Schumpeter Is Right, Brandeis Is Wrong: Large Retailers Benefit the Economy More Than Small Retailers

Large retail companies are more productive than small retailers. That is why they can offer better prices to consumers, pay higher wages to their employees, and contribute more to the overall economy—which puts the lie to the neo-Brandeisian argument that “big is bad.”

KEY TAKEAWAYS

Key Takeaways

Contents

Schumpeter Theory in the Retail Sector 3

Retail Firm Size And Productivity 4

Retail Firm Size and Productivity Growth. 9

Retail Firm Size and Price. 12

Introduction

Antitrust rules governing the economy have been affected by proponents of several antitrust schools in recent years.[1] The neo-Schumpeterian and neo-Brandeisian schools of thought are now at battle—and while both schools agree that the Chicago school’s goal of generating static consumer surplus is no longer adequate, their opinions vary on all the other issues. Specifically, they have diverging views about whether it is large or small enterprises that benefit society and the economy more.

The neo-Brandeisians advocate for Justice Louis Brandeis’s traditions, which call for “a democratic distribution of power and opportunity in the political economy.”[2] Neo-Brandeisians prefer smaller businesses to larger ones because they believe that small businesses are less likely to wield any political power. However, empirical evidence does not support this view. Large businesses “spend less on lobbying per dollar of revenue,” and small businesses “wield significant political power through trade associations.”[3] Moreover, this view fails to account for the dynamic structure of an economy, which encourages innovation. Neo-Schumpeterians favor large firms because large firms with market power spend more on research and development and are more innovative.[4] However, the dominant firm’s market power is not entrenched because “new goods and services, firms, and industries compete with existing ones in the marketplace, taking customers by offering lower prices, better performance, new features, and catchier styling.”[5]

Trends in the U.S. retail industry show how the neo-Schumpeterian view of the economy is more accurate. Schumpeter’s process of creative destruction in the economy is played out in the transition to larger, more productive retailers and has resulted in larger retail enterprises, faster productivity growth, higher incomes, and lower pricing. Instead of promoting small, less-efficient merchants while punishing giant retailers, governments should take a position of size neutrality.

Schumpeter Theory in the Retail Sector

The evolution of the retail sector towards large firms shows how Schumpeterian theory plays out in the economy. The shift to larger firms in recent decades is not new. The historical evolution of the retail sector is one in which the size of retailers has become increasingly larger owing to economies of scale. In the mid-to the late-1800s, the department store carrying multiple lines of products replaced small specialty stores with their efficiency and low prices.[6] Despite department stores’ capacity to fill multiple floors with merchandise for consumers, the next stage of the retailing evolution shifted to an even larger and more efficient retailing format: the chain store.[7] Early chain stores, such as A&P, did not hold an enormous quantity of merchandise in a single location as in early department stores. However, they were generally larger than department stores due to their multiple establishments.[8]

The shift toward large retailers did not conclude with chain stores. In the next stage of the retailing evolution, big-box stores adopted the large, efficient department store and chain store model to become retailers selling extensive lines of products at multiple large-scale establishments.[9] In other words, they were larger than department and chain stores. The most recent stage of the retailing evolution has shifted toward online platforms that can scale even further because space does not constrain them.[10] Although all these types of retailers continue to exist, consumers have shifted toward shopping at larger retailers. The trend toward huge stores demonstrates how this sector exemplifies Schumpeter’s notion of creative destruction.

The process of creative destruction in a dynamically evolving retail sector shows how, increasingly, larger retailers are more efficient and how they benefit the economy with lower prices.

At each step in the growth of retailing, these ever-larger retailers have become more efficient. For instance, department shops eliminated wholesale intermediaries, thereby decreasing the input costs required to purchase merchandise.[11] Chain stores then adopted these methods. Yet, they also centralized their marketing and purchasing functions, further increasing their efficiency.[12] In the next stage, big-box stores adopted new technologies while reducing overhead costs, becoming even more efficient than chain stores.[13] Finally, online platforms used a combination of technologies to sell virtually any product online and deliver products efficiently to busy consumers, becoming even more efficient than big-box stores.[14] Moreover, each of these retailers reduced costs because of their increased efficiency, which they then passed on to consumers at lower prices.[15] In other words, the process of creative destruction in a dynamically evolving retail sector shows how, increasingly, larger retailers are more efficient and how they benefit the economy with lower prices.

Moreover, the process of creative destruction, resulting in a shift toward larger retailers, also has driven productivity growth for the sector. Consider, for example, the case of Walmart. According to McKinsey & Company, a large portion of productivity growth since 1995 has been attributed to innovative technological processes that have increased the firm’s efficiency.[16] In the general-merchandise retailing industry, “productivity growth more than tripled after 1995 because competitors started more rapidly adopting Wal-Mart’s innovations—including the large-scale (‘big-box’) format.”[17] Due to Walmart’s innovations, “competitors increased their productivity by 28 percent from 1995 to 1999, while Wal-Mart … [increased] their productivity by an additional 22 percent.”[18] This productivity growth happened only because the process of creative destruction shifted the sector from chain stores to big-box stores.

The shift to larger retailers has also resulted in higher wages for workers. The National Bureau of Economic Research has found that “wage rates in the retail sector increase markedly with firm and establishment sizes. By holding a constant set of standard control variables, pay is 15 percent higher in large firms (1,000-plus workers) than in small firms (less than ten workers) for the high school educated. For those with some college education or a degree, pay is 25 percent higher in large than small firms.”[19] The creative destruction process, shifting the sector toward larger retailers, plays a role in higher wages for the sector.

The Schumpeterian process of creative destruction has shifted the retail sector toward larger, more productive firms.

Despite the shift toward large retail firms, the majority of retail industries are still competitive. According to Ali Hortacsu and Chad Syverson (2015), the concentration ratio of the four largest firms (CR4) in the retail sector rose from 7.9 percent in 1997 to 12.3 percent in 2007.[20] However, a CR4 of the overall retail sector does not show the actual environment of the retail market because lumping all retail industries into a single sector implies that, for example, car dealers are competing with supermarkets for customers. Moreover, even if retail concentration could be measured as a sector, a CR4 of 12.3 percent is still competitive. The concentration of industries provides a clearer picture of the retail market’s competitive environment. Data shows that the majority of retail industries did not shift from a competitive to a highly concentrated market from 2002 to 2017 despite the shift toward larger retail firms.[21]

The Schumpeterian process of creative destruction has shifted the retail sector toward larger, more productive firms. As a result, the sector’s productivity has increased, retail employees are paid higher wages, and consumers pay lower prices. In other words, the trend toward large retail firms has been economically beneficial.

The following sections utilize economic data to demonstrate how the retail sector has transitioned toward more productive, bigger enterprises. In addition, the data indicates that this change has resulted in increased retail productivity, increased wages, and decreased prices. Unless otherwise specified, “large firms” refers to companies with more than 500 employees, and small firms to those with fewer than 20 employees.

Retail Firm Size And Productivity

Large firms are generally more productive than small firms. The Organization for Economic Development claims that “large firms are on average more productive than smaller ones … [because] of increasing returns to scale through capital-intensive production.”[22] The retail sector is not different. The creative destruction process shows that retail firms have become increasingly larger at each stage of the retail evolution, from department stores to online marketplaces. Foster, Haltiwanger, and Krizan (2006) explain that the sector is shifting toward larger firms because retailers belonging to larger firms, such as national chains, are more productive, displacing less-productive retailers belonging to single-unit establishment firms.[23]

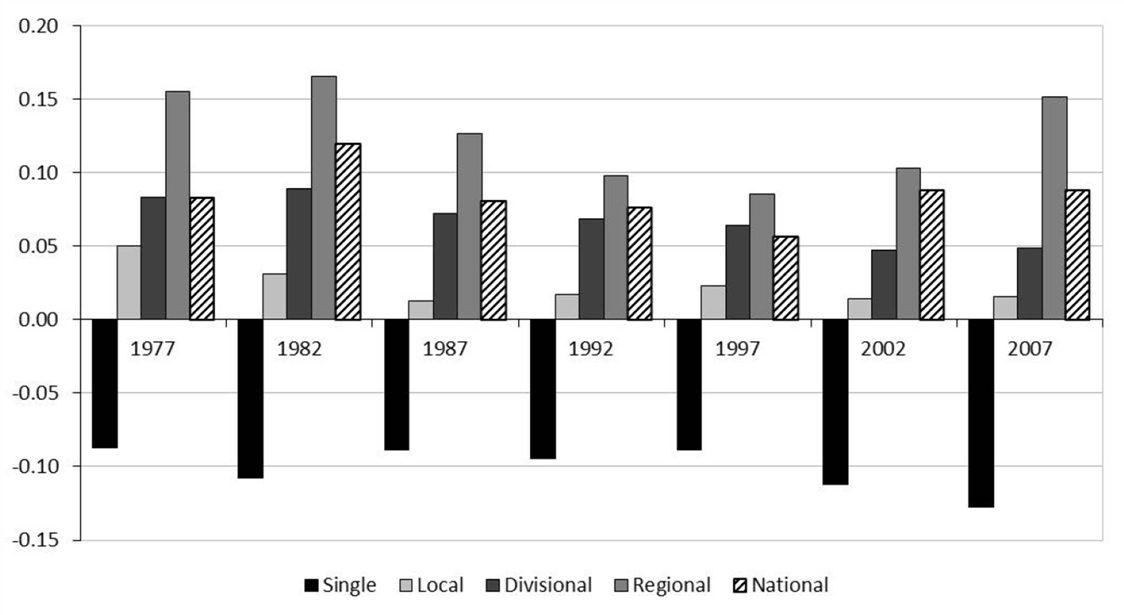

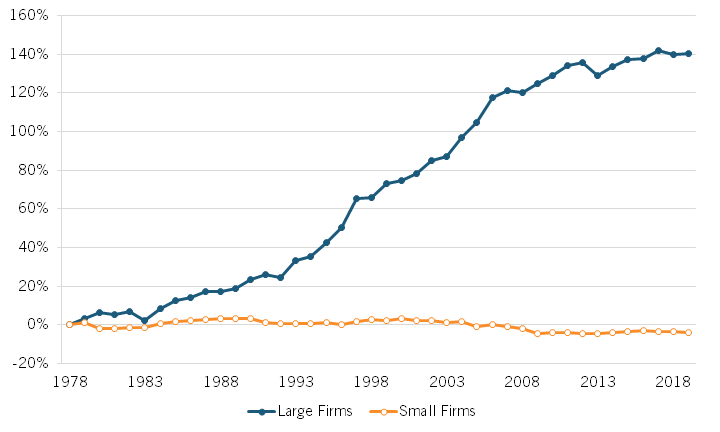

A study using the Longitudinal Business Database and Census of Retail Trade finds that, in 2007, the productivity levels of national chains (described as firms with multiple establishments operating in 18 or more states) were approximately 0.08 greater than the industry’s average employment-weighted productivity levels, which is measured as the log of total sales over total employment.[24] In contrast, the productivity levels of single-establishment retail firms were approximately 0.12 below the industry’s mean productivity level.[25] Although the figures vary over time, the productivity level of national chains was consistently higher than the industry average, whereas those of single-establishment firms have been below average since 1977.[26] (See figure 1.) In other words, the productivity levels of large firms, such as national chains, tend to be higher than smaller single-unit retail firms.

Figure 1: Employment-weighted mean firm-level productivity by chain size[27]

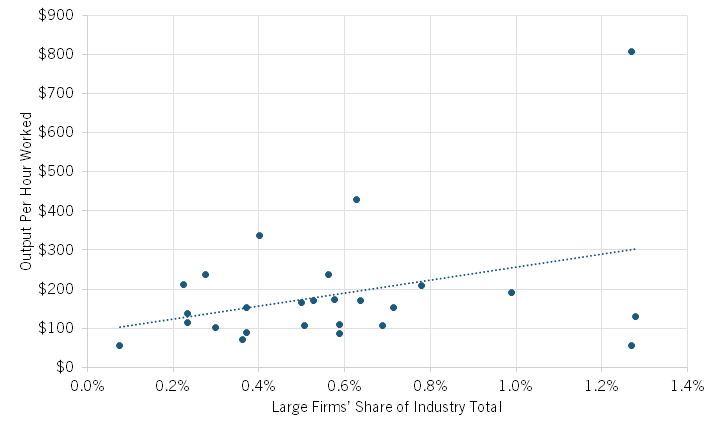

Large retail firms are still associated with higher productivity. A correlation between the share of large firms in 26 4-digit retail NAICS industries and their respective sectoral output per hour worked—a measure of productivity—in 2019 resulted in a coefficient of 0.35, meaning that industries with a higher share of large firms also had higher productivity levels.[28] In contrast, the same correlation for small firms found a coefficient of -0.32, meaning that industries with a larger share of small firms tend to have lower output per hour.[29] (See figure 2.)

Figure 2: Retail industries’ productivity vs. number of large firms, 2019[30]

The Role of Technology in Large Firm Productivity

The high productivity of large firms can be partially attributed to their better usage of information technology. An analysis of large and small firms in the 1990s from Doms, Jarmin, and Klimek (2003) finds that “coefficients on the IT share variable are positive and significant for the large firm sample and negative and insignificant for the small firm sample … this result is suggestive that large firms were more able to exploit IT investments to improve productivity.”[31] Large retail firms are more capable of using technology to increase their output without changing their inputs than small retail firms.

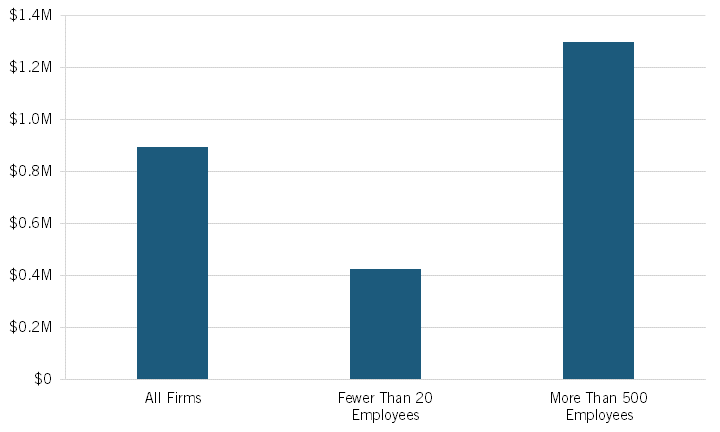

Online shopping and mail-order houses are one of the better industries to look at for determining whether large retail organizations are more capable of leveraging technology to boost their productivity, as measured by sales per worker. Retail industries with brick-and-mortar stores may employ technology to increase productivity; however, other factors impacting sales per worker, such as in-store customer service, might obscure whether greater technology use is essential to large enterprises’ increased productivity. In contrast, the shopping experience and subsequent revenues in Internet shopping and mail-order businesses depend heavily on technology deployment. As a result, quantifying the influence of technology on productivity, or sales per worker, of large and small businesses in this industry is less complicated.

Large retail firms in the online shopping and mail-order houses industry are more productive than their smaller counterparts. In 2017, the average sales per worker of large firms in this industry was $1.3 million. By contrast, the average sales per worker for small firms in this industry was $425,000. (See figure 3.) Although sales per worker is not a perfect measure of productivity, the difference between large and small firms’ average sales per worker shows that large firms are generally better at implementing technology to increase their productivity than are small firms. Consequently, large retail firms have higher productivity than do their small counterparts.

Figure 3: Online shopping and mail-order house sales per worker by firm size[32]

Retail Firm Size Trends

Retail firms are becoming larger in order to benefit from scale economies. A National Bureau of Economic Research study finds that, from 1958 to 2000, “all the growth in the number of retail outlets and most of the growth in retail employment [came] from retail firms that operate multiple establishments.”[33] The growing number of stores and employees in the retail sector has resulted in increasingly larger firms. Moreover, the study finds that employment growth exceeded that of retail establishments, meaning the average size of stores also increased.[34] In other words, consumers prefer to shop at large chain stores more today than they did 40 years ago, and retail firms are responding to this preference.[35]

Whereas less-productive, smaller retail firms and their respective establishments exited the market, the more-productive larger retail firms remained while increasing their establishments in order to benefit from scale economies.

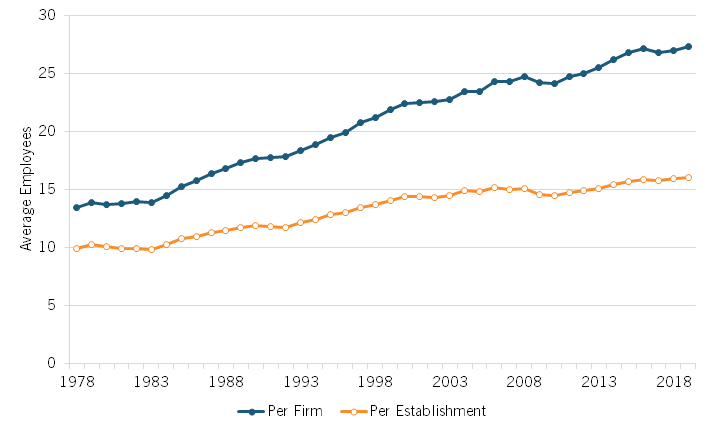

Retail firm and establishment sizes have continued to grow. The Bureau of Labor Statistics describes an “establishment” as a “single physical location where one predominant activity occurs.”[36] A “firm” is described as “an establishment or a combination of establishments” and can “operate in one or multiple industries.”[37] From 1978 to 2019, the average number of employees per firm more than doubled from 13.4 to 27.3.[38] Moreover, retail firms have increased their establishment size. From 1978 to 2019, the average establishment size rose from 9.9 employees to 16.1 employees.[39] In other words, the retail sector shifted toward larger firms and stores. (See figure 4.)

The average firm size grew faster than the average establishment size because firms shut faster than establishments. From 1978 to 2019, the number of retail firms declined by 21 percent, whereas that of establishments declined by only 1 percent.[40] Meanwhile, the number of employees has increased, growing by 60 percent during that same period.[41] In other words, whereas less-productive, smaller retail firms and their respective establishments exited the market, the more productive larger retail firms remained while increasing their establishments in order to benefit from scale economies.

Figure 4: Average number of employees per retail firm and establishment, 1978–2019[42]

According to Hortacsu and Syverson (2015), the shift toward larger firms in the retail sector is due to the “increasing importance of network economies.… For example, economies of scale in procurement, logistics, or brand, would all encourage a larger scale of operations, at least at the firm level.”[43] Disaggregating the above statistics provides indirect evidence that the shift toward larger retail firms is partially attributed to economies of scale. From 1978 to 2019, the share of large firms’ establishments rose from 15.6 percent to 33.9 percent due to the benefits from scale economies in areas such as logistics.[44] Due to the rapid growth in the number of establishments, the number of employees for large firms has also increased. As a result, the average size of large retail firms rose by 143.1 percent during that period.[45] By contrast, the share of establishments belonging to small firms declined from 71.2 percent to 54.1 percent.[46] (See figure 5.) Small firms’ average number of employees decreased by 3.8 percent from 1978 to 2019.[47] Large firms grew at a higher rate because they benefited more from economies of scale than did small firms.

Figure 5: Change in average employees per retail firm 1978–2019[48]

Retail Firm Size and Productivity Growth

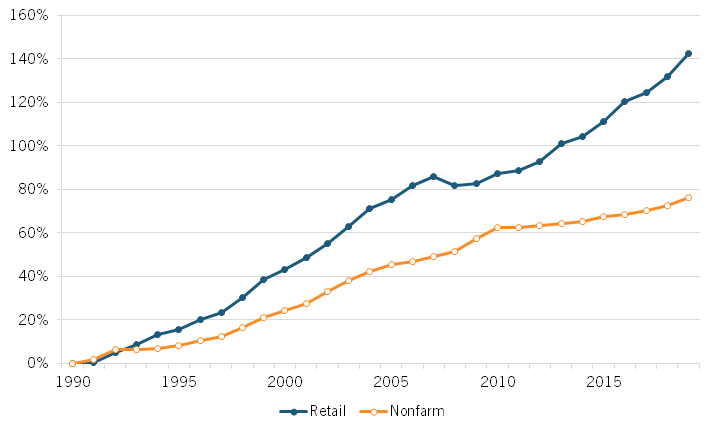

Retail sector productivity has grown as the sector has shifted to more productive, larger retailers. From 1990 to 2019, the retail sector’s productivity grew at an annual average of 3.1 percent compared with the nonfarm sector’s annual average of 2 percent.[49] The retail sector’s productivity grew by 142 percent during this period, almost double the nonfarm business sector’s growth of 76 percent.[50] In other words, the retail sector’s productivity grew faster than did the average sector’s during its shift toward larger retailers, meaning large firms played a partial role in the sector’s productivity growth. (See figure 6.)

Figure 6: Retail sector versus nonfarm business sector productivity change 1990–2019[51]

The study by Foster, Haltiwanger, and Krizan (2006) showed that the shift toward larger retailers played a role in the sector’s productivity growth.[52] The authors found that “all of the labor productivity growth in the retail sector is accounted for by more productive entering establishments displacing less productive exiting establishments … entering high-productivity establishments from large, national chains play a disproportionate role.”[53] Large retail firms play a significant role in the sector’s productivity growth because of the investment and adoption of information technology.[54]

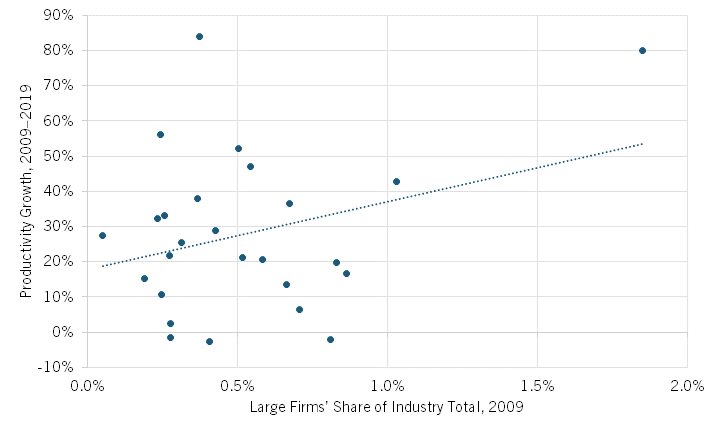

Large firms also continue to play a role in boosting the retail sector’s productivity growth. A correlation between the share of large firms in 2009 and labor productivity percentage change from 2009 to 2019 resulted in a coefficient of 0.31, meaning industries with a higher share of large firms tend to have higher labor productivity growth in the subsequent 10 years.[55] By contrast, the same analysis for small firms resulted in a correlation coefficient of -0.04, signifying that industries with larger shares of small firms are associated with lower or no productivity growth.[56] Taken together, retail industries with a higher share of large firms tend to have higher productivity growth in the following decade, driving growth in the overall sector. (See figure 7.)

Figure 7: Retail industries’ productivity growth vs. number of large firms[57]

Retail Firm Size and Wages

Large retailers pay their workers more than do small retailers. A 2015 study analyzing data from the Current Population Survey (CPS) from 1996 to 2013 finds that large retail firms with more than 1,000 workers compensate their employees with some college education 25 percent more than do small retail firms with fewer than 10 workers.[58] Large retail firms also pay high-school-educated workers 15 percent more than do small firms.[59] One likely explanation for this pay premium in the retail sector is “that employees in larger firms are more productive on average … and that they are compensated for their increased productivity.”[60]

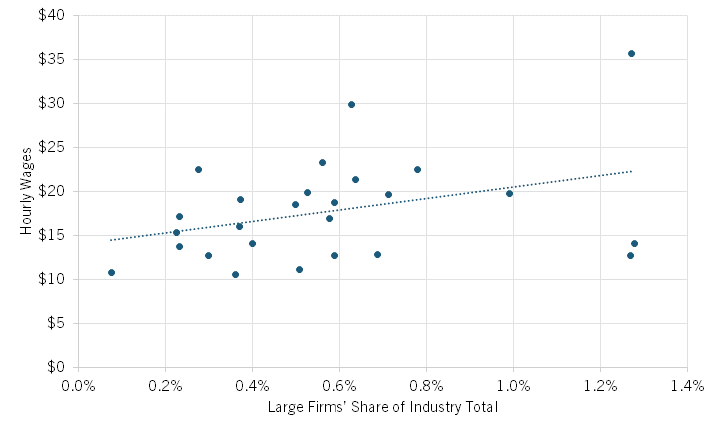

Large firms continue to be associated with higher wages than small firms. A correlation between the share of large retail firms at the 4-digit NAICS level and hourly wages in 2019 resulted in a coefficient of 0.36, meaning industries with a higher share of large firms also had higher wages.[61] A similar correlation for small firms finds that industries with a higher share of small firms were associated with a lower hourly wage, with a coefficient of -0.47.[62] In other words, workers are better off in large retail firms than in small firms. (See figure 8.) Moreover, according to the Washington Center for Equitable Growth, a shift toward large retailers may also increase wages in the sector.[63]

Figure 8: Hourly wages vs. number of large firms in 4-digit NAICS retail industries[64]

Retail Firm Size and Prices

The shift to larger retailers has also lowered consumer prices. According to Giroldo and Hollenbeck (2020), multi-store firms set prices significantly lower than do single-store firms for the same product.[65] For example, the average price difference in 2017 between large and small firms was $0.36, a 5 percent difference when the median retail price was $6.65.[66] Moreover, multi-store firms “do not simply pass their lower costs along to consumers but also charge significantly lower margins” than do single-unit retail firms.[67] One reason for this lower price and margin is economies of scale result in lower wholesale prices.[68] Plus, large firms are more productive than small firms. Bagwell, Ramey, and Spulber (1997) found that “low price firms anticipate a growing sales volume, so they also find large investments in cost reduction more attractive.”[69] These technological investments cut costs and eliminate the “middleman” that increases margins, leading to more efficient processes and lower prices.[70]

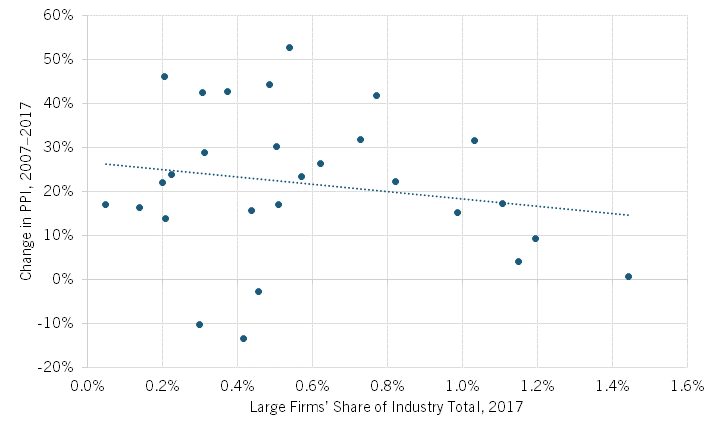

Large retail firms are more likely to be deflationary than small ones are. A correlation between the percentage change in the producer price index from January 2007 to January 2017 and the sales per worker share of large firms in 2017 for 28 retail industries resulted in a correlation coefficient of -0.18, meaning that industries with a higher share of large firms in 2017 experienced fewer price increases in the previous decade.[71] (See figure 9.) The same analysis for small firms in the same 28 retail industries with available data resulted in a correlation coefficient of 0.10, indicating that industries with a higher share of small firms experience more price increases.[72] In other words, large firms play a role in minimizing price increases, benefitting consumers.

Figure 9: Change in producer price index vs. number of large firms[73]

Retail Concentration

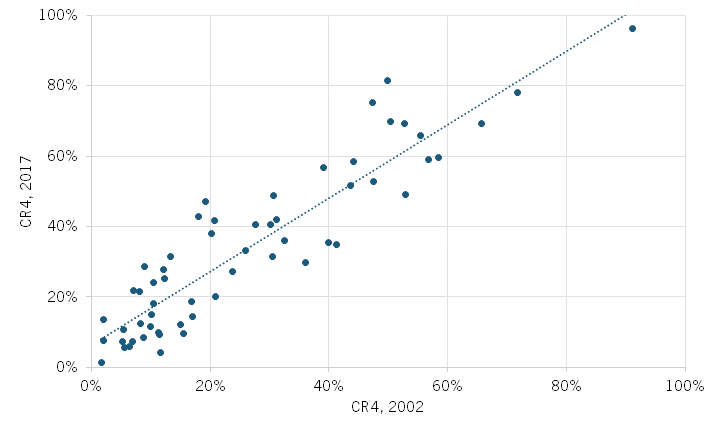

Despite the shift toward large retail firms, the majority of retail industries are not highly concentrated. A market is highly concentrated if the concentration ratio of CR4 is greater than 50 percent.[74] In 2017, the CR4 for 46 of 64 retail industries with available data was below 50 percent.[75] In other words, the majority of retail industries are not concentrated despite the growing preference and continual shift toward larger retailers.

From 2002 to 2017, the CR4 of only 6 of 58 retail industries with available data rose from below to more than 50 percent, meaning only 6 retail industries went from competitive to concentrated.

Moreover, the shift toward larger retailers has not led to growing concentration in retail industries. From 2002 to 2017, the CR4 of only 6 of 58 retail industries with available data rose from below to over 50 percent, meaning only 6 retail industries went from competitive to concentrated despite the shift toward larger firms in the overall retail sector.[76] In other words, the competitive retail industries stayed competitive, and those concentrated stayed concentrated. (See figure 10.) The shift toward more productive, large retail firms did not create a more concentrated market for the majority of retail industries.

Figure 10: CR4 in retail industries, 2017 vs. 2002[77]

Policy Recommendations

Policymakers should oppose legislation targeting large retailers because of their size. Over the last few decades, the shift toward large retailers has played a key role in U.S. economic growth. Critics promote legislation such as the American Innovation and Choice Online Act (AICOA) that “restricts normal business practice, imposing common-carrier obligations” based on a company’s market capitalization and would reduce the productivity of large online retail firms.[78] In other words, bills such as the AICOA would reduce economic productivity. Moreover, this intervention in large online retail firms’ business practices would hurt workers who rely on their higher wages and consumers who depend on their lower prices.

At the same time, policymakers should not revive the Robinson-Patman Act, which seeks to intervene in the efficient buying practices of large retail firms. Named after former senator Joseph Robinson (D-AR) and representative Wright Patman (D-TX), the act prohibits buyers from receiving lower prices regardless of the “efficiencies firms generate that come with scale, as well as how lower prices at the wholesale level can lead to lower prices for consumers.”[79] For example, the American Economic Liberties Project has asserted that large retailers “like Walmart and Amazon … extract discriminatory prices and other favorable terms from all the sellers;” however, they do not consider the “price differences between [buyers were often due to] service costs, selling costs, purchase volumes, [and] wholesale functions performed by the buyer.”[80] Price differences, in other words, often reflected phenomena that led to high firm productivity or economies of scale.”[81] As a result, heeding Federal Trade Commission (FTC) chair Khan and commissioner Bedoya’s calls to revive the Robinson-Patman Act would hurt the efficiency of large retailers and shift market shares to smaller, less-efficient ones. The shift in market share would only hurt consumers and the economy with lower productivity and higher prices.

Bills such as the AICOA would reduce economic productivity. Moreover, intervention in large online retail firms’ business practices would hurt workers who rely on their higher wages and consumers who depend on their lower prices.

In general, policymakers should take a neo-Schumpeterian perspective toward general antitrust measures. The retail industry exemplifies how creative destruction improves innovative efficiency; in this example, it results in a greater variety of stores, which helps the economy. As a result, the neo-Schumpeterian approach is the most accurate representation of how the economy runs, and gives insights into how to boost its prosperity.

Conclusion

Over the past several decades, the trend toward larger, more-productive retail firms has played a significant role in enhancing the sector’s productivity and wages while also helping to reduce inflation. Despite this, neo-Brandeisians continue to hold an ideological animus toward large retailers specifically and large firms overall, believing that small retailers are not really business owners, but a form of victimized proletariat. Policymakers should not fall for this rhetoric and instead should adopt a position of size neutrality.

In addition, the trend toward enormous stores has demonstrated that these businesses contribute positively to the economy and that this movement itself results from the Schumpeterian process of creative destruction. To put it another way, the trend toward enormous stores demonstrates that neo-Schumpeterian theories provide a more accurate depiction of the economy. Therefore, antitrust and economic policymakers must adopt a neo-Schumpeterian perspective.[82]

Acknowledgment

The authors would like to thank Rob Atkinson for his help on this report. Any errors or omissions are the authors’ responsibility alone.

About the Authors

Trelysa Long is a research assistant for antitrust policy with ITIF’s Schumpeter Project on Competition Policy. She was previously an economic policy intern with the U.S. Chamber of Commerce. She earned her bachelor’s degree in economics and political science from the University of California, Irvine.

Dr. Aurelien Portuese (@aurelienportues) is the director of the Schumpeter Project on Competition Policy at ITIF. He focuses on the interactions of competition and innovation. Portuese holds a Ph.D. in law and economics from the University of Paris II (Sorbonne), an M.Sc. in Political Economy from the London School of Economics, and an LL.M. from the University of Hamburg. Portuese’s latest book, Algorithmic Antitrust, was published in 2022 by Springer.

The Information Technology and Innovation Foundation (ITIF) is an independent 501(c)(3) nonprofit, nonpartisan research and educational institute that has been recognized repeatedly as the world’s leading think tank for science and technology policy. Its mission is to formulate, evaluate, and promote policy solutions that accelerate innovation and boost productivity to spur growth, opportunity, and progress. For more information, visit itif.org/about.

Endnotes

[1]. Aurelien Portuese, “Biden Antitrust: The Paradox of the New Antitrust Populism,” George Mason Law Review volume 29, issue 4 (2022) https://lawreview.gmu.edu/print__issues/biden-antitrust-the-paradox-of-the-new-antitrust-populism/.

[2]. Lina Khan “The New Brandeis Movement: America’s Antimonopoly Debate,” Journal of European Competition Law & Practice 9, no.3 (2018), https://academic.oup.com/jeclap/article/9/3/131/4915966.

[3]. Hadi Houalla, “Oops! It Turns Out Aggressive Antitrust Would Increase Business Lobbying” (ITIF, January 2023), https://itif.org/publications/2023/01/18/oops-it-turns-out-aggressive-antitrust-would-increase-business-lobbying/.

[4]. Franklin Fisher and Peter Temin, “Returns to Scale in Research and Development: What Does the Schumpeterian Hypothesis Imply?” Journal of Political Economy 81, no. 1 (1973): 57, http://www.jstor.org/stable/1837326.

[5]. Ibid.

[6]. Aurelien Portuese and Trelysa Long, “The Process of Creative Destruction, Illustrated: The US Retail Industry” (ITIF, October 2022), https://itif.org/publications/2022/10/03/the-process-of-creative-destruction-illustrated-the-us-retail-industry/.

[7]. Ibid.

[8]. Ibid.

[9]. Ibid.

[10]. Ibid.

[11]. Ibid.

[12]. Ibid.

[13]. Ibid.

[14]. Ibid.

[15]. Ibid.

[16]. William W. Lewis et. al., “What’s right with the US economy” (McKinsey & Company paper, February 2002), https://www.mckinsey.com/featured-insights/employment-and-growth/whats-right-with-the-us-economy.

[17]. Ibid.

[18]. Ibid.

[19]. Brianna Cardiff-Hicks, “Do Large Modern Retailers Pay Premium Wages?” (working paper for the National Bureau of Economic Research, July 2014), 5, https://www.nber.org/system/files/working_papers/w20313/w20313.pdf.

[20]. Ali Hortacsu and Chad Syverson, “The Ongoing Evolution of US Retail: A Format Tug-of-War,” Journal of Economics Perspectives 29, no. 4 (2015), https://pubs.aeaweb.org/doi/pdfplus/10.1257/jep.29.4.89.

[21]. US Census Bureau, Economic Census Survey 2002 (concentration ratio in file EC0244SSSZ6.zip), accessed March 25, 2022, https://www2.census.gov/econ2002/EC/Sector44/; US Census Bureau, Economic Census Survey 2017 (concentration of largest firms for the US in 2017), accessed December 11, 2022, https://data.census.gov/table?q=EC1700SIZECONCEN:+Selected+Sectors:+Concentration+of+Largest+Firms+for+the+U.S.:+2017&g=0100000US&n=N0600.44&tid=ECNSIZE2017.EC1700SIZECONCEN.

[22]. Organization for Economic Development, “Productivity in SMEs and Large Firms” (technical report, OECD, 2021), https://www.oecd-ilibrary.org/sites/54337c24-en/index.html?itemId=/content/component/54337c24-en.

[23]. Lucia Foster, John Haltiwanger, and C. J. Krizan, “Market Selection, Reallocation, and Restructuring in the U.S. Retail Trade Sector in the 1990s,” The Review of Economics and Statistics 88, no. 4 (2006), https://www.jstor.org/stable/40043032.

[24]. Lucia Foster et. al., “The Evolution of National Retail Chains: How We Got Here,” Center for Economics Studies 15-10 (2015), https://www2.census.gov/ces/wp/2015/CES-WP-15-10.pdf.

[25]. Ibid.

[26]. Ibid.

[27]. Ibid.

[28]. US Census Bureau, Business Dynamics Statistics 1978-2020 (number of firms by size for NAICS 44-45), accessed March 5, 2023, https://data.census.gov/table?d=ECNSVY+Business+Dynamics+Statistics&tid=BDSTIMESERIES.BDSFSIZE; Bureau of Labor Statistics, Labor Productivity and Cost Measures, Detailed Industries (sectoral output and hours worked for NAICS 44-45).

[29]. US Census Bureau, Business Dynamics Statistics 1978-2020; Bureau of Labor Statistics, Labor Productivity and Cost Measures, Detailed Industries.

[30]. US Census Bureau, Business Dynamics Statistics 1978-2020; Bureau of Labor Statistics, Labor Productivity and Cost Measures, Detailed Industries (sectoral output and hours worked for NAICS 44-45).

[31]. Mark Doms, Ron Jarmin, and Shawn Klimek, “IT Investment and Firm Performance in U.S. Retail Trade,” Federal Reserve bank of San Francisco Working Paper 2003-19 (2003), https://www.frbsf.org/economic-research/wp-content/uploads/sites/4/wp03-19bk.pdf.

[32]. Ibid.

[33]. Ronald Jarmin, Shawn Klimek, and Javier Miranda, “The Role of Retail Chains: National, Regional, and Industry Results” (2009), https://www.nber.org/system/files/chapters/c0487/c0487.pdf.

[34]. Ibid.

[35]. Ibid.

[36]. Akbar Sadeghu, David Talan, and Richard Clayton, “Establishment, firms, or enterprise: does the unit of analysis matter?” BLS Monthly Labor Review, November 2016, https://www.bls.gov/opub/mlr/2016/article/establishment-firm-or-enterprise.htm#:~:text=An%20establishment%20is%20a%20single,Internal%20Revenue%20Service%20(IRS).

[37]. Akbar Sadeghu, David Talan, and Richard Clayton, “Establishment, firms, or enterprise: does the unit of analysis matter?” BLS Monthly Labor Review, November 2016, https://www.bls.gov/opub/mlr/2016/article/establishment-firm-or-enterprise.htm#:~:text=An%20establishment%20is%20a%20single,Internal%20Revenue%20Service%20(IRS).

[38]. US Census Bureau, Business Dynamics Statistics 1978-2020.

[39]. Ibid.

[40]. Ibid.

[41]. Ibid.

[42]. Ibid.

[43]. Hortacsu and Syverson, “The Ongoing Evolution of US Retail: A format Tug-of-War.”

[44]. US Census Bureau, Business Dynamics Statistics 1978-2020.

[45]. Ibid.

[46]. Ibid.

[47]. Ibid.

[48]. Ibid.

[49]. Bureau of Labor Statistics, Labor Productivity and Cost Measures for Detailed Industries (productivity index for NAICS 44-45); Bureau of Labor Statistics, Labor Productivity and Cost Measures for Major Sectors (productivity index for nonfarm business sector, accessed November 21, 2022), https://www.bls.gov/productivity/tables/home.htm.

[50]. Bureau of Labor Statistics, Labor Productivity and Cost Measures for Detailed Industries (productivity index for NAICS 44-45); Bureau of Labor Statistics, Labor Productivity and Cost Measures for Major Sectors.

[51]. Bureau of Labor Statistics, Labor Productivity and Cost Measures for Detailed Industries (productivity index for NAICS 44-45); Bureau of Labor Statistics, Labor Productivity and Cost Measures for Major Sectors.

[52]. Foster, Haltiwanger, and Krizan, “Market Selection, Reallocation, and Restructuring in the U.S. Retail Trade Sector in the 1990s.”

[53]. Ibid.

[54]. Doms, Jarmin, and Klimek, “IT Investment and Firm Performance in U.S. Retail Trade”; “Productivity Growth and the Retail Sector,” FRBSF Economic Letter, December 17, 2004, https://www.frbsf.org/wp-content/uploads/sites/4/el2004-37.pdf.

[55]. US Census Bureau, Business Dynamics Statistics 1978-2020 (number of firms by size and annual payroll for NAICS 44-45); Bureau of Labor Statistics, Labor Productivity and Cost Measures, Detailed Industries (sectoral output and hours worked for NAICS 44-45), accessed March 3, 2023, https://www.bls.gov/productivity/tables/.

[56]. US Census Bureau, Business Dynamics Statistics 1978-2020; Bureau of Labor Statistics, Labor Productivity and Cost Measures, Detailed Industries (sectoral output and hours worked for NAICS 44-45).

[57]. US Census Bureau, Business Dynamics Statistics 1978-2020; Bureau of Labor Statistics, Labor Productivity and Cost Measures, Detailed Industries (sectoral output and hours worked for NAICS 44-45).

[58]. Brianna Cardiff-Hicks, Francine Lafontaine, and Kathryn Shaw, “Do Large Modern Retailers Pay Premium Wages,��� ILR Review 68, no. 3 (2015), https://www.jstor.org/stable/24810317.

[59]. Ibid.

[60]. Ibid.

[61]. US Census Bureau, Business Dynamics Statistics 1978-2020 (number of firms by size for NAICS 44-45); Bureau of Labor Statistics, Hours Worked and Employment Measures: Detailed industries (hours worked for NAICS 44-45).

[62]. US Census Bureau, Business Dynamics Statistics 1978-2020 (number of firms by size for NAICS 44-45); Bureau of Labor Statistics, Hours Worked and Employment Measures: Detailed industries (hours worked for NAICS 44-45).

[63]. “The retail sector and the future of American wages,” Washington Center for Equitable Growth, July 28, 2014, https://equitablegrowth.org/retail-sector-future-american-wages/.

[64]. US Census Bureau, Business Dynamics Statistics 1978-2020 (number of firms by size for NAICS 44-45); Bureau of Labor Statistics, Hours Worked and Employment Measures: Detailed industries (hours worked for NAICS 44-45).

[65]. Renato Zaterka Giroldo and Brett Hollenbeck, “Winning Big: Scale and Success in Retail,” (research paper, Federal Trade Commission, 2020), https://www.ftc.gov/system/files/documents/public_events/1567421/hollenbeckgiroldo.pdf.

[66]. Ibid.

[67]. Ibid.

[68]. Ibid.

[69]. Kyle Bagwell, Garey Ramey, and Daniel F. Spulber, “Dynamic Retail Price and Investment Competition,” The RAND Journal of Economics 28, no. 2 (1997), https://www.jstor.org/stable/2555802.

[70]. Ibid.

[71]. US Census Bureau, Statistics of U.S. Businesses (SUSB) (2017 share of firms by size for NAICS 44-45); US Bureau of Labor Statistics, Producer Price Index Industry Data (producer price index from Jan 2007 to Dec 2017 for NAICS 44-45 at the 6-digit NAICS level), accessed on December, 12, 2022, https://data.bls.gov/PDQWeb/pc.

[72]. Ibid.

[73]. Ibid.

[74]. Environment Protection Agency, “§316(b) EEA Chapter 4 for New Facilities” (Washington, D.C., Environmental Protection Agency), https://www3.epa.gov/npdes/pubs/chapter4g.pdf.

[75]. US Census Bureau, Economic Census Survey 2017 (concentration of largest firms for the US in 2017, accessed December 11, 2022), https://data.census.gov/table?q=EC1700SIZECONCEN:+Selected+Sectors:+Concentration+of+Largest+Firms+for+the+U.S.:+2017&g=0100000US&n=N0600.44&tid=ECNSIZE2017.EC1700SIZECONCEN.

[76]. US Census Bureau, Economic Census Survey 2002 (concentration ratio in file EC0244SSSZ6.zip, accessed March 25, 2022), https://www2.census.gov/econ2002/EC/Sector44/; US Census Bureau, Economic Census Survey 2017 (concentration of largest firms for the US in 2017, accessed December 11, 2022), https://data.census.gov/table?q=EC1700SIZECONCEN:+Selected+Sectors:+Concentration+of+Largest+Firms+for+the+U.S.:+2017&g=0100000US&n=N0600.44&tid=ECNSIZE2017.EC1700SIZECONCEN.

[77]. US Census Bureau, Economic Census Survey 2002 (concentration ratio in file EC0244SSSZ6.zip, accessed March 25, 2022), https://www2.census.gov/econ2002/EC/Sector44/; US Census Bureau, Economic Census Survey 2017 (concentration of largest firms for the US in 2017, accessed December 11, 2022), https://data.census.gov/table?q=EC1700SIZECONCEN:+Selected+Sectors:+Concentration+of+Largest+Firms+for+the+U.S.:+2017&g=0100000US&n=N0600.44&tid=ECNSIZE2017.EC1700SIZECONCEN.

[78]. “Analysis of the American Innovation and Choice Online Act (AICOA): Putting the Brakes on Innovation” (Computer & communications Industry Association), https://ccianet.org/wp-content/uploads/2021/10/Analysis-of-the-American-Innovation-and-Choice-Online-Act-AICOA_-Putting-the-Brakes-on-Innovation.pdf.

[79]. Jeffrey Westling, “FTC to Use Robinson-Patman Act as an Antitrust Tool to Target Large Retailers,” American Action Forum, October 11, 2022, https://www.americanactionforum.org/insight/ftc-to-use-robinson-patman-act-as-an-antitrust-tool-to-target-large-retailer/.

[80]. Katherine Van Dyck, “Price Discrimination and Power Buyers: Why Giant Retailers Dominate the Economy and How to Stop It” (American Economic Liberties Project, September 2022), https://www.economicliberties.us/our-work/price-discrimination-and-power-buyers-why-giant-retailers-dominate-the-economy-and-how-to-stop-it/; Ryan Bourne and Rachel Chiu, “The Zombie Robinson-Patman Act Doesn’t Deserve Revival” (Cato Institute, October 2022), https://www.cato.org/blog/zombie-robinson-patman-act-doesnt-deserve-revival.

[81]. Katherine Van Dyck, “Price Discrimination and Power Buyers: Why Giant Retailers Dominate the Economy and How to Stop It” (American Economic Liberties Project, September 2022), https://www.economicliberties.us/our-work/price-discrimination-and-power-buyers-why-giant-retailers-dominate-the-economy-and-how-to-stop-it/; Ryan Bourne and Rachel Chiu, “The Zombie Robinson-Patman Act Doesn’t Deserve Revival” (Cato Institute, October 2022), https://www.cato.org/blog/zombie-robinson-patman-act-doesnt-deserve-revival.

[82]. Aurelien Portuese, “Principles of Dynamic Antitrust” (ITIF Report, June 2021), https://itif.org/publications/2021/06/14/principles-dynamic-antitrust-competing-through-innovation/; Aurelien Portuese, “Principles of Dynamic Antitrust” (CD Howe Report, September 2021), https://www.cdhowe.org/sites/default/files/IM-Portuese_2021_0917.pdf ; Aurelien Portuese and Joshua Wright, “Antitrust Populism: Towards a Taxonomy,” Stanford Journal of Law, Business & Finance, volume 25, issue 131 (2020), https://law.stanford.edu/publications/antitrust-populism-towards-a-taxonomy/.