Crawford Misses the Mark

Susan Crawford has written an 8,300 word blog post defending her claims that American broadband is a second rate monopoly against criticisms of her facts, methods, and findings recently published as op-eds in the New York Times; it’s titled Responding to Distorted Op-Eds Published by the New York Times and is published in the Roosevelt Institute’s web site.

This is the first installment of a two part response; it deals with the technical claims Crawford makes for Fiber to the Home (FTTH,) her belief that the fastest network always wins (except when cable does) and a few miscellaneous observations. The second part will deal with Europe. So here we go.

While it’s remarkable to see such a lengthy response to a couple of 700 word op-eds, the more unusual feature of Crawford’s blog post is its use of actual research reports to bolster her claims; her book Captive Audience leaned on blog posts and articles from the popular press for authority, second- and third-hand sources at best, but the blog links to an FCC report, a European Commission report, and an OECD Communications Outlook report. If nothing else, my op-ed (and another by Verizon CEO Lowell McAdam) has forced Crawford to dig just a little deeper and consult some actual research. As we’ll see, her use of research data leaves much to be desired, but at least she’s making an effort rather than simply waving her hands, so that much is progress.

The Paranoid Style

Before Crawford gets to her research she makes the false and ridiculous charge that my op-ed was placed in the Times by the telecom companies: “Recently, the incumbent communication companies in America arranged for the publication in The New York Times of two op-eds (in a single week) claiming that America was doing just fine when it comes to high-speed Internet access.” This is a very bizarre allegation to make, and Times editorial staffers should be incensed at the accusation that they take their marching orders from the phone companies. It causes me to wonder why the Times previously published two op-eds by Crawford herself. Who “arranged” that?

My op-ed was written in response to an article by Times staffer Eduardo Porter that got all the key facts on broadband wrong and it was pitched to the Times without any help from outside ITIF. It’s astonishing that Crawford would make such a claim, as she is certainly in no position to verify it; the clear takeaway is that facts don’t matter to Crawford and other advocates who cultivate what’s been called “The Paranoid Style in American Politics.” All the claims I made in the op-ed are supported by the references in ITIF’s international broadband report, The Whole Picture: Where America’s Broadband Networks Really Stand, which is mentioned in my Times bio line. Broadband standings are a subject in which the facts matter more than mere suppositions about motives and processes.

Avoiding the Obvious

Crawford also refuses to discuss her reasons for citing Akamai’s Q4 2009 State of the Internet report to the effect that American broadband speed is 22nd in the world and declining; she discusses Akamai, but only to cast doubt on their current finding that we’re in 8th and generally rising. If nothing else, she might have explained why she once found Akamai credible and why she didn’t check their latest figures when preparing Captive Audience for publication. My op-ed specifically refers to this claim of Crawford’s because it’s one of the few sentences in Captive Audience that refers to a verifiable source; if I were rebutting an op-ed like mine, this would be the first thing I’d address, so this is a bit of a mystery, especially following her bizarre claim about telecom control of the Times opinion pages.

The Wisdom of John Malone

Crawford buries her argument underneath some thousand words of admiration for the business acumen of TCI Cable founder and current Liberty Media mogul John Malone, betraying a poor understanding of Malone’s business strategies. Malone heads an empire that includes holdings in satellite systems DirecTV and Sirius XM, cable systems, as well as TV programming and content plays such as Game Show Network and Starz, regional sports networks, the investment group Associated Partners, L.P., and a large piece of Barnes and Noble. Malone, the largest private owner of land in the U. S. (with 2M acres,) has made most of his money buying and selling companies, so we can’t reach too many conclusions on the bullish remarks he’s made on cable recently; he made similar remarks before selling TCI to AT&T and moving his cash into DirecTV, after all. In investing, actions – and their results – speak louder than words, and Malone is investing most heavily in cable systems in Europe, on the apparent expectation that cable has more to offer investors than heavily regulated DSL does.

That very well may be correct, but not for the reasons that Crawford likes. The value of cable in Europe is more a question of regulatory treatment than of technology, and it doesn’t bode well for Crawford’s “fiber everywhere” dream. Europe’s head telecom regulator, Neelie Kroes, is lobbying for a pan-European broadband market that would enable investors with substantial holdings in cable to thrive for a decade or more, especially as the EC has turned down Kroes’ request for major public investment in fiber. If you want to understand what Malone is doing, forget about Charter Cable and turn your mind to Europe.

Crawford doesn’t seem to realize that European cable operators are free to upgrade their networks all the way to 10 Gigabits per second whenever they want, while DSL operators can’t even go to 80 Mbps without regulatory approval (because of tariffs, loop reconfiguration and crosstalk issues.) The next step for DSL, G.Fast, will reach speeds of a gigabit per second, or close to it, but to mention that would confuse the narrative, so Crawford doesn’t touch it.

Networks Today for Applications of Tomorrow (Maybe)

Crawford’s claims about fiber supremacy are becoming more exaggerated. I don’t expect the typical law professor to rival the engineer’s understanding of technology, but it seems prudent for those who aren’t well versed in this area to refrain from making sweeping pronouncements. But just as Crawford pretends to know the dynamics of the New York Times’ editorial process, she claims to know things about fiber that no one else knows. For example, she claims that fiber differs from cable in two key ways:

- She claims only fiber can provide symmetrical connections with equal, upload capacity: “[Fiber] is objectively a better communications product than cable because it allows for symmetrical, equal uploads as well as downloads”; and:

- She claims that fiber provides each home with its own, unshared connection: “And a connection shared with the members of a single household will always trump a connection shared with an entire neighborhood. This isn't a question of legislation. It’s because of physics.”

In fact, the question of provisioning bandwidth between the upload and download paths is a network operator decision rather than a technology restriction. DSL can be symmetric or asymmetric; the name “ADSL” stand for “Asymmetric DSL” and “SDSL” stands for “Symmetric DSL.” In the cable realm, the operator can assign as much or as little capacity to the upstream side as they desire. In fact, real FTTH products such as Verizon’s FiOS are sold in both symmetric and asymmetric configurations as well. Since most Internet users download much more data than they upload, typical packages are asymmetric. But this is a pattern of network usage that engineers detected long before there was an internet. Dumb terminals on time-shared mainframes worked the same way, downloading 100 times more data than they uploaded.

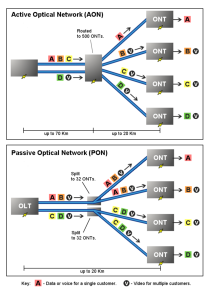

Similarly, fiber systems that use Passive Optical Networking (xPON,) such as Verizon FiOS, Google Fiber, and the Australian National Broadband Network, share bandwidth with an entire neighborhood, just as cable and wireless systems do. To understand how this works, consider the graphic from the Wikipedia article on PON:

[caption id="attachment_6184" align="aligncenter" width="420"] Wikipedia PON Diagram[/caption]

Wikipedia PON Diagram[/caption]

While it appears that each house has its own cable (from the standpoint of the house,) that cable merges with every other cable in the neighborhood at the passive splitter shared by 32 or 64 homes. This topology is exactly the same as for cable, which merges 100 – 400 homes across several splitters that ultimately share a single wire at the Cable Modem Termination System (CMTS,) a device that performs a service analogous to the OLT in the Wikipedia diagram.

Crawford is simply wrong about fiber vs. cable and wireless on these two points. Fiber is preferable to cable and wireless simply because fiber is more immune to environmental noise and thus is capable of supporting higher speed transmissions (it has more “bandwidth”,) not because of issues related to sharing and symmetry. She confuses the properties of a wire with the choices that network operators make about how best to use it.

Crawford’s appreciation of the value of bandwidth is also lacking. She repeatedly makes the claim that future applications will certainly require the high bandwidth that fiber offers today, but fails to realize that the applications of today work fine on most networks in most places anyway. The question for the supposed high bandwidth applications of tomorrow isn’t about the utility of today’s networks, it’s whether tomorrow’s networks will be able to support them at the appropriate time. Crawford confuses the time line with respect to bandwidth demands. As long as networks stay slightly ahead of applications, the interests of innovators and users will be protected.

Bandwidth is Nice, but so is Mobility

She also fails to appreciate the fact that bandwidth isn’t the only feature of networks that matters. Consumers are certainly sensitive to price, so there’s no compelling reason for them to pay the price today for capacity they may not be able to use for five, ten, or twenty years. Some of us will probably be dead before applications that consume more than 10 Gigabits per second are commonplace, and it’s only at that level that we can make an argument for the wholesale replacement of all forms of copper with fiber to the home. We should realize that DSL, cable, and wireless networks are hybrids of fiber, copper, and radio systems already, so the likely evolution of these systems is toward more and more fiber and faster radios until everything that can be done with fiber is done and the rest is handled by speedy radios.

Network users certainly place a great deal of value on mobility. All over the world (as well as in the U. S.) more people subscribe to mobile networks than to wired broadband. Mobility does things for us that no wire can do, and vice versa. Crawford grudgingly admits that mobile and fixed networks are “complementary,” but she clearly believes that fixed networks are superior:

The bottom line is that a mobile connection doesn’t compete with a wired one. These are complementary products, not competitive markets. At least 83% of Americans with smartphones also have a wire at home…The truth is that mobile wireless is complementary to wired connections - unless it’s all you can afford.

In fact, many mobile users consider their mobile device their primary communication vehicle, and several of the 17% of smartphone users with no wired connection at home simply don’t want or need one. Korea and Japan, two countries Crawford idolizes for their high capacity fiber networks, are seeing increasing numbers of users cutting the cord on high-speed fiber at home simply because they’re so comfortable with their mobile devices that they don’t want the complication of dealing with a second device and a second network. This trend is especially pronounced among young people with LTE smartphones:

Japan’s NTT is finding consumers are shifting demand from fixed networks to Long Term Evolution mobile networks, which is a real world test of whether LTE 4G networks can compete with fixed network high speed Internet access.

As a result, NTT has cut fixed network broadband access prices by 34 percent, from JPY5,460 (USD67) to JPY3,600, TeleGeography says.

You might say that price cut now shows there is serious evidence for the view that Long Term Evolution is a suitable replacement for fixed network service, with the greatest danger emerging where you would expect, with younger users.

While Crawford sneers at LTE as nothing more than a secondary connection, in the real world we’re learning that it’s quite good enough for many. It may well be the case that applications of tomorrow will need more bandwidth than the mobile networks of today can provide, it may also be the case that the mobile networks of tomorrow will be up to the task. However it turns out, it’s probably best to let the users make their own networking choices than to have them dictated by the whims of armchair engineers making policy pronouncements today. LTE and its successor LTE Advanced depend heavily on fiber backhaul, but that’s not the same kind of network as fiber to the home.

In fact, the Australian NBN that Crawford likes so much will only extend fiber to 93% of Australian homes; the rest will be served by LTE or satellite, simply because the cost of fiber everywhere is prohibitive despite its utility.

More Factual Errors

The bulk of Crawford’s blog post consists of attempts to rebut specific portions of either my op-ed or McAdam’s. I’ll address the comments she makes regarding mine (for obvious reasons.)

Crawford claims that FTTH, cable, DSL, satellite, and LTE don’t compete with each other. Her reasoning is quite doctrinaire. For instance, she claims that “Where DSL or cable is available, people don't subscribe to satellite Internet access services” because of their high price and latency. In fact, a relative of mine dropped DSL for satellite and is very pleased. His subsidized DSL was limited to 3 Mbps, but his new satellite connection runs at 15 Mbps. The satellite connection costs more, but it’s also less prone to interruptions, so he’s likely to keep it. So there’s one person who does prefer satellite to DSL, hence Crawford’s argument fails. I’m sorry she didn’t make a better one.

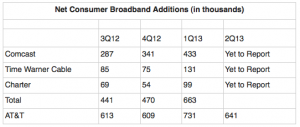

Crawford claims that DSL has no future: “Moving forward, most people think DSL will not be able to compete with cable or fiber, knocking telcos without fiber networks out of the marketplace and leaving us with just cable or fiber as our primary fixed-location competitors.” Yet the current market trends and future technology prospects undercut this belief. In the Whole Picture, we noted that short-loop VDSL (DSL with Fiber to the Node) is winning subscribers in the US faster than cable (page 37): 750K new adds in a recent quarter compared to 575K for cable. More recent reports find the trend is continuing:

Yet, if you take a look at broadband subscriber metrics over the past year, AT&T is outperforming all of the cable MSOs, by a long shot. AT&T is first to report 2Q13 numbers, during which they added 641K net broadband additions. If 2Q13 compares in any way to the previous three quarters, AT&T is crushing their faster cable competitors. For the past three quarters, AT&T has more broadband net adds than three of the top five cable MSOs of Comcast, Time Warner Cable, and Charter, combined (see table below).

- DSL vs. Cable Adds

Source: Company Quarterly Reports (compiled by telecompetitor)

Most, if not all, of those net adds are U-Verse broadband, considering AT&T (and Verizon) lose considerable legacy DSL subscribers every quarter. AT&T’s best U-Verse offer is 24 Mbps, for now anyway. That compares with DOCSIS 3.0 offers from their cable competitors that can range from 50 Mbps to 305 Mbps, on the high end. If higher speed broadband tiers are so important, how is it AT&T is adding more broadband subscribers than three of the top five cable MSOs combined?

So if DSL can’t compete with cable, why does telecompetitor say AT&T is “crushing” the cable companies? They offer the reasonable answer: “But for this moment in time, one could draw the conclusion that super fast broadband is not as an important as we may think it is.”

Perhaps the dynamic will change in the future – I suspect it will – but AT&T will probably offer services in the future that have more bandwidth than they do today. They always have, after all; and yes, Virginia, there will be more fiber in those future networks than there is in the networks of today.

Crawford makes a similar argument against mobile regarding the capacity constraints of today’s mobile networks vs. the supposed needs of the applications of tomorrow. I’d be more inclined to believe that mobile networks will grow faster than to believe that fiber networks will develop mobility. I suppose time will tell.

Crawford has some interesting observations about Europe that deserve a more lengthy response, but I’ll get to that in another post. This one is too long already.

Summary of Part 1

Crawford makes a serious attempt to forecast the future of communications applications and to posit the nature of the communications networks that will be required to serve the applications of the future. Oh wait, she doesn’t actually do that at all. Rather, she assumes that if all networks become faster as fast as they possibly can, fiber to the home networks will crush cable, DSL, wireless, and satellite across the board. This is a natural state of affairs, more or less like the withering away of the state as we enter the highest stage of Marx’ post-capitalist utopia. The only way this could fail to happen is for John Malone and his fellow Dark Lords of Cable to make cable so ubiquitous that no one has any appetite for investment in Fiber to the Home. Arguing for a particular future from the first principles of today’s technology is a good way to take a bath in the stock market, because things are never that neat. Ask the former shareholders of Global Crossing how that worked out for them when the company went bankrupt in 2000 after another fiber enthusiast, George Gilder, boosted its stock all the way to the poor house. (note: Gilder was a true believer, not a stock swindler; he lost most of his fortune along the way as well.)

The dynamics of today’s broadband marketplace cast doubt on Crawford’s prognosis, as we see in the rate at which fiber is being installed in the U. S. (faster than anywhere else in the world,) the rate at which LTE deployment encourages cord-cutting in high-fiber nations (so much that fiber operators have to slash prices in hopes of retaining subscribers,) and the rate at which fiber-intensive VDSL and Vectored DSL products take customers away from cable (significantly.) In fact, there is no prize for having the fastest technology in the world when several others are fast enough, some are cheaper, and some are mobile. As the saying goes, I don’t have to outrun the bear if I can outrun the other guy.

In the next installment we’ll compare the U. S. with Europe and see how Crawford takes liberties with financial data. It will be more fun than it sounds.