China Is Following the Same Path as the Asian Tigers

While China remains much poorer than its wealthier neighbors on a per-capita basis, it has been on the same growth trajectory. Essentially, China has experienced the same growth trend that some of the Asian Tigers, such as South Korea, have experienced. Only China’s path is about 25 years behind.

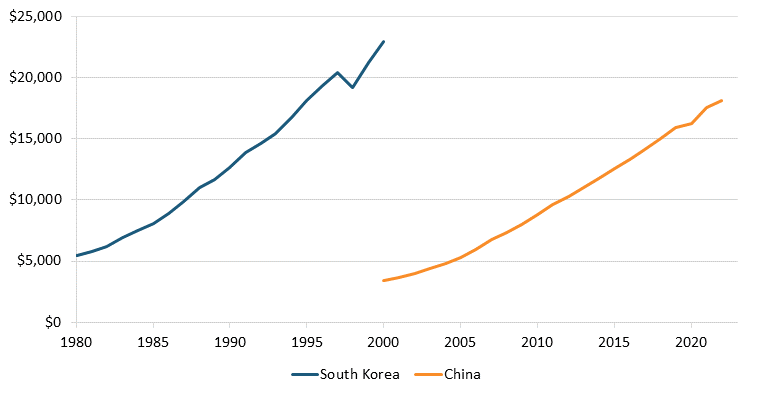

For instance, China’s real per-capita GDP grew from around $5,300 to around $18,100 from 2005 to 2022. That is an increase of about 242 percent over that period. About 25 years earlier, South Korea experienced almost the same trend over a similar period. Between 1980 and 1997, real per-capita GDP grew from around $5,500 to around $20,400. That’s an increase of about 272 percent. These trends should be an eye-opener to anyone who is concerned about China’s rising influence. If current growth rates continue, then China could easily get to where South Korea is currently in 20- to 30-years’ time. This would mean that China’s GDP would go from 29 percent of US levels today to around 80 percent by 2050. It would be putting hope over experience to believe that China could not become as wealthy as its neighbors. (See table 1 and figure 1)

Table 1: 25-year per-capita GDP growth for China and South Korea (constant 2017 PPP $)

|

Country |

Period |

Growth |

% Growth |

|

China |

2005-2022 |

$12,823 |

242% |

|

South Korea |

1980-1997 |

$14,903 |

272% |

Figure 1: Growth trend of per-capita GDP for China and South Korea (constant 2017 PPP $) (International Monetary Fund)

Some will point out that the Chinese economy has been in trouble the last year-and-a-half, often as a way to suggest that its challenge to the United States and our allies is beginning to weaken. However, these challenges are merely short-term business cycle challenges, much of it due to its over-investment in residential construction. Because these issues are cyclical, the United States should not treat them as signs of some kind of protracted, secular decline.

There is also the view that China relies too heavily on exports, which would make it difficult to move to consumer-led growth. This is a fallacy of simplistic Keynesian thinking that holds that growth can only come from consumption, government spending, investment, or net exports. But such a framework pertains more to short-term business cycle dynamics. South Korea did not experience its phenomenal growth because of exports, but because of productivity growth.

Ultimately, long-run growth can only come from two sources: labor force expansion and productivity growth. This gets to another flawed talking point; one that pertains to China’s shifting age structure. It is certainly true that China’s aging population will lead to labor force stagnation and eventual shrinkage. However, this ignores productivity’s equally important role as a driver of continued GDP growth over the longer term. For instance, a recent analysis from the Dallas Fed found that total factor productivity, a proxy for technological innovation, has been the single biggest contributor to China’s per-capita GDP growth. By contrast, the size of the working-age population constituted very little. Given China’s massive investments in new and emerging technologies as part of Made in China 2025, it is wrong to assume that there will be some sort of abrupt productivity stagnation any time soon.

Editors’ Recommendations

August 28, 2023