What Manufacturing Rebound?

With a new president in the White House, it’s worth looking back and assessing the performance of U.S. manufacturing during the last four years. Defenders of the Biden administration’s record argue that “manufacturing is back.” For example, former Energy Secretary Jennifer Granholm wrote on X: “Make no mistake—@POTUS’ industrial strategy has revived American manufacturing, created jobs, and made our country more secure.” The New York Times wrote recently, “The manufacturing sector has more jobs than under any president since Mr. Bush.” And Mark Zandi, chief economist of Moody’s Analytics, concurred, “President Trump is inheriting an economy that is about as good as it ever gets.”

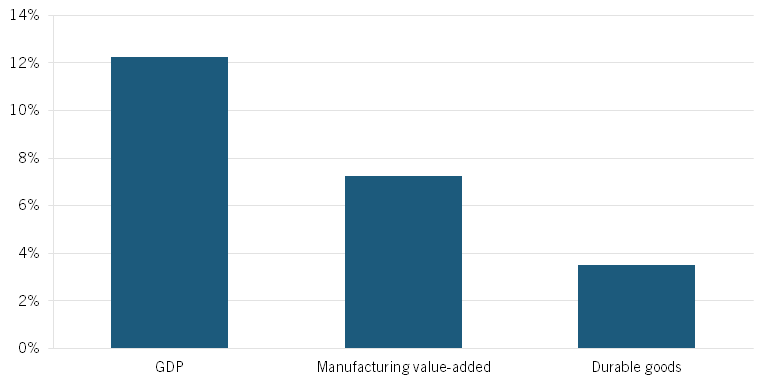

But the reality is that, according to the Bureau of Economic Analysis, inflation-adjusted U.S. manufacturing value-added output grew at less than two-thirds the rate of the rest of the U.S. economy from the 4th quarter of 2019 through the 3rd quarter of 2024 (the first quarter of 2020 was artificially low because of COVID, and 4th quarter 2024 numbers have not yet been released).

This is not meant to be a knock on the accomplishments of the Biden administration. It is meant to be an injection of reality: Yes, U.S. manufacturing grew over the last four years, but as a share of U.S. GDP it got smaller, not larger. The durable goods sector, which includes semiconductors, steel for infrastructure, and clean energy equipment, grew at a rate 70 percent slower than the rest of the economy. If manufacturing policy is based on feel-good statements out of touch with that reality, then the United States will never fix the problem.

Figure 1: Cumulative U.S. growth, Q4 2019 to Q3 2024

It is certainly possible, and even likely, that these numbers will look better in a few years. After all. Congress appropriated hundreds of billions of dollars in spending and tax incentives that will go to manufacturers for items like broadband equipment, infrastructure materials, clean energy products, and of course semiconductors. The problem is that very little of this money has gone into manufacturing projects. Most of the CHIPS Act projects were approved only in the last 6 months. No broadband funding awards have been made. And infrastructure projects were slow to get started. Let’s hope we see this rebound reflected in the BEA numbers in the next few years.

But a more important point is that it is not the right framing to tout how investments accounted for a manufacturing strategy and will lead to a manufacturing rebound. America’s challenge is not more manufacturing output or jobs. What difference does it make if we double or triple manufacturing output in easy-to-make sectors like wood products, furniture, plastics, and textiles? They are not strategically important for the country’s economic competitiveness or national security. They are low value-added goods. And at one level, who even cares if we produce solar panels? That is not a strategically important industry, either. If we were dependent on China for solar panels and they decided to cut us off, then existing solar panels would still work and we’d just use other technologies to produce additional electricity, such as natural gas turbines. What really matters is what happens to advanced, dual-use sectors like semiconductors and computing, machinery and equipment, biopharmaceuticals, aerospace and motor vehicles—industries that China is now running away with at America’s expense.

It’s not clear whether the Trump administration will have an advanced-manufacturing strategy or just a manufacturing strategy. But the reality is that potato chip production is not the same as computer chip production. And the sooner both political parties recognize this and prioritize it—not manufacturing per se, but advanced manufacturing—the better off the nation will be.