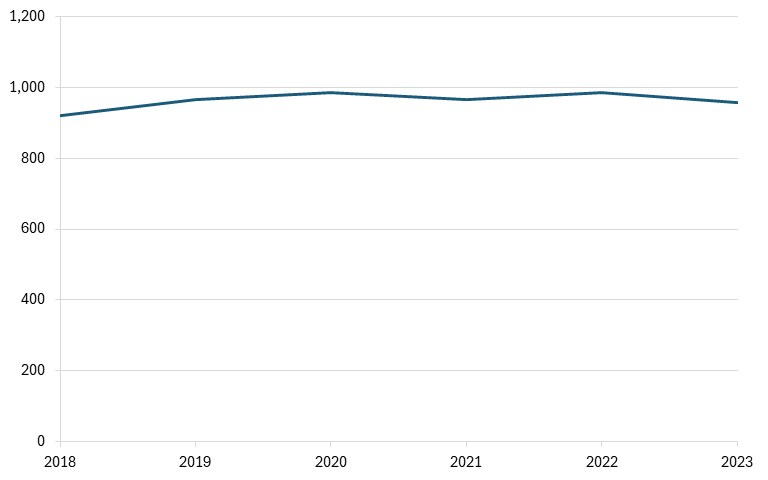

Computer and storage device manufacturing includes products such as servers, enterprise computing systems, and computer storage devices. These products are critical to the digital economy, particularly as the build-out of data centers continues, and the demand for data storage to support AI grows. Seagate Technology, a major global data-storage company, has a long-standing presence in Colorado, leading the industry in the state. Between 2017 and 2023, employment declined gradually, falling from about 450 to 300. Yet, as of 2023, 7 percent of the country’s workforce in this industry is still located in Colorado, making it the second-largest employer in the U.S. computer storage device industry, behind only California.[49](#_edn49)

**Figure 20: Employment in computer storage device manufacturing in Colorado**

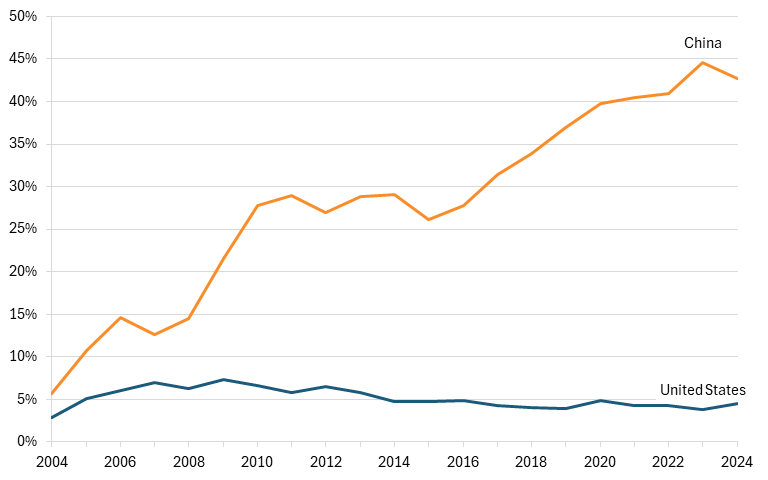

However, this industry, like many others, is being increasingly shaped by Chinese firms, themselves supported by large-scale industrial policy. China has outpaced the United States in global exports of computer storage devices (HS codes 8471, 8473, and 8523) over the past two decades, with China’s share of exports increasing from 20 percent in 2004 to 28 percent in 2024, and reaching a peak of 37 percent in 2023. The United States, on the other hand, has seen its share of global exports in this industry sit at about 5 percent over the same two-decade period.[50](#_edn50) (See figure 21.)

**Figure 21: United States’ and China’s shares of global exports of computer storage devices**

China accounted for about 6 percent of exports to Indonesia, the Philippines, and Vietnam in 2004, but by 2024, this share had increased substantially to nearly 45 percent. This increase also significantly widened the gap between China and the United States. U.S. exports to these markets in 2024 was very similar to 2004, with its share of exports increasing from 3 percent to just 5 percent.[51](#_edn51)

**Figure 22: United States’ and China’s shares of computer storage device exports to Indonesia, the Philippines, and Vietnam**

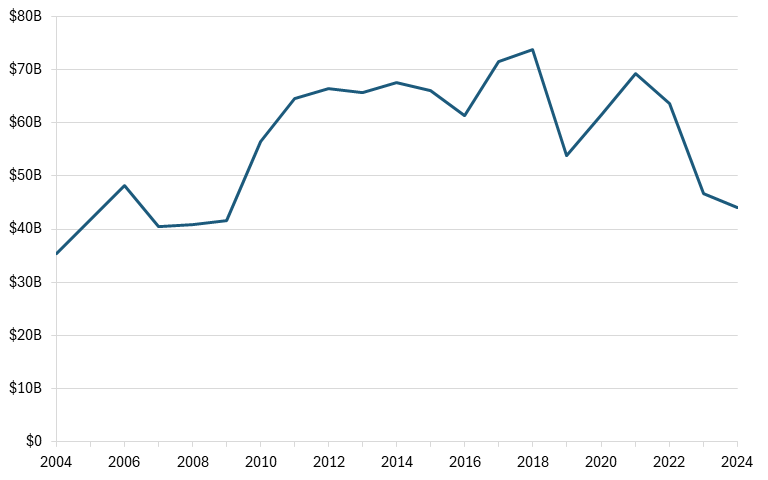

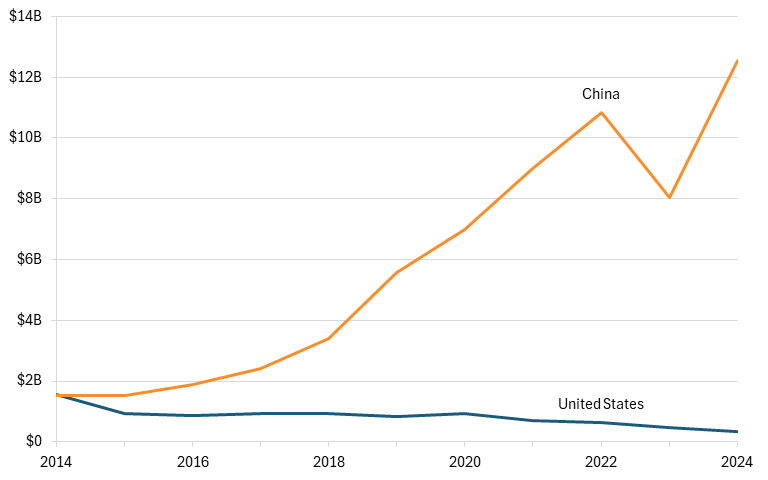

China has penetrated not only foreign, third-country markets but also the U.S. market. Imports of computer storage devices from China increased steadily from 2004 to 2018, rising from $35 billion to nearly $74 billion. In the years since, imports from China have declined gradually, falling to $43 billion, still a 25 percent increase since 2004.[52](#_edn52)

**Figure 23: U.S. imports of computer storage devices from China**

China’s dominance in computer and storage device manufacturing has been driven by a deliberate strategy to build out its broader computing hardware ecosystem. Under Made in China 2025, Beijing identified next-generation information technology as a priority sector and advanced that goal through coordinated national, provincial, and local policy support.[[53]](#_edn53) In practice, this support has helped Chinese firms expand production of higher-value computer hardware, including servers, data center equipment, and other digital infrastructure products.[54](#_edn54) China’s vast domestic market for cloud services, enterprise IT, and digital infrastructure has reinforced this growth, allowing domestic producers to achieve scale at home before expanding aggressively into foreign markets.

China’s concerted effort to build advanced manufacturing capacity and move into higher-value technology products has been highly successful, fueling a surge in exports and likely a substantial increase in global market share. While it is difficult to say definitively that China’s rise in computer storage device manufacturing has directly caused a decline in Colorado employment or the stagnation of U.S. exports, the correlation is hard to ignore.

China’s continued growth in this industry could pose an even greater threat to Colorado in the years ahead. If China continues to support next-generation IT industries through industrial strategies similar to Made in China 2025, Chinese exports are likely to continue rising while U.S. producers face mounting competitive pressure. For Colorado, China’s competition could still place pressure on the expanding industry, resulting in potential for lower profits, reduced output, and substantial job losses.

## Connecticut: Aircraft Engine and Engine Parts Manufacturing (NAICS 336412)

Connecticut is one of the most important states for aircraft engine and engine parts manufacturing in the United States, with a highly specialized workforce and a concentration of globally competitive firms. However, the industry operates in an increasingly competitive global market in which China’s state-backed push into aerospace manufacturing poses a growing long-term threat to U.S. leadership.

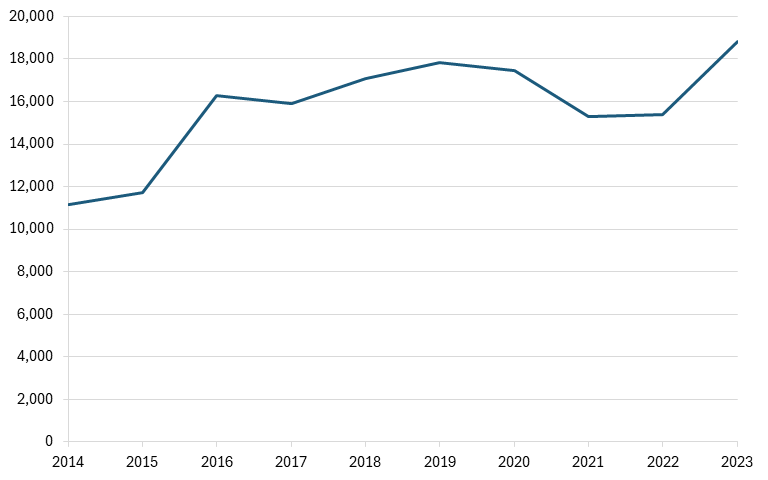

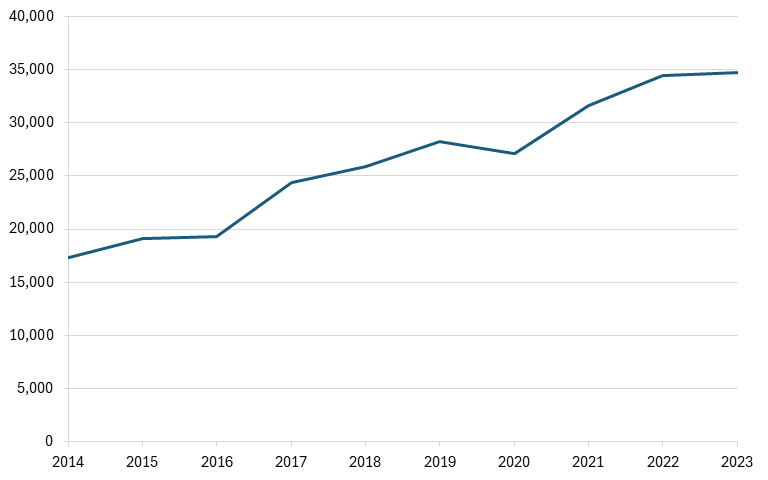

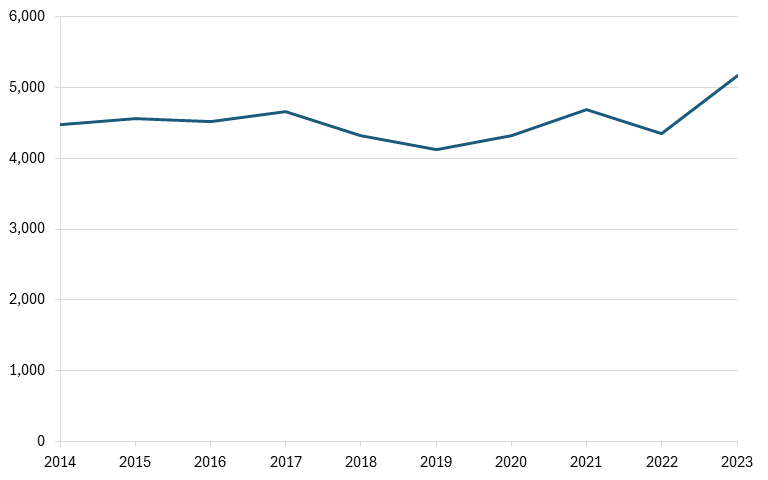

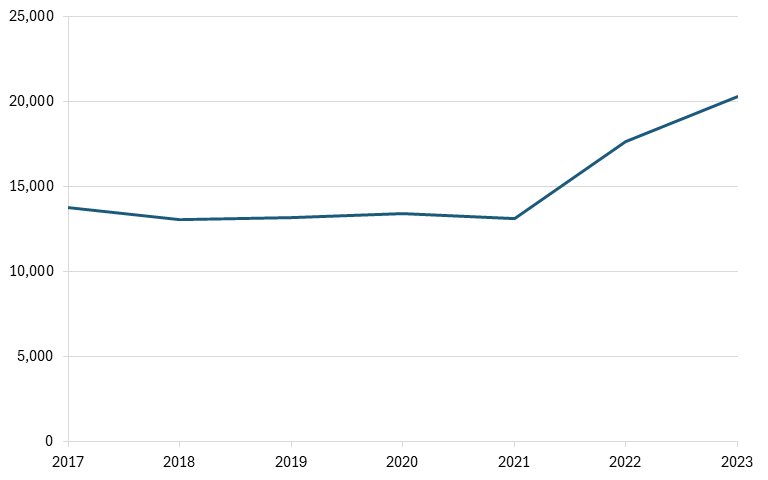

Aircraft engine and engine parts manufacturing includes the production of propulsion systems, turbines, and critical components used in both commercial and military aircraft. These products are essential to national defense, commercial aviation, and the broader aerospace supply chain. Connecticut plays an outsized role in this industry, anchored by major firms such as RTX, which owns Pratt & Whitney, a leading manufacturer of aircraft engines, and GE Aerospace, which maintains significant operations in the state. Sikorsky (a Lockheed Martin company) also contributes to the broader aerospace ecosystem in Connecticut.[55](#_edn55) Employment trends reflect the strength and growth of the industry over the past decade, with employment increasing from approximately 11,000 workers in 2014 to a peak of nearly 19,000 in 2023.[56](#_edn56) (See figure 24.)

**Figure 24: Employment in aircraft engine and engine parts manufacturing in Connecticut**

Despite Connecticut’s importance domestically, the United States has seen its position in the global aerospace supply chain face increasing pressure. Historically, the United States has maintained a strong lead in aircraft engine exports, but its share of global exports (HS codes 840710, 840910. 8411, 841210) has declined over time as other countries—including China—have expanded their capabilities. In the late-2000s, the United States accounted for over 13 percent of global exports in this industry, but that share has since fallen to below 10 percent in recent years. China’s share of global exports has also increased marginally over this period, from about 1.5 percent to 2 percent.[57](#_edn57) (See figure 25.)

China’s comprehensive five-year plan, Made in China 2025, identifies aerospace equipment as a priority sector, and therefore the Chinese government has provided extensive support to domestic aerospace firms through subsidies, state-directed financing, and government procurement policies.[58](#_edn58) For example, the Commercial Aircraft Corporation of China (COMAC), the country’s flagship civil aviation manufacturer, has received tens of billions of dollars in state support to develop indigenous aircraft such as the C919. According to the Center for Strategic and International Studies (CSIS), COMAC had received an estimated $49 billion in state subsidies and support mechanisms as of 2020.[59](#_edn59) However, it is notable that COMAC does not produce its own engines and instead relies on other firms.

**Figure 25: United States’ and China’s shares of global exports of aircraft engines and engine parts**

In addition to direct subsidies, Chinese aerospace firms benefit from preferential access to financing from state-owned banks, subsidized inputs, and government-backed R&D initiatives. The OECD has documented significant government support across China’s aerospace sector, noting that such policies reduce production costs, enable below-equity returns for investors, and allow firms to compete internationally even before achieving full technological parity.[60](#_edn60)

While China still lags behind the United States and key allies in high-performance jet engine technology, it has made notable progress. Programs such as the CJ-1000A jet engine aim to reduce reliance on foreign suppliers and build a fully domestic aerospace supply chain. Over time, this could allow Chinese firms to compete more directly in global markets, particularly in third-country exports.

Exports to some of the United States’ closest aerospace trading partners, including Canada, the United Kingdom, and Germany, closely mirror global trends.[61](#_edn61) The United States still holds a greater share of the export market in these countries than China does; however, its leadership has faced a slow decline. As of 2024, the United States accounted for 8 percent of all exports to these countries, while China accounted for just 2 percent.[62](#_edn62)

**Figure 26: United States’ and China’s shares of aircraft engine and engine part exports to Canada, the United Kingdom, and Germany**

China’s expansion into aerospace part manufacturing has broader implications for global market dynamics. As in other advanced manufacturing sectors, state support can enable overcapacity and pricing advantages that distort international competition. China’s sustained investment signals a long-term strategy to compete with established producers in the United States. For Connecticut, a state that is highly competitive in this industry and has seen its workforce grow over the past several years, these dynamics do not pose an imminent risk, but they could threaten the success of the industry in the long term.

## Delaware: In-Vitro Diagnostic Substance Manufacturing (NAICS 325413)

In-vitro diagnostic substance manufacturing is a growing advanced-manufacturing industry in Delaware. While China has expanded its presence in the global diagnostics market, the available evidence does not indicate that Chinese competition is currently a major cause for concern for Delaware producers, but it is something to watch out for in the future. China has benefited from substantial state support in the broader medical technology sector and has improved its capabilities over time, but the United States remains the far larger exporter of in-vitro diagnostic substances and continues to dominate exports to key advanced foreign markets. For Delaware, the data suggests that the state’s diagnostics industry is growing in a market wherein U.S. firms still hold a stronger competitive position.

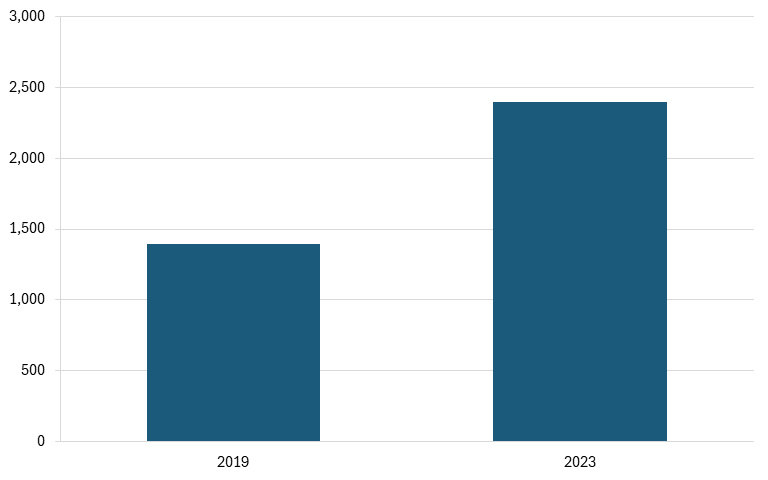

In-vitro diagnostic substance manufacturing includes the production of diagnostic and laboratory reagents, assay kits, calibrators, controls, and related products used to detect disease and monitor patient health. These goods are a critical part of modern health care and support hospital laboratories, chronic disease management, and infectious disease testing. Delaware has become a meaningful location for this activity. Employment in this industry in Delaware rose from about 1,400 in 2019 to 2,400 in 2023, an increase of 72 percent.[63](#_edn63) (See figure 27.) Though its workforce is relatively small in absolute terms, Delaware employs 6 percent of all workers in in-vitro diagnostic substance manufacturing, making it home to a significant share of the national workforce. The state is home to several major firms in this industry, including Siemens Healthineers, which, in 2021, announced that it would invest more than $32 million to expand its laboratory diagnostics manufacturing facility in Newark, Delaware, increasing its manufacturing capacity.[64](#_edn64)

**Figure 27: Employment in in-vitro diagnostic substance manufacturing in Delaware**

China has invested heavily in its biopharmaceutical and medical devices industries, with these sectors among the 10 critical industries highlighted in its Made in China 2025 strategy. Under Made in China 2025, China mobilized federal, state, and local funding to support critical industries and elevate national champions, aiming to lead the world in advanced manufacturing and strategic industries.[65](#_edn65) And though China has made significant strides in all these industries, it has failed to make a meaningful mark in the in-vitro diagnostic substance industry, lagging behind the United States in total exports.

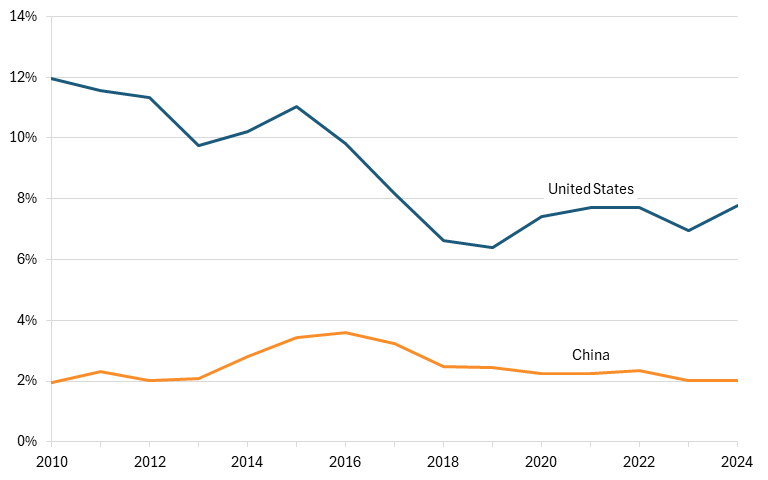

The United States’ export share of in-vitro diagnostic substances (HS codes 3002 and 3822) has actually fallen in recent years, despite the United States’ leadership and the industry’s growth in states such as Delaware. From 2004 to 2024, the share of global exports from the United States declined from 22 percent to 17 percent, with the low point occurring during the COVID pandemic, when medical device manufacturing increased globally. Despite this decline, the United States still maintains a meaningful lead over China, whose exports have accounted for close to 0 percent of the total market for most of the period from 2004 to 2024. Notably, China’s exports increased sharply during the pandemic, reaching a peak global export share of 7 percent, but have since declined back to pre-2020 levels.[66](#_edn66) (See figure 28.)

**Figure 28: United States’ and China’s shares of global exports of in-vitro diagnostic substances**

Similarly, China has failed to make inroads into the United States’ most prominent export markets. Looking at the three largest export destinations for U.S. in-vitro diagnostic substances (excluding China), the United States still dominates the market, accounting for 25 percent of all exports in 2024.[67](#_edn67) China, on the other hand, accounted for just 0.3 percent of exports to these markets in 2024, down from its surge in 2020, further demonstrating its weakness in this industry relative to the United States.[68](#_edn68) (See figure 29.)

That said, China has demonstrated its ability to rapidly increase output and gain market share in industries it deems critical to national power, and it has long treated medical technology as one of these industries. Under Made in China 2025, China set a goal of increasing its global market share in this industry by developing 5 to 10 globally recognizable brands, which the U.S.-China Economic and Security Review Commission finds China has succeeded at.[69](#_edn69) They also set a goal of procuring 70 percent of hospital medical devices domestically, which China has not yet achieved. The localization rate for in-vitro diagnostic equipment was about 46 percent in 2024.[70](#_edn70)

Additionally, a report from MERICS finds that Chinese medical technology firms received measurable financial support from the government between 2017 and 2022, including subsidies, tax incentives, and below-market financing. Overall, government support grew from $725 million in 2017 to between $2.9 billion and $3.9 billion in 2022.[71](#_edn71) This support was equivalent to at least 25 percent of companies’ net profit over that period. With such substantial support for firms and a clearly defined plan to increase competitiveness and global market share, medical device manufacturers in China have the means to become major competitors in the future, posing a potential threat to the dominance of the U.S. in-vitro diagnostic industry.

**Figure 29: United States’ and China’s shares of in-vitro diagnostic substance exports to Germany, Japan, and the Netherlands**

For Delaware, the main takeaway is that China’s role in this industry should be viewed as a long-term development rather than an immediate threat. Delaware’s in-vitro diagnostic substance manufacturing base has expanded in recent years, with employment growing substantially and large investments on the way, helping the United States to lead the world in this industry. Conversely, China has seen minimal growth in this industry’s exports, suggesting that Chinese firms have thus far failed to challenge their U.S. counterparts. However, if Chinese firms continue to receive substantial state support, they could become more formidable competitors in the future, posing a threat to the U.S. industry’s success.

## Florida: Computer Terminal and Other Computer Peripheral Equipment (NAICS 334118)

Florida is a strong producer of computer terminals and peripheral equipment, particularly in high-value segments such as enterprise hardware, storage systems, and defense-related electronics. However, China’s growth in the industry, supported by state-backed industrial policies, poses a significant challenge to the long-term competitiveness of U.S. producers.

Computer terminal and other computer peripheral equipment manufacturing includes products such as monitors, terminals, storage devices, servers, and input/output peripherals. These products are critical inputs into the broader information technology ecosystem, supporting industries ranging from cloud computing and telecommunications to defense and aerospace systems. Notably, these products are increasingly valuable because of their necessity for data center construction.

Florida is home to several major firms in this industry, including Jabil Inc., one of the largest electronics manufacturing services firms in the world, and TD SYNNEX, a distributor of information technology. These firms, along with several others, support one of the largest workforces for this industry in the country, employing 12 percent of the U.S. workforce. Despite the industry’s growing importance and Florida’s strength, employment has remained relatively stagnant. Between 2017 and 2023, employment in this industry increased by just 36 workers, from 1,200 to 1,236.[[72]](#_edn72) (See figure 30.)

**Figure 30: Employment in computer terminal and computer peripheral equipment manufacturing in Florida**

However, like other technology manufacturing industries, the United States remains a relatively small player in the global market, especially compared with China. Under the Made in China 2025 strategy, Beijing identified next-generation information technology as a priority sector and pushed implementation through national, provincial, and city-level guidance.[[73]](#_edn73) In practice, that support has enabled Chinese firms to produce high-value computer hardware, including servers, terminals, and other digital infrastructure products.[74](#_edn74) China’s vast domestic market for cloud services, enterprise IT, and digital infrastructure has further reinforced this growth, allowing domestic producers to scale rapidly before expanding abroad.

China’s concerted effort to build advanced manufacturing capacity in computer equipment and next-generation IT has been highly successful, driving a surge in exports and likely a substantial increase in global market share. It has also enabled Chinese firms to emerge as global leaders. Lenovo, for example, was the world’s largest PC manufacturer as of 2024, accounting for roughly one-quarter of global shipments.[75](#_edn75) Other major firms, including Huawei and Inspur, are leading producers of enterprise computing equipment, while contract manufacturers such as Foxconn operate large-scale facilities in China that supply global markets.

While China has consistently exported more computer terminals and peripheral equipment (HS codes 8471 and 8473) than the United States has since the early 2000s, the gap has widened over the past two decades. From 2004 to 2024, China’s share of global exports grew from approximately 20 percent to 30 percent, peaking at about 41 percent around 2013. In contrast, the United States’ share of exports stagnated, staying at about 10 percent or less over the 21-year period.[76](#_edn76) (See figure 31.)

**Figure 31: United States’ and China’s shares of global exports of computer terminals and other computer peripheral equipment**

China’s rapid export growth has been driven by its ability to dominate third-country markets, particularly in Asia. Malaysia, Vietnam, and the Philippines—three key electronics manufacturing hubs—serve as critical destinations for intermediate goods used in global supply chains. Over the past two decades, China’s share of exports of computer peripheral equipment to these countries has increased significantly, rising from about 16 percent to about 35 percent from 2004 to 2024, and peaking at 45 percent in 2023. In contrast, The United States’s share of exports to these markets again stayed stagnant between 5 and 10 percent.[[77]](#_edn77)

**Figure 32: United States’ and China’s shares of computer terminal and other computer peripheral equipment exports to Malaysia, Vietnam, and the Philippines**

China’s push for dominance in the global computer hardware market poses a direct threat to U.S. producers, and its growth is unlikely to slow. As Chinese firms continue to benefit from extensive state support and rapidly increase exports, especially into key third-country markets, U.S. firms will also continue to face reduced export opportunities, risking the growth of the already large gap between the United States and China. In Florida, where this industry supports high-value manufacturing and high levels of skilled employment, continued erosion of global competitiveness could translate into slower growth, reduced investment, and weaker job creation, posing a long-term risk to the state’s economy.

## Georgia: Storage Battery Manufacturing (NAICS 335911)

Georgia is specialized in and dependent on the storage battery industry, which operates in a highly competitive global market. However, by using mercantilist policy instruments such as subsidies and tax incentives, China has rapidly expanded its manufacturing capacity in this industry, moving it from a nation on par with the United States to a global leader. Though recent policy actions have strengthened the Georgia battery economy, China’s dominance is likely to pose a challenge to the sector’s future success.

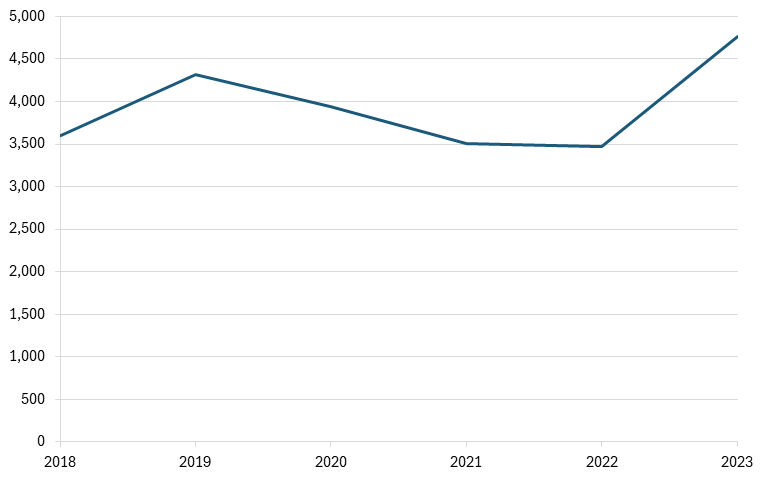

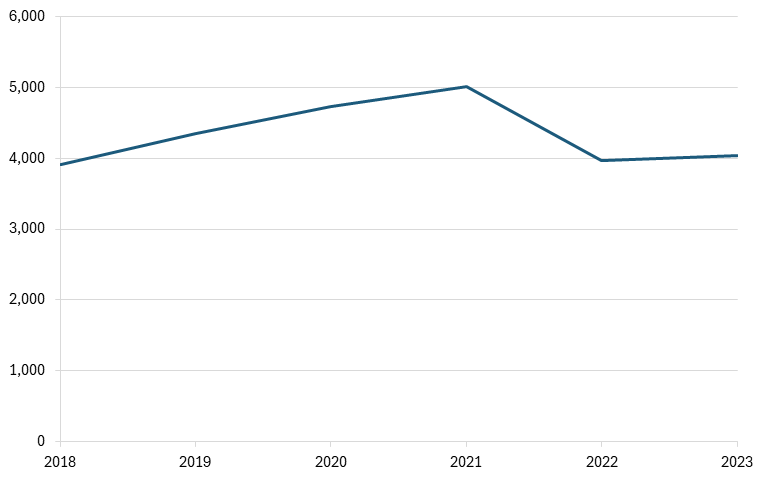

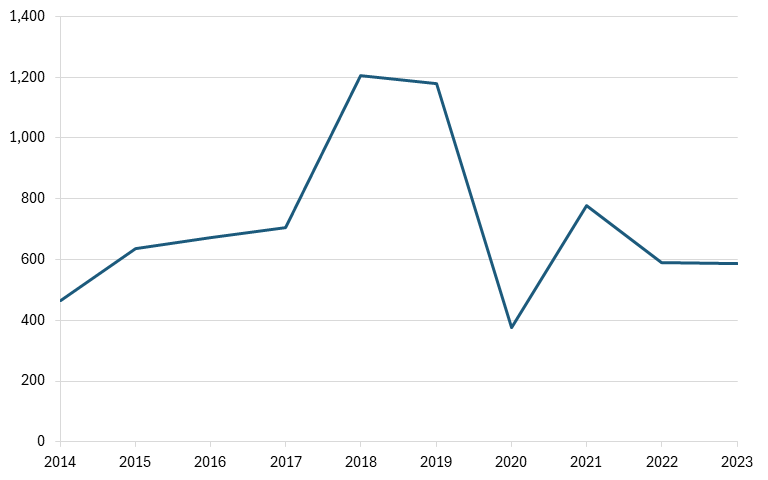

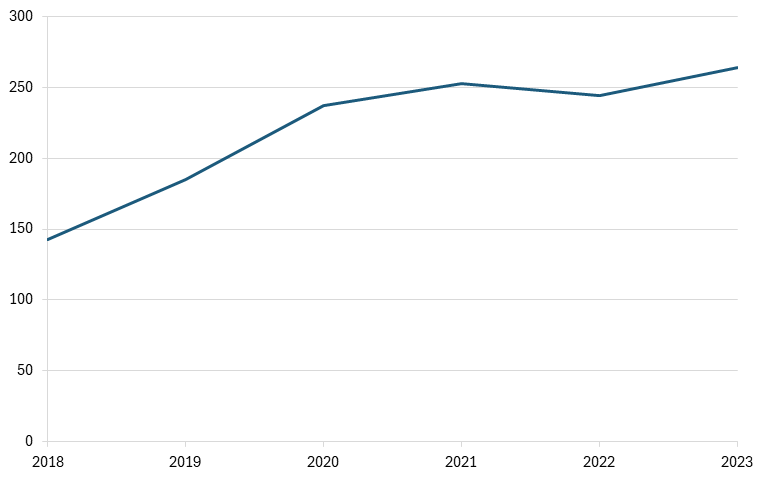

Storage battery manufacturing, which includes the production of rechargeable batteries, including lithium-ion and lithium iron phosphate (LFP), is a critical input to several national power industries, including electric vehicles (EVs) and renewable energy storage, and Georgia is a critical producer of these products in the United States. Following the passage of the Inflation Reduction Act (IRA), which provides tax credits for EVs with battery minerals and components sourced in North America, Georgia received billions of dollars in investment for battery production as SK On, LG Energy, and several EV companies constructed factories in the state.[78](#_edn78) Of the national workforce in this industry, 13 percent is reside in Georgia, totaling 4,200 workers directly employed, a more than sixfold increase in the size of the workforce compared with 2015.[79](#_edn79) (See figure 33). Additionally, following the completion of an LG Energy Solutions plant in Bryan County in 2026, another 3,000 workers will be employed in the state.[80](#_edn80) However, the repeal of the EV tax credits under the Trump administration could be detrimental to the industry. The International Council on Clean Transportation has estimated that by 2030, the loss of the EV tax credit could risk 7,000 jobs in battery pack and cell component manufacturing and recycling.[81](#_edn81)

**Figure 33: Employment in storage battery manufacturing in Georgia**

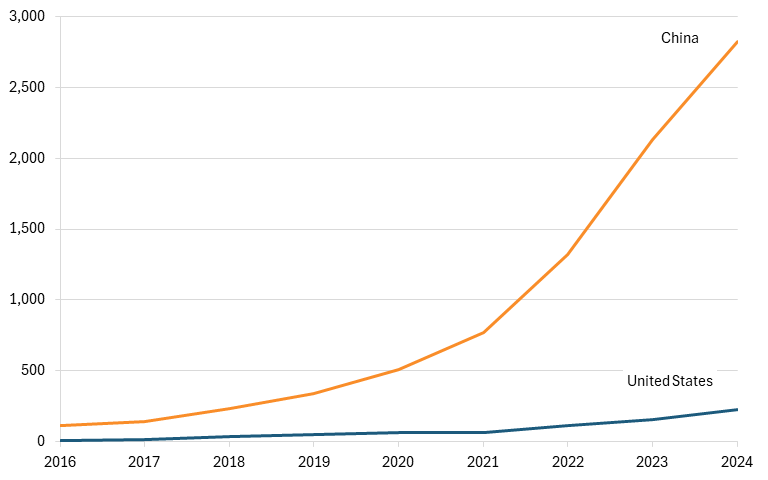

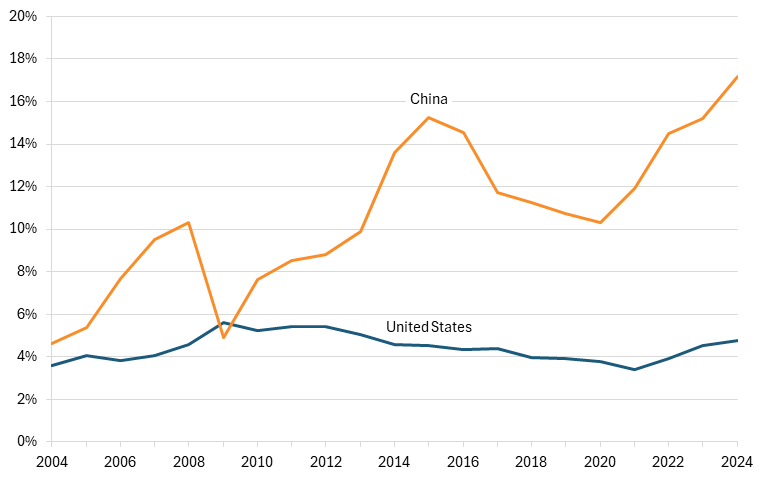

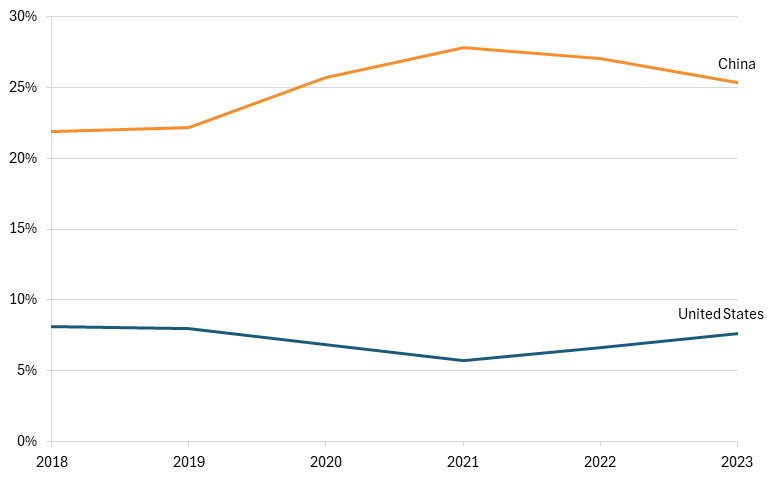

Regardless of the future of Georgia’s battery manufacturing economy, the state’s current strength in this industry is relatively small compared with China’s. In 2024, China accounted for 85 percent of global battery production capacity, while the United States held less than 10 percent. Looking specifically at lithium-ion batteries, China’s capacity was about 12 times that of the United States.[82](#_edn82) (See figure 34.)

**Figure 34: Lithium-ion battery manufacturing capacity (gigawatt hours)[83](#_edn83)**

China’s dominance in the battery industry would not be possible without the support of China’s federal and provincial governments, which have used a concerted strategy of industrial subsidies, research and development (R&D) financing, and vertical integration to support the increase and advancement of Chinese battery supply, while using EV adoption incentives and minimum battery purchase mandates to boost demand.

Perhaps the most powerful reason Chinese firms have been able to innovate and rapidly increase production in the battery industry is their complete vertical integration. China mines over two-thirds of the world’s graphite and 18 percent of its lithium—two key inputs to batteries—and overall extracts 60 percent of all rare earth minerals mined annually in the world. China also holds a near monopoly on the processing of rare earth minerals. In 2023, China refined 95 percent of the world’s manganese, 70 percent of cobalt and graphite, 67 percent of lithium, and more than 60 percent of nickel. In the transition of these minerals to battery components, China accounts for more than 90 percent of global cathode and anode material capacity.[84](#_edn84) Moreover, China’s dominance is expected to continue and grow, with the International Energy Agency (IEA) estimating that more than 77 percent of refined rare earths will come from China by 2030.[85](#_edn85) By dominating the battery supply chain, Chinese battery makers gain first access to key intermediate inputs for battery production, purchase these products at lower prices, experiment with new chemical combinations before competitors can, and potentially block competitors from accessing materials.[86](#_edn86)

Additionally, China’s federal and provincial governments have provided battery producers with substantial subsidies. CATL, China’s largest battery maker, received $1.8 billion from the Chinese government in subsidies from 2018 to 2023, while EVE Energy, the country’s fourth-largest battery producer, received $209 billion in 2023 alone. The government has also provided battery makers with R&D subsidies, helping Chinese firms stay ahead of global competition and boost sales. CATL and BYD, which together produce nearly half of all batteries globally, received nearly $830 million in research support to produce solid-state batteries, the next generation of storage batteries.[87](#_edn87)

The Chinese government has also boosted sales of its national champions in battery manufacturing by incentivizing EV adoption and the use of storage batteries. Since 2009, the Chinese government has invested hundreds of billions of dollars in advancing the EV industry, enabling Chinese EVs to be the cheapest in the world, often priced below cost. China has also implemented financial incentives for EV owners, such as waiving the license plate fee, exempting EVs from traffic control measures (which limit the number of cars on the road), and developing the world’s largest public charging infrastructure.[88](#_edn88) In the energy sector, the Chinese government began requiring firms to add 10 to 30 percent of battery storage to their grids for each gigawatt of wind or solar power, increasing demand for batteries.[[89]](#_edn89) By incentivizing EV and battery storage adoption, the Chinese government has catalyzed demand for batteries, boosting industry sales.

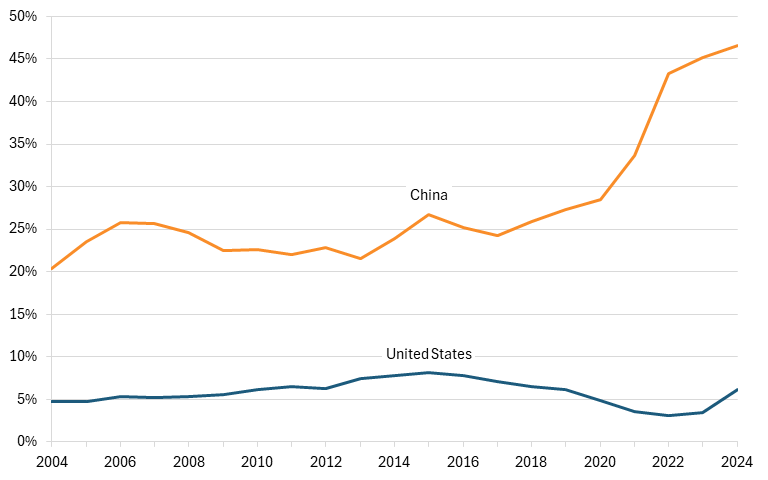

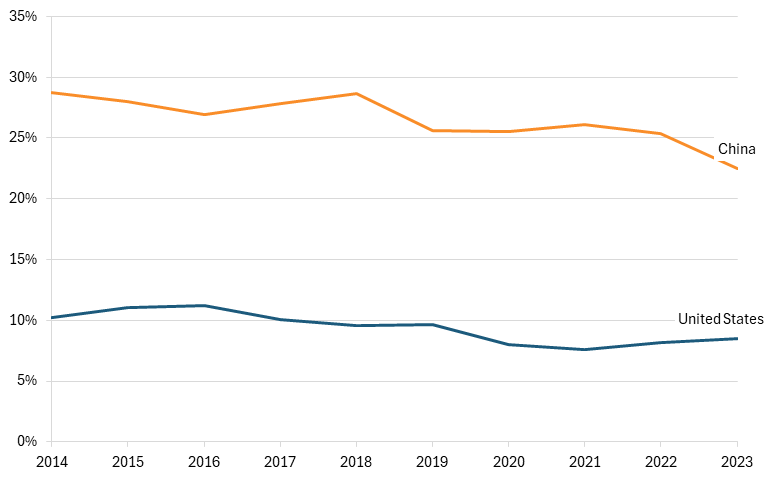

It’s no surprise that, given these favorable policies, China has become the world’s largest battery manufacturer. In 2024, China’s share of storage battery exports (HS code 8507) reached a peak of 46 percent, meaning that almost half of all storage batteries exported originated in China. China’s exports are far above those of the United States, despite recent investments in the industry, as U.S. exports accounted for just over 5 percent of global exports in 2024, as seen in figure 35.

**Figure 35: United States’ and China’s shares of global exports of storage batteries**

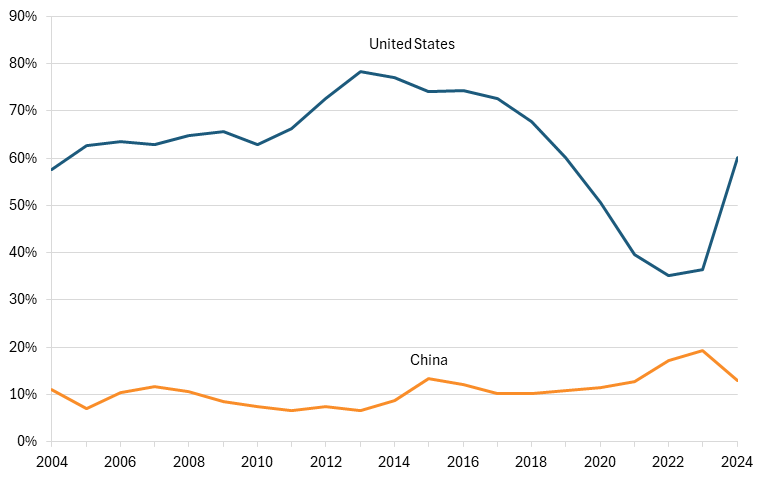

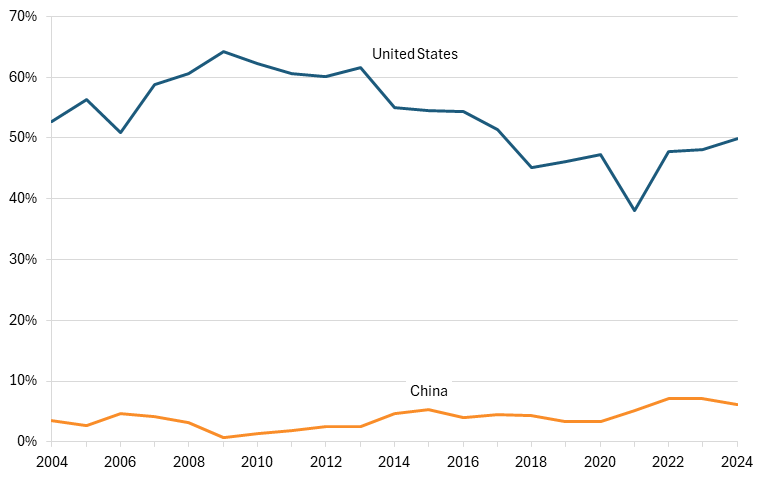

Despite its dominance in the storage battery industry, China has so far failed to take a significant share of the export market of America’s closest trade partners. Canada and Mexico are the two largest destinations for U.S. storage battery exports, and for much of the early to mid 2000s, the United States accounted for the majority of battery exports to those two countries. Its share of exports increased from 60 percent to about 80 percent from 2004 to 2013, but then experienced a decline, falling to a nadir of just 35 percent in 2022. In the years since, U.S. exports have rebounded, jumping back to 60 percent in 2024. In contrast, China has slowly increased its exports to these countries, with its export share increasing from about 10 percent in 2004 to 20 percent in 2023. In 2024, China’s share of exports to Canada and Mexico declined to 13 percent, as shown in figure 36.

**Figure 36: United States’ and China’s shares of storage battery exports to Canada and Mexico**

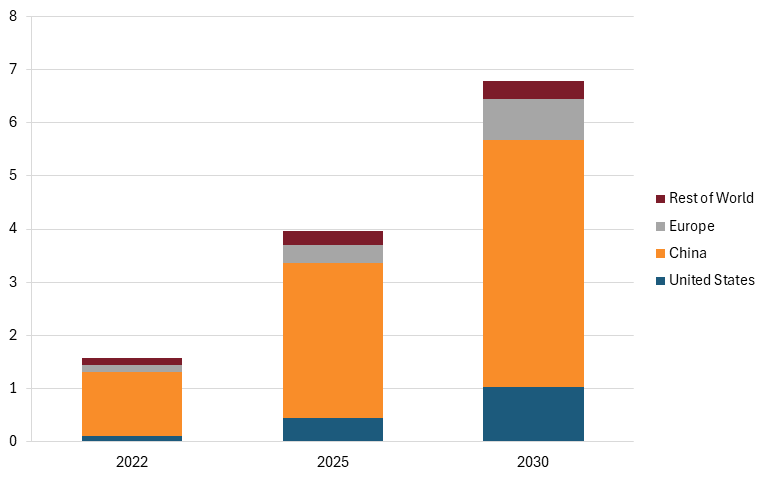

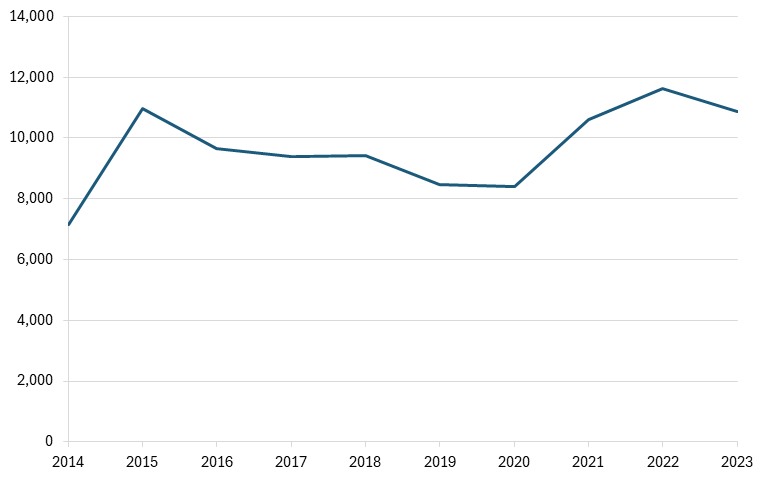

According to IEA, China is expected to increase its battery manufacturing capacity significantly over the next several years, but additional capacity created in the United States and Europe in response to a critical need to diversify the battery supply chain is set to erode China’s lead in global market share. By 2030, IEA estimates that China will account for about two-thirds of the global market share, and its manufacturing capacity will rise to 4.7 terawatt-hours (TWh). The United States, heavily influenced by the growth of domestic manufacturing in states such as Georgia, is expected to see its lithium-ion battery manufacturing more than double between 2025 and 2030, reaching 1 TWh. (See figure 37).

**Figure 37: Lithium-ion battery manufacturing capacity, TWh (projected for 2025 and 2030)[90](#_edn90)**

China’s dominance in battery manufacturing poses a direct threat to U.S. firms seeking to enter or expand in the global battery market, and recent U.S. policy actions put the future of battery manufacturing in Georgia and other states at risk. As Chinese firms continue to benefit greatly from favorable policies and massive subsidies from the federal and provincial governments, American policymakers must view battery manufacturing not just as another industry but also as one critical to national power. In Georgia, the storage battery industry has been a boon to the economy, resulting in thousands of jobs and high levels of economic growth. However, failing to protect and empower this industry on the state and federal levels will threaten the progress that has already been made, resulting in the continued loss of global market share, slower growth, and weaker job creation—a threat to the Georgia economy.

## Hawaii: Optical Instrument and Lens Manufacturing (NAICS 333314)

Hawaii has developed a niche but strategically important presence in optical instrument and lens manufacturing, an industry that supports scientific research, defense, and advanced imaging technologies. However, the industry operates in an increasingly competitive global market in which China’s rapid expansion—supported by concerted industrial policy and state-backed financing—poses a growing threat to U.S. producers.

Optical instruments and lens manufacturing includes the production of microscopes, telescopes, surveying instruments, and precision optical components used across aerospace, defense, medical, and research applications. Institutions in Hawaii, such as the University of Hawaii and observatories on Mauna Kea, have helped foster a localized ecosystem of optical engineering and precision manufacturing.[91](#_edn91) Firms such as Oceanit Laboratories and smaller precision optics contractors contribute to this specialized manufacturing base, often serving defense and research markets.[92](#_edn92)

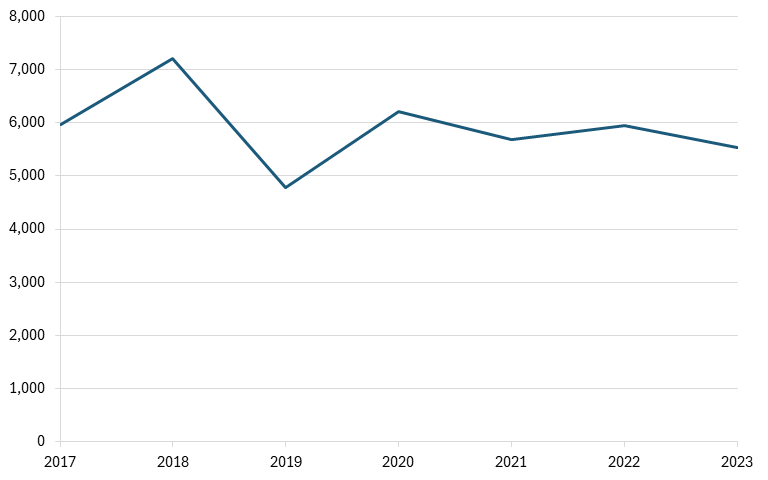

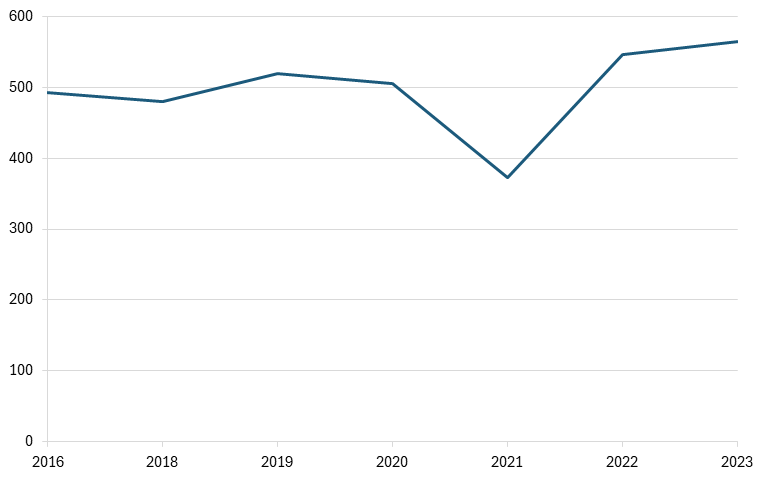

Despite its relatively small size, Hawaii’s optical manufacturing workforce has remained stable and has shown modest growth in recent years. Employment declined from just over 50 workers in 2018 (the first year of available data) to about 34 in 2020, then rebounded to approximately 51 by 2023, reflecting both the volatility and resilience of this niche sector.[93](#_edn93)

**Figure 38: Number of workers in optical instrument and lens manufacturing in Hawaii**

At the national level, the United States remains a significant producer of high-end optical instruments, particularly in advanced and defense-related applications. However, it is a relatively small player in the global export market compared with China, which has rapidly expanded its production capacity across a wide range of optical goods, including lower- and mid-range instruments.

China’s rise in the optical instruments and lens industry has been substantial. In the early 2000s, China held a larger share of global exports (HS code 9001, 9002, 9005, 9011, 9013), than the United States did, holding about 17 percent compared with the United States’ 9 percent. Over the next decade, China steadily increased its share, reaching a peak of 33 percent in 2021, while the United States saw its share hover between 4 and 7 percent. However, in 2022, Chinese exports experienced a sudden dip, dropping to about 16 percent in 2024, while the U.S. export share increased to 12 percent.[94](#_edn94) (See figure 39.)

**Figure 39: United States’ and China’s shares of global exports of optical instruments and lenses**

China’s dominance in this industry (at least up until 2022) has been enabled in large part by Chinese government support. Optical and precision instruments are identified as priority sectors under China’s Made in China 2025 strategy, which emphasizes high-end manufacturing and technological self-sufficiency.[95](#_edn95) Chinese firms benefit from a range of policy tools, including direct subsidies, tax incentives, discounted land, and below-market financing from state-owned banks. According to analyses by the OECD, such support mechanisms reduce production costs and allow Chinese firms to scale rapidly, often leading to overcapacity and downward pressure on global prices.[96](#_edn96)

Major Chinese firms in the optical instruments industry include Sunny Optical Technology, one of the world’s largest manufacturers of optical components and camera modules, as well as firms such as OFILM, which produces optical and imaging components for consumer electronics and industrial applications.[97](#_edn97) These firms have benefited from strong domestic demand and government-backed expansion into global markets. In contrast, U.S. optical manufacturing is concentrated in high-value, specialized segments. Leading American firms such as Teledyne Technologies focus on precision optics, photonics, and scientific instrumentation for specific industries.[98](#_edn98)

China’s continued expansion in optical manufacturing—fueled by state support, economies of scale, and aggressive export strategies—poses a long-term risk to U.S. producers. As Chinese firms move up the value chain and compete more directly with high-end manufacturers, the competitive pressures facing U.S. firms are likely to intensify. For Hawaii, where the industry is small and highly specialized, these global dynamics translate into heightened vulnerability. Maintaining a strong foothold in this industry will depend on continued investment in research, innovation, and defense-related applications. Without such support, the state’s niche optical manufacturing sector risks being overshadowed by lower-cost, state-backed competitors in the global market, and the United States risks ceding greater shares of the export market to Chinese competitors.

## Idaho: Semiconductor and Related Device Manufacturing (NAICS 334413)

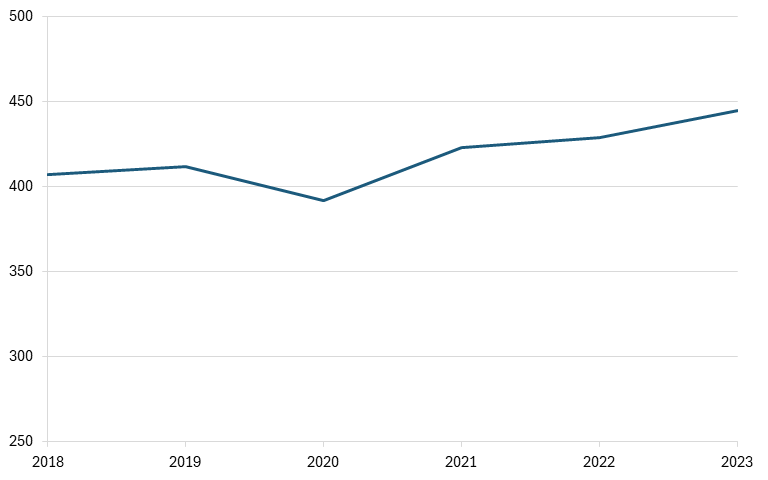

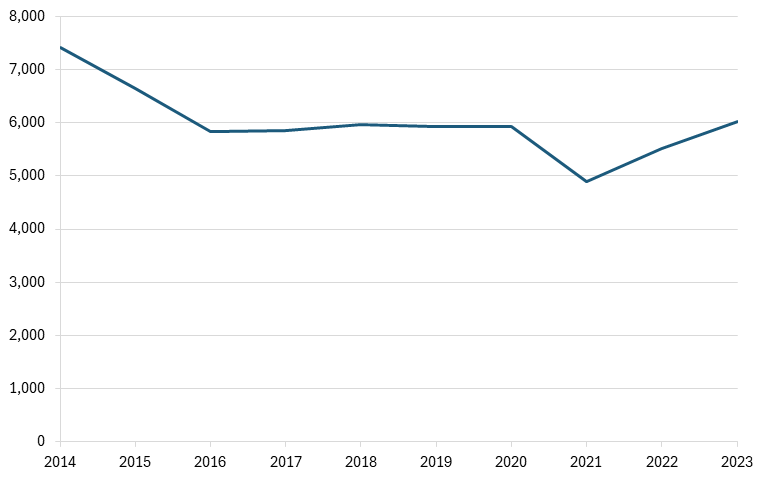

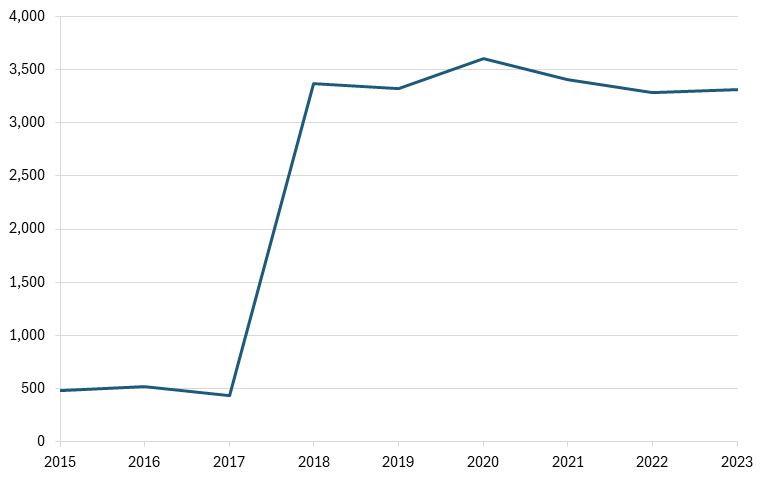

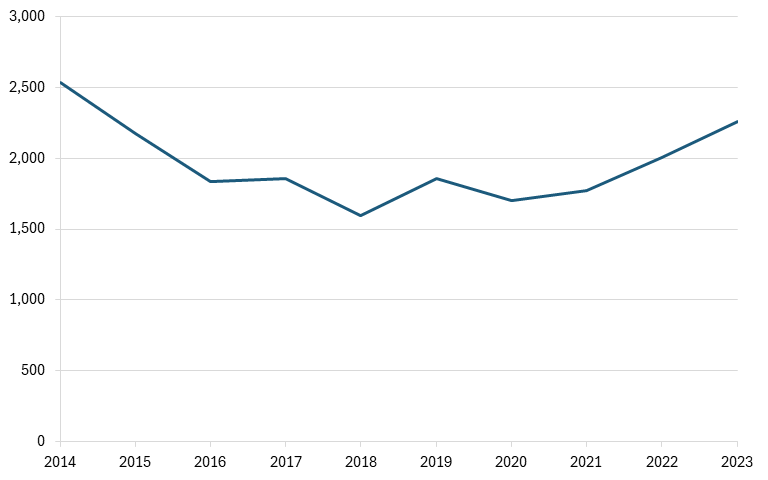

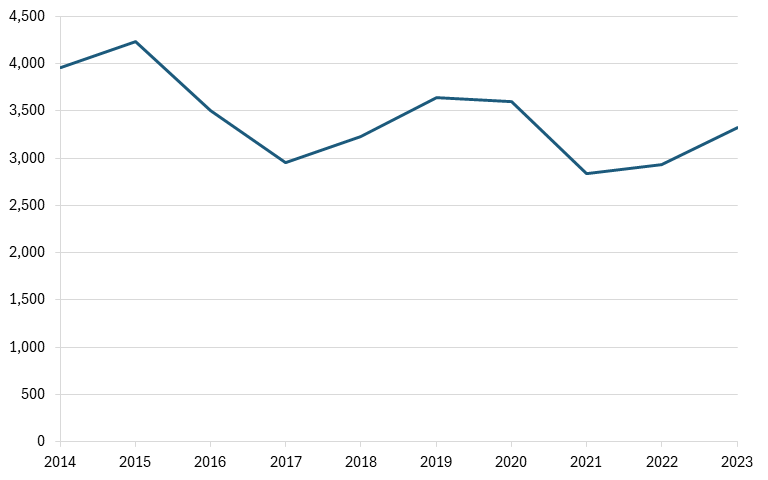

Idaho is specialized in and dependent on the semiconductor industry, which operates in a highly competitive global market. Micron, a leading producer of memory semiconductors that’s headquartered in Idaho, is poised to make a significant investment in the Idaho economy and increase manufacturing output. However, China’s extensive subsidies to its own memory chip manufacturer pose a significant challenge to Micron’s future domestic manufacturing success.

The semiconductor industry is Idaho’s largest export industry, exporting $539 million in 2022.[99](#_edn99) It is also one of the largest employers in the state, employing just over 6,000 workers in 2023. However, since 2018, employment in the semiconductor manufacturing industry has declined by roughly 9 percent while Idaho’s overall workforce has increased by nearly 19 percent, demonstrating a decline in the industry despite high levels of economic output.[100](#_edn100) (See figure 40).

**Figure 40: Employment in the semiconductor manufacturing industry in Idaho**

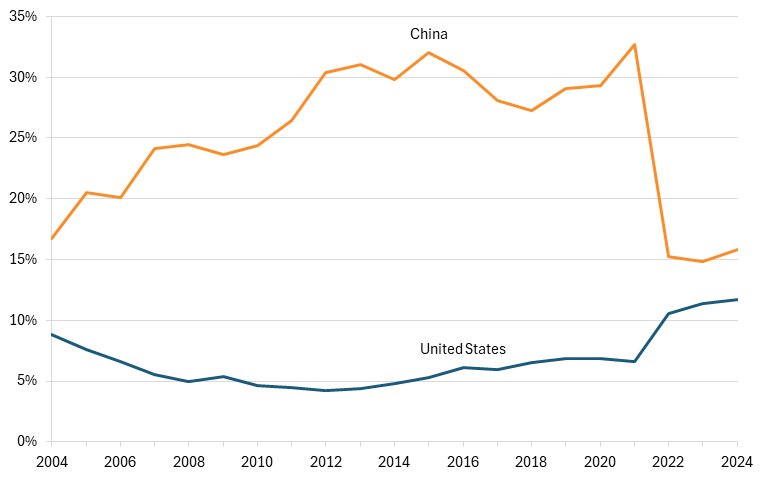

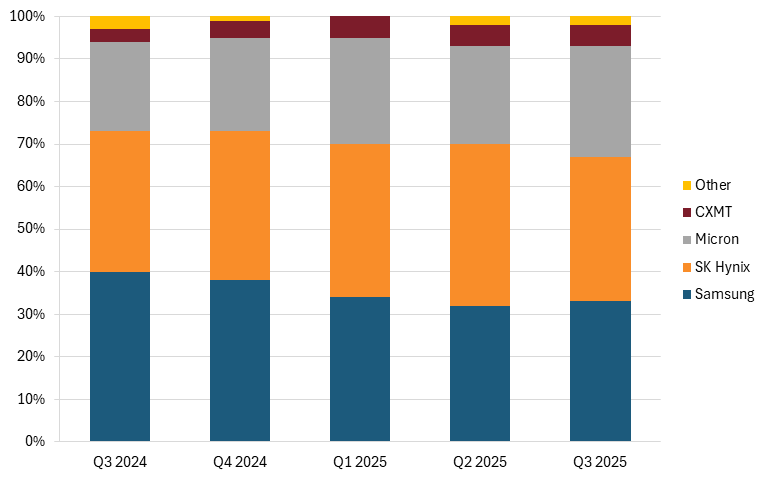

Micron, one of the largest dynamic random access memory (DRAM) chip manufacturers in the world, is the state’s largest employer, employing 10,000 workers and contributing substantially to the $2.5 billion in value added created by the Idaho semiconductor industry.[101](#_edn101) DRAM chips are essential for the construction of data centers and the build-out of AI, as they provide the high-bandwidth memory needed to power AI server computations.[[102]](#_edn102) Micron controls 26 percent of the global market share in this industry, behind South Korean firms Samsung and SK Hynix.[[103]](#_edn103) Though this industry has historically been dominated by these three firms, Chinese competitor ChangXin Memory Technology (CXMT) has made waves in the global market, rising to the fourth-largest firm and holding 5 percent of global market share in late 2025.[[104]](#_edn104) (See figure 41.)

CXMT was founded by the local government of the Chinese city of Hefei and receives substantial subsidies from the Chinese national government.[[105]](#_edn105) The Chinese government plans to invest over $150 billion in the semiconductor industry by 2030, nearly three times the $52 billion invested by the United States in the CHIPS and Science Act in 2022.[[106]](#_edn106) What’s more, the Chinese government has recently indicated that DRAM memory technologies are a priority area for future subsidies, a benefit for CXMT, and a potential threat to Micron.[[107]](#_edn107)

**Figure 41: Global DRAM chip market share by revenue[108](#_edn108)**

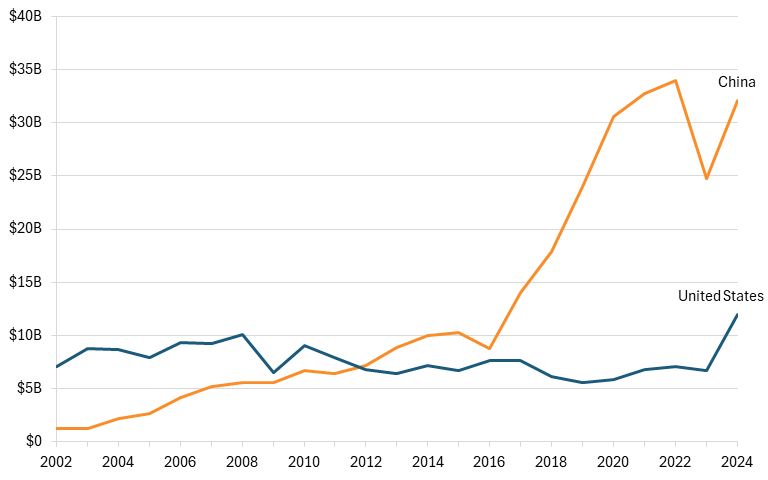

Despite Micron’s success, memory chip manufacturing has historically been offshored, with very few fabs operating in the United States. However, Micron has announced that it will increase its investment in the U.S. semiconductor manufacturing industry, with plans to build two new fabs in Idaho, one of which will be operational by 2027.[[109]](#_edn109) These investments will likely increase U.S. exports of memory chips (HS 854232), which fell by 64 percent from 2014 to 2024. In comparison, China, with its significant subsidies, saw exports increase nearly threefold over the same period. (See figure 42.)

**Figure 42: Memory semiconductor exports**

However, Micron’s expansion of domestic production does not guarantee increased exports. The U.S. Commerce Department has noted that China’s chip industry expansion poses a threat to new chip facilities in the United States, and that new Chinese chip capacity could lead U.S. and allied countries’ fabs to produce fewer chips than is necessary to remain profitable.[[110]](#_edn110) Between 2022 and 2026, China is expected to increase production capacity by building more new fabs and completing more major expansions than any other region in the world, bringing 26 facilities online, compared with only 16 in the Americas.[111](#_edn111) (See figure 43.)

**Figure 43: New fabs and major expansions to come online, 2022–2026[112](#_edn112)**

The high subsidies in the Chinese semiconductor industry enable Chinese firms to sell semiconductors at lower prices than U.S. competitors can, at times selling chips below production cost. Chinese manufacturers sell chips 30 to 50 percent cheaper than U.S. suppliers, making their products more attractive in third-party markets.[113](#_edn113) U.S. exports of memory chips to Malaysia, Singapore, and Vietnam have grown at a fraction of the pace of China’s since 2014, with Chinese exports to these markets 38-times greater in value than U.S. exports. (See figure 44.)

**Figure 44: Memory semiconductor exports to Malaysia, Singapore, and Vietnam**

In China’s Made in China 2025 strategy, the government explicitly aims to achieve 70 percent self-sufficiency in semiconductor products by 2025 and to become the leader in semiconductor manufacturing, including DRAM chips, by 2030.[114](#_edn114) Although these goals haven’t yet been reached, China-based firms are expected to continue to grow rapidly as policy support and government subsidy programs remain aligned with these objectives.

China’s push for dominance in the global semiconductor market and its emergence in the memory chip market pose a direct threat to U.S. firms, and its progress is not expected to slow.[[115]](#_edn115) As Chinese producers replace U.S. suppliers domestically and expand aggressively into third-country markets, U.S. semiconductor exports will face sustained erosion in global market share, revenue, and profitability. Chinese firms such as CXMT will continue to receive financial benefits unmatched by U.S. competitors, enabling them to retain and gain market share at the expense of American and allied firms. Chinese authorities will continue to aggressively subsidize the semiconductor industry in order to reach their $150 billion target, thereby contributing to artificially low prices for Chinese firms. For Idaho, which has seen both a recent decline in its semiconductor industry and heightened investment in the industry, these trends are worrying, as China’s dominance in this industry could translate into slower growth and weaker job creation in the state’s most important traded industry.

## Illinois: Construction Machinery Manufacturing (NAICS 333120)

Illinois is specialized in and dependent on the construction equipment manufacturing industry, which operates in a highly competitive global market. Despite the dominance of American firms in this industry, many of which are based in Illinois, Chinese firms have become legitimate players on the global stage. China’s use of subsidies and artificial demand shocks has contributed to the rapid growth of Chinese construction equipment manufacturers, posing a significant risk to the future success of American firms.

Machinery manufacturing is the second-largest export industry in Illinois (behind chemical manufacturing), with exports valued at $12.5 billion in 2024.[116](#_edn116) Construction machinery exports alone accounted for $1.8 billion, driven by the presence of some of the largest manufacturers in the world.[117](#_edn117) Illinois employs about 1/10th of the country’s workforce in construction machinery manufacturing, with about 5,500 employees as of 2023. However, the number of employees has declined by about 7 percent since 2017, while, in comparison, Illinois’s total workforce has grown by 3 percent.[118](#_edn118) (See figure 45.)

**Figure 45: Employment in construction machinery manufacturing in Illinois**

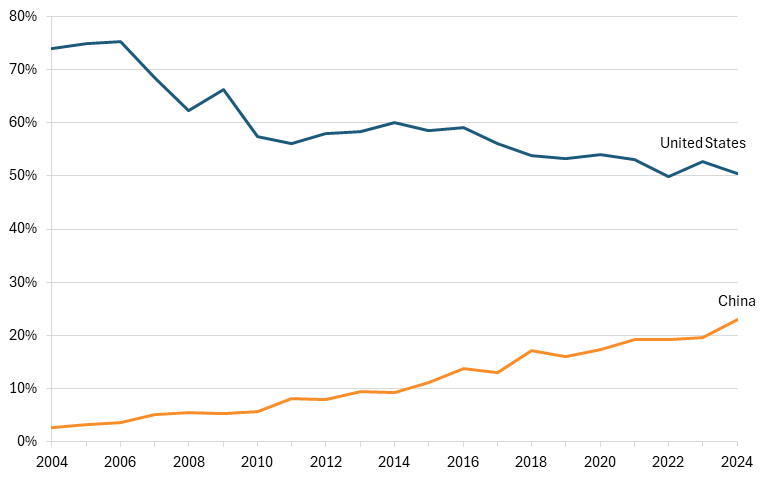

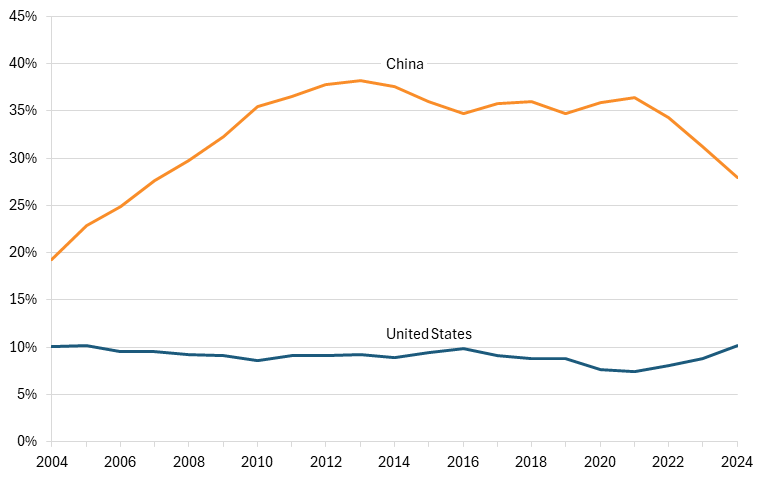

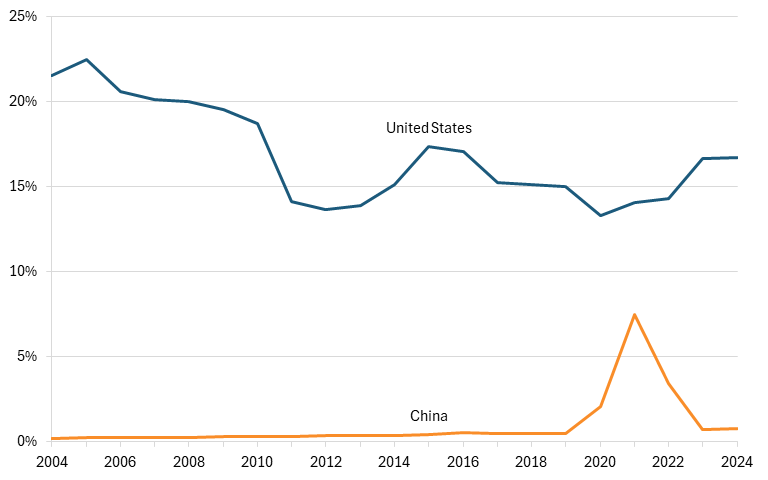

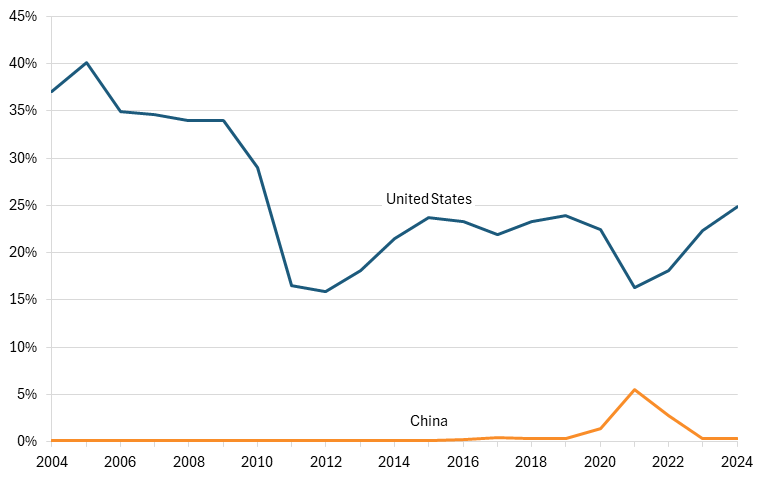

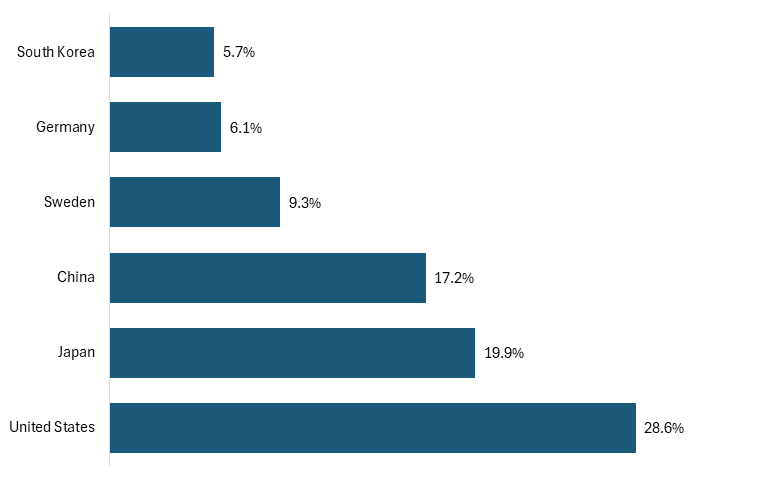

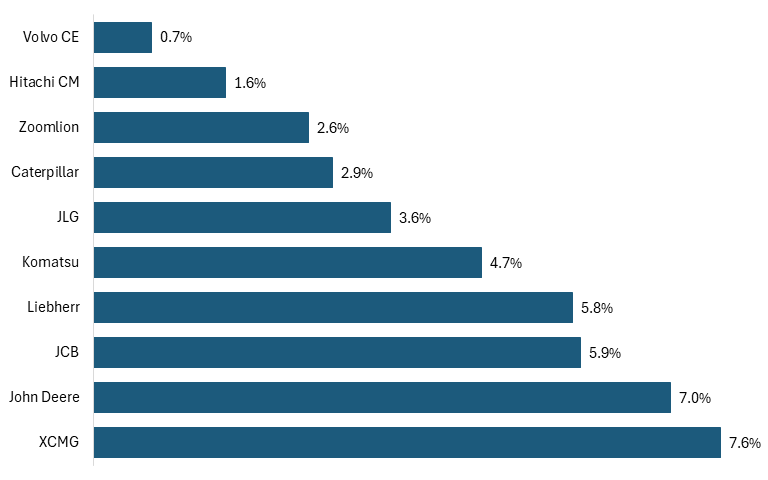

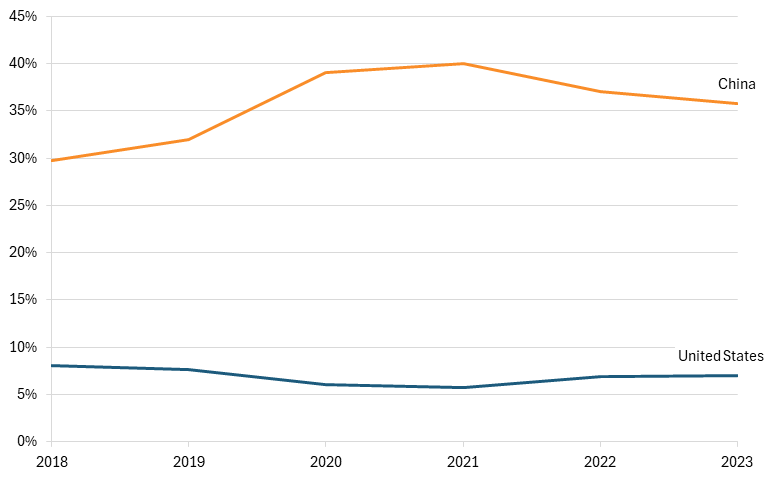

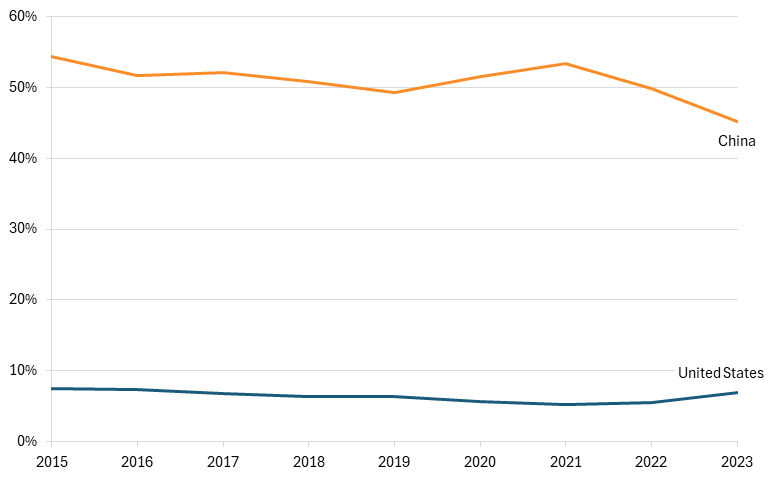

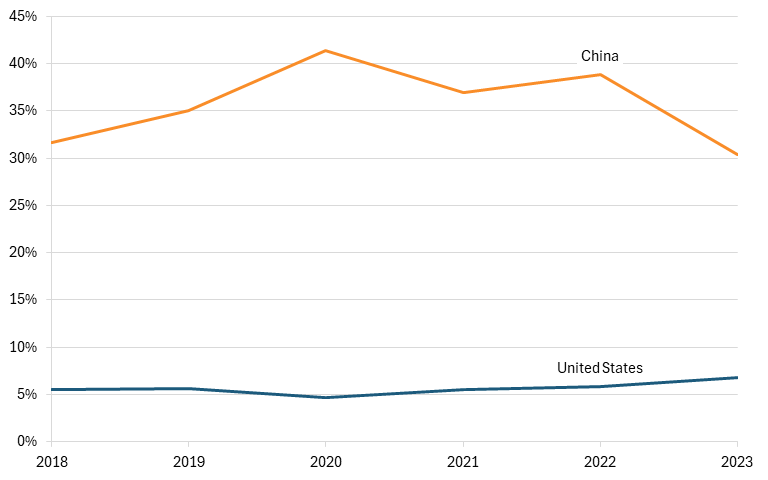

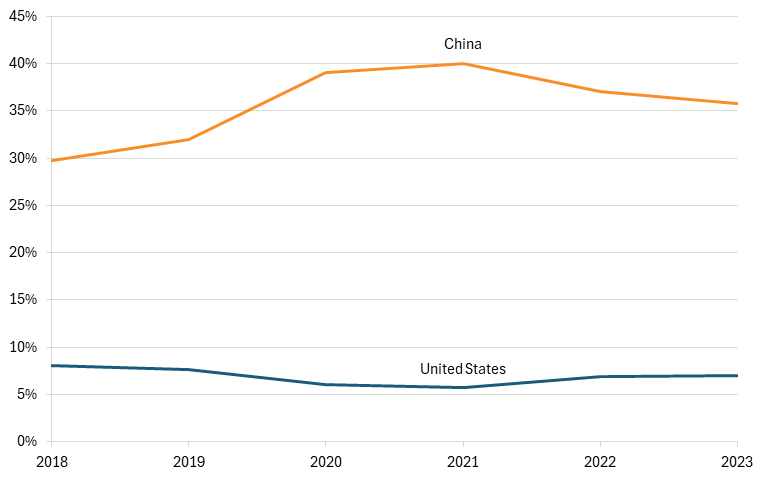

Caterpillar and John Deere, the first and third-largest construction equipment manufacturers by global revenue, are each headquartered in Illinois, while Komatsu, the second-largest firm by global revenue, also maintains manufacturing operations in the state.[119](#_edn119) In total, American firms control roughly 27 percent of the global market share in this industry, ahead of Japan (21 percent) and China (18 percent). (See figure 46.)

**Figure 46: Global market share in construction equipment by revenue, 2025[120](#_edn120)**

However, American leadership in this industry is far from guaranteed. While employment has declined in Illinois, U.S. global market share has also seen a decline, falling by more than 1 percentage point between 2024 and 2025, while China increased its market share by an equal amount. Chinese firms have benefited from the national government’s financial and policy support, including several policies that increase demand for industrial equipment. First, Chinese construction equipment firms have received direct government subsidies, enabling them to produce more goods and sell them at lower prices. In 2022 and 2023, XCMG, the largest construction manufacturer in China and the fourth-largest in the world, received $56 million and $94 million in government subsidies, respectively.[[121]](#_edn121) The European Union has also found evidence of subsidization and dumping by the Chinese construction equipment industry, which allowed Chinese firms to sell products at below-market prices, making it difficult for European firms to compete.[[122]](#_edn122)