Recent U.S. Manufacturing Employment Growth Hides the Sector’s Abysmal Productivity Performance

Over the last two years, the U.S. economy has added 830,000 manufacturing jobs. At first glance, this suggests a renewed strength in manufacturing. In reality, it masks a new weakness: productivity decline.

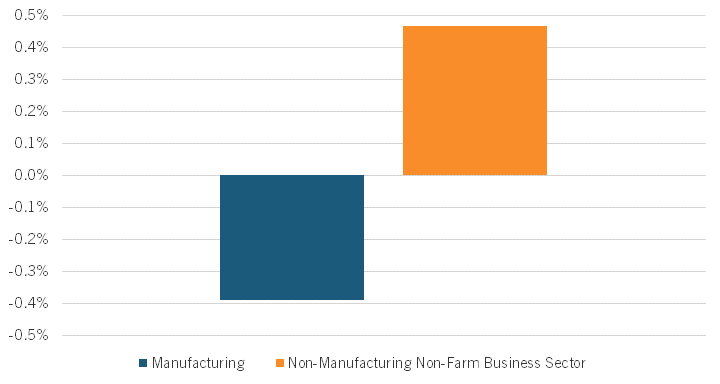

Productivity (measured in real output per hour of labor) in the manufacturing sector is lower today than two years ago. Between Q4 of 2020 and Q4 of 2022, manufacturing productivity declined by 0.4 percent, meaning more labor is required to maintain the same level of output. In contrast, productivity increased by 0.5 percent for the non-manufacturing, non-farm business sector. More generally, U.S. manufacturing productivity has been in a secular decline. Between 2011 and 2021, it fell by 2.8 percent after increasing significantly between 2001 and 2011.

Figure 1: Q4 2020–Q4 2022 labor productivity growth in the business sector

Sources: U.S. Bureau of Labor Statistics, Federal Reserve Bank of St. Louis (FRED), Author’s calculations

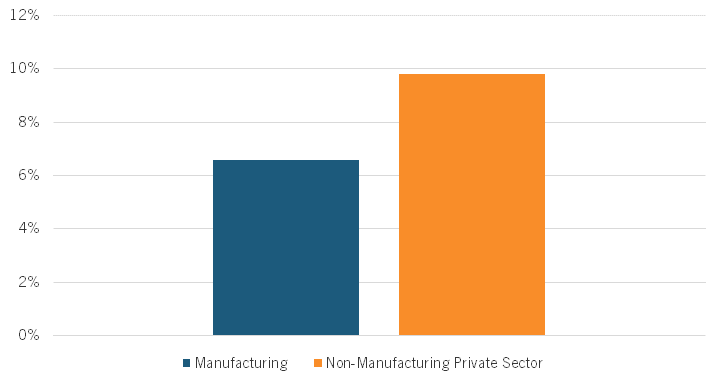

Moreover, job growth in the sector has been slower than that of the rest of the private sector. Between January 2021 and January 2023, manufacturing employment increased by 6.6 percent, compared to 9.5 percent for the non-manufacturing private sector.

Figure 2: January 2021–January 2023 employment growth in the private sector

Source: U.S. Bureau of Labor Statistics

Many point to this manufacturing job growth as a sign of success, and this job growth is certainly welcome. But while pointing to job growth might make for good politics, it makes for bad policy. Success in American manufacturing needs to be measured in productivity and the share of global value added in advanced manufacturing industries. Unfortunately, when measured this way, U.S. manufacturing fares much worse. As mentioned above, U.S. manufacturing productivity has been in a significant secular decline. The U.S. also lags behind other major advanced economies in measures like industrial robot adoption. According to the International Federation of Robotics, the United States ranked eighth in industrial robot density in 2021 (measured as industrial robots per 10,000 workers), behind South Korea, Singapore, Japan, Germany, China, Sweden, and Taiwan. The United States has also lost substantial market share and become less specialized in advanced manufacturing industries, as shown in ITIF’s Hamilton Index.

These dismal productivity numbers should be a wake-up call for the Biden administration and Congress. Since the nation’s founding, it is likely that manufacturing productivity grew faster than the overall economy for every five-year period (let alone ten-year periods). Something has gone wrong. Economists and policy advisors should be sounding the alarm, but this prolonged productivity slump receives very little attention.

If the nation does not turn around this manufacturing productivity “recession,” wages will grow more slowly, and U.S. manufacturing competitiveness will continue to decline. The result will ultimately be fewer jobs, a larger trade deficit, and a weakened U.S. advanced industrial base.

This is not the place to lay out a full manufacturing productivity agenda, but Congress should see this as cause for alarm and, at minimum, hold hearings on the causes and solutions. Specifically, Congress should take the following actions:

1. Institute a 10-year investment tax credit of at least 20 percent on new capital equipment and restore full first-year expensing for purchases of such equipment. Increases in new capital equipment drive innovation and are key to productivity gains. Lowering the after-tax cost of capital equipment will spur more of this much-needed investment.

2. Increase funding for the Manufacturing USA program by at least an additional $500 million per year.

3. Increase funding for the NIST Manufacturing Extension Partnership Program by at least an additional $500 million per year.

4. Significantly increase funding for the Advanced Robotics Manufacturing Institute, and give it the authority to fund R&D projects in industry and between industry and universities.

5. Establish a program at NIST to provide pilot grants for small manufacturers to automate parts of their production processes. In exchange for receiving funding, the companies would agree to share the lessons from their experiences with other U.S. small manufacturers.

6. Significantly increase the NSF graduate research fellowship program funding specifically dedicated to manufacturing and robotic engineering.

7. Establish the Industrial Finance Corporation of the United States to boost investment in key manufacturing industries such as semiconductors and advanced batteries.

Editors’ Recommendations

June 8, 2022

The Hamilton Index: Assessing National Performance in the Competition for Advanced Industries

April 5, 2012

Revitalizing U.S. Manufacturing

December 21, 2011