Reforming Merger Reviews to Preserve Creative Destruction

The neo-Brandeisian case for more aggressive merger reviews assumes that market concentration is out of control and enforcement has been too lax. Neither is true. Antitrust regulators should recognize that mergers can contribute to innovation, productivity, and competition.

KEY TAKEAWAYS

Key Takeaways

Contents

The Importance of the Correct Diagnosis of Economic Structure. 4

Market Concentration Has Not Increased. 5

The Importance of the Correct Diagnosis of Merger Law and Practice. 9

Merger Control Has Not Decreased. 9

Merger Laws Are Sufficiently Broad and Encompassing. 12

Merger Laws Capture Harms to Innovation. 14

Using Divestitures Is a Powerful Tool for Remedying Mergers 14

Merger Case Law Evolves in the Right Direction. 16

The Need Not to Return to Early Merger Cases 16

The Valuable Evolution of Merger Guidelines 18

Mergers and Innovation: Moving Toward a Dynamic Approach to Acquisitions 20

Reforming Merger Review: Industry Studies 21

Internet and Software Industry 21

The Biopharmaceutical Industry 23

How Not to Change Merger Review. 29

CALERA May Harm Innovation. 29

An Aggressive Merger Policy May Harm High-Growth Start-Ups 30

How to Reform Merger Review Under an Innovation- and Productivity-Centric Approach. 31

Develop Wide-Ranging Retrospective Merger Evaluations 32

Revise Merger Guidelines, With an Emphasis on Lowering Entry and Exit Barriers 32

Balance Blocking Mergers With Mandatory Licensing. 33

Increase Agencies’ Resources 34

Introduction

A core component of the Left’s “neo-Brandeisian” agenda to constrain and shrink large corporations is for agencies and courts to engage in more aggressive merger review.[1] Some have even called for prohibiting all large-scale mergers.[2] Many in the media have echoed these calls.[3] All that activism has resulted in Democratic proposals in the House and the Senate, as well as President Biden’s recent “Executive Order on Promoting Competition in the American Economy,” which call for tightening merger guidelines for antitrust agencies.[4] Moreover, under the leadership of Chairwoman Lina Khan, the Federal Trade Commission (FTC) recently rescinded its 1995 policy statement about past violations of merger laws.[5] The FTC also has withdrawn its approval for a set of vertical merger guidelines it issued jointly with the Justice Department in July 2020, and it has released findings of a new inquiry into acquisitions that the country’s five largest technology companies have made in the past but were not required to report.[6]

Contrary to the FTC’s new position, this report demonstrates how the 2020 Vertical Merger Guidelines were valuable and needed further improvements rather than being withdrawn rashly. This report also explains that competition concerns arising out of unreported acquisitions are largely exaggerated, given that the FTC itself has failed to demonstrate how the acquisitions it has pointed to as examples have reduced competition or harmed society by shutting down innovations.

Popular fears of merger mania—together with assertions that merger control has become too lax—regularly resurface in the public debate. Evidence nonetheless challenges common wisdom.

This impetus to limit mergers stems in large part from a new “anti-bigness” ideology held by neo-Brandeisians.[7] To justify their calls for limiting mergers, they assert, wrongly, that market concentration, profits, and markups have all increased because enforcement of merger law and rules has been too lax.[8] The majority of the antitrust community endorses an aggressive merger policy. Also, popular fears of merger mania—together with assertions that merger control has become too lax—regularly resurface in the public debate. Evidence nonetheless challenges common wisdom.

Popular fears regarding corporate buyouts are not new. In United States v. Pabst Brewing (1966), Justice Douglas appended a well-known column from humorist Art Buchwald in which the writer speculated that all U.S. companies would eventually merge into one giant corporation that would be large and powerful enough to actually purchase the entire United States. Fears of merger mania regularly gain prominence in popular opinion. Writing in The New York Times in 1985 about “the peril behind the takeover boom,” Leonard Silk lamented about “the biggest wave of corporate acquisitions and buyouts in American history beginning to cause widespread alarm.”[9] A decade later, Forbes would warn against the “dangers of global M&A,” and that “[many] … are looking at this process and worrying: ‘Won’t the wave of business concentration turn into an uncontrollable anticompetitive force?’”[10]

But what is different now is the widespread influence of the neo-Brandeisians, particularly in the Biden administration, and the widespread repetition of their misleading narrative about the purported rise of concentration, their focus on producer welfare, particularly smaller firms, and their embrace of the discredited prior structure-conduct-performance doctrine governing antitrust.

Although misguided and harmful, a return to the 1950s and 1960s’ approach to mergers advocated by neo-Brandeisians—wherein a greater number of mergers are rejected—could certainly occur under current rules. This call is, according to law professor Hubert Hovenkamp, a “disparagement of low consumer prices” for “harsh rules” but without a consistent test to reform merger analysis.[11] Hovenkamp has rightly cautioned against neo-Brandeisians’ ability to “denigrate the importance of prices to merger analysis.”[12] To be sure, prices are not the sole—or even the main—criterion for merger analysis. However, rejecting mergers because they generate efficiencies has proven to be a misguided approach antitrust agencies have justifiably rejected.

This report discusses the claims made by neo-Brandeisians that merger review requires a radical change of approach. First, the report scrutinizes and then debunks the claims being made in support of revising merger laws. Next, it examines case studies of mergers in the Internet and software, biopharmaceutical, and creative industries. Finally, the report formulates recommendations for merger analysis that follows a more dynamic approach to antitrust and recognizes that in some cases mergers enable not only increased innovation and productivity, but increased competition.[13] As a result, regulators can improve merger policy in the following ways:

1. Develop wide-ranging retrospective merger analysis: Antitrust agencies should systematically retrospectively evaluate past merger analyses so that discrepancies between predictions and reality could be used to better inform future merger analysis. To the extent the agencies need more resources for this process, Congress should provide the funding.

2. Update merger guidelines with a focus on lowering entry and exit barriers: As President Biden’s executive order calls for revision of both the 2020 Vertical Merger Guidelines and the 2010 Horizontal Merger Guidelines, antitrust agencies may seize this opportunity to ensure that merger control addresses concerns over artificially high entry barriers and blocking mergers occasionally increasing exit barriers for small companies at the expense of creative destruction.

3. Balancing blocking mergers with mandatory licensing: Instead of purely blocking mergers, antitrust authorities could remedy the most problematic mergers with mandatory licensing requirements. The merged firm could thus reap the multiple benefits of pooling resources while the antitrust authorities ensure that the market can utilize the nonexclusive licenses.

4. Increase antitrust agencies’ resources: Complex mergers involving companies in rapidly changing market environments as well as the need to engage in thorough post-merger analysis both justify in themselves increased resources for antitrust agencies to ensure greater accuracy of evidence-based merger analysis.

The Importance of the Correct Diagnosis of Economic Structure

If the performance and structure of the economy as it relates to industrial organization and structure were healthy, the case for significant change in merger law and regulation would be limited. Thus, neo-Brandeisian advocates of change base their campaign on a set of misleading analyses that, for the most part, have nevertheless become widely accepted as truth.

Market Concentration Has Not Increased

Calls for reforms of merger review are grounded in the belief that industry concentration has increased to problematic levels. President Biden’s executive order rests on the belief that “corporate consolidation has been accelerating” and that in over “75 percent of U.S. industries, a smaller number of large companies now control more of the business than they did twenty years ago.”[14] Biden declared that there is “less competition and more concentration that holds our economy back. We see it in big agriculture, in big tech, in big pharma. The list goes on. Rather than competing for consumers, they are consuming their competitors.”[15]

The antitrust community echoes the claim that market concentration has increased. Yet, market concentration has not substantially increased, as the concentrated industries in 2002 became less concentrated by 2017 (the latest year of available data from the Census Bureau).

The executive order reiterates the claim that concentration has increased, thereby denying “Americans the benefits of an open economy,” and widened “racial, income, and wealth inequality.”[16] Summoning just as much ammunition to support that claim, the administration also endorsed the faulty assertion that markups have tripled over the last few decades.[17] Allegedly, increased market concentration, higher profits, and higher markups signal lax merger review.[18]

Yet, claims that market concentration has increased to problematic levels remain largely unconvincing. For instance, in order to justify the executive order, which claims that the market has indeed concentrated, the White House referred to the study carried by Grullon et al. to conclude that “over 75 percent of U.S. industries” have consolidated over the last decades.[19] But the study defines industries based on NAICS (North American Industry Classification System) three-digit classification, which is unreliable as a measurement tool of market concentration and should not be used to generate policy decisions. Indeed, a 2020 White House Council of Economic Advisors (CEA) report debunks the use of two-digit NAICS sectors to measure market concentration, as used in the 2016 CEA report.[20] Indeed, “The Agencies and other economists often find evidence of robust competition in markets with only a few firms engaged in head-to-head competition. Thus, either the HHI … or a four-firm concentration ratio … would be more appropriate for a competition study.”[21]

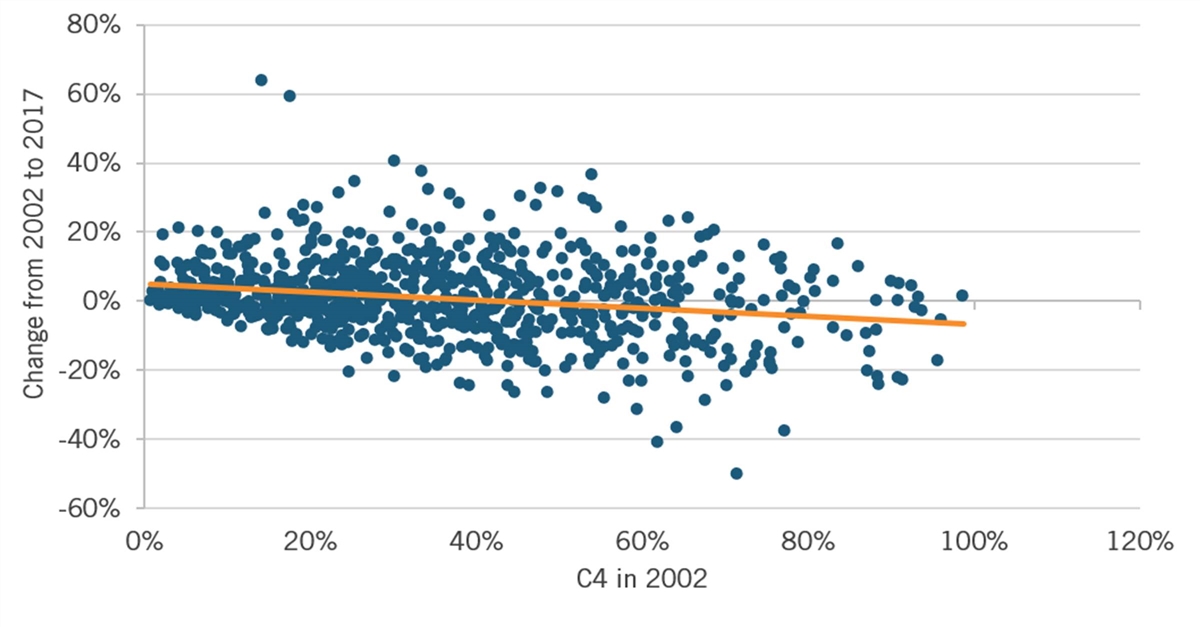

Census data shows U.S. industries have not become more concentrated: The average C4 ratio increased by just 1 percentage point from 2002 to 2017.

Accordingly, the Information Technology and Innovation Foundation (ITIF) carried out a market concentration analysis using the six-digit NAICS industries code for the C4 ratio (i.e., the top-four firms in each market).[22] The analysis uses the most recent data from the U.S. Census Bureau (namely, the 2017 Economic Census data released on December 3, 2020) and compares it with 2002 data.[23] As a result, the reality of market concentration trends stands in sharp contrast to the White House’s claims. Census data shows U.S. industries have not become more concentrated: The average C4 ratio increased by just 1 percentage point from 2002 to 2017.

Despite claims of widespread monopolization, just 4 percent of U.S. industries are highly concentrated, with the share of industries with low levels of concentration growing by around 25 percent from 2002 to 2017. The more concentrated industries were in 2002, the more likely they were to become less concentrated by 2017. In short, the widely accepted narrative that monopolization is increasing to crisis levels is not supported by the facts. Overall, the U.S. economy remains vibrantly competitive.

Figure 1: Relationship between C4 ratio in 2002 and percentage-point change by 2017[24]

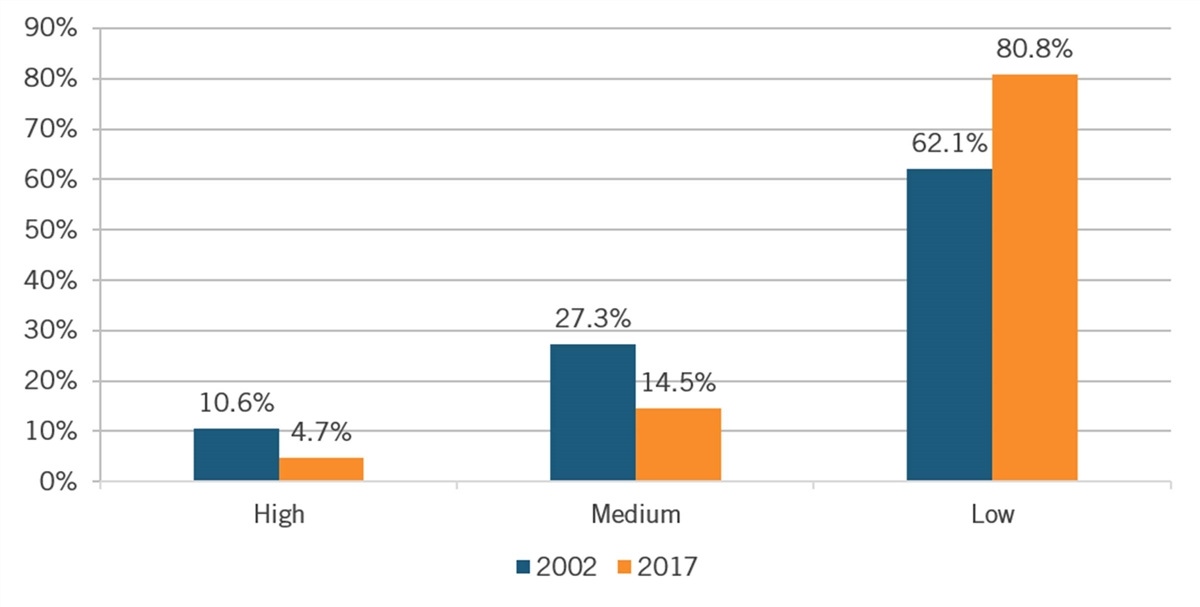

Interestingly, less-concentrated industries gained a larger share of the economy between 2002 and 2017:

Figure 2: Change in business output by C4 ratio classification as a share of the U.S. economy[25]

Overall, the C4 ratio for all 851 industries increased by just 1 percentage point, from 34 percent to 35 percent. This finding is consistent with many studies that find little to no increase in market concentration.

Likewise, if mergers have indeed been rampant, then the result should be seen in profits. Yet, as ITIF has shown, market concentration does not necessarily lead to higher profits, which means merged firms also face intense competition, thereby preventing them from reaping rapacious profits. Indeed, “there [was] no relationship between industry profitability and concentration ratio in 2017 (a correlation coefficient of 0.04).”[26]

Finally, one of the key problems with citing merger data is that this is the wrong unit of analysis. The right unit of analysis is mergers minus divestitures. While mergers are often front-page stories and complained about by neo-Brandeisians, divestitures are page 10 stories that are largely ignored—case in point being AT&T’s merger with Time Warner in 2018. At the time of the proposed merger, neo-Brandeisians called this a “Godzilla merger” that would lead to higher prices and profits.[27] Clearly, those profits did not emerge, which is why AT&T spun off Time Warner three years later, to little fanfare.

While full data on divestitures is difficult to come by, one OECD study finds that in certain years between 2008 to 2014, divestitures were greater than mergers and acquisitions among multinational firms. And in every year examined, the number of divestitures was at least 55 percent.[28] Moreover, another study estimates that the value of divestitures is around one-third that of mergers and acquisitions.[29]

Mergers Can Be Beneficial

Advocates of stronger merger review paint mergers as almost uniformly bad, with companies buying up firms to eliminate rivals and perhaps even create monopolies.

Yet, usually, companies merge in order to gain beneficial economies of scale or scope. Studies provide evidence of the overall beneficial aspect of mergers for economic efficiency and productivity.[30] For instance, when Disney acquired Pixar in 2006 for $7.4 billion, the acquisition of Pixar’s advanced animation technology enabled Disney to generate considerable value with a new sort of movie, which garnered consumer demand. In addition, the merger extended a 1997 production cost-sharing agreement between Disney and Pixar. It annihilated any legal disputes over this agreement that had arisen and impeded full synergies between the two film companies.

Google acquiring Android in 2005 for approximately $50 million created an effective competitor to Apple’s breakthrough innovation with the iPhone. With the acquisition of Aetna by CVS in 2018 for $69 billion, added health services in CVS stores contributed to reduced health care costs and increased access to these services for individuals. In 1998, when Exxon and Mobil entered into a $73.7 billion merger agreement, the oil and gas industry anticipated further consolidation, which happened in 2016, when Royal Dutch Shell acquired BG Group to become the second-largest oil and gas company by market capitalization (after Exxon Mobil). The Exxon Mobil merger thus enabled the merged company to benefit from, and outperform the expectations of, scale economies. Indeed, Weston et al. wrote that “the initial synergies were estimated at $2.8 billion. As a result of rapid and effective integration of the two companies, Chairman Lee Raymond announced within 7 months of the completion of the merger that synergies of $4.6 billion had been achieved.”[31] These scale economies have greatly benefitted the merged company concerning its rivals, and proved to be a particularly decisive factor in Exxon Mobile’s global competitiveness.[32]

Historically, mergers have mostly contributed to the rise of more productive, innovative companies. Describing the historical role of horizontal and vertical integrations in rationalizing and consolidating corporations to compete and innovate more effectively (both domestically and globally), Alfred Chandler Jr. noted that “the modern industrial enterprise in the United States appeared after merger or acquisition. Leaders among the pioneers acquired or merged with competitors; and then they consolidated production facilities into plants of optimal size, established the necessary marketing networks, and recruited the managerial organization.”[33]

Yet, despite the capabilities building inherent to most mergers and acquisitions, neo-Brandeisians, just as Justice Brandeis himself did a century before, warn that mergers contribute to harmful market concentration, are inherently harmful, and do not generate beneficial economies of scale and scope. Matt Stoller, of the American Economic Liberties project, spoke for many neo-Brandeisians today when he tweeted, “I’m increasingly convinced the biggest con in business history is the notion of 'economies of scale.’”[34]

In reality, one of the most widely agreed upon points by industrial organization economists is that economies of scale and scope are real. This does not mean that all mergers increase them; it does mean that some do. This is why the market very well anticipates increased corporate performance by merged firms.[35] Mergers often generate increased productivity, which directly helps workers and consumers.[36] Mergers often increase the acquired company’s productivity thanks to more efficient use of capital and labor.

Moreover, mergers enable firms to adjust liquidities more efficiently. “Liquidity mergers” reallocate liquidity from liquidity-abundant firms to liquidity-lacking firms.[37] Liquidity-driven acquisitions foster capital circulation, thereby fostering broadening asset-reallocation opportunities.[38] Because of the efficiencies often generated by mergers (both for the acquirer and the acquired), mergers and acquisitions can create added value.[39]

The benefits many mergers generate led innovation economist Joseph Schumpeter to capture the transformational change these takeovers bring about. Indeed, in analyzing the “railroadization” of the U.S. economy at the turn of the 20th century, Schumpeter underlined these “liquidity mergers” when he wrote that “new types of men took hold of [the railroads], very different from the type of earlier railroad entrepreneurs.”[40] He also praised the economic benefits of mergers as conducive to innovations with his claim that “new units of control, new principles of management, new possibilities of industrial research, and, at least eventually, new types of plants and equipment [create] absolute optimum—namely, optimal economic equilibria.[41]

Finally, contrary to the narrative specifically related to so-called “killer acquisitions,” according to which large incumbents acquire small rivals to discontinue competing products, the reality is merger entities often have strong incentives not to discontinue the different lines of businesses from the merging firms.[42]

In summary, many mergers are beneficial, and the ones that are not are routinely prevented by regulators.

The Importance of the Correct Diagnosis of Merger Law and Practice

The economic argument to significantly limit mergers is flawed—but so too is the argument that U.S. merger policy and practice are deficient.

Merger Control Has Not Decreased

Advocates for fewer mergers argue that merger control has decreased, in addition to concentration having reached problematic levels. Unfortunately for them, this claim, too, does not hold up to scrutiny.

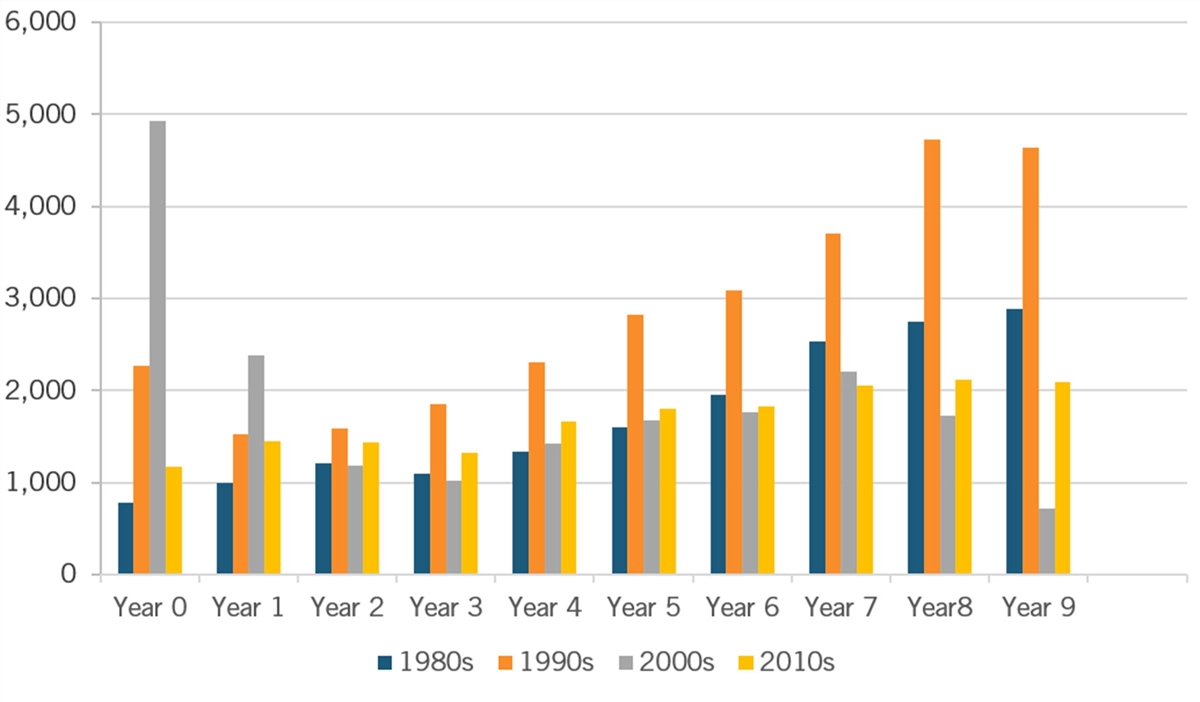

Figure 3 compares the reportable merger transactions from previous decades. These transactions are referred to as HSR merger transactions after the Hart-Scott-Rodino Antitrust Improvement Act of 1976, which obliges companies to file for merger approval by antitrust agencies whenever a proposed merger reaches certain transaction thresholds. Figure 3 also demonstrates that the decades of the 1980s, 2000s, and 2010s broadly followed the same pattern of HSR-reportable merger transactions. However, the decade of the 1990s saw an increased number of HSR-reportable merger transactions, with a particularly sharp increase in the late 1990s/early 2000s corresponding to the so-called “dot-com bubble” from 1997 to 2001.

Figure 3: HSR merger transactions reported per decade[43]

As figure 3 shows, the number of mergers reported in the 2010s pales in comparison with those reported during the 1990s and the first two years of the 2000s when another technological revolution (i.e., the “start-up bubble”) occurred. In other words, we are not in the midst of a merger wave, let alone an unprecedented one.

During both the 2010s and the 2000s, the number of mergers reported was lower and increased less than during the 1980s—a decade during which no major technological revolution took place. However, the fear that we are experiencing an unprecedented merger wave regularly resurfaces in the antitrust discourse. For instance, a 1948 FTC report worries about the merger movement “under way since 1940, [which] has resulted in the disappearance of more than 2,450 formerly independent manufacturing and mining companies. These firms held assets aggregating some 5.2 billion dollars or more than 5 percent of the total assets of all manufacturing corporations in the country.”[44] But, as Patrick Gaughan wrote, “These mergers did not result in increased concentration because most of them did not represent a significant percentage of the total industry’s assets. In addition, most of the family business combinations involved smaller companies.”[45]

Each cyclical rise in mergers arguably threatens to concentrate the economy and create unassailable monopolies. This selective perception ignores not only corporate divestitures but also new entrants that eventually become big.

During both the 2010s and the 2000s, the number of mergers reported was lower and increased less than during the 1980s—a decade during which no major technological revolution took place.

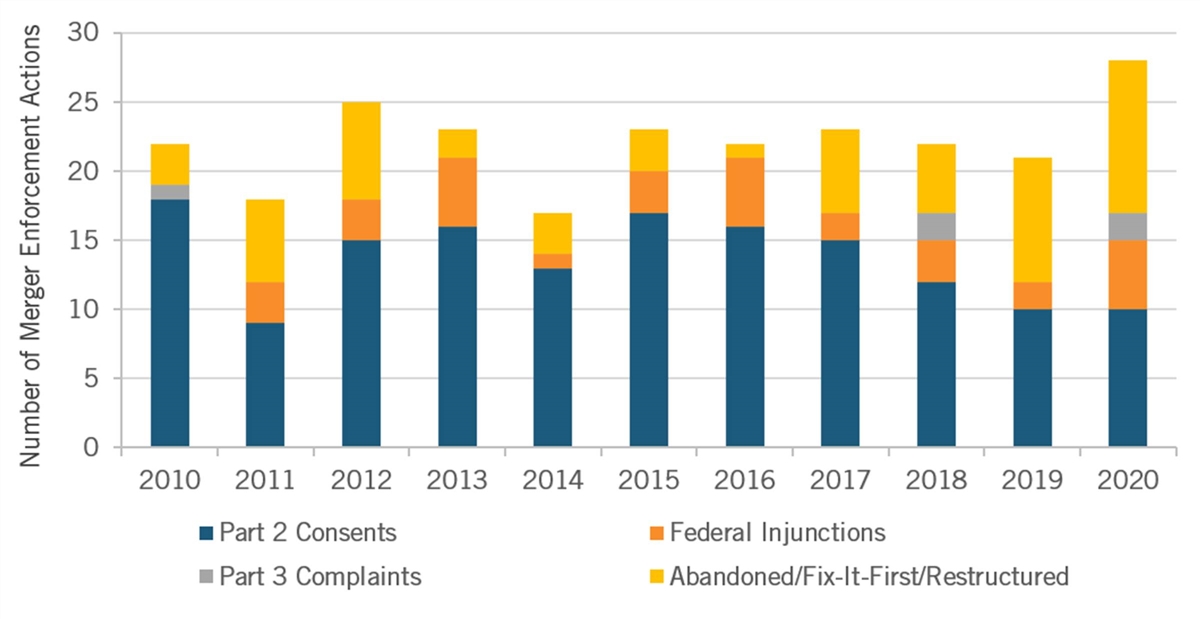

Another oft-made fundamental claim purports that lax merger enforcement enables market concentration. We tested the reality of this claim and found that merger enforcement actions remained stable over the last decade. Figure 4 examines four merger enforcement actions, namely Part 2 consents (e.g., negotiated settlements), federal injunctions (e.g., parties prevented from consummating a transaction), Part 3 administrative complaints (i.e., agencies’ challenge of a merger), or “fix-it-first” remedies (e.g., merger proceeds with modifications that preserve competition).

Figure 4: Total merger enforcement actions[46]

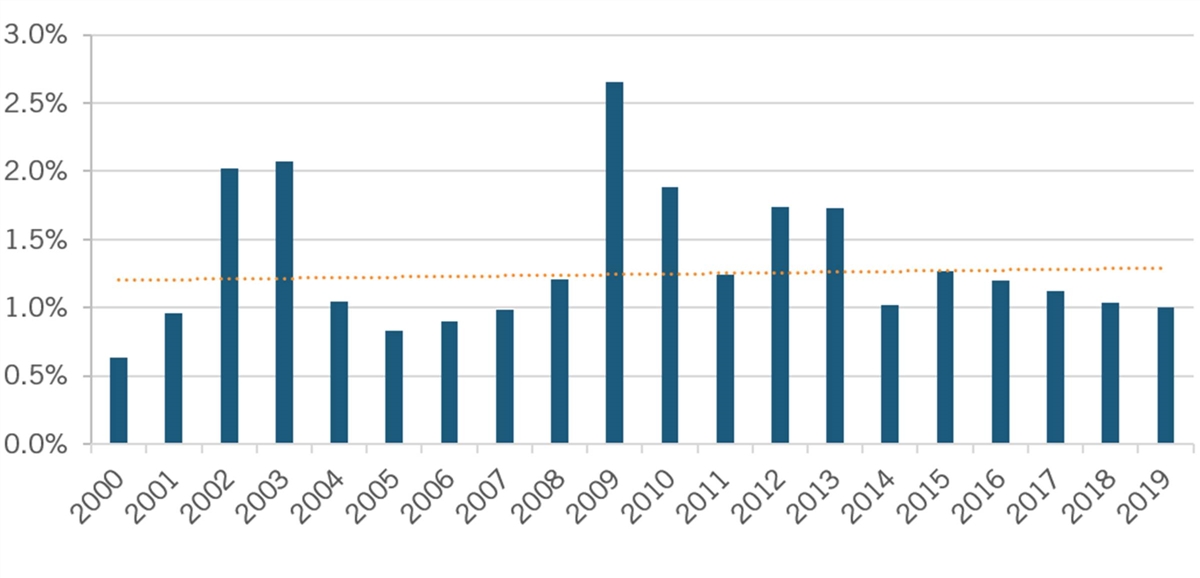

The data regarding the last decade of merger control reveals no lax enforcement or decline thereof. Figure 5 shows the yearly merger enforcement actions from 2000 to 2019 reported under the HSR Antitrust Improvement Act of 1976, or “merger enforcement intensity.”[47] The figure reveals that merger ratios increased post-recession and, on average, remained stable:

Figure 5: Merger enforcement intensity (enforcement actions as a share of HSR reportable mergers) [48]

These findings corroborate other recent studies, such as that of Macher and Mayo, which finds that, contrary to the prevalent narrative, “the Agencies [became] more likely to challenge proposed mergers over 1979–2017.”[49] Antitrust agencies have not fundamentally reduced merger control over the last decade; and recent studies also demonstrate that there is no under-enforcement in merger policy.[50] Merger enforcement actions grew steadily from 1979 to 2017, albeit with an unprecedented and sudden rise during the Clinton administration. [51]

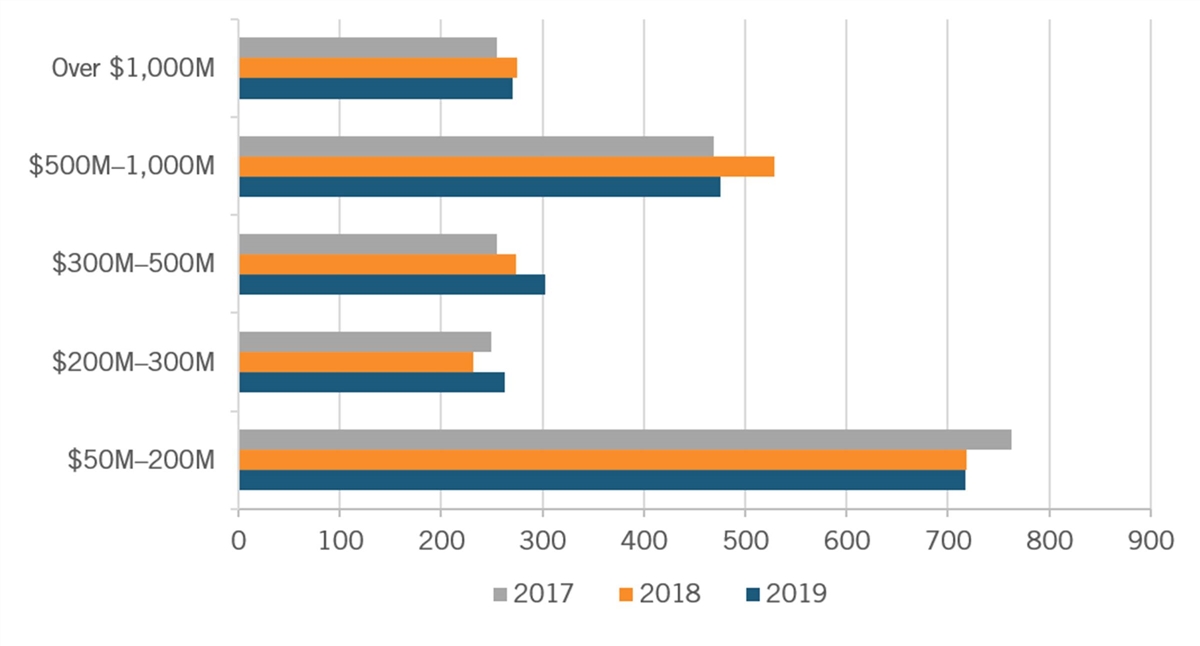

Finally, we evaluated the claim that antitrust agencies do not review killer acquisitions that go unreported and thus unchecked. (See figure 6.)

Figure 6: Number of HSR mergers reported according to the size of the transactions[52]

A large number of mergers indeed involve “small” transactions, namely those below $200 million, as shown in figure 6. Therefore, antitrust agencies also review small transactions, which thus do not go unreported, as some proponents of the killer acquisitions narrative argue.

Both the fear that we are currently experiencing an unprecedented merger wave and that small acquisitions go unreported seem exaggerated. Despite the lack of under-enforcement in merger policy, the general fear of under-enforcement the prevalent narrative relies on is simple: Current merger laws, including relevant case law, have become inadequate to address contemporary problems of market concentration.

Merger Laws Are Adequate

Proposals for new merger laws rely on the assumption that current merger rules are inadequate. Yet, merger policy changes can and do occur within existing merger laws and rules.

Merger Laws Are Sufficiently Broad and Encompassing

The Sherman Antitrust Act of 1890 remains a powerful tool, with Section 1 specifically applying to mergers.[53] Section 2 is particularly capable of addressing the rising concern over killer acquisitions, as illustrated by the Washington, D.C. Circuit Court’s decision in United States v. Microsoft Corporation (2001) ago that it “would be inimical to the purpose of the Sherman Act to allow monopolists free rein to squash nascent, albeit unproven, competitors at will, particularly in industries marked by rapid technological advance and frequent business model shifts.”[54]

The Sherman Antitrust Act is already capable of addressing concerns over killer acquisitions of nascent competitors. It is possible to “merge” innovation concerns within the Sherman Act’s main statutory provision for merger control—namely, the Clayton Antitrust Act of 1914.[55] Indeed, the main statutory provision for merger review remains Section 7 of the Clayton Act, which prohibits acquisitions wherein “the effect of such acquisition may be substantially to lessen competition, or to tend to create a monopoly.” The Celler-Kefauver Antimerger Act of 1950 prohibits companies from acquiring stocks for the sole purpose of reducing competition. It includes vertical and conglomerate mergers as part of the acquisitions prohibited under Section 7 of the Clayton Act.[56] Although that section originally aimed at preventing anticompetitive use of holding companies, it has become the key statutory provision for merger control by federal agencies.[57]

The Clayton Antitrust Act prohibits mergers that may monopolize the market and prohibits mergers that may lessen competition before the anticompetitive harm materializes. This has become known as the “incipiency doctrine.”[58] In other words, the Clayton Act requires the FTC to look into the future and predict which mergers are likely to lessen competition. Thus, this statute enables regulators to prevent monopolization before it arises.

The Sherman Antitrust Act is so broad that it is already capable of addressing concerns over killer acquisitions of nascent competitors.

Current rules and exemptions appropriately allow for addressing mergers adequately.[59] The HSR Act of 1976 established a premerger notification mechanism wherein firms willing to merge must notify antitrust agencies beforehand. Although a transaction may be reportable because it is above the thresholds, the merging companies may qualify for an HSR Act exemption. There are 25 categories of acquisitions that are exempt from HSR reporting.[60] In addition, the 2000 amendment to the HSR Act increases the exemption for deals to be notified from $10 million to deals whose target firms have assets under $50 million (and sales under $10 million for acquired firms in the manufacturing industry). These thresholds are annually adjusted. On February 2, 2021, the FTC announced decreased reporting thresholds under the HSR, given the U.S. gross domestic product’s (GDP) contraction in 2020. Accordingly, the FTC lowered the transaction threshold from $94 million to $92 million, meaning acquisitions below this threshold are reportable.

In light of the HSR Act, does the claim that some killer acquisitions go unreported hold water? It depends on whether killer acquisitions fall below the $92 million threshold. Yet, few if any acquisitions falling below this threshold are problematic for antitrust purposes.

Indeed, the oft-referred to instance of lax merger review is Facebook’s acquisition of Instagram in 2011. It is regularly argued that Facebook could have acquired Instagram without merger scrutiny.[61] But, as the acquisition was valued at $747.1 million it was thus not only reportable to the FTC but highly scrutinized by the FTC in conjunction with the United Kingdom’s Competition Authority (then the Office of Fair Trading).[62] With a 5–0 unanimous vote, the FTC considered that Facebook was a weak competitor in the mobile photo app market. Moreover, Instagram’s lack of advertising revenue constituted an opportunity for Facebook to compete with Google’s market position in the advertising market.[63]

Since current antitrust laws assess the potential lessening of competition from reported mergers, killer acquisitions of nascent competitors can only be unreported acquisitions because they are either exempt or fall below the $92 million threshold. Thus, the relevant question to ask is, Do these unreportable acquisitions lessen competition? Absent evidence, it is doubtful these transactions may lessen competition.[64]

Merger Laws Capture Harms to Innovation

The idea that some mergers, especially those falling below the HSR thresholds, may generate “harm to innovation”—meaning harm to the ability of the acquired firm to innovate absent the merger, and of rivals to innovate absent the appropriation by the incumbent firm of the acquired firm’s strategic assets—has recently been articulated. This harm-to-innovation argument follows the belief that current merger guidelines do not address this issue adequately. However, such a claim is erroneous since, as early as 1995, the Intellectual Property Guidelines, which apply to merger analysis, have defined “innovation markets” following the work of Richard Gilbert and Steven Sunshine:

[Innovation markets consist of] the research and development directed to particular new or improved goods or processes, and the close substitutes for that research and development. The close substitutes are research and development efforts, technologies, and goods that significantly constrain the exercise of market power with respect to the relevant research and development, for example by limiting the ability and incentive of a hypothetical monopolist to retard the pace of research and development.[65]

In other words, contrary to what policy advocates currently argue, antitrust agencies’ analysis fully considers alleged harms to innovation. The political pressure to tackle mergers would create a damaging drift between judicial analysis and the populist desire to de-concentrate the economy regardless of costs, including having an aggressive stance on all mergers.

Consequently, it is both unsurprising and sensible that the Antitrust Modernization Commission of 2007 considered, “No substantial changes to merger enforcement policy are necessary to account for industries in which innovation, intellectual property, and technological change are central features.”[66] But the report then contradicts itself by asking the antitrust agencies to “update the Merger Guidelines to explain more extensively how they evaluate the potential impact of a merger on innovation.”[67] The 2010 horizontal merger guidelines would later materialize this concern with a new section titled “Innovation and Product Variety.”

The political pressure to tackle mergers would create a damaging drift between judicial analysis and the populist desire to de-concentrate the economy regardless of costs, including having an aggressive stance on all mergers.

According to the Clayton Act, it cannot be assumed that unreportable acquisitions due to HSR exemptions lead to a lessening of competition. This is the de minimis exception according to which these mergers are so small that they generate minimal or no effect on markets and thus may not “substantially” lessen competition. There is, therefore, no need to alter the HSR exemptions. These acquisitions that are considered unreportable because the transaction sizes are insufficiently important raise the question of whether there should be a de minimis rule at all.

Using Divestitures Is a Powerful Tool for Remedying Mergers

Section 15 of the Clayton Act and Section 4 of the Sherman Act provide for antitrust officials to challenge problematic mergers with the imposition of several types of remedies. From blocking the merger (i.e., injunctions) to a “fix-it-first” remedy according to which antitrust officials allow mergers to proceed provided that modifications to the merger preserve market competition, current antitrust laws have various tools designed to capture potential harms to innovation from mergers. One of the most radical (yet preferred) tools is divestitures: Agencies and courts approve a merger subject to a company spinning off some corporate assets of either its own company or the target company’s assets. The Justice Department has recently updated its “Merger Remedies Manual” but has not changed it long-standing preference for divestitures (i.e., spin-offs) over conduct remedies (i.e., firms’ commitments).[68] Contrary to popular claims, the last decade saw increased scrutiny of merger control by antitrust agencies, especially regarding proposed divestiture buyers (i.e., the ability of the buyers of the divested assets to become an effective competitor of the acquirer).[69]

Divestitures not only represent an administrative requirement imposed as part of a set of remedies, they often represent a defensive corporate strategy that enables firms to reorient their efforts and assets in light of changing market conditions. Spin-offs of business assets indeed can constitute an opportunity for firms to increase shareholder value. Divestment strategies have increasingly become mainstream corporate strategies, as a report from Deloitte documents: 75 percent of the 1,000 U.S. companies surveyed were expected to pursue divestitures in 2020.[70]

In that respect, when considering the potential market concentration effects of mergers, it is also important to consider the potential market “deconcentration” effects of divestitures.[71] These effects are non-negligible since approximately two-thirds of the mergers over the last decade involved divestitures.[72] Indeed, waves of acquisitions portray similar waves of divestitures.[73] Moreover, the more acquisitions occur among unrelated lines of businesses, the more likely it is divestitures will eventually occur.[74]

In that regard, the distinction between “standard divestiture” (i.e., voluntary, market-based spin-off) with “regulator-mandated divestiture” provides policy implications for antitrust regulators: The acquirer is likely to receive a discounted value for the assets divested under regulator-mandated divestiture as opposed to the fair value acquirers receive for standard divestiture.[75] Such corporate asset devaluation needs to be considered by regulators as a deterrent factor for companies to merge. Consequently, although regulator-mandated divestitures entail a lower deterrent effect on mergers than a probability for regulators to block mergers, divestitures necessarily downgrade the valuation of the relevant corporate assets in the market.

Nevertheless, divestitures constitute a powerful tool for antitrust agencies to control mergers and address their concerns without necessarily blocking mergers that could be beneficial for consumers and innovation. Indeed, because the consent decree is prospective and avoids legal uncertainty and innovation costs generated with unwinding consummated mergers, divestitures should remain the preferred remedy for problematic mergers. In that regard, the recent decision for the 4th Circuit to allow for the first time a private party to successfully compel a divestiture of a consummated merger appears regrettable, as it generated heightened legal uncertainty and considerable costs related to unwinding the merger and of future mergers.[76]

In addition, conduct remedies run the risk of micro-management of dynamic companies by government officials in rapidly changing market environments. Divestitures address competitive concerns without complex litigations or regulations.[77] Indeed, the Justice Department rightly noted that “conduct remedies substitute central decision making for the free market. They may restrain potentially procompetitive behavior, prevent a firm from responding efficiently to changing market conditions, and require the merged firm to ignore the profit-maximizing incentives inherent in its integrated structure.”[78]

Current merger laws, operating under a general and much-needed rule of reason, thus appear well suited for the challenges of today’s economy. Unfortunately, it could be argued that the current application of the rule of reason to merger review won’t last, as experts have predicted the return to per se liability and legal presumptions against mergers.[79] This prediction appears to be materializing, with legislative proposals suggesting a de facto ban on all mergers for a handful of companies, or strong legal presumptions, which will constitute insurmountable obstacles to many mergers. The two main proposals are the bill introduced by Sen. Amy Klobuchar (D-MN), the Competition and Antitrust Law Enforcement Reform Act (CALERA), and the bill introduced by Rep. Hakeem Jeffries (D-MN), the Platform Competition and Opportunity Act.[80] Both bills propose the de facto banning of mergers altogether or introducing presumptions reminiscent of old cases widely criticized for their unintended effects on the economy.

Merger Case Law Evolves in the Right Direction

Current case law evolved out of past errors, when the so-called “Structure-Conduct-Performance” (SCP) paradigm, according to which market deconcentration would inherently increase market competition, dominated early merger cases.[81] Fortunately, the case law moved away from the SCP paradigm as the economic understanding of the relationship between market concentration and innovation improved. This section argues that the case law in mergers has evolved in the right direction—namely, toward a more-economic, less-presumptive approach.[82]

The Need Not to Return to Early Merger Cases

In the famous case of Brown Shoe Company, Inc. v. United States (1961), the Supreme Court considered that “if a merger achieving 5 percent control were approved, we might be required to approve future merger efforts.”[83] This was the first time the court articulated the incipiency doctrine—the idea that mergers should be blocked because they may prevent small firms from growing and competing. The incipiency doctrine resembles a precautionary approach to concentration. Over fear of increased consolidation, merger policy preemptively intervenes to block the merger before hypothetical harm materializes.

Consequently, following Brown Shoe, horizontal mergers are now deemed to violate Section 7 of the Clayton Antitrust Act. However, they involve exceedingly small market shares. Brown Shoe represents a merger policy designed to halt mergers for the sake of halting any concentration trend, not for achieving the objective of preventing anticompetitive mergers. Another instance wherein the Supreme Court articulated the incipiency doctrine was the case of United States v. Philadelphia National Bank (1963) in which the Supreme Court held that horizontal mergers conducive to merged firms holding less than 30 percent of market share could violate antitrust laws.[84]

This period was also when courts could decide that a merger made four decades earlier was illegal and had to be undone. Indeed, in 1957, the Supreme Court decided that E.I. du Pont’s 1917 acquisition of 23 percent of General Motors’ shares was unlawful because du Pont influenced General Motors’ choice of suppliers.[85] Forty-four years later in 1961, in a 4–2 decision, the Supreme Court ordered “complete divestiture” of the company, thus requiring E.I. du Pont to sell over the next 10 years of all the 63 million shares it owned of General Motors.[86] Economically severe and legally insecure decisions such as the United States v. EI du Pont de Nemours & Co. (1957 and 1961) need to remain past judgments, not inspirations for future cases.

An aggressive merger policy led to the blocking of such mergers as Brown Shoe, Philadelphia National Bank, and others because those mergers created efficiencies with a price reduction, not because of a lack of efficiencies.[87] The case law was tortuous and inconsistent, blocking small mergers with procompetitive effects. As Supreme Court Justice Stewart said, “The sole consistency that I can find is that in litigation under Section 7 [of the Clayton Act], the Government always wins.” But neo-Brandeisians advocate for a return to these cases and this consistency, for which the evolution of Merger Guidelines has reasonably ensured departure.[88] Indeed, the new FTC Chair Lina Khan, together with Vaheesan, wrote that “in the realm of merger law, the Supreme Court’s presumption in United States v Philadelphia National Bank should be reinvigorated…. [A] merger that created an entity with a share greater than twenty percent would have to show credible business justifications to overcome the presumption of illegality.”[89]

In other words, small mergers leading to merged firms that enjoy less than 30 percent market share should be presumptively illegal. To promote a “citizen interest standard” rather than the traditional “consumer welfare standard,” Khan and Vaheesan suggest not accepting divestitures or conduct remedies, and instead just blocking mergers.[90] This return to an aggressive merger policy would thwart necessary corporate consolidation as a way to innovate and compete. Moreover, the consolidation of suppliers or customers could weaken the bargaining power of dispersed firms.

Firms surely have to provide “credible business justifications” for merger review. But to enforce a presumption of illegality for mergers would deter consolidation for efficiency and innovation reasons, since the legal threshold is set too high. Applying the rule of reason to merger review proves to be the optimal standard for judicial analysis since neither defendants nor government officials should specifically have an easier burden of proof. Instead, both parties should equally have to demonstrate their arguments.[91]

The case law has moved away from presumptions (for or against mergers) for a good reason. Many mergers have been blocked or presumed to be illegal despite low market shares and procompetitive effects.[92] Presumptions of illegality as well as of legality are indeed not advisable.[93] A full-fledged, fact-finding inquiry must analyze the static effects (i.e., price and quality) and dynamic effects (i.e., innovation incentives) of proposed mergers.

Applying the rule of reason to merger review proves to be the optimal standard for judicial analysis since neither defendants nor government officials should specifically have an easier burden of proof. Instead, both parties should equally have to demonstrate their arguments.

Even advocates of presumptions in merger analysis, such as Steven Salop, recognize that a rebuttable presumption of illegality for mergers may create “false positives.”[94] For example, Philadelphia National Bank applied a presumption of illegality to “inherently suspect” mergers.[95] However, to apply such discretionary standards to today’s mergers involving complex economic considerations would leave doors open to arbitrary considerations. Thus, the long but secured move away from legal presumptions in merger analysis deserves consideration, not disdain.[96]

Economic analysis requires an open discussion without prejudices, biases, and a regulatory “quick look” preventing optimal decisions.[97] Economic analysis increasingly focuses on balancing pro- and anti-efficiency arguments, leaving less importance to the concern over concentration itself.[98] Since the FTC’s challenge to Staples’ merger with Office Depot in 1995, there is a renewed interest for more merger enforcement. However, economic analysis has remained essential throughout the evolution of merger case law.

While antitrust agencies rely on presumptions as adopted in Philadelphia National Bank, courts have relied on a test of economic reasonableness to mergers that assesses the pro- and anticompetitive effects of mergers using a more open, unbiased approach.[99] Thus, the judicial evolution of horizontal mergers gradually has rejected presumptions on mergers to avoid blocking procompetitive mergers.[100]

Importantly, the evolution of merger case law does not necessarily suggest that merger policy has evolved toward under-enforcement, contrary to some claims. Indeed, a recent study reveals that judicial standards have evolved in favor of a pro-enforcement tendency, thereby suggesting that the more-economically grounded standards have not led to under-enforcement.[101] Moreover, the valuable evolution of merger case law has accompanied another valuable evolution: the reviews of merger guidelines over time.

The Valuable Evolution of Merger Guidelines

Merger Guidelines have improved over time.[102] Indeed, the 1984 Justice Department Merger Guidelines, reissued jointly with the FTC in 1992, rationalized merger control with objective standards—namely, the Hirschman-Herfindahl Index (HHI).[103]

Although imperfect, the revision of the Horizontal Merger Guidelines in 2010 refined merger analysis to further align merger control with market realities.[104] The Guidelines also influence courts.[105] And they rightly reduce the importance of market shares as one of many relevant factors to consider in merger analysis.[106]

The Merger Guidelines address particularly well the issue of what would later be referred to as killer acquisitions. In Section 6.4, the Guidelines outline the concerns about mergers that may threaten competition by limiting “innovation and product variety.” Particularly, the agencies now evaluate “the extent to which successful innovation by one merging firm is likely to take sales from the other, and the extent to which post-merger incentives for future innovation will be lower than those that would prevail in the absence of the merger” and will also “consider whether a merger is likely to give the merged firm an incentive to cease offering one of the relevant products sold by the merging parties.”[107] Additionally, the Guidelines make clear that “the Agencies may consider whether a merger is likely to diminish innovation competition by encouraging the merged firm to curtail its innovative efforts below the level that would prevail in the absence of the merger.”[108]

Merger cases frequently involve concerns about the alleged harms to innovation. Indeed, Gilbert and Hillary Greene rightly noted that the “frequency of innovation concerns raised within mergers in high technology industries may indicate the Agencies are adept at challenging only mergers in contexts that are likely to harm innovation.”[109]

Acknowledging that “reductions in variety following a merger may or may not be anticompetitive,” the Guidelines thus appear well informed about the innovation concerns advocates of the “killer acquisition” theory articulate.[110] Consequently, it is dubious how a revision of the 2010 Guidelines to integrate these concerns is convincing since they are already addressed in the 2010 Guidelines. However, a revision of the Guidelines could clarify how agencies approach alleged harms to innovation in merger cases.[111]

In merger cases, the need for market definition diminishes as the dynamic analysis gains traction.[112] Market definition is already not required for unilateral effects in horizontal merger analysis.[113] More generally, a market definition in merger cases should play a considerably less-significant role. The 2010 Horizontal Merger Guidelines reduce, albeit insufficiently, the role of defining markets in analyzing mergers. Relatedly, the importance of market shares analyzed from a static perspective must become ancillary to merger analysis. As disruption inherently generates a massive increase or decrease in market shares, antitrust agencies must better assess mergers from a disruption perspective.[114] The particular concern over killer acquisitions may justify marginal changes to the antitrust doctrine under current laws.

Regarding vertical mergers, the 2020 Vertical Merger Guidelines were in line with the Antitrust Modernization Commission’s report, which, in 2007, considered that “the agencies should update the Merger Guidelines to include an explanation of how the agencies evaluate non-horizontal mergers.”[115] Thus, the Vertical Merger Guidelines issued in 2020 did not constitute a radical approach but rather better aligned the approach to vertical mergers with the one adopted to horizontal mergers since 2010.[116] Therefore, it is ironic that President Biden’s executive order asked antitrust agencies to revise the Vertical Merger Guidelines, despite the fact they had just been updated last year.[117] And it is highly regrettable that rather than preserving and improving them, the FTC has chosen the more radical and damaging approach of withdrawing them altogether.

The anticompetitive potential of vertical mergers is much smaller than of horizontal mergers.[118] This is because vertical mergers generate more measurable efficiencies than do horizontal mergers.[119] Also, because the contemporary concern over killer acquisitions rarely pertains to vertical mergers and more to horizontal ones, the law on vertical mergers ought not change.[120]

The particular concern over killer acquisitions may justify marginal changes of the antitrust doctrine under current laws.

In conclusion, we agree with the findings of the 2007 Antitrust Modernization Commission report, which states that “there is no need to revise the antitrust laws to apply different rules to industries in which innovation, intellectual property, and technological change are central features … no statutory change is recommended concerning Section 7 of the Clayton Act … current law, including the Merger Guidelines, as well as merger policy developed by the agencies and courts, is sufficiently flexible to address features in such industries.”[121] But the commission nevertheless recognized that “the agencies should update the Merger Guidelines to explain more extensively how they evaluate the potential impact of a merger on innovation.”[122] Accordingly, the 2010 Horizontal Merger Guidelines and the 2020 Vertical Merger Guidelines integrated these concerns.

The radical changes suggested in President Biden’s executive order may presumably not take place in favor of greater consideration for both the innovation incentives and the critical role of Schumpeterian competition in today’s economy. However, President Biden’s executive order suggests embracing the radical approach advocated by neo-Brandeisians to change our already flexible-enough merger laws. The often-praised 2010 Horizontal Merger Guidelines would be changed to revert to more structural approaches. The recently adopted 2020 Vertical Merger Guidelines would be suspended, thereby creating legal uncertainty at an unprecedented pace.

Mergers and Innovation: Moving Toward a Dynamic Approach to Acquisitions

With the technological revolution of the Internet in the 1990s, and more generally of capital-intensive innovators, the approach to mergers has become increasingly more dynamic.[123] The FTC’s review in 2004 of Genzyme’s acquisition of Novazyme marked the first time the outcome of a merger review was determined solely by innovation considerations.[124] The review scrutinized whether or not post-merger innovation incentives would lead to increased research and development (R&D) or improved efficiency of R&D expenditures. In the decision, the FTC ruled that the merger would enhance rather than hinder innovation. However, in 2009, the FTC determined that Thoratec’s proposed merger with HeartWare would not incentivize Thoratec to bring HeartWare’s left-ventricular-assist devices to market, and therefore rejected it.

Assessing the dynamic effects of mergers can be an extremely challenging exercise, especially when the entrepreneurs are wrong. Perhaps the best illustration of this is the 2018 AT&T/Time Warner merger. After fighting against the government to get the merger approved, AT&T announced its decision to spin off WarnerMedia and merge it with Discovery to create the content giant Warner Bros. Discovery—just three years after AT&T management had advocated for the original merger as being “the perfect match.”[125] A great dose of humility is not only necessary but essential to merger cases, especially in fast-changing environments with capital-intensive industries. The “innovation markets” may very well be the unpredictable markets within which government officials must make their predictions.

Relatedly, both the price effects and innovation effects of mergers are unpredictable. Indeed, when two drug manufacturers merge, the price effects on the drugs they sell often prove exceedingly difficult to predict—and less so the innovation effects. Would the merged entity close down some drug production lines, or would it rather expand the R&D capabilities of the acquired entity that has a greater drug portfolio? When two digital platforms merge, the price effects may be inconsequential if both platforms are already delivering ad-funded services at no cost to consumers. Would the integration be conducive to product innovations and entry into new adjacent markets?[126]

A great dose of humility is not only necessary but essential to merger cases, especially in fast-changing environments with capital-intensive industries. The “innovation markets” may very well be the unpredictable markets within which government officials must make their predictions.

Merger analysis invariably should consider the size of merged firms in light of the innovation dynamics.[127] One of these innovation dynamics depends on the ability of firms to appropriate innovation and R&D efforts. Indeed, weak appropriations support the Schumpeterian view that scale economies matter, with firms increasing their size and market share to compensate for weak appropriations.[128] Reversely, strong appropriation regimes (as illustrated by vigorous protection of intellectual property rights) help illustrate Kenneth Arrow’s theory that profits and market power may lower innovation incentives.[129] Correspondingly, as size increases, the need for appropriability to preserve innovation incentives decreases. Thus, a welfare function can theoretically lead to an optimal trade-off between a firm’s size and its level of appropriability.

These considerations, necessarily more qualitative than quantitative, increasingly become relevant for antitrust officials regarding price effects. The dynamic effects of mergers suggest less focus on market structure/concentration and price effects and more focus on the innovation dynamics and incentives to expand R&D capabilities (although innovation incentives are much broader than the R&D metric).[130]

This report presents three case studies of capital-intensive, rapidly changing industries wherein dynamic effects and global competition play a key role in constraining major actors: the tech industry, the pharmaceutical industry, and the creative industries, respectively. These industry studies support the recommendations we articulate in the last section of this report.

Reforming Merger Review: Industry Studies

This section briefly discusses key instances of merger control in the tech industry, the pharmaceutical industry, and the creative industries. It then focuses on the key claim that dominant players thwart competition by acquiring nascent competitors. In each case, we find that this claim is overwhelmingly exaggerated and that current laws are particularly adequate at tackling potential concerns.

Internet and Software Industry

Big Tech mergers are acquisitions that are seemingly harmful to innovation because they involve large tech acquirers buying innovative start-ups that are perceived as nascent competitors.[131] For example, Motta and Peitz have argued that virtually every Big Tech merger has been insufficiently scrutinized, including such prominent ones as Google/YouTube, Google/Waze, Google/DoubleClick, Facebook/Instagram, Facebook/WhatsApp, and Microsoft/LinkedIn.[132] As mentioned, antitrust authorities’ claim that contestable tech mergers go unnoticed is inaccurate, as agencies reviewed and cleared those mergers, often with remedies.

Whether referred to as digital platforms or by the popular moniker “Big Tech,” they in no way represent a challenge for current antitrust laws, and accordingly, cannot justify changes in antitrust laws. Indeed, Keith Hylton found that “there is nothing so unusual about digital platforms that would require a reform of the antitrust laws.”[133] Frequently, the characteristics of the tech industry prove useful for advocates of such reforms. Network effects, the winner-takes-all phenomenon, Big Data and algorithms, and their ad-funded zero-priced business models are unmistakable evidence that antitrust laws are ill-suited to address these issues. However, these arguments are flawed for at least two reasons. Other industries (e.g., telecommunications, advertising) also display some—if not all—of these characteristics. And even if the tech industry generates novel challenges for antitrust enforcement, antitrust laws are flexible enough to adapt. Indeed, companies as different as Standard Oil and Google face antitrust lawsuits under the same statutory provisions.[134]

Do tech mergers justify a change to the Clayton Antitrust Act? Do the tech giants create a “kill zone” or a “danger zone” against nascent competitors and innovators, whereby investments are deterred because of the existential threats created by powerful incumbents? Antitrust agencies are keen to identify this claim as justification for interventions.[135] ITIF has discussed at length the dubious claim that large tech companies create kill zones wherever venture capitalists refrain from investing in start-ups because Big Tech threatens to acquire them.[136] However, those acquisitions identified as problematic in academic papers and by the press have proven to be pro-competition overall, both serving consumers and helping those businesses enter new markets where tech platforms can topple traditional incumbents.[137]

Indeed, the claim that venture capitalists flee the tech industry wherever large digital platforms operate is unsubstantiated.[138] The specific study advocates of this claim often refer to is a widely “misinterpreted” blog post from Ian Hathaway.[139] Moreover, because of the relatively small impact of acquisitions by large tech companies, there is no evidence to suggest that these acquisitions impact the evolution of the venture capital markets.[140] Venture capitalists contest the fact that “kill zones” justify antitrust interventions.[141] Quite the contrary, “entry for buyouts” investments attract venture capitalists.

Thus, acquisitions of start-ups may not dry out investments, but rather attract them, as Gilbert explained:

Some firms are motivated to invest in R&D by the prospect of a buy-out. Venture capitalists invest in many high-tech start-ups with the expectation that, if successful, they will be sold to established companies. The pharmaceutical industry alone witnessed more than 1,200 mergers and acquisitions in the years 2014–2016, totaling more than $750 billion in aggregate total deal value. Some of these acquisitions may have eliminated potential rivals. But other acquisitions rewarded innovations that would not have occurred if the entrepreneurs could not sell their R&D assets or license their discoveries to established companies. Many of these acquisitions combine complementary assets, such as R&D, clinical testing, marketing, and distribution, which cannot be economically duplicated by either the acquiring or the acquired firm. A prohibition on acquisitions would discourage innovation, and consumers would be worse off if the number of discouraged discoveries exceeded the number of products suppressed by acquiring firms.[142]

Venture capitalists contest the fact that “kill zones” justify antitrust interventions. Quite the contrary, “entry for buyouts” investments attract venture capitalists.

Nevertheless, economists often use a baseline scenario to conclude that anticompetitive tech mergers are both oversimplified and limited, which can be summed up using Motta and Peitz’s assumptions:

In our setting, a start-up can develop a project that succeeds with some probability. Whenever the start-up has the ability to pursue its project, the merger will be anticompetitive. The acquisition then becomes either a “killer acquisition” or an upgrade with suppressed competition. The merger can only be procompetitive if the start-up would not be able to pursue its project absent the merger and if the incumbent will have an incentive to develop the project after acquiring the start-up.[143]

This approach reveals that whenever a start-up envisages merging, the merger may be presumed to be anticompetitive. Indeed, since any start-up is built to pursue and complete its self-assigned projects, the possibility for a start-up to merge may presumptively be prohibited, thereby considerably increasing its exit barriers and barriers to expansion. External growth represents for start-ups a major source of scalability at great speed and low cost. We can see from the baseline scenario that it is for the merging firms to rebut this presumption (“the merger can only be procompetitive if…”).[144] This rebuttal is made all the more difficult by the start-up having to demonstrate that it “would not be able to pursue its project absent the merger.”[145] This is virtually never the case. All start-ups create projects they can pursue independently. The real question is how to pursue the project most efficiently, not whether the project is pursuable.

To illustrate how this standard de facto leads to the blocking of tech mergers, let’s take two recent acquisitions frequently mentioned as evidence of inadequate merger enforcement: Facebook/Instagram and Facebook/WhatsApp. Would Instagram not have pursued its project (i.e., the Instagram app itself) independently absent the merger? Of course not. Instagram would have remained an unprofitable, low-investment, niche app without benefiting from the scale economies of Facebook and without turning into a shopping app and digital ad app capable of competing with other incumbents such as Amazon and Google. Would WhatsApp not have pursued its project (i.e., the messaging app itself) independently absent the merger? Of course not. WhatsApp would still have charged its customers for using its app rather than becoming the free messaging app it is today—but it would have certainly lived on.

Therefore, the question should not be whether blocking the merger would prevent the start-up from pursuing its project (since blocking mergers may, no matter what, lead to the project being continued differently). Instead, the question should be whether blocking the merger would prevent the start-up and the acquirer from developing specific capabilities essential for them to compete on the merits. If the merger would enable competition not on the merits, or if it would not lead to more innovation and instead harm competition, then stringent scrutiny of the merger by antitrust agencies would be warranted. Otherwise, creating specific capabilities and preserving the innovation incentives may suggest caution on the desire to block the merger.

Because of the efficiencies and innovation incentives inherent to mergers, current laws and merger guidelines capture the concerns raised by tech mergers, especially the so-called “killer acquisitions.” This term was originally coined for mergers in the pharmaceutical industry—an industry we now turn to.

The Biopharmaceutical Industry

Some pundits claim that the biopharmaceutical industry is excessively concentrated.[146] In reality, the concentration ratio of this industry is relatively moderate, as the top eight firms share 58 percent of the market—a percentage antitrust agencies consider unconcentrated.[147] Indeed, Atkinson and Ezell have revealed that “in 2006, the top 10 drug producers accounted for 56 percent of global industry sales, a number that fell to 43 percent by 2019.”[148] In 2019, the top four companies accounted for only 21 percent of global drug sales.[149]

Nevertheless, antitrust agencies are keen to scrutinize pharma mergers as a way of reducing pharmaceutical consolidation. The FTC in particular intends to do so under so-called “novel theories of harm.”[150] This vague concept is aimed at blocking mergers that allegedly would be harmful to innovation yet go unchallenged by antitrust agencies. Thus, the belief that antitrust agencies and courts rarely scrutinize acquisitions of nascent competitors, especially in the pharmaceutical industry, is false.[151]

Nevertheless, the influential idea that some mergers may harm innovation by causing the discontinuation of certain products mainly stems from a March 2021 University of Chicago Journal of Political Economy article by Cunningham, Ederer, and Ma titled “Killer Acquisitions” that scrutinizes deals in the pharmaceutical industry.[152] On the other hand, some authors consider that killer acquisitions are nothing new and should not generate new antitrust concerns beyond the existing framework because, according to Limarzi and Phillips’s article “‘Killer Acquisitions,’ Big Tech, and Section 2: A Solution In Search of A Problem,” in CPI’s Antitrust Chronicle, “[I]t’s hard (and somewhat futile) to say whether existing tools are fit to meet a problem without knowing whether that problem exists.”[153]

First, although the Cunningham, Ederer, and Ma article is widely quoted (primarily to justify aggressive merger enforcement), the discussion often overlooks some fundamental tenets of the article. For example, the authors considered that approximately 6.3 percent of the acquisitions they sampled were killer acquisitions—namely, mergers wherein the acquirer discontinued the acquiree’s products in an attempt to thwart competition.[154] The authors referred to Schumpeter and argued that killer acquisitions might “stem the ‘gale of creative destruction’ of new inventions.”[155]

Cunningham, Ederer, and Ma themselves acknowledge that product discontinuation may not necessarily be anticompetitive and anti-innovation. Indeed, less-efficient products can justify discontinuing the merged firm without harming both consumers/patients and innovation. Also, perfectly homogeneous drugs produced by both merging firms (either because of past imitation or the drugs having become standardized) may justify consolidation across business lines to reap the scale economies and network effects without harming consumers/patients and innovation. The authors cursively addressed this aspect in footnote 43, wherein, after having alleged that killer acquisitions reduce consumer surplus, they considered,

Although killer acquisitions reduce consumer surplus, they need not reduce social surplus under a welfare standard that weights consumer surplus and producer surplus equally. This can occur if the entrepreneur’s product partly duplicates development costs but does not provide sufficiently large increases in consumer surplus to fully compensate for the loss in producer surplus of the existing incumbents.[156]

In other words, assuming that the few identifiable “killer acquisitions systematically harm patients,” some killer acquisitions may be pro-innovation and pro-competition, as they enable efficiencies that increase net social welfare overall. Consequently, the authors wisely refrained from inferring welfare implications from the killer acquisitions phenomenon:

A comprehensive welfare analysis of the impact of killer acquisitions is, however, much more difficult, given the many different forces involved in the innovation process. In particular, such an analysis would have to quantify the impact on patient mortality, consumer surplus, technological spillovers from innovation, and ex ante incentives to generate new ideas. As a result, a formal welfare analysis is well beyond the scope of this paper.[157]

In other words, out of the approximately 6 percent of mergers identified as killer acquisitions, how many are welfare-decreasing and hence anticompetitive and anti-innovation? It is reasonable to predict that less than 50 percent of these killer acquisitions are potentially anticompetitive and anti-innovation, thereby confining this allegedly problematic phenomenon to an extremely marginal concern unworthy of altering merger law and enforcement principles?

Second, the authors referred to Schumpeterian competition but narrowed down the notion of innovation to product innovation (i.e., discontinuation of products that allegedly harm innovation). However, Schumpeter’s notion of innovation is fivefold: product innovation, process innovation, market innovation, supply innovation, and organizational innovation. However, the authors wrongly equated reductions in product innovation with reductions in overall innovation.[158] Reducing product innovation (i.e., shutting down a product line) not only does not mean rivals cannot develop a similar product, but, most importantly, it does not mean that the merged firm reduces overall innovation. Should, say, organizational innovation or supply innovation be improved, the merged entity may develop stronger innovation capabilities than the former two entities could independently of each other. For instance, let’s assume that two drug companies intend to merge. Company A produces a treatment, whereas company B produces the generic version of the same treatment. Arguably, the merged entity may have strong incentives to shut down the generic version of the treatment created by company B. Not only would it mean that other companies would still be able to enter the generic market company B once dominated, but most importantly, the reduced product innovation would need to be balanced against, say, the organizational innovation (e.g., cost efficiencies and enhanced capabilities) or the supply innovation (e.g., the acquisition of a valuable facility or marketable patents).[159] Unless the perspective on innovation is encompassing, the claims that mergers may harm innovation can only be truncated claims that partially portray the business dynamics.

It is important to remember that pharma mergers contribute to pharmaceutical innovation—a remarkable success of the U.S. pharmaceutical industry.[160] Contrary to the popular claim that pharmaceutical companies have diminished their R&D expenditures as a result of a merger wave, pharmaceutical companies have constantly increased (and improved) their R&D-to-sales ratios: From 2006 to 2018, this ratio increased by 11 percent, thereby suggesting a capital-intensive and knowledge-intensive industry competing through innovation efforts.[161]

Unless the perspective on innovation is encompassing, the claims that mergers may harm innovation can only be truncated claims partially portraying the business dynamics.

As empirical studies in the pharmaceutical industry reveal, size can be considered by far the most important contingency concerning the performance of firms.[162] Therefore, companies merge and then outperform their rivals due to having increased their innovation capabilities—although some mergers may temporarily reduce certain aspects of innovation. Still, dynamically, a firm’s reorganization will enable it to innovate in a more diversified or more focused portfolio of drugs.

The scalability gained by U.S. drug companies has enabled them to reinforce their innovation efforts further. Indeed, as Atkinson and Ezell wrote,

Drug companies in America are incredibly R&D intensive and have become even more so, with their R&D-to-sales ratio increasing from 11 percent in 2006 to 20 percent in 2018. The ratio for the top 20 U.S. companies increased from 15 percent in 2006 to 23.6 percent. Further, while drug revenues increased 56 percent from 2006 to 2018 (in nominal dollars), R&D increased by 85 percent.[163]

Pharma mergers may nevertheless deserve antitrust scrutiny, although the considerable innovation dynamics underpinning many of these deals suggest a workable antitrust framework. Professor Daniel Sokol has proposed such an antitrust framework for pharma mergers: “In the pharma setting, antitrust law needs to be careful to identify issues that killer acquisitions raise properly.”[164] In addition, there is a need for a strong evidentiary basis before envisaging blocking a merger. As Sokol noted, “Without theories backed up by actual facts, antitrust law will chill innovation as investors are scared off from backing the next generation of biotech ventures for fear of lack of exit options for founders and investors to reap the rewards of a successful exit.”[165] Such an evidentiary basis would involve two main issues:

▪ If the acquirer pays a lot of money and the target has already invested in the pipeline product (given it is already so advanced that is an actual threat to the acquirer), why assume the target will be killed, especially if there is at least some room for product differentiation (e.g., in anti-depressants)?

▪ How can we be sure the pipeline product would have become a significant constraint (i.e., the deal—assuming it will be killed—will lead to a substantial lessening of competition, given the internal sales forecasts are often overly optimistic?[166]

The recent focus on pharma mergers by antitrust agencies, such as the FTC’s multilateral working group and public consultation, ought to ensure that the lack of an evidentiary basis does not lead to blocking procompetitive and pro-innovative mergers.[167] In that regard, a retrospective merger analysis of past pharma mergers would shed light on general business dynamics, and factual instances in particular. We articulate such recommendations in the last section of the report.

It thus appears that the FTC does not need novel theories of harm to apply to a merger, let alone to pharma mergers. Not only does R&D keep strengthening at the industry level and need to be assessed on a case-by-case basis, but many cases in the past reveal agencies’ concerns over acquisitions of potential competitors well before the concept of killer acquisitions was formalized. Indeed, under the current approach, the FTC can effectively address killer acquisitions by alleging that the acquisition of a potential competitor may potentially stifle competition.[168]

Creative Industries

Creative industries are experiencing significant changes largely due to technological advancements.[169] For example, the music industry is not becoming digitalized—it is already a digital industry.[170] Or rather, the digital industry is a creative industry.[171] After all, tech platforms are part of the creative economy. Streaming platforms such as Spotify and Apple Music have become considerable forces alongside traditional music industry actors, accounting for two-thirds of all recorded music in the United States, and thus changing both industry business models and the relationship between label and artist.[172] However, although the economics have dramatically changed among music industry actors, record labels remain the key enablers for artists.[173]

Despite the disruption of the tech platforms, enforcers and experts often consider the music industry to be excessively concentrated.[174] Therefore, enforcers and experts want to de-concentrate the music industry, notably with a stronger merger policy. However, this intention begs two related questions:

▪ Is the music industry excessively concentrated?

▪ Does the industry concentration justify a more aggressive merger policy?

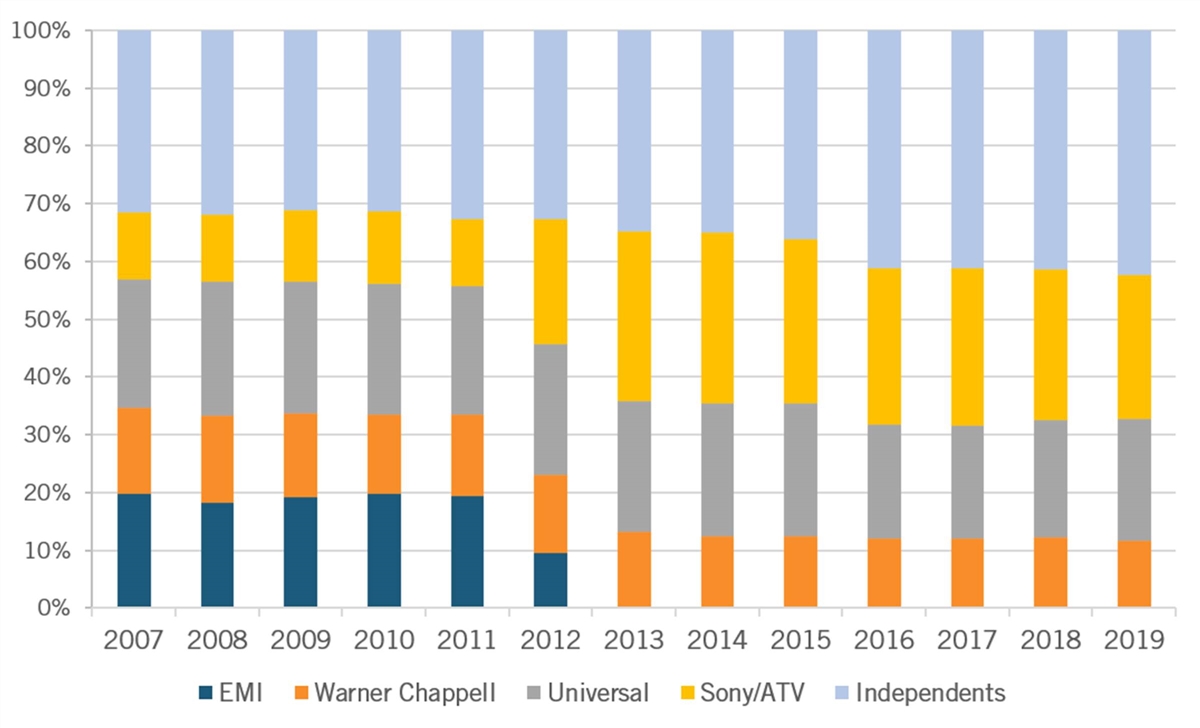

On the first question, the Independent Music Publishers International Forum argues that mergers and acquisitions in the music industry are bad for independent music companies.[175]In fact, the market shares of the four largest music publishers and record labels have fallen since 2007.

In other words, as figure 7 shows, the market shares of independent music publishers have grown significantly, and are hardly evidence of concentration problems. The digitalization and platformization of the creative economy in large part explain this underlying trend.

Figure 7: Revenue market share of the largest music publishers[176]

The U.S. Census data from 2017 reveals that the top four firms in the music publishing business (NAICS code 512230) increased their market share by just 1.6 percentage points, from 55.4 percent in 2002 to 57 percent in 2017—and it remains moderately concentrated today.[177]

In the related industry of sound recording studios (NAICS code 512240), the concentration ratio went from 9.7 percent in 2002 to 12 percent in 2017, showing that it is not concentrated.[178] Therefore, the music industry appears to be either not concentrated (i.e., the sound recording studios) or moderately concentrated (i.e., music publishers). In any case, concentration did not significantly increase from 2002 to 2017.

The second question on whether merger enforcement should be tougher in the music industry suggests that antitrust agencies have heretofore not scrutinized music mergers. Again, this is not the case. First, corporate consolidation in the music industry constitutes a key aspect of the risk-management tools available to major labels. Indeed, Passerard and Cartwright considered that